Chapter 12

Answers to Review Problems

Finance For Executives – 4th Edition

1. Valuation issues.

a.

When the yield on government securities rises, equity investors require a higher return to hold

b.

For typical cash-flow streams, it is the present value of the cash flows expected beyond the 5- to

c.

In a leveraged buyout, debt financing provides more than valuable tax savings. It is also a device

to monitor management (more debt means more pressure on management to generate cash to

service debt and, thus, less wasted cash). And because management usually holds a relatively

2. Some issues in mergers and acquisitions.

a.

b.

Value can be created in a merger even in the absence of synergies if the management of the target firm

c.

d.

12-1

3. Leveraged buyout.

Value creation

Lower taxes from additional annual depreciation expenses resulting from the revaluation of

fixed assets

Value destruction

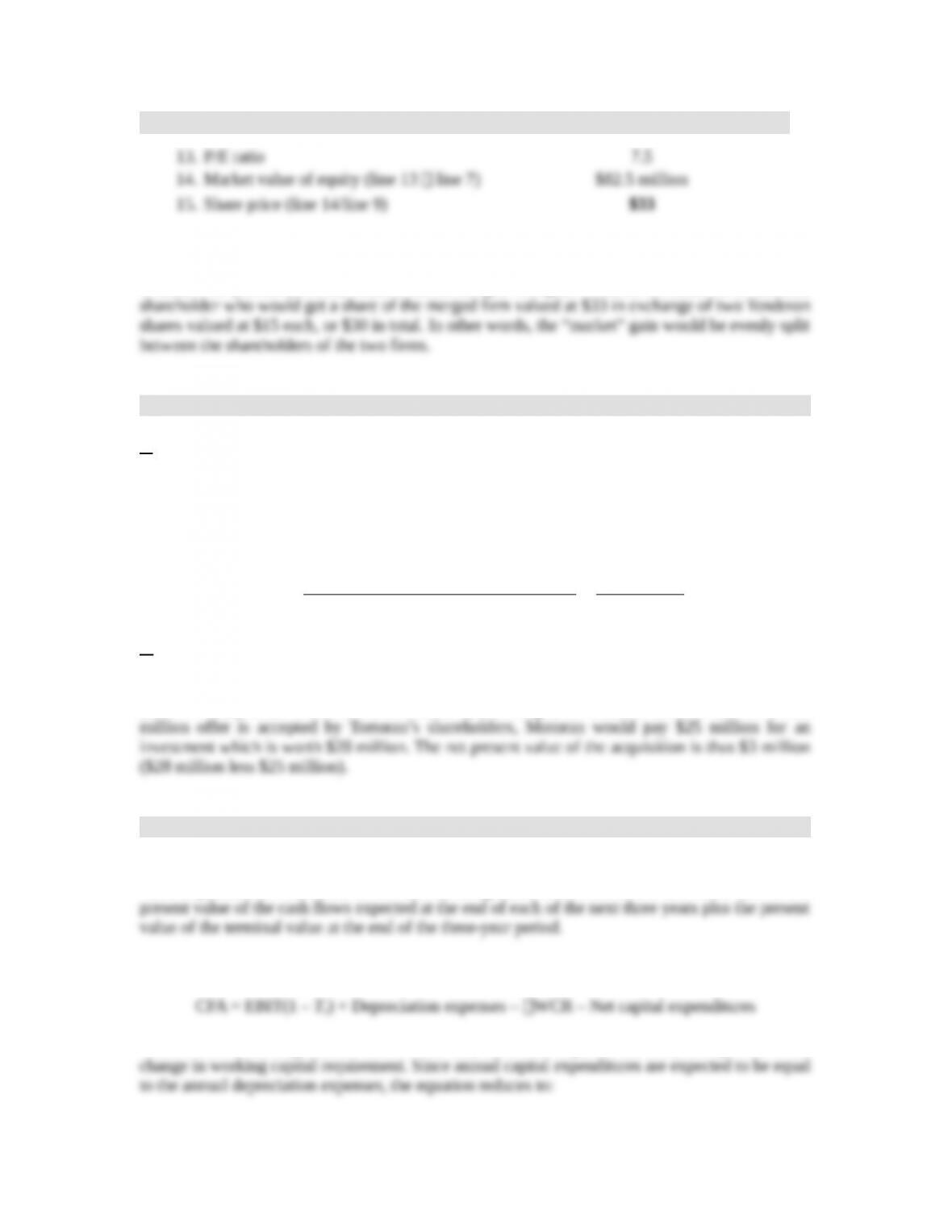

3. Mergers and price-to-earnings ratios.

a.

The maximum price that Maltonese should pay for the acquisition of Targeton is $60 million.

This is the value of Targeton standing alone—$45 million (1.5 million shares at $30 each)—plus

b.

The following table shows how the P/E ratio of the merged firm can be estimated.

Maltonese Inc. Targeton Corp.

Merged firm

12-2

9.Number of shares outstanding 5 million of outstanding Maltonese shares

+ .75 (1.5/2) million Maltonese shares to

issue = 5.75 million shares

4. Mergers and price-to-earnings ratios.

a.

The following table shows how the earnings per share, price-to earnings ratio, and share price of

the merged firms can be calculated.

Mergecandor Corp. Tenderon Inc.

Merged firm

Note that since the merger does not create any wealth gain, the net present value of the

transaction is zero. Further, since the exchange ratio is exactly equal to the ratio of the two

companies’ share price, there must not be any wealth transfer between the shareholders of

b.

If the P/E ratio of Mergecandor stays at 7.5 after the merger, we have the following:

12-3

Merged firm

At $33 a share instead of $30, there is a “market” gain from the merger of $7.5 million ($33 – $30

= $3 2.5 million shares). A Mergecandor shareholder would gain $3 per share held ($33 – $30),

or make a 10 percent ($3/$30) return form the merger. The gain would be the same for a Tenderon

5. Net present value of an acquisition.

a.

The amount of wealth created by the merger is the present value of the $1,000,000 savings on the

administrative costs of the two firms. This is the present value of a constant cash flow of

$1,000,000 at Motoran’s cost of capital of 12.5 percent and its value is given by equation 12.3

where the constant growth rate g is set equal to zero:

million8$

125.

000,000,1$

capitalofCost

savingsflowcashannualExpected

createdWealth

b.

If Motoran acquires Tortoran, it will get two things. First, the value of Tortoran standing alone

($20 million) plus $8 million of value created by the merger, for a total of $28 million. If the $25

6. Discounted cash flow valuation.

The minimum price that David Murlow should ask for his firm is the present value of the cash

flows expected from the assets of the firm standing alone. The value of the firm is the sum of the

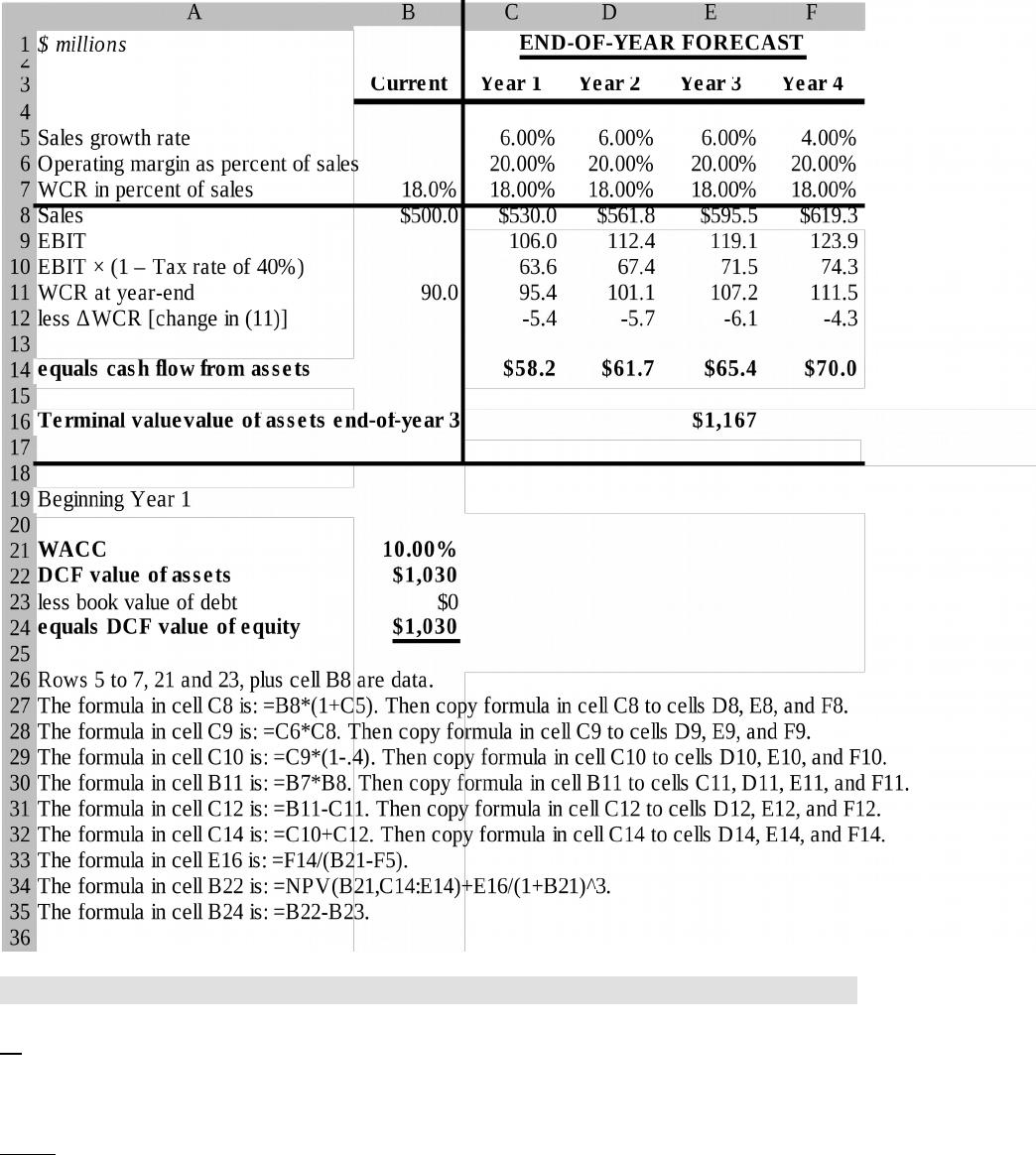

The cash flows from the firm’s assets (CFA) can be estimated from equation 12.5:

where EBIT is earnings before interest and tax, TC is the corporate tax rate, and WCR is the

12-4

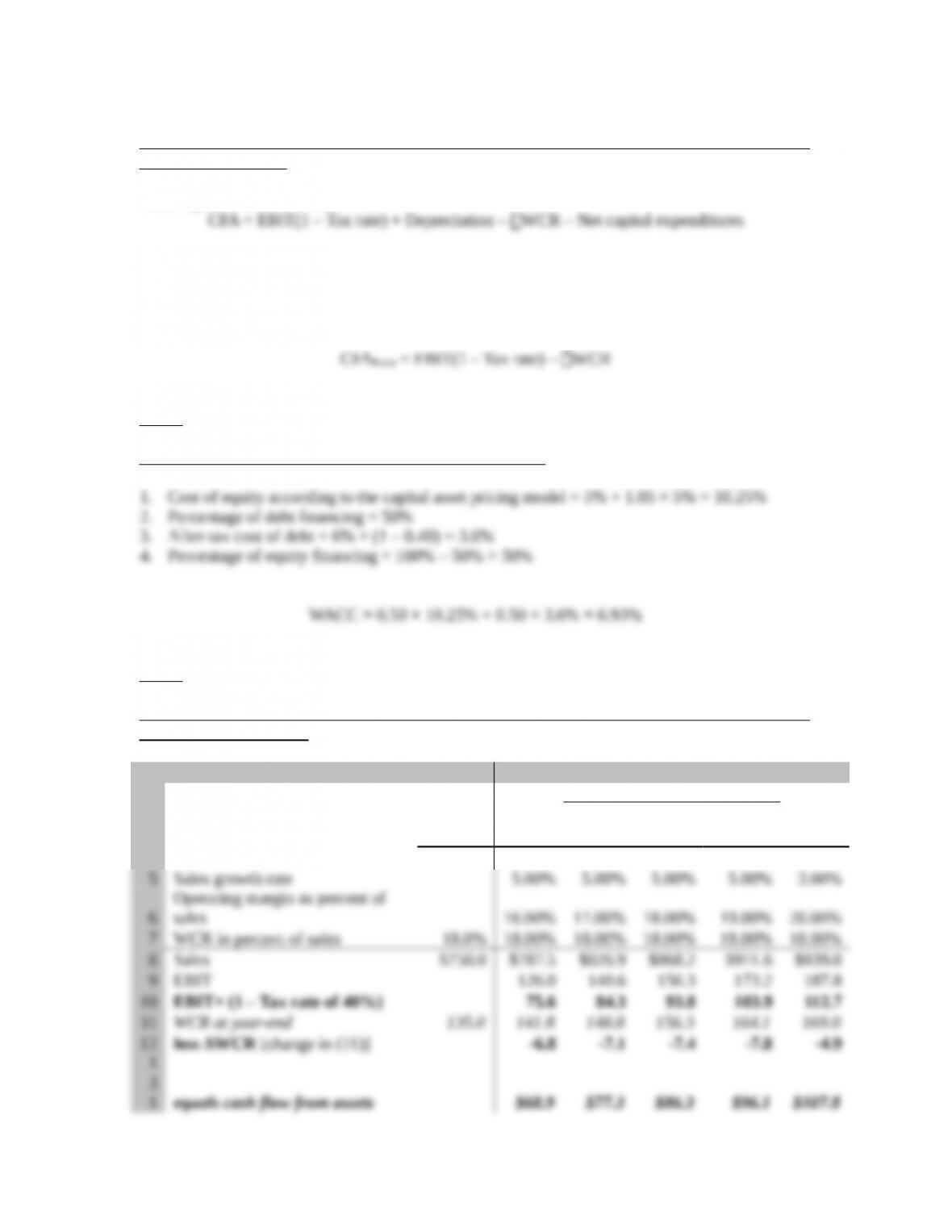

CFA = EBIT(1 – TC) – WCR

Using a spreadsheet similar to Exhibit 12.6 we can estimate the equity value of Murlow Company

as follows:

7. Discounted cash-flow valuation.

a.

Apply the following three-step method:

Step 1:

12-5

Provide a formula to estimate the cash flows from assets (CFA) that Portal is expected to generate

in the next five years.

From equation 12.5, we can write:

where EBIT is earnings before interest and tax, or pretax operating profit, and WCR is the

change in working capital requirement. But because annual capital expenditures will be equal to

annual depreciation expenses,

Step 2:

Estimate LMC’s weighted average cost of capital (WACC).

Step 3:

Using a spreadsheet similar to Exhibit 12.6 estimate the DCF value of Portal’s equity from the

forecasting assumptions:

A B C D E F G

1$ millions END-OF-YEAR FORECAST

2

3Current Year 1 Year 2 Year 3 Year 4 Year 5

4

12-6

4

1

5

17

18

1

9Beginning Year 1

20

2

5

26

Rows 5 to 7, and 23, plus cell B8are data.

27 The formula in cell C8 is: =B8*(1+C5). Then copy cell C8 to cells D8, E8, F8, and G8.

28 The formula in cell C9 is: =C6*C8. Then copy cell C9 to cells D9, E9, F9, and G9.

2

9The formula in cell C10 is: =C9*(1-.4). Then copy cell C10 to cells D10, E10, F10, and G10.

3

0The formula in cell B11 is: = B7*B8. Then copy cell B11 to cells C11, D11, E11, F11, and G11.

3

1The formula in cell C12 is: =B11-C11. Then copy cell C12 to cells D12, E12, F12, and G12.

3

2The formula in cell C14 is: =C10+C12. Then copy cell C14to cells D14, E14, F14, and G14.

3

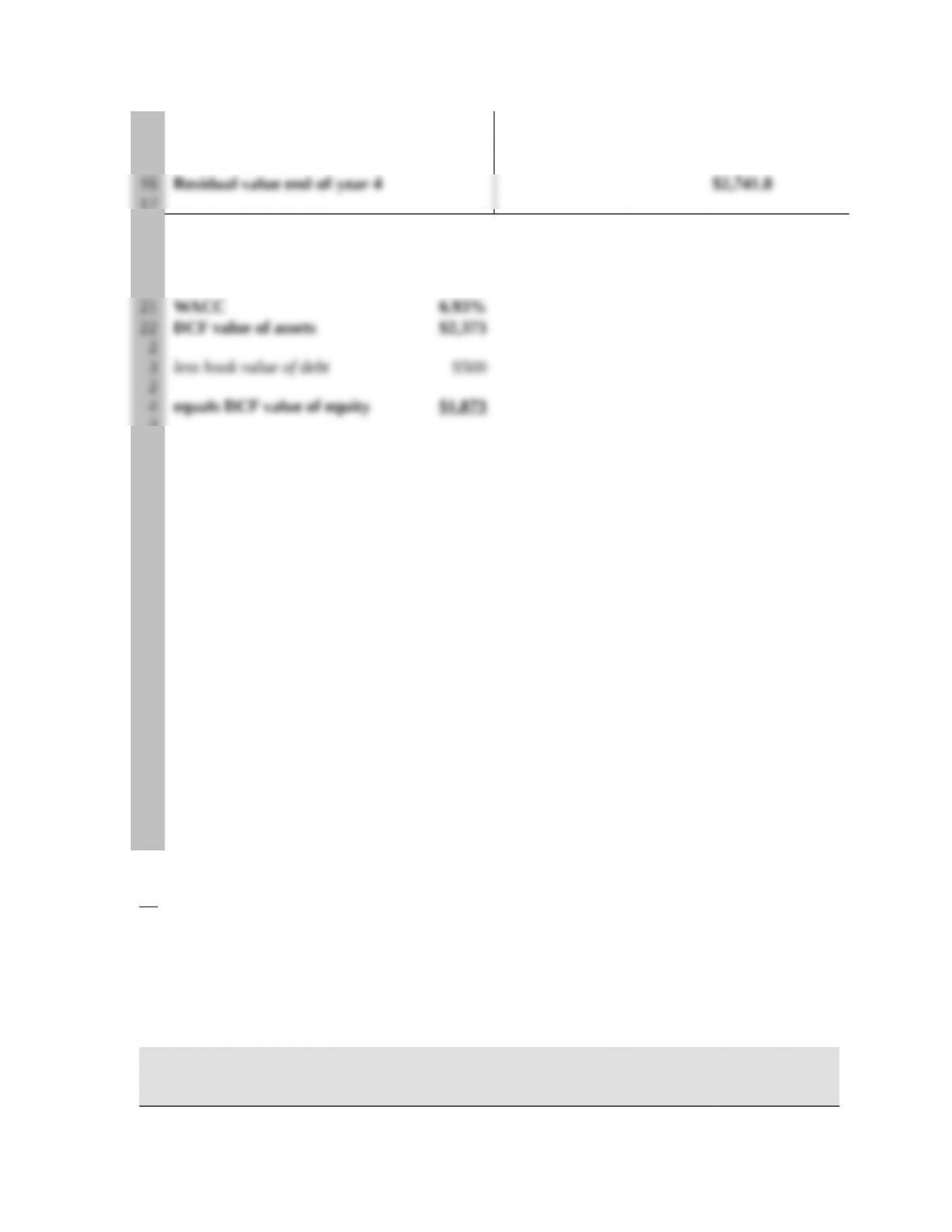

3The formula in cell F16 is: =G14/(B21-G5).

3

4The formula in cell B22 is: =NPV(B21,C14:F14)+F16/(1+B21)^4.

3

5The formula in cell B24 is: =B22-B23.

3

6

b.

To estimate the changes in equity value resulting from the suggested performance improvements,

simply modify the relevant data in the spreadsheet used in part a. To find the estimated amount of

value created, simply deduct $1,873 million, the DCF value of Portal’s equity without

improvements, that is its value “as is.”

Action

Expected Cash Flows from

Assets

($ millions)

New DCF Value Value Created

12-7

1 Terminal value at year-end 4

The sum of the changes in value resulting from each separate action ($703 million) is smaller

than their cumulative effects ($807 million) because combining the various actions reinforces

9. Alternatives to cash acquisition.

a.

From equation 12.3, where the constant growth rate g is set equal to zero, the discounted cash

flow (DCF) value of the $800,000 indefinitely annual increase to Osiris’ cash flow from assets is:

million10$

08.

000,800$

capitalofCost

increaseflowcashannualExpected

DCF Osiristo

Since the market value of Polos prior to the acquisition is $30 million, its value to Osiris when

accounting for the expected synergies is:

Value of the acquisition to Osiris = Value of Polos standing alone + Value of synergies

b.

After the acquisition, the market value of Osiris would be:

Osiris’ valuepost acquisition = Osiris’ valuestanding alone + Value of the acquisitionto Osiris

12-8

Under the exchange of shares alternative, the cost to Osiris would be 25 percent of its

c.

Under the exchange of shares alternative, the NPV of the acquisition would be the value of the

10. Cash or Stock offer?

a.

Mirandel’s share price, PMirandel, is the present value of an annuity equal to the dividend expected

for next year growing at a constant rate, g (5 percent), forever. Equation 12.1 and the appendix to

the chapter show that we can write:

gk

DIV

P

yearnext

Mirandel

where k is Mirandel’s cost of capital. From this relationship, we get:

g

P

DIV

k

Mirandel

yearnext

The following table shows how we can calculate Mirandel’s cost of capital using this equation:

b.

If Mirandel acquires Tarantel, the dividend would grow by 8 percent instead of 5 percent.

Applying the price formula from above, we get:

06.33$

08.129.

)08.1(50.1$

Mirandel

P

12-9

This represents an increase of $13.06 per share ($33.06 – $20). Since Mirandel has 2 million

shares outstanding, the value of Tarantel for Mirandel’s shareholders is $26.12 million ($13.06

c.

If Mirandel offers $50 in cash for each outstanding share of Tarantel, it will acquire Tarantel for

$25 million ($50 .5 million shares). The net present value of the acquisition would be $1.12

million ($26.12 million – $25 million). If it offers 756,000 of its shares in exchange of the

Whether Mirandel should make a cash or a stock exchange offer depends upon the following

considerations:

1. If Mirandel’s management believes that Mirandel’s shares are currently overvalued, the

2. If cash is offered to Tarantel’s shareholders, they would receive a fixed price. If the

merger is very successful, they would not benefit from the additional wealth created by

3. In a cash offer, Tarantel’s shareholders may have to pay capital gain taxes, while in a

12-10