107

CHAPTER 7

COST MANAGEMENT

INTRODUCTION

Chapter 6 discussed the concept of establishing prices to help achieve a particular desired return

on investment. However, there is often a limit to how high prices can be pushed before customer

resistance occurs and reduced demand for the product or service occurs. To avoid constantly

raising prices, concentrating on controlling costs may be required without which costs could

escalate out of proportion to sales revenue. In Chapter 5, we saw how the use of standard cost

control can assist in controling the cost of food and beverages. This chapter continues the

discussion on cost control and discusses the importance of cost management and decision–

making.

TRUE OR FALSE QUESTIONS

(Correct answer indicated by T for True and F for False)

1. Knowledge of the identity and classification of a specific cost is essential when

making business decisions.

T

2. An indirect cost is normally controllable by an operating department head.

F

3. A joint cost is one that is partly direct and partly indirect.

F

4. A sunk cost is one that is not normally relevant to future decisions.

T

5. A fixed cost is one that never changes, even in the long run.

F

6. A semivariable cost is one that is partly fixed and partly variable.

T

7. A variable cost is one that varies in linear fashion with sales revenue.

T

8. A standard cost is what the cost should be for a given level of sales revenue.

T

9. An opportunity cost is one that is recorded on the income statement.

F

10. A discretionary cost is one that can either be incurred or not incurred.

T

11. Allocation of indirect costs to operating departments should be done with caution.

T

12. One should never sell below total cost.

F

13. In making decisions about costs, no other factors need to be considered other than the

relevant costs.

F

14. An operation is considering closing for a certain period during which it has been

losing money. If by closing, the remaining fixed costs would be greater than the

previous losses, then normally the decision will be to close.

F

108

15. If at an equivalent sales revenue level, Business A has higher fixed costs than

Business B, then Business B will make more net income than Business A from each

additional sales revenue dollar above the current level.

F

16. A business with high fixed costs relative to variable costs is said to have high

operating leverage.

T

17. Given two comparable business situations, the one with the lower fixed costs will

have a higher break-even sales revenue level.

F

18. The equation for calculating the indifference point when deciding to pay a fixed rent

amount or rent based on a percent of sales revenue is: Fixed rent costs divided by the

variable rate percent.

T

19. The high-low method of separating semivariable costs into their two elements is the

most accurate method.

F

20. On a multipoint graph, the information about the independent variable is plotted on

the vertical axis.

F

21. On a multipoint graph, only one “correct” straight line can be drawn.

F

22. On a multipoint graph, the point at which the sloped straight line intersects the

vertical axis gives the amount of total variable costs.

F

23. Regression analysis is a mathematical technique for separating the two elements in

semivariable costs.

T

24. In regression analysis, the information about the independent variable is given the

symbol X.

T

25. Regression analysis gives the least exact results for fixed and variable costs.

F

26. Standard portion sizes are an integral part of food cost control.

T

27. A standard recipe for each menu item is essential for effective cost control.

T

28. The fixed cost of labor is not a factor in labor cost control.

F

MULTIPLE CHOICE QUESTIONS

(Correct answer indicated by asterisk)

1. A sunk cost is one that is:

(c) Controllable in the future

(d) The same as an opportunity cost

2. Which of the following costs is primarily fixed?

(c) Labor cost

(d) Operating supplies

109

3. Variable costs:

(a) Decrease 10% if sales revenue increases 10%.

4. Standard costs:

(c) Are the same as variable costs

(d) Must be broken down into their fixed and variable elements

5. Indirect costs should be allocated to operating departments:

(a) Because otherwise the departmental income after deducting direct costs will be incorrect

(b) To insure that each department has a net income after deducting both direct and indirect

costs

6. One can sell below cost when the sales revenue:

(c) Covers fixed costs but not necessarily all variable costs

(d) Covers all direct costs

7. An operation should close during the off season when:

(a) Variable costs are higher than fixed costs

(b) The lost sales revenue would be higher than total costs

8. A restaurant with high operating leverage has:

(a) Low fixed costs relative to variable costs

(b) A high net income in relation to sales revenue

9. A company with low operating leverage:

(a) Is better off than one with high operating leverage

(b) Is not going to be as successful as one with high operating leverage

10. In times of rising sales revenue, it would be better to:

(c) Try and convert some of the fixed costs into variable ones

(d) Change direct costs into indirect costs

110

11. The equation for calculating the indifference point when deciding to pay a fixed rent amount

versus rent based on a percent of sales revenue is:

(a) Sales revenue divided by the variable rent percentage

(b) Fixed rent cost multiplied by the variable rent percentage

12. Using the high-low method, what are the fixed and variable costs if the high sales revenue is

$160,000 with total costs of $90,000, and the low sales revenue is $96,000 with total costs of

$58,000. What is the fixed cost and the variable percentage per dollar of sales revenue?

(c) $ 6,750 fixed and 32.5% per dollar of sales revenue

(d) $ 4,240 fixed and 56.0% per dollar of sales revenue

13. The intersect point of the vertical and sloped lines on a multi-point graph:

(c) Gives the total cost

(d) Gives the total units

14. In making a decision about which piece of equipment to buy, two types of costs are

considered. They are relevant and:

(a) Sunk

15. Which is the best concept for allocating indirect costs?

(c) Based on contributory income

(d) Based on square footage

EXERCISE SOLUTIONS

E7.1 Find variable cost %.

E7.2 Find contribution margin: [SR – VC = CM]

111

E7.3 Find the contribution margin and operating income; accept or reject?

Sales Revenue [70 × $18]

$1,260

Variable costs [$1,260 × 68%]

( 857)

Contribution Margin

$ 403

Fixed costs

( 100)

Operating Income

$ 303

* Accept the proposal

E7.4 Allocation of indirect costs based on square footage.

E7.5 Find variable cost per guest and total fixed costs.

Guests

Labor Cost

High data

18,000

$25,500

Low data

(12,000)

(18,000)

▲

6,000

▲

$ 7,500

▲ Cost / ▲ Guests = VC per guest = $7,500 / 6,000 = $1.25

High labor cost

$25,500

High VC [18,000 × $1.25]

(22,500)

Fixed cost

$ 3,000

Low labor cost

$18,000

Low VC [12,000 × $1.25]

( 15,000)

Fixed cost

$ 3,000

E7.6 Find variable cost per dollar of sales revenue and total fixed costs.

S.R.

Operating Cost

High data

$28,000

$20,000

Low data

( 23,000)

( 17,000)

▲

$ 5,000

▲

$ 3,000

▲ Cost / ▲ Guests = VC per SR dollar = $3,000 / 5,000 = 60%

High operating cost

$20,000

High VC [28,000 × 60%]

(16,800)

Fixed cost

$ 3,200

Low operating cost

$17,000

Low VC [23,000 × 60%]

( 13,800)

Fixed cost

$ 3,200

112

E7.7 Calculate the contribution margin and operating income. Justify your decision to accept

or not accept the booking.

Sales Revenue [40 × $10.50]

$420

* Accept the function. By selling below

total cost of $423 ($273 + 150), we offset

FC costs by $147 of $150 that is incurred

with or without the function.

* Accept the offer!

Variable costs [$420 × 65%]

( 273)

Contribution Margin

$147

Fixed costs (per day)

( 150)

Operating loss

($ 3)

E7.8 Find the indifference point (the breakeven point of sales revenue at which the fixed rent

and variable rent for a year are the same). Explain which option you recommend?

E7.9 Given the information, do you recommend they close or stay open for the last three

months.

113

PROBLEM SOLUTIONS

P7.1 Objective evaluation made to determine the best investment considering only relevant

costs of the alternatives. Identify which model would be the best investment.

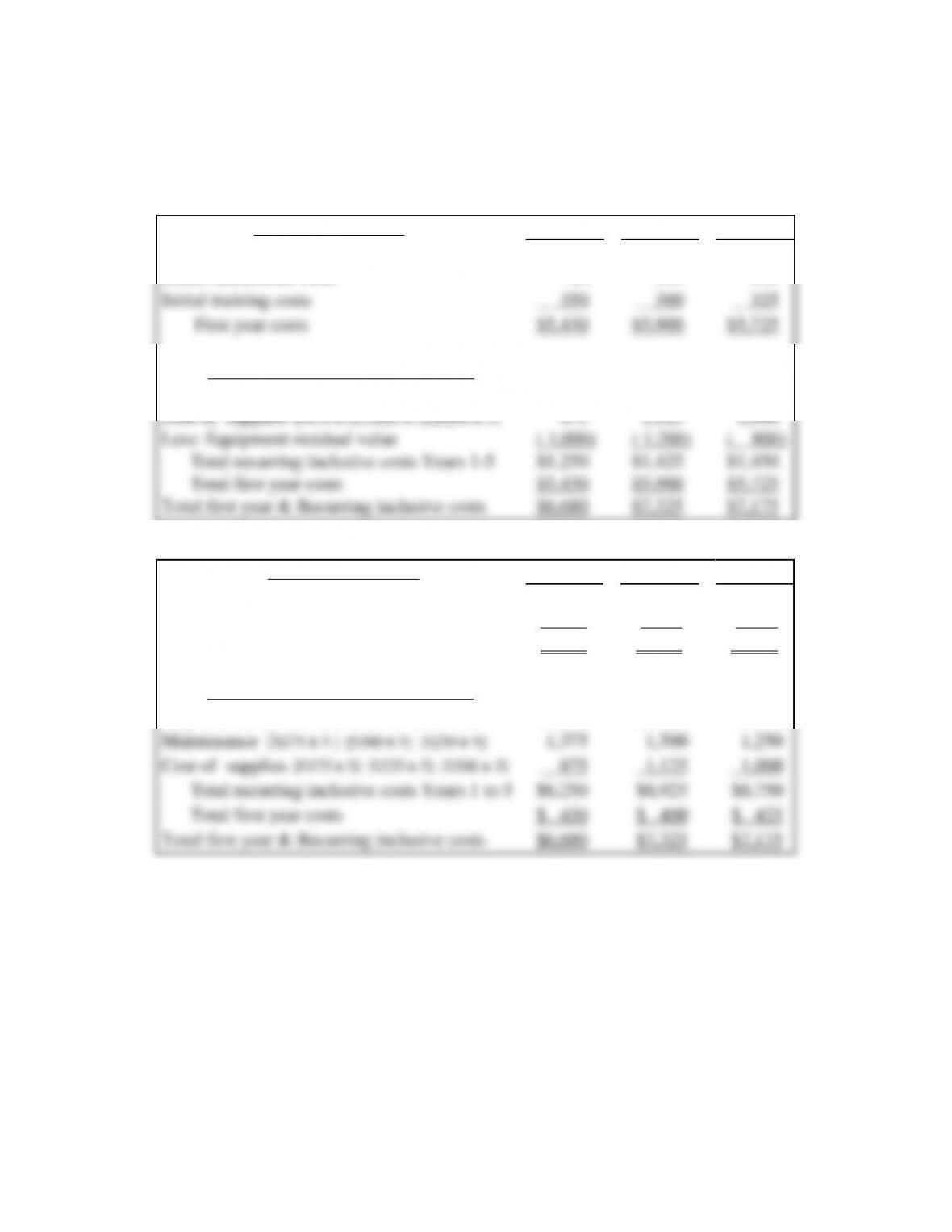

(Primary) Unique costs Year 1

Model 1

Model 2

Model 3

New equipment cost

$5,000

$5,500

$5,300

Initial installation costs

80

100

100

Initial training costs

350

300

325

First year costs

$5,430

$5,900

$5,725

Recurring inclusive costs Years 1-5

Maintenance [$275 x 5 ] [$300 x 5] [$250 x 5]

$1,375

$1,500

$1,250

Cost of supplies [$175 x 5] [$225 x 5] [$200 x 5]

875

1,125

1,000

Less: Equipment residual value

( 1,000)

( 1,200)

( 800)

Total recurring inclusive costs Years 1-5

$1,250

$1,425

$1,450

Total first year costs

$5,430

$5,900

$5,725

Total first year & Recurring inclusive costs

$6,680

$7,325

$7,175

(Alternative) Unique costs Year 1

Model 1

Model 2

Model 3

Initial installation costs

$ 80

$ 100

$ 100

Initial training costs

350

300

325

First year costs

$ 430

$ 400

$ 425

Recurring inclusive costs Years 1-5

Depreciation [$800 x 5] [$860 x 5] [$900 x 5]

$4,000

$4,300

$4,500

Maintenance [$275 x 5 ] [$300 x 5] [$250 x 5]

1,375

1,500

1,250

Cost of supplies [$175 x 5] [$225 x 5] [$200 x 5]

875

1,125

1,000

Total recurring inclusive costs Years 1 to 5

$6,250

$6,925

$6,750

Total first year costs

$ 430

$ 400

$ 425

Total first year & Recurring inclusive costs

$6,680

$7,325

$7,175

114

P7.2 Consideration of selling below cost can be made if an objective analysis indicates

variable costs are covered and a contribution towards fixed costs.

a. The total variable cost plus the allocated fixed cost per person determines the total

cost on a per person basis:

Cost per person evaluation

Food cost of sales

$ 6.50

Wage cost

2.75

Other costs

1.25

Total variable cost per person

$10.50

Fixed cost per person [$350 / 100]

3.50

Total cost per person

$14.00

b. If 100% is the unknown selling price, contributory income wanted is 20%. Then

100% − 20% = 80% represents the total cost. If total cost per person is $14.00 or

c. With the per person selling price, variable cost, fixed cost, and contributory income

known, evaluate the position of accepting or not accepting the offer.

Accepted

Yes

No

Sales revenue [100 × $13.75]

$1,375

-0-

Variable costs [100 × $10.50]

(1,050)

-0-

Function gross margin

$ 325

-0-

Fixed costs

( 350)

( 350)

Operating loss

($ 25)

($350)

Accept the function if there is no chance of accepting another offer. Variable costs

are covered and a contribution of $325 is made towards fixed costs, thus the loss is

minimized to $25 instead of $350 if the function is not accepted.

Allocated indirect costs

( 12,480)

( 52,000)

Operating income

P7.3 a. Allocate indirect costs (IDC) to each division based on square footage.

Division

IDC

Allocated

Dining Room

2,200 sq. ft.

/

4,000

=

55.0%

×

$52,000

=

$28,600

Coffee Shop

840 sq. ft.

/

4,000

=

21.0%

×

$52,000

=

$10,920

Lounge

960 sq. ft.

/

4,000

=

24.0%

×

$52,000

=

$12,480

Total Sq. Ft.

4,000 sq. ft.

100.0%

$52,000

116

P7.4 Annual operating income:

1st qtr.

+

2nd qtr.

+

3rd qtr.

−

4th qtr.

=

Operating Income

$7,100

+

$10,100

+

$8,600

−

($2,650)

=

$23,150

Operating income for 9 months; closed Quarter 4:

1st qtr.

+

2nd qtr.

+

3rd qtr.

=

Operating Income

$7,100

+

$10,100

+

$8,600

=

$25,800

Less 4th quarter expenses to be paid if closed:

Operating income for 3 quarters

$25,800

Wages

$3,000

Advertising [600 × 50%]

300

Utilities [$100 × 3 mo.]

300

Maintenance [stated]

200

Insurance [$1,200 × 40%]

480

Interest [stated @ $750 per qtr.]

750

Depreciation [$700 × 25%]

175

Rent [stated @ $6,000 per qtr.]

6,000

( 11,205)

Adjusted operating income; 3 qtrs.

$ 14,595

Do not close. Known costs to be incurred if 4th quarter operations are closed is $11,205

and adjusts operating income from $23,150 to $14,595, or an additional loss of $8,555

($23,150 – $14,595).

P7.5 a. If Motel A is closed, overall net loss will be:

Motel A Fixed costs

($110,000)

Motel B Operating income

8,000

Motel C Operating income

30,000

Net operating loss

($ 72,000)

If Motel B is closed, overall net loss will be:

Motel A Operating Loss

($ 5,000)

Motel B Fixed costs

( 167,000)

Motel C Operating income

30,000

Net operating loss

($142,000)

If Motel C is closed, overall net loss will be:

Motel A Operating Loss

($ 5,000)

Motel B Operating income

8,000

Motel C Fixed costs

( 260,000)

Net operating loss

($257,000)

117

Thus, closing Motel A which will minimize the overall loss. Leaving Motel’s B and

C open with operating income of $8,000 and $30,000 respectively, they will provide

b. If Motel A is closed overall net loss will be:

Motel A Fixed costs

($110,000)

Motel B Operating income

45,000

Motel C Operating income

63,000

Net operating loss

($ 2,000)

If Motel B is closed overall net income will be:

Motel A Operating income

$ 55,000

Motel B Fixed costs

(113,000)

Motel C Operating income

63,000

Net operating income

$ 5,000

If Motel C is closed overall net loss will be:

Motel A Operating income

$ 55,000

Motel B Operating income

45,000

Motel C Fixed costs

(112,000)

Net operating loss

($ 12,000)

Thus, close Motel B because the company overall will have a net operating income

rather than an operating loss. Motel’s A and C will provide a total net operating

income of $5,000 after absorbing the fixed costs Motel B, ($55,000 + $63,000 –

$113,000).

Note: This time Motel B is closed despite the fact it has the highest fixed costs. The

same discussion applies to this situation as it does to Part a. However, in Part b.

there is little leeway with increasing additional labor costs.

118

P7.6 Determine the present operating income of each motel and recommend which should be

purchased.

Jack’s

Jock’s

Sales revenue

$550,000

$550,000

Variable costs

$302,500

$330,000

Fixed costs

212,500

(515,000)

185,000

(515,000)

Operating income

$ 35,000

$ 35,000

Stated assumptions: (1) Sales revenue can be increased by 25% in both of the motels.

(2) A saving of $12,000 on interest expense (FC) is possible in Jack’s Motel. (3) A cost

savings of 6% reducing variable wage costs to 54% (60% − 6%) for Jock’s Motel. If

these assumptions were achieved, the operating income would be:

Jack’s

Jock’s

Sales revenue

$687,500

$687,500

Variable costs

$378,125

$371,250

Fixed costs

200,500

185,000

Total operating costs

(578,625)

(556,250)

Operating income

$108,875

$131,250

Calculations of stated assumptions:

Sales revenue: Jacks and Jocks = $550,000 x 125% = $687,500

Jack’s

Jock’s

VC: $687,500 x 55% = $378,125

VC: $687,500 x 54% = $371,250

FC: $212,500 – $12,000 = $200,500

FC: $185,000 no change

Based on the assumptions being achieved, Jock’s Motel would be a better proposition

since its operating income would be higher than Jack’s Motel. The entrepreneurs should

be advised that this would only be true if all the assumptions are correct. For example:

reduction of variable cost from 60% to 55%.

P7.7 a. Fixed lease cost / Variable lease % (or FC / VC%)

$2,800 × 12 months = $33,600

b. Assuming the average sales revenue forecast for the coming year is correct at

$525,000, the anticipated fixed and variable cost would be:

(1) Fixed lease cost remains at $33,600

P7.8 a. Calculate the variable cost per room, total variable cost and, using the High-Low

method, find the fixed cost per month.

VC per room unit (person):

b. Using the highest month, total variable cost is: 2,800 rooms × $0.70 = $1,960

120

P7.10 Regression analysis:

SR

Wage Cost

XY

X²

X

Y

(X × Y)

(X × Y)

1

$ 11,200

$ 5,300

$ 59,360,000

$ 125,440,000

2

13,000

6,100

79,300,000

169,000,000

3

14,900

6,200

92,380,000

222,010,000

4

19,100

7,000

133,700,000

364,810,000

5

22,000

9,000

198,000,000

484,000,000

6

24,200

9,600

232,320,000

585,640,000

7

26,300

9,700

255,110,000

691,690,000

8

27,400

10,100

276,740,000

750,760,000

9

23,500

8,300

195,050,000

552,250,000

10

20,100

7,600

152,760,000

404,010,000

11

18,200

8,000

145,600,000

331,240,000

12

16,000

7,100

113,606,000

256,000,000

Totals

$235,900

$94,000

$1,933,920,000

$4,936,850,000

X

Y

XY

X²

Fixed costs = (Y)( X2) – (X)( XY)

n(X2) – (X)2

Total annual wages

$94,000

Less: Fixed costs [$2,185.17 x 12]

( 26,222)

Variable wages

$67,642

P7.11 Additional data will require adjustments to high July data and low December data.

July Adjustments: (Wage costs) Retroactive wage increase of $1,800 must be deducted:

$21,600 − $1,800 = $19,800 July wage cost.

Dec. Adjustments: (Sales revenue) The special $3,400 sales revenue must be deducted:

122

CASE 7 SOLUTION

Additional sales revenue

Food Sales revenue: [15 × $5.25 × 6 ×52]

$24,570

Beverage Sales revenue: [15 × $0.92 × 6

×52]

4,306

Total sales revenue

$28,876

Cost of sales:

Food [39.5% × $24,570]

$ 9,705

Beverages [21.8% × $4,306]

939

Total cost of sales

( 10,644)

Gross Margin

$18,232

Increase in expenses

Wages: [4 × $5.50 × 6 × 52]

$ 6,864

Laundry: 2.6%

China and tableware: 1.9%

Glassware: 0.3%

Other operating costs: 0.6%

5.4%

Total Variable Expenses [5.4% × $28,876]

$ 1,559

Total Increase in Expenses

( 8,423)

Operating Income

$ 9,809

Less: Cost of advertising

( 3,000)

Operating Income (Increase)

$ 6,908

The advertising should be carried out.