151

P9.9 Complete an analysis for budget, price and volume variances.

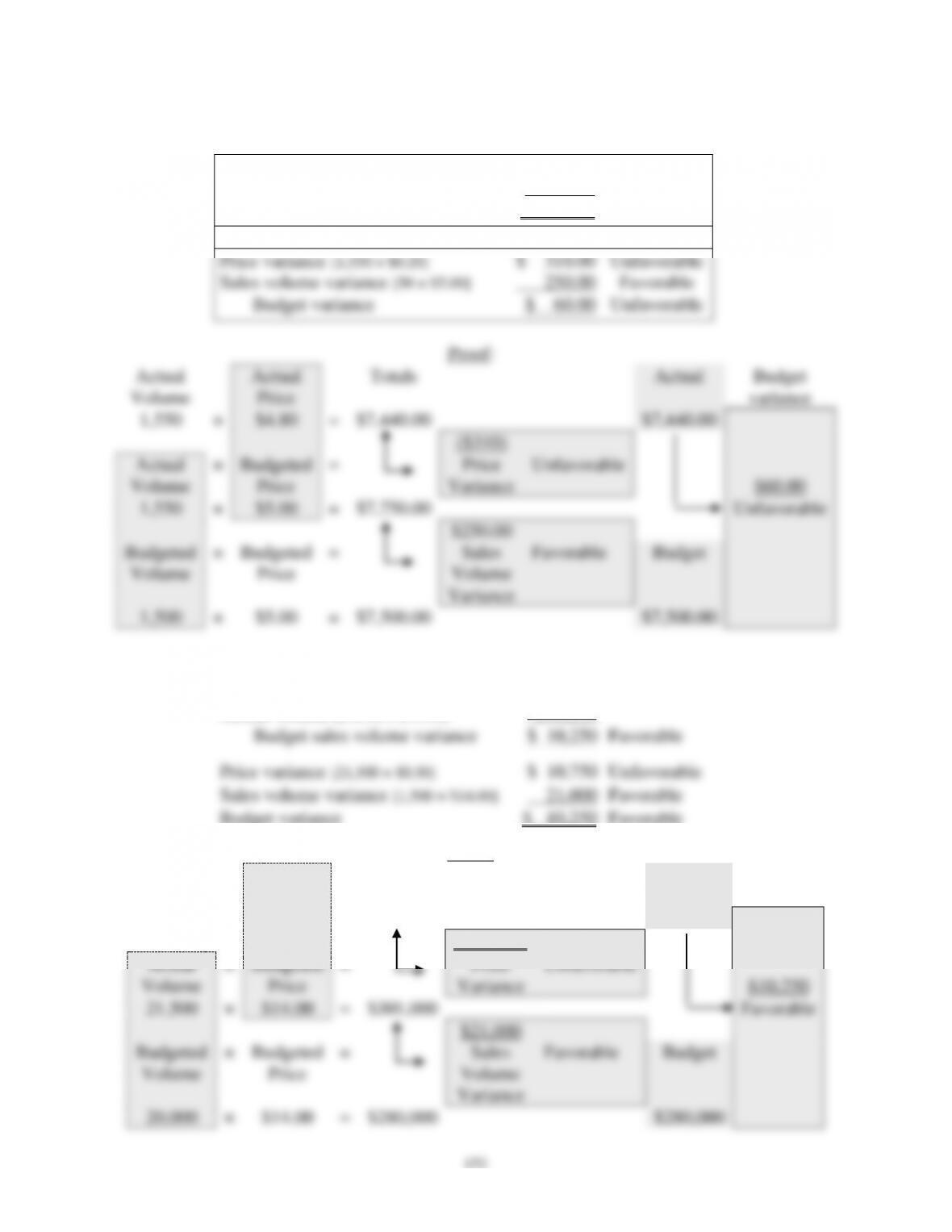

a. Sales revenue volume and price variances:

Budget [1,500 × $5.00]

$7,500.00

Actual [1,550 × $4.80]

7,440.00

Budget sales volume variance

$ 60.00

Unfavorable

Price variance [1,550 × $0.20]

$ 310.00

Unfavorable

Sales volume variance [50 × $5.00]

250.00

Favorable

Budget variance

$ 60.00

Unfavorable

Proof:

Actual

Volume

Actual

Price

Totals

Actual

Budget

variance

1,550

×

$4.80

=

$7,440.00

$7,440.00

($310)

Actual

Volume

×

Budgeted

Price

=

Price

Variance

Unfavorable

$60.00

1,550

×

$5.00

=

$7,750.00

Unfavorable

$250.00

Budgeted

Volume

×

Budgeted

Price

=

Sales

Volume

Variance

Favorable

Budget

1,500

×

$5.00

=

$7,500.00

$7,500.00

b. Sales revenue volume and price variances:

Budgeted volume [20,000 × $14.00]

$280,000

Actual volume [21,500 × $13.50]

290,250

Budget sales volume variance

$ 10,250

Favorable

Price variance [21,500 × $0.50]

$ 10,750

Unfavorable

Sales volume variance [1,500 × $14.00]

21,000

Favorable

Budget variance

$ 10,250

Favorable

Proof:

Actual

Volume

Actual

Price

Totals

Actual

Budget

Variance

21,500

×

$13.50

=

$290,250

$290,250

($10,750)

Actual

Volume

×

Budgeted

Price

=

Price

Variance

Unfavorable

$10,250

21,500

×

$14.00

=

$301,000

Favorable

$21,000

Budgeted

Volume

×

Budgeted

Price

=

Sales

Volume

Variance

Favorable

Budget

20,000

×

$14.00

=

$280,000

$280,000

152

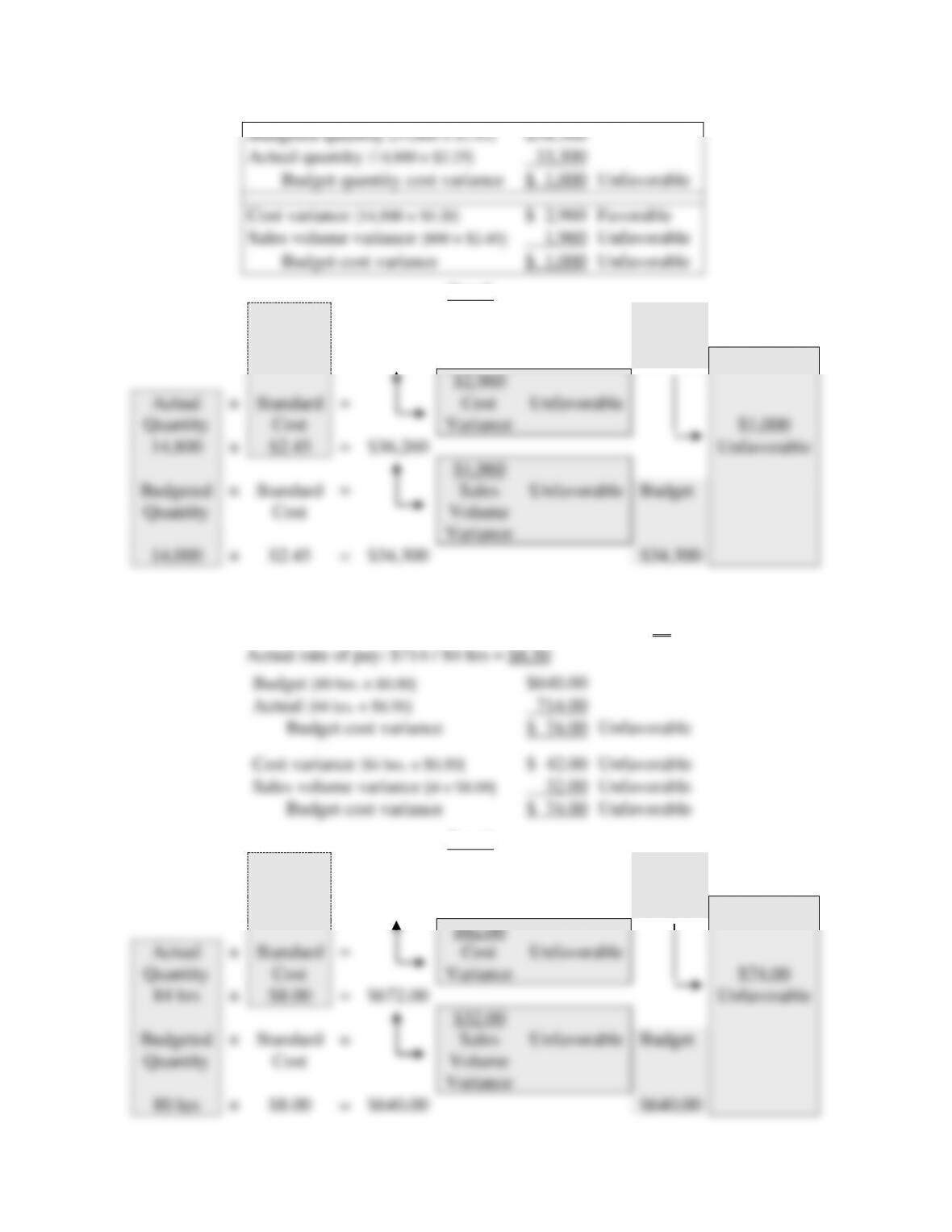

c. Cost and sales volume variances

Budgeted standard cost [1,000 × $6.00]

$6,000

Actual quantity [900 × $6.25]

5,625

Budget cost variance

$ 375

Unfavorable

Cost variance [900 × $0.25]

$ 225

Unfavorable

Sales volume variance [100 × $6.00]

600

Favorable

Budget cost variance

$ 375

Unfavorable

Proof:

Actual

Quantity

Actual

Cost

Totals

Actual

Budget

variance

900

×

$6.25

=

$5,625

$5,625

$225

Actual

Quantity

×

Standard

Cost

=

Cost

Variance

Unfavorable

$375

900

×

$6.00

=

$5,400

Favorable

$600

Budgeted

Quantity

×

Standard

Cost

=

Sales

Volume

Variance

Favorable

Budget

1,000

×

$6.00

=

$6,000

$6,000

d. (1) Sales revenue volume and price variances:

Budgeted price [14,000 × $6.45]

$90,300

Actual volume [14,800 × $6.75]

99,900

Budget sales revenue variance

$ 9,600

Favorable

Price variance [14,800 × $0.30]

$ 4,440

Favorable

Sales volume variance [800 × $6.45]

5,160

Favorable

Budget sales revenue variance

$ 9,600

Favorable

Proof:

Actual

Volume

Actual

Price

Totals

Actual

Budget

Variance

14,800

×

$6.75

=

$99,900

$99,900

$4,440

Actual

Volume

×

Budgeted

Price

=

Price

Variance

Favorable

$9,600

14,800

×

$6.45

=

$95,460

Favorable

$5,160

Budgeted

Volume

×

Budgeted

Price

=

Sales

Volume

Variance

Favorable

Budget

14,000

×

$6.45

=

$90,300

$90,300

153

(2) Cost variances:

Budgeted quantity [14,000 × $2.45]

$34,300

Actual quantity [14,800 × $2.25]

33,300

Budget quantity cost variance

$ 1,000

Unfavorable

Cost variance [14,800 × $0.20]

$ 2,960

Favorable

Sales volume variance [800 × $2.45]

1,960

Unfavorable

Budget cost variance

$ 1,000

Unfavorable

Proof:

Actual

Quantity

Actual

Cost

Totals

Actual

Budget

variance

14,800

×

$2.25

=

$33,300

$33,300

$2,960

Actual

Quantity

×

Standard

Cost

=

Cost

Variance

Unfavorable

$1,000

14,800

×

$2.45

=

$36,260

Unfavorable

$1,960

Budgeted

Quantity

×

Standard

Cost

=

Sales

Volume

Variance

Unfavorable

Budget

14,000

×

$2.45

=

$34,300

$34,300

e. Cost variances:

Budgeted hours: 400 guests / 20 guests = 20 × 4 hrs = 80 hours

Proof:

Actual

Quantity

Actual

Cost

Totals

Actual

Budget

variance

84 hrs

×

$8.50

=

$714.00

$714.00

$42.00

Actual

Quantity

×

Standard

Cost

=

Cost

Variance

Unfavorable

$74.00

84 hrs

×

$8.00

=

$672.00

Unfavorable

$32.00

Budgeted

Quantity

×

Standard

Cost

=

Sales

Volume

Variance

Unfavorable

Budget

80 hrs

×

$8.00

=

$640.00

$640.00

Budget [80 hrs. × $8.00]

Cost variance [84 hrs. × $0.50]

Unfavorable

Sales volume variance [4 × $8.00]

Unfavorable

Budget cost variance

Unfavorable

154

P9.10 Budgeted rooms to be sold next year: 80 × 75% × 365 = 21,900

a. Budgeted Departmental Contributory Income Statement

Rooms Department

Sales Revenue: [21,900 × $68.00]

$1,489,200

Expenses

Fixed wages expense

$ 186,000

Housekeeping expenses [21,900 × 0.5 × $9.00]

98,550

Subtotal

$ 284,550

Fringe benefits: [18% × $284,550]

51,219

Other costs: [21,900 × $2.75]

60,225

( 395,994)

Rooms Contributory income

$1,093,206

Overnight guests: 80 rooms × 75% = 60 rooms occupied

40% × 60 = 24 rooms double occupied

84 overnight guests

Average breakfast guests: 80% × 84 = 67.2 Guests

Snack bar sales revenue

Breakfast: [67.2 × $6.50 × 365]

$159,432

Lunch: [50 × 1.5 × $8.95 x 365]

245,006

Dinner: [50 × 2.0 × $10.95 × 365]

399,675

Total Sales Revenue

$804,113

Expenses [78% × $804,113]

( 627,208)

Snack Bar Contributory Income

$176,905

Consolidated Motel Departmental Income Statement

Rooms Contributory Income

$1,093,206

Snack Bar Contributory Income

176,905

Total Contributory Income

$1,270,111

Less: Indirect, Undistributed Costs

( 580,800)

Budgeted Operating Income

$ 639,311

b. Rooms budgeted sales revenue variance analysis

Rooms sales revenue:

Budget [21,900 × $68.00]

$1,489,200

Actual [21,700 × $68.40]

1,484,280

Budget rooms sales revenue variance

$ 4,920

Unfavorable

Price variance [21,700 × $0.40]

$ 8,680

Favorable

Sales volume variance [200 × $68.00]

13,600

Unfavorable

Budget rooms sales revenue variance

$ 4,920

Unfavorable

155

Proof:

Actual

Volume

Actual

Price

Totals

Actual

Budget

Variance

21,700

×

$68.40

=

$1,484,280

$1,484,280

$8,680

Actual

Volume

×

Budgeted

Price

=

Price

Variance

Favorable

($4,920)

21,700

×

$68.00

=

$1,475,600

Unfavorable

($13,600)

Budgeted

Volume

×

Budgeted

Price

=

Sales

Volume

Variance

Unfavorable

Budget

21,900

×

$68.00

=

$1,489,200

$1,489,200

The wage variance needs to be determined using hours and cost per hour, not cost per

room. By doing it this way, you can see the effect of the change in the labor rate per hour

plus the change in the time used to clean and clear each room.

Actual hours worked = 21,700 × 32 minutes per room

Rooms wage costs variance analysis:

Budget quantity [21,900 × 0.5 × $9.00]

$ 98,550

Actual quantity [21,700 × (32/60) × $9.35]

108,211

Budget quantity variance

$ 9 ,661

Unfavorable

Hours quantity variance [(11,573.3 – 10,850) × $9.00]

$ 6,510

Unfavorable

Quantity volume variance [200 × 0.5 × $9.00]

900

Favorable

Cost variance [11,573.3 × $0.35]

4,051

Unfavorable

Budget cost variance

$ 9,661

Unfavorable

Proof:

Actual

Quantity

Actual

Cost

Totals

Actual

Budget

variance

11,573.3

×

$9.35

=

$108,208

$108,208

($4,051)

Actual

Quantity

×

Standard

Cost

=

Cost

Variance

Unfavorable

($9,661)

11,573.3

×

$9.00

=

$104,160

Unfavorable

($5,610)

Budgeted

Quantity

×

Standard

Cost

=

Sales

Volume

Variance

Unfavorable

Budget

10,950

×

$9.00

=

$98,550

$98,550

156

P9.11 Calculate individual department contributory income statements, then combine each

department into a combined departmental operating budget. Determine total combined

operating income before depreciation, interest and taxes.

Combined Departmental Operating Budget (First Year)

Rooms Department

Rooms sales revenue: [100 × 64% × $72 × 365]

$1,681,920

Operating Expenses

Wages expense, fixed [given]

$326,900

Wages expense, variable: [100 × 64% = 64]

[64 / 16 = 4] [4 × 8 × $8.50 × 365]

99,280

Total estimated wages expense

$426,180

Employee fringe benefits [12% × $426,180]

51,142

Other variable expenses: [6% + 3%] × $1,681,920]

151,373

Total departmental direct costs

( 628,695)

Rooms Department Contributory Income

$1,053,225

Food Department

Dining room sales revenue:

Lunch: [75 × 1.5 × $8.25 × 6 × 52]

$289,575

Dinner (food only) [75 × 1.0 × $14.00 × 6 × 52]

327,600

Total Dining Room Sales Revenue

$ 617,175

Coffee Shop Sales Revenue

Breakfast: [65 × 1.0 × $5.75 × 365]

$136,419

Lunch: [65 × 1.5 × $7.75 × 365]

275,803

Dinner: [65 × 1.0 × $9.95 × 365]

236,064

Coffee breaks: [65 × 6.0 × $1.75 × 365]

249,113

Total Coffee Shop Sales Revenue

897,399

Lounge sales revenue: [20 × $8.50 × 310]

57,200

Subtotal food department

$1,571,744

Total variable expenses: [89% × $1,571,744]

( 1,398,879)

Food Department Contributory Income

$ 172,865

Beverage Department Sales Revenue

Beverage sales revenue per seat [90 × $5,250]

$472,500

Beverage sales revenue; from coffee shop, lunch

and dinner [($275,803 + $236,064) = $511,867 × 15%]

76,780

Beverage sales revenue; from dining room, lunch

and dinner [25% × $617,175]

154,294

Total Beverage Sales Revenue

$ 703,574

Beverage variable operating expenses

[32% + 25% + 5% = 62%] [62% × $703,574]

( 436,216)

Beverage Department Contributory Income

$ 267,358

Combined Departmental Operating Budget

Contributory Income, Rooms

$1,053,225

Contributory Income, Food

172,865

Contributory Income, Beverage

267,358

Total Contributory Income

$1,493,448

Less: Total Undistributed Indirect Expenses:

( 513,100)

Operating Income (before depreciation, interest and tax)

$ 980,348

157

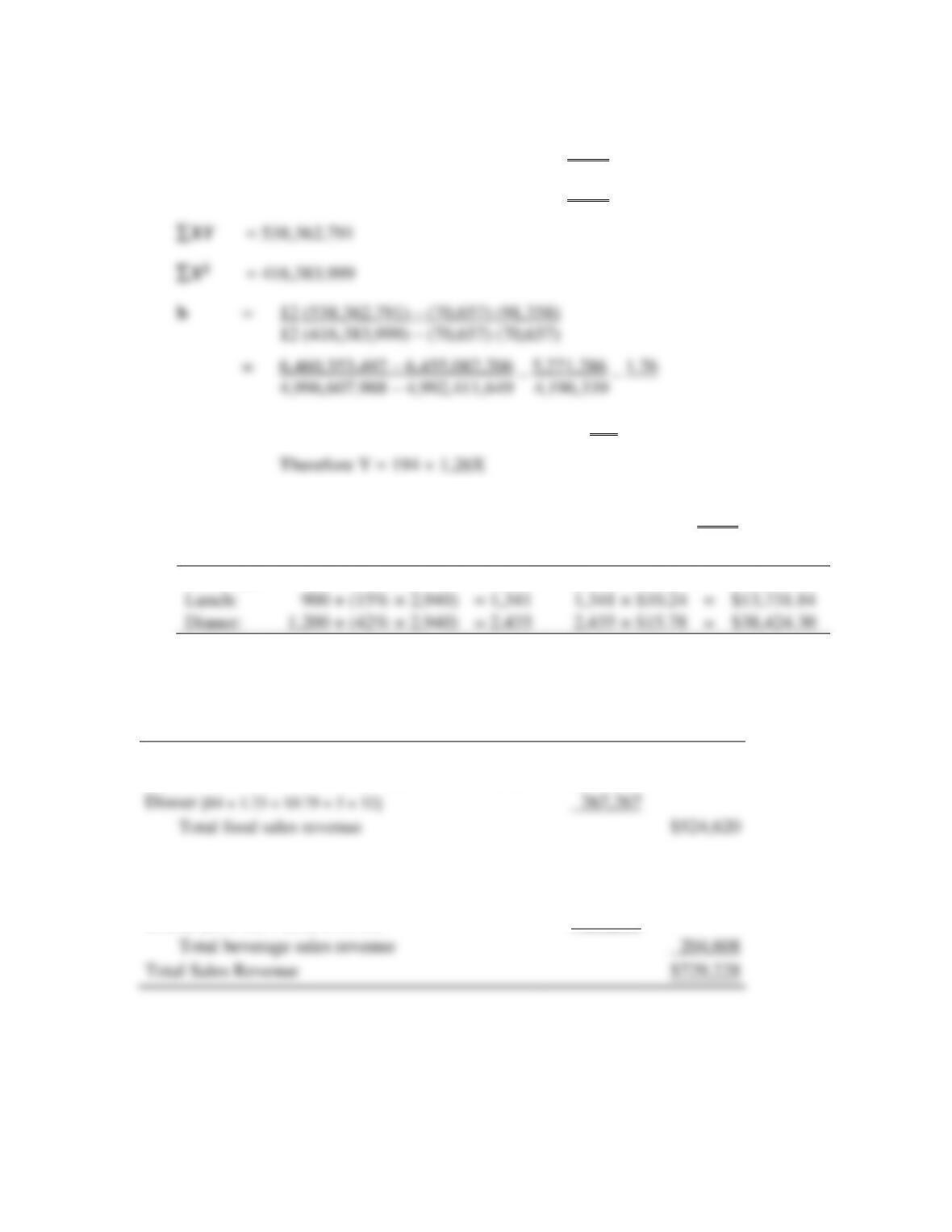

P9.12 Use regression analysis. The equation: Y = a + bX

X = 70,657 (average of X nights, 5,888.08 5,888)

Y = 91,358 (average Y guests = 7,613.167 7,613)

a = 7,613 – (1.26 × 5,888) = 7,613 – 7,419 = 194

P9.13 Regression analysis: Total guests in Nov. 100 × 70% × 140% × 30 = 2,940

Breakfast:

750 + (82% × 2,940)

= 3,161

3,161 × $5.25

=

$19,595.25

Lunch:

900 + (15% × 2,940)

= 1,341

1,341 × $10.24

=

$13,731.84

Dinner:

1,200 + (42% × 2,940)

= 2,435

2,435 × $15.78

=

$38,424.30

CASE 9 SOLUTION

a. 4C Company forecasted sales revenue for Year 2008

Food Sales Revenue

Lunch [84 × 1.5 × $5.85 × 6 × 52] + [15 × $5.85 × 6 × 52]

$257,353

Dinner [84 × 1.25 × $9.79 × 5 × 52]

267,267

Total food sales revenue

$524,620

Beverage Sales Revenue

Lunch [84 × 1.5 × $1.12 × 6 × 52] + [15 × $1.12 × 6 × 52]

$ 49,271

Dinner [84 × 1.25 × $5.69 × 5 × 52]

155,337

Total beverage sales revenue

204,608

Total Sales Revenue

$729,228

158

b. 4C Company, Budgeted Income Statement, For the Year 2008

Sales Revenue

Sales revenue: Food

$524,620

Sales revenue: Beverage

204,608

Total sales revenue

$729,228

Cost of Sales

Cost of sales: Food [39.5% × $524,620]

207,225

Cost of sales: Beverage [21.8% × $204,608]

44,605

Total Cost of Sales

( 251,830)

Gross Margin

$477,398

Operating Expenses

Salary and wages expense

$255,903

[($223,543 – $18,000 + $6,864) = ($212,407 × 104% + $35,000)]

Laundry expense [2.6% × $729,228]

18,960

Kitchen fuel expense

7,846

[VC: 0.5% × $729,228] + [Fixed costs: $3,800 + $400]

China & tableware expense [1.9% × $729,228]

13,855

Glassware expense [.03% × $729,228]

2,188

Contract cleaning expense [$5,906 + $600]

6,506

Licenses expense

3,205

Other operating expense [0.6% × $729,228]

4,375

Administrative & general expenses [$15,432 × 105%]

16,204

Marketing expenses [$6,917 + $3,000]

9,917

Utilities expense [ 0.8% × $729,228] + Fixed costs: $3,100 + $2,000]

10,934

Insurance expense [$1,895 × 110%]

2,085

Rent expense [$24,000 × 110%]

26,400

Interest expense

19,500

Depreciation expense

20,124

Total Operating Expenses

( 418,002)

Operating Income

$ 59,396

Income tax [22% × $59,396]

( 13,067)

Net income

$ 46,329

159

c. A comparative horizontal analysis and common-size vertical analysis of the 4C Company

Budgeted Income Statement for Year 2008 will be compared to Year 2007 income statement

(Case 2) and the common-size income statement (Case 3).

Comparative

Common-size

Horizontal Analysis

Vertical Analysis

Sales Revenue

Yr. 2007

Yr. 2008

$ Change

▲Change

Yr. 2008

Yr.2007

Sales revenue: Food

$458,602

$524,620

+$66,018

+14.4%

71.9%

71.8%

Sales revenue: Beverage

180,509

204,608

+ 24,099

+13.4%

28.1%

28.2%

Total Sales Revenue

$639,111

$729,228

+$90,117

+14.1%

100.0%

100.0%

Cost of Sales: Food

$181,323

$207,225

+$25,902

+14.3%

28.4%

35.5%

Cost of Sales: Beverage

39,303

44,605

+ 5,302

+13.5%

6.1%

21.8%

Total Cost of Sales

( 220,626)

( 251,830)

+ 31,204

+14.1%

(34.5%)

(34.5%)

Gross Margin

$418,485

$477,398

+ 58,913

+14.1%

65.5%

65.5%

Operating Expenses

Salaries & wages expense

$223,543

$255,903

+$32,360

+14.5%

35.1%

35.0%

Laundry expense

16,609

18,960

+ 2,351

+14.2%

2.6%

2.6%

Kitchen fuel expense

7,007

7,846

+ 839

+12.0%

1.1%

1.2%

China–Tableware expense

12,214

13,855

+ 1,641

+13.4%

1.9%

1.9%

Glassware expense

1,605

2,188

+ 583

+36.3%

0.3%

0.3%

Contract cleaning expense

5,906

6,506

+ 600

+10.2%

0.9%

0.9%

Licenses expense

3,205

3,205

– 0 –

– 0 –

0.4%

0.5%

Other operating expenses

4,101

4,375

+ 274

+ 6.7%

0.6%

0.6%

Admin–general expenses

15,432

16,204

+ 772

+ 0.5%

2.2%

2.4%

Marketing expense

6,917

9,917

+ 3,000

+43.4%

1.4%

1.1%

Utilities expense

7,918

10,934

+ 3,016

+38.1%

1.5%

1.2%

Insurance expense

1,895

2,085

+ 190

+10.0%

0.3%

0.3%

Rent expense

24,000

26,400

+ 2,400

+10.0%

3.6%

3.8%

Interest expense

23,981

19,500

– 4,481

–18.7%

2.7%

3.8%

Depreciation expense

20,124

20,124

– 0 –

– 0 –

2.8%

3.1%

Total Operating Expense

$374,457

$418,002

+ 43,545

+11.6%

(57.3%)

58.6%

Operating Income

$ 44,028

$ 59,396

+ 15,368

+34.2%

8.1%

6.9%

Income tax

( 9,686)

( 13,067)

+ 3,381

+34.9%

1.8%

1.5%

Net Income

$ 34,342

$ 46,329

+ 11,987

+34.2%

6.4%

5.4%

(1) A comparative horizontal analysis of the 4C Company budgeted income statement for

Year 2008 shows the following:

160

(b) Total operating expenses increased $43,545 or 11.6% ($418,002 – $374,457). Total

(2) A common-size vertical analysis of 4C Company’s budgeted income statement for Year

2008 shows the following:

(a) Sales revenue–food increased 0.1% (71.9% – 71.8%) relative to total sales revenue

and sales revenue–beverage decreased 0.1% (28.1% – 28.2%). This change is

insignificant.