140

CHAPTER 9

OPERATIONS BUDGETING

INTRODUCTION

This chapter, although it covers most of the relevant theory of budgeting, concentrates on

budgeted income statements. For this reason, the student should be very familiar with the content

of Chapter 2 concerning income statements and their typical content and format. Also,

familiarity with the information of Chapter 6 concerning menu prices and room rates will be

useful. The material in Chapters 7 and 8 concerning fixed and variable costs and their

relationship to sales revenue is essential. This chapter will discuss budgeting and create a base

for the section on cash budgeting in Chapter 11 and for much of the material in Chapter 12 that

discusses long-term investments.

TRUE OR FALSE QUESTIONS

(Correct answer indicated by T for True and F for False answers)

1. Budgets are always expressed in monetary terms.

F

2. A long-term budget is usually for a period from 1 to 5 years.

T

3. A cash budget is a type of capital budget.

F

4. A fixed budget is one based on a specific level of sales revenue.

T

5. A flexible budget is one based on various possible levels of sales revenue.

T

6. One purpose of budgeting is to provide management control over operations.

T

7. The general manager and the comptroller should be the only ones to prepare a budget.

F

8. One of the advantages of budgeting is that it permits subsequent comparison of actual

with forecast figures.

T

9. Budgets should only be prepared when the future is perfectly predictable.

F

10. In establishing objectives in budgeting, limiting factors should be considered.

T

11. Because there is usually a difference between budgeted figures and actual results, there

is little reason to spend time and money on budgeting.

F

12. The first step in the preparation of departmental budgets is the sales revenue forecast.

T

13. Past actual sales records, when available, are the foundation on which budgeted sales

revenue is built.

T

14. Derived demand is sales revenue from customers who walk in off the street.

F

15. In preparing budgeted sales revenue figures from historic records, current competition

can be ignored.

F

16. Current economic factors are considered in budgeting.

T

17. Preparing a staffing schedule for employees is one of the purposes of budgeting.

T

141

18. To forecast restaurant sales revenue for a meal period, the only factors that must be

taken into consideration are the number of seats, seat turnover rate, and average check.

F

19. In forecasting monthly room sales revenue in a hotel, the number of rooms in the hotel

can be ignored.

F

20. In forecasting beverage sales revenue in a dining room, that sales revenue can usually

be calculated as a percent of food sales revenue.

T

21. With incremental budgeting, budgets are automatically increased each year by the rate

of inflation.

F

22. A restaurant plans to keep its advertising budget at the same amount as last year. This

is a form of ZBB.

F

23. An advantage of ZBB is that it concentrates on the dollar cost of each department’s

activities and budget and not on broad percentage increases.

T

24. Variance analysis is a method of analyzing the differences between budgeted figures

and actual results.

T

25. A difference between budgeted sales revenue and actual sales revenue can be broken

down into a price variance and a sales volume variance.

T

26. A restaurant budgeted 1,000 customers with an average check of $12.00. Actual

customers were 900 with an average check of $12.50. The price variance will be $250

favorable.

F

27. A motel budgeted the sale of 3,000 rooms and a cleaning cost of $4.00 per room.

Actual results showed 3,100 rooms occupied with a cleaning cost of $4.05 per room;

there is a sales volume variance of $200 unfavorable.

F

28. Variance analysis is only useful for showing department heads how badly they are

doing their job.

F

29. A moving-average forecast is a time-series method of analysis.

T

30. A regression analysis forecast is not a time-series method.

F

MULTIPLE CHOICE QUESTIONS

(Correct answer indicated by asterisk)

1. Short-term budgets differ from long-term budgets in that a short-term budget:

(a) Is for a day, week, or month and a long-term one is for six months or a year

(b) Is expressed in monetary terms where a long-term budget is generally expressed in the

number of customers or some other measure

142

2. A capital budget is one:

(a) Prepared at the head office

3. A flexible budget is one:

(c) That is not part of the master budget

(d) That includes only variable costs

4. The budget preparation procedure:

(c) Starts from the top down

(d) Commences after the period concerned has started

5. An advantage of budgeting is that:

(c) If budgeted expenses are overestimated, there will be extra money at the end of the period

for staff bonuses

(d) Staff involved in budgeting will learn about confidential management matters

6. One of the steps in the budget cycle is to:

(a) Increase the forecast return on investment over the previous period

(b) Establish goals that are 50% above last year

7. Limiting factors in budgeting are factors that:

(c) Prevent a department head from talking to his staff about budgeting

(d) Ensure that sales revenue goals will always be established at the highest limits

8. If restaurant has budgeted 1,000 customers at an average check of $9.00 and actual customers

were 800 with an actual average check of $9.50, then:

(a) Actual sales revenue will be higher than budgeted

(b) We can assume that the higher average check is keeping customers away

9. Derived demand is demand:

(c) From customers who have given up going to competitive restaurants

(d) As a result of additional advertising

143

10. A restaurant has 125 seats with an average check of $8.00 and a daily seat turnover of 2.5. It

is open 5 days a week and the average check is forecast to increase by 10% in the next year.

Next year’s budgeted sales revenue will be:

(a) $286,000

(b) $650,000

11. When departmental budgets are increased each year by a flat percentage rate, this is known

(c) Incidental budgeting

(d) Inflationary budgeting

12. Which of the following is not true of ZBB?

(c) It obliges managers to identify inefficient or obsolete functions within their areas of

responsibility

(d) It can identify areas of overlap or duplication

13. Variance analysis is a:

(a) Procedure for questioning department heads about differences between budgeted and

actual results

(b) Method of analyzing limiting factors

14. A banquet department’s annual budgeted sales revenue was based on 45,000 guests at an

average check of $10.00. Actual figures were 47,500 guests at a $9.50 average check. The

total budget, price, and sales volume variances respectively are:

(a) $1,250 Unfavorable, $23,750 Unfavorable, and $22,500 Favorable

(b) $1,250 Favorable, $2,750 Favorable, $1,500 Unfavorable

15. The general equation for a moving-average forecast that uses n for the number of periods is:

(c) Total of all of the previous n periods multiplied by n

(d) Average for each of the previous n periods multiplied by n

144

EXERCISE SOLUTIONS

E9.1 Estimate sales revenue: [Seats × Turnover × Average check × Operating days]

E9.2 Estimate monthly sales revenue:

E9.3 Calculate housekeeping cost and quantity variance analysis.

a. Budget: 8,000 × $4.40 = $35,200

Actual: 8,480 × $4.90 = $41,552

Proof:

Actual

Quantity

Actual

cost

Totals

Actual

Budget

variance

8,480

×

$4.90

=

$41,552

$41,552

$4,240

Actual

quantity

×

Budgeted

cost

=

cost

variance

Unfavorable

($6,352)

8,480

×

$4.40

=

$37,312

Unfavorable

$2,112

Budgeted

quantity

×

Budgeted

cost

=

Quantity

volume

Variance

Unfavorable

Budget

8,000

×

$4.40

=

$35,200

$35,200

145

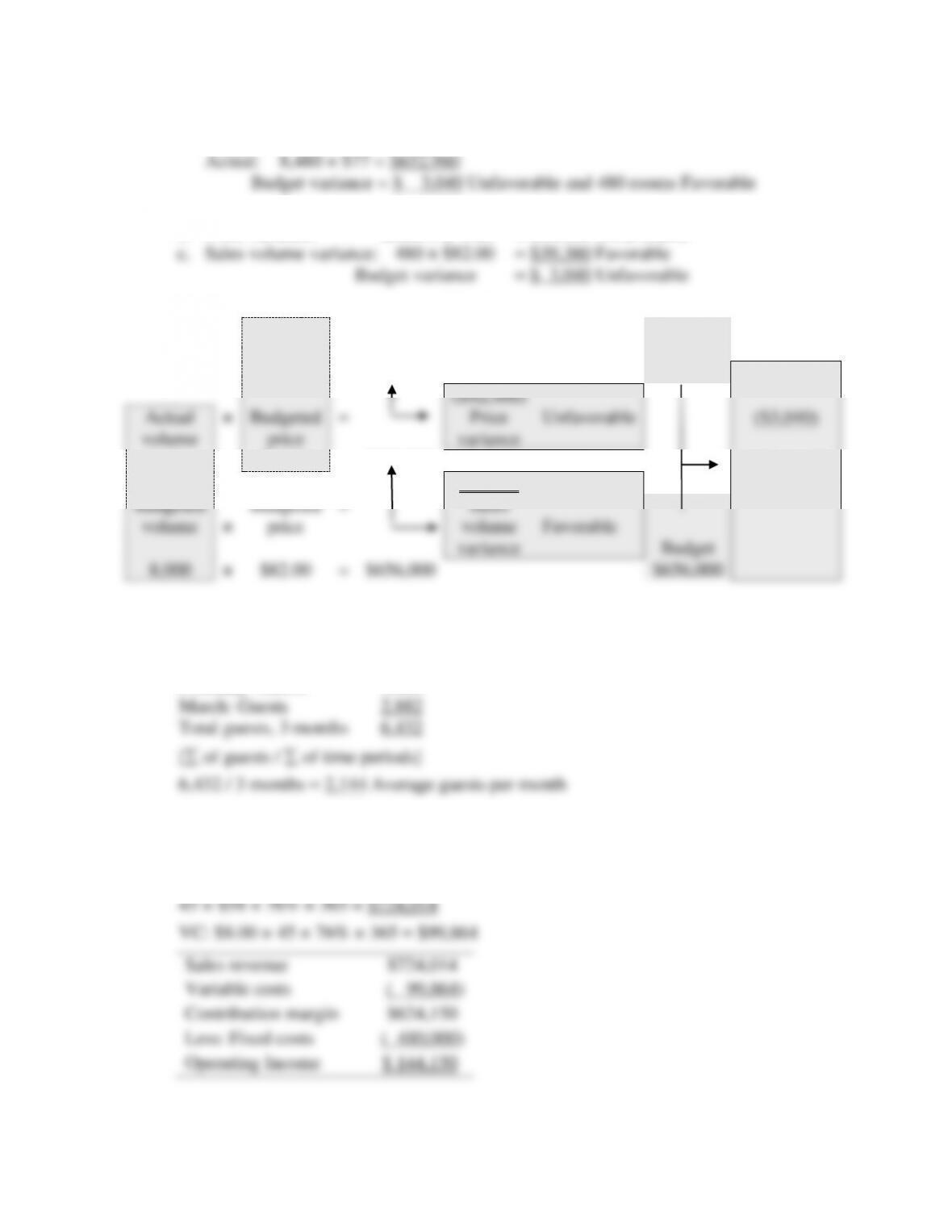

E9.4 Calculate sales revenue variance analysis.

a. Budget: 8,000 × $82 = $656,000

b. Price variance: 8,480 × $ 5.00 = $42,400 Unfavorable

Proof:

Actual

volume

×

Actual

price

Totals

Actual

Budget

variance

8,480

×

$77.00

=

$652,960

$652,960

($42,400)

Actual

volume

×

Budgeted

price

=

Price

variance

Unfavorable

($3,040)

8,480

×

$82.00

=

$695,360

Unfavorable

$39,360

Budgeted

volume

×

Budgeted

price

=

Sales

volume

variance

Favorable

Budget

8,000

×

$82.00

=

$656,000

$656,000

E9.5 Calculate the moving average guests count for three months.

January: Guests 1,670

February: Guests 1,880

E9.6 Forecast operating income.

SR: [Rooms × Occupancy % × Average room rate × Operating days]

146

E9.7 Forecast annual sales revenue by meal periods.

SR: [Seats × Turnover × Average check × Operating days = Meal sales revenue]

E9.8 Calculate room sales revenue for three months.

E9.9 Calculate sales revenue and operating income for a year.

SR = [Rooms Available x Avg. Occupancy % x Avg. room rate x 365 days]

Rooms sales revenue: 70 × $125 × 74% × 365 = $2,363,375

E9.10 Answer questions relative to VC, gross margin and operating income.

a. VC = VC% × SR = 72% × $ 912,000 = $656,640

147

PROBLEM SOLUTIONS

P9.1 Determine monthly sales revenue considering room rate increases and occupancy.

Room rate increase for July and August is: $80 × 110% = $88

P9.2 Prepare an annual budget for the coming year.

Sales revenue [60 × 74% × $84 × 365]

$1,361,304

Variable costs [60 × 74% × $8 × 365]

( 129,648)

Contribution margin

$1,231,656

Fixed costs

( 825,000)

Operating income

$ 406,656

P9.3 Calculate budgeted food sales revenue and beverage sales revenues.

Meal period SR = [Meal period × Seats × Turnover × Days Available]

Lunch: [66 × 1.75 × $12.95 × 27] = $ 40,385

Beverage: [15% × $40,385] = 6,058

P9.4 Calculate the budgeted sales revenue for the coffee shop for January.

[Seats × Turnover ×Average check × Operating days]

Breakfast: [120 × 1.50 × $ 7.50 × 31] = $ 41,850

148

P9.5 Prepare a 3 level flexible budget. Comment on the affect of operating and net income.

Sales Revenue

$800,000

$900,000

$1,000,000

Variable Costs: [38% + 28% + 10% = 76%]

(608,000)

(684,000)

( 760,000)

Contribution Margin

$192,000

$216,000

$ 240,000

Fixed Costs: [$52,000 + $102,000]

(154,000)

(154,000)

( 154,000)

Operating Income

$ 38,000

$ 62,000

$ 86,000

Tax rate [29%]

( 11,020)

( 17,980)

( 24,940)

Net income

$ 26,980

$ 44,020

$ 61,060

Breakeven: Fixed costs + OI $154,000 + $0 $154,000 $641,667

1 − VC% 1 − 76.0% 24.0%

All three sales revenue levels exceed breakeven. At $800,000, operating income and net

income represents 4.8% and 3.4% of sales revenue respectively. At $900,000, operating

P9.6 Calculate the food sales revenue for the month of June.

149

P9.7 Complete a budgeted income statement.

Budgeted Income Statement

Food Sales Revenue

Weekday lunch [120 × 1.5 × $8.50 × 305]

$466,650

Weekday dinner [120 × 1.25 × $18.50 × 305]

846,375

Sundays-holidays etc. [120 × 2.0 × $21.00 × 60]

302,400

Private party room food sales revenue

144,000

Total budgeted food sales revenue

$1,759,425

Beverage Sales Revenue

Lunch [12% × $466,650]

$ 55,998

Dinner [25% × $846,375]

211,594

Private party room [40% × $144,000]

57,600

Total budgeted beverage sales revenue

$ 325,192

Total budgeted sales revenue

$2,084,617

Cost of sales

Food cost [37% × $1,759,425]

$650,987

Beverage cost [33% × 325,192]

107,313

Total cost of sales

( 758,300)

Gross Margin

$1,326,317

Operating Expenses

Salaries expense

$284,000

Variable wage expenses [15% × $2,084,617]

312,693

Employee Benefits expense [12% × $596,693]

71,603

Other operating expenses [11.7% × $2,084,617]

243,900

Fixed overhead expenses

226,400

Total Operating Expenses

(1,138,596)

Net operating income

$ 187,721

150

P9.8 Two alternative income statements; explain which you recommend and why?

Budgeted Average Monthly Income Statement

Alternative 1

Alternative 2

Sales revenue food

$40,000

$48,000

Sales revenue beverage

10,000

12,000

Total Sales Revenue

$50,000

$60,000

Cost of sales, food [37%]

$14,800

$17,760

Cost of sales, beverage [30%]

3,000

3,600

Total Cost of Sales

(17,800)

(21,360)

Gross Margin

$32,200

$38,640

Operating Expenses

Wages expenses

$13,600

$15,600

Operating Supplies expense

4,000

4,800

Admin. & general expenses

2,600

2,800

Advertising & promo.

1,800

3,800

Repairs & maintenance

900

1,200

Utilities expense

1,300

1,400

Depreciation

700

700

Interest expense

600

600

Total Operating Expenses

(25,500)

(30,900)

Operating income

$ 6,700

$ 7,740

Alternative 2 appears to be the best choice and provides a higher level of operating

income of $1,040. Alternative 2 also provides a higher level of sales revenue that

adequately provides the increases to operating expenses and yields more net income.

However, either alternative is risky if customers object to decreased portion sizes.