Chapter 14

Answers to Review Problems

Finance For Executives – 4th Edition

1. Exposure.

This problem illustrates one of the dilemmas facing multinational companies. It is

basically about changes in the valuation of a foreign subsidiary’s assets and liabilities,

how to report them in the consolidated accounts of the group, and ultimately whether

they can have an impact on share prices. With the current method (FASB52), presented in

Appendix 14.1, all assets and liabilities of the subsidiary are translated at the rate

prevailing on the date of the balance sheet. This means, other things equal, that if the

Is hedging a potential loss with a forward contract a wise decision? The idea of the hedge

is to make a gain on the forward contract that would offset all or part of the loss in value.

If the peso did fall 20% to peso 60 per USD, the value of the subsidiary’s equity would

fall to $41.67 million (peso 2,500 million divided by peso/USD60) producing a USD 8.33

million loss. Assuming a full hedge, pesos would be sold forward at peso/USD 53, and

the contract would show a gain of USD 5.5 million [peso 2,500 million divided by

peso/USD 60 less peso 2,500 million divided by peso/USD 53)]. This will produce a net

Another point to consider is the overall economic impact of a depreciation in the

subsidiary’s currency. If most or all of the subsidiary output is exported, the cheaper peso

should mean more sales and, consequently, higher profits. So if in the immediate future, a

2. Parity relations.

14-1

a.

Purchasing power parity says that changes in the exchange rate between two countries’

b.

According to the international Fisher effect, the difference in interest rates between two

c.

Interest rate parity says that changes in the exchange rate between two countries’

d.

3. Interest rate parity relation.

a.

The return on one USD deposit is:

b.

The return in USD on a dollar-covered euro lending is:

248.1)0315.01(

25.1

1

c.

If you borrow USD 1.00, you will have to repay US D1.03 in one-year time. The return

you will get from using this USD 1.00 to buy spot euros, placing them at the euro interest

4. Arbitrage activity.

14-2

a.

The arbitrage would be as follows:

Now:

2. Invest these dollars in a 90-day dollar time deposit at 3.125% p.a. The interest to

Since the risk from a fall in the value of the dollar has been eliminated by the forward

contract, we can calculate the arbitrage profit against the riskless alternative investment

b.

The forward rate can be derived from the interest rate parity relation (IRP). In Appendix

14.2, we show that this relationship implies the following:

f

h

fh

fh

r

r

S

F

1

1

0

/

0

/

or

f

h

fhfh

r

r

SF

1

1

0

/

0

/

where:

0

/fh

F

/fh

14-3

If the dollar interest rate were to suddenly increase by 25 bp (and assuming no change to

the spot rate or the yen interest rate), the forward rate should immediately rise to ¥110.88:

A B

14-5

Cells B1 – B6 are data.

Formula in cell B7 is =B1*B3.

The finance manager should invest the money in the United Kingdom.

b.

From equation 14.1

(

❑❑

❑

)

❑❑

❑

(

❑❑

)

(

❑❑

)

❑❑

❑

(

❑❑

❑

)

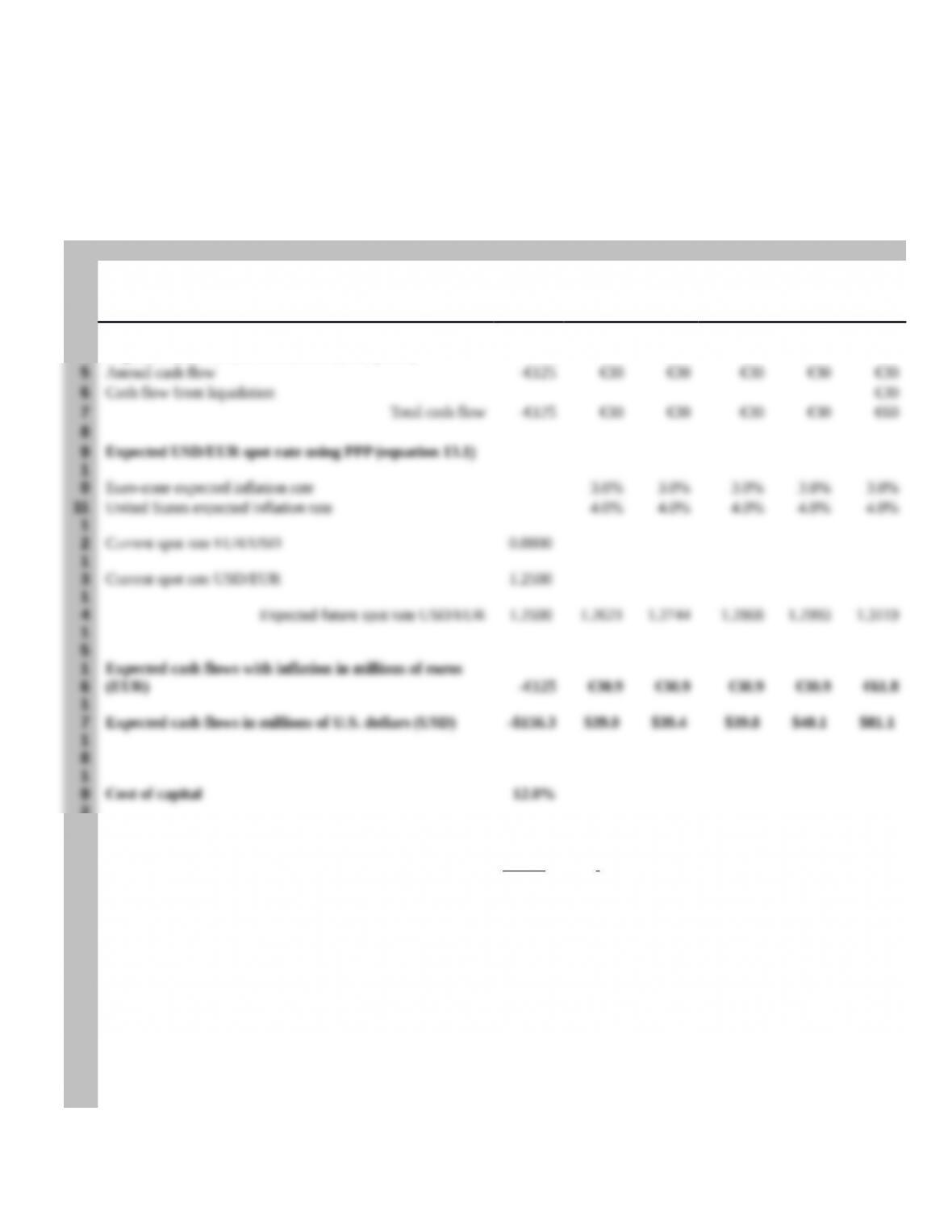

8. International capital budgeting (1).

14-6

The net present value calculation follows exactly the same approach as the one used for

Chapter 14’s Zap Scan project in Switzerland (Exhibit 14.3). The cost of capital is 12

percent (5 percent U.S. government rate plus 7 percent risk premium).

G: note that I replaced ‘End-of-‘ by ‘Year-end’ for consistency with the answers to the RP

of previous chapters

A B C D E F G

1Year-e

nd 1

Year-e

nd 2

Year-en

d 3

Yea-en

d 4

Year-e

nd 5

2 Now

3

4Expected cash flows in millions of euros (EUR)

2

0

2

1Net present value $9.782 million

2

2

2

3Rows 5, 6, 10, 11, 12, 19 are data

2

4The formula in cell B7 is: =B5+B6. Then copy formula in cell B7 to cells C7, D7, E7, F7, and G7.

2

5The formula in cell B13 is: =1/B12.

2

6

The formula in cell B14 is =B13. The formula in cell C14 is: =B14*(1+C11)/(1+C10). Then copy formula in cell C14 to cells

D14, E14, F14, and G14.

2

7The formula in cell C16 is =C7*(1+C10). Then copy formula in cell C16 to cells D16, E16, F16, G16.

2The formula in cell B17 is = B16*B14. Then copy formula in cell B17 to cells C17, D17, E17, F17, and G17.

14-7

8

2

9The formula in cell B21 is =B17+NPV(B19;C17:G17).

9. International capital budgeting (2).

a.

The minimum price that the owners of Chateau Cheval Noir should ask for the vineyard

is the present value of the cash flows expected from the assets of the vineyard. This is the

where EBIT is earnings before interest and tax, TC is the corporate tax rate, and WCR is

the change in working capital requirement. Since annual capital expenditures are

The following spreadsheet, which is a combination of the valuation spreadsheets used in

Chapter 12 and Chapter 14, shows how the net present value of the project can be

estimated.

A B C D E F G H

1

Year-e

nd

Year-e

nd

Year-e

nd

Year-e

nd

Year-e

nd

Year-e

nd

22010 2011 2012 2013 2014 2015 2016

3

1

14-8

4

1

5Residual value year-end 2015 in AUD $186.2

1

6

1

1

8Vineyard value in Australian dollars $146 million

1

9

2

2

6

2

7Residual value year-end 2015 in euros €78.2

2

8

2

3

1

3

2Rows 4 to 6, 17, 20, 21, 29, plus cells B7 and B8 are data.

3

3The formula in cell C7 is: =B7*(1+C4). Then copy formula in cell C7 to cells D7, E7, F7, G7, and H7.

3

4The formula in cell C8 is: =B8*(1+C4). Then copy formula in cell C8 to cells D8, E8, F8, G8, and H8.

3

5The formula in cell C9 is: =C8*(1-C5). Then copy formula in cell C9 to cells D9, E9, F9, G9, and H9.

3

6The formula in cell B10 is: =B6*B7. Then copy formula in cell B10 to cells C10, D10, E10, F10, G10, and H10.

3

7The formula in cell C11 is: =-(C10-B10). Then copy formula in cell C11 to cells D11, E11, F11, G11, and H11.

3

8The formula in cell C13 is: =C9+C11. Then copy formula in cell C13 to cells D13, E13, F13, G13, and H13.

3

9The formula in cell G15 is: =H13/(B17-H4).

4

0The formula in cell B18 is: =NPV(B17,C13:G13)+G15/(1+B17)^5.

4

1The formula in cell B22 is: =1/B21.

4The formula in cell C23 is: =B23*(1+C20)/(1+C4). Then copy formula in cell 23 to cells D23, E23, F23, G23, and

14-9

2H23.

4

3The formula in cell C25 is =C13*C23. Then copy cell C25 to cells D25, E25, F25, G25, and H25.

4

4The formula in cell G27 is: =H25/(B29-H20).

4

5The formula in cell B30 is: =NPV(B29,C25:G25)+G27(1+B29)^5.

b.

Why the higher discount rate for Australian dollar cash flows? One argument could be

that this represents the only diversification of the investors and that any favorable

portfolio effects this might bring them would be offset by the possibility of unforeseen

10. International Capital Budgeting (3).

a.

Project in China

A B C D E F G

1Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

Cash flows from China plant

Rows 2 – 5 and 9 are data.

The formula in cell B6 is = 1/B5.

The formula in cell B7 is = B6. The formula in cell C7 is =B7*(1+C4)/(1+C3). Then copy cell C7 to

14-10

next cells in row 7.

The formula in cell B8 is =B2*B7. Then copy cell B8 to next cells in row 8.

The formula in cell B10 is =B8+NPV(B9;C8:G8).

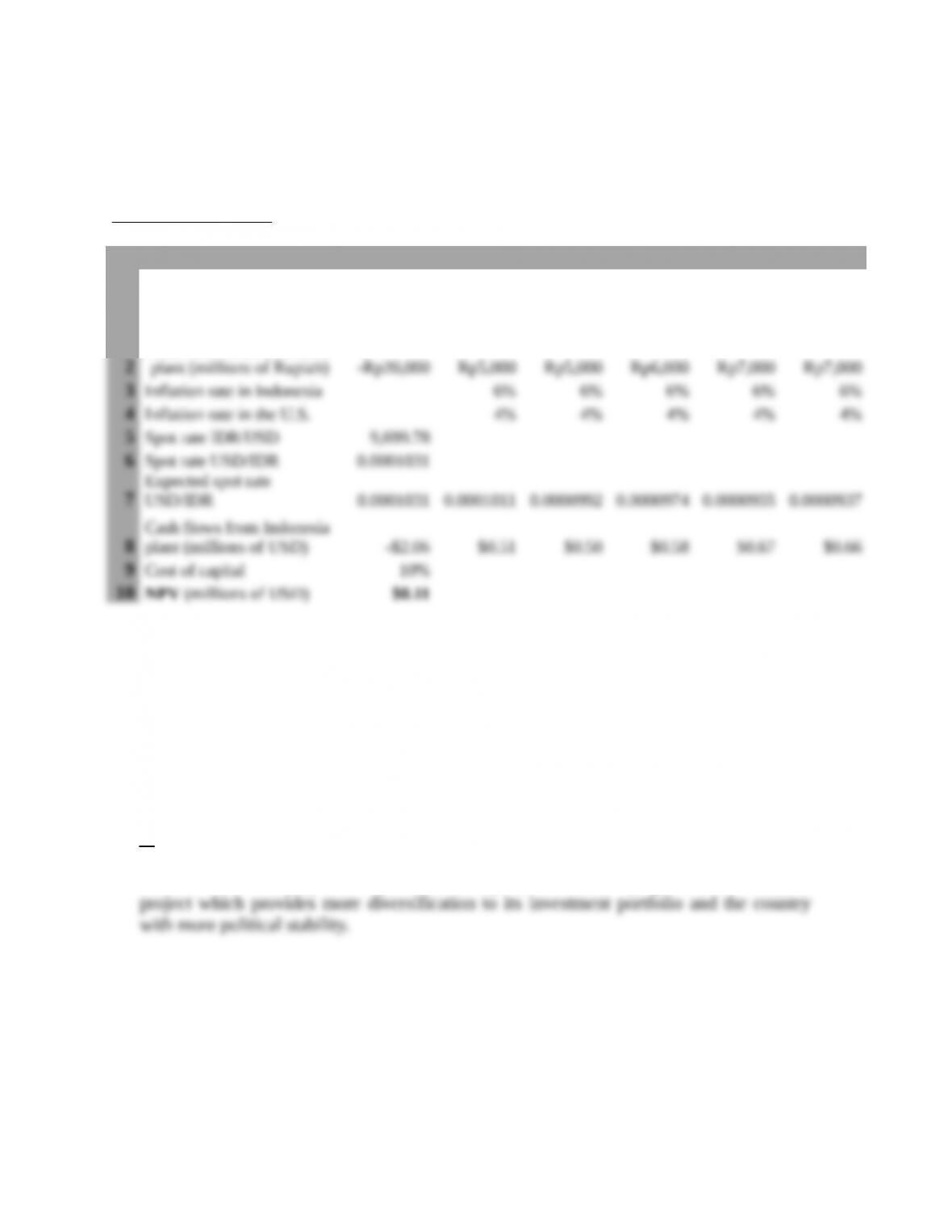

Project in Indonesia

A B C D E F G

1Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

Cash flows from Indonesia

Rows 2 – 5 and 9 are data.

The formula in cell B6 is = 1/B5.

The formula in cell B7 is = B6. The formula in cell C7 is =B7*(1+C4)/(1+C3). Then copy cell C7 to

next cells in row 7.

The formula in cell B8 is =B2*B7. Then copy cell B8 to next cells in row 8.

The formula in cell B10 is =B8+NPV(B9;C8:G8).

The U.S. company would choose the project in China because its NPV is higher.

b.

If the NPV of two projects are positive and equal, the U.S. company could consider the

14-11