CHAPTER 3

ANALYSIS AND INTERPRETATION OF

FINANCIAL STATEMENTS

INTRODUCTION

Before financial statements can be analyzed, the reader must have a good grasp of the way

different statements are prepared. It is extremely beneficial to have a firm conceptual under–

standing of basic accounting and the accounting terminology used by hospitality industry firms.

For this reason, Chapters 1 and 2 should be reviewed or studied, as a prerequisite to this chapter

on analysis and interpretation of information presented by balance sheets and income statements.

TRUE OR FALSE QUESTIONS

(Correct answer indicated by T for True answers and F for False answers)

1. Various readers of financial statements will generally analyze them in different ways.

T

2. Comparative horizontal balance sheet analysis shows each individual account, subtotal

and total balance changes from one balance sheet date to the next. Changes are

described in both dollars and percentages.

T

3. Comparison of periodic balance sheets is useful for controlling the day-to-day

operations of a business.

F

4. In doing comparative horizontal analysis, the two terms used to describe changes from

one period to the next are absolute changes for percent differences, and relative

changes for dollar differences.

F

5. Common-size vertical income statements show each expense item as a percent of total

sales revenue.

T

6. The average check is calculated by dividing the number of customers served during a

period by the sales revenue for that period.

F

7. All other things being equal, it would be preferable to serve 4,000 guests each spending

$2.50, than 4,200 guests each spending $2.40.

F

8. If a net income of $825 was made at a banquet and 750 customers were served,

average net income per guest would be $1.10.

T

9. An analysis of trend results over time is usually more useful than looking at the results

for two consecutive periods only.

T

10. Trend results are often useful in forecasting future results.

T

11. A trend index for several periods usually assigns the current period figure the value of

100.

F

12. A trend index shows sales revenue has increased from Year 1 to Year 4 by 63%.

During the same period the accounts receivable trend index shows an increase of 75%.

This would normally be a desirable trend.

F

13. Comparison of operating results in times of inflation can be done quite easily without

adjusting for the effects of inflation.

F

38

14. To convert historic dollars to current dollars one multiplies historic dollars by the trend

index number for the historic period and then divides that result by the trend index

number for the current period.

F

15. Year 1 sales revenue is $240,000, and its trend index number is 120. Year 5 sales

revenue (current year) is $360,000 and its trend index number is 150. Year 1 sales

revenue converted to current dollars is $300,000.

T

16. An establishment can use internally generated information to produce its own series of

trend index numbers.

T

17. The calculation of percentage change figures for specific income statement items when

viewed over multiple periods can identify the direction in which a business is going.

T

18. Vertical analysis and trends analysis are similar forms used to conduct financial

statements analysis.

F

MULTIPLE CHOICE QUESTIONS

(Correct answer indicated by asterisk)

1. Financial statement analysis is carried out by:

(c) Management for the use of the tax department.

(d) Stockholders for the use of management.

2. Comparative horizontal balance sheets show the:

(a) Change in individual account balances in dollars from one period to the next.

(b) Change in individual account balances in percentage terms from one period to the next.

3. In doing comparative horizontal analysis:

(c) Total assets are given the value of 100%, and all other assets are expressed relative to

that.

(d) Relative changes show dollar differences and absolute changes show percent differences.

4. Common-size vertical income statements:

(c) Show net income as 100% and express all other items as a percentage of that.

(d) Show the change from last period’s income statement to this period’s in percentage

terms.

39

(c) Sales revenue for a period by the number of guests served during that period and

multiplying by 100.

(d) Annual sales revenue by 365 and multiplying by number of guests served.

6. Average guest check has increased from $12.50 to $14.00. Average operating income per

guest has increased from $1.00 to $1.50. From this information it is obvious that:

(a) Higher prices are driving away customers.

(b) More total net income is being made by the restaurant.

7. Sales revenue in Period 1 is $100,000 and food cost is 40%. Sales revenue in Period 2 is

$104,000 and food cost is 44%. The percent change in food cost percentage from Period 1 to

Period 2 is:

(a) 4%.

(b) $4,400

8. Sales revenue in Period 1 is $3,000 and in Period 2 it is $4,000. The trend index figure for

Period 2 (assuming Period 1 is given the value of 100) will be:

(a) 104.0

(b) 130.0

9. Sales revenue in Year 1 is $120,000 with a trend index number of 110. Sales revenue in Year

2 is $140,000 with a 121 trend index number. Year 1 sales revenue converted to current

dollars is:

(c) $151,000

(d) $110,000

10. A restaurant’s average check in Year 1 is $20.00, in Year 2 is $21.00, and in Year 3 is

$22.00. Using this as a basis, calculate the trend index numbers. The trend index numbers for

the three years respectively, would be:

(a) 120, 121, 122.

40

EXERCISE SOLUTIONS

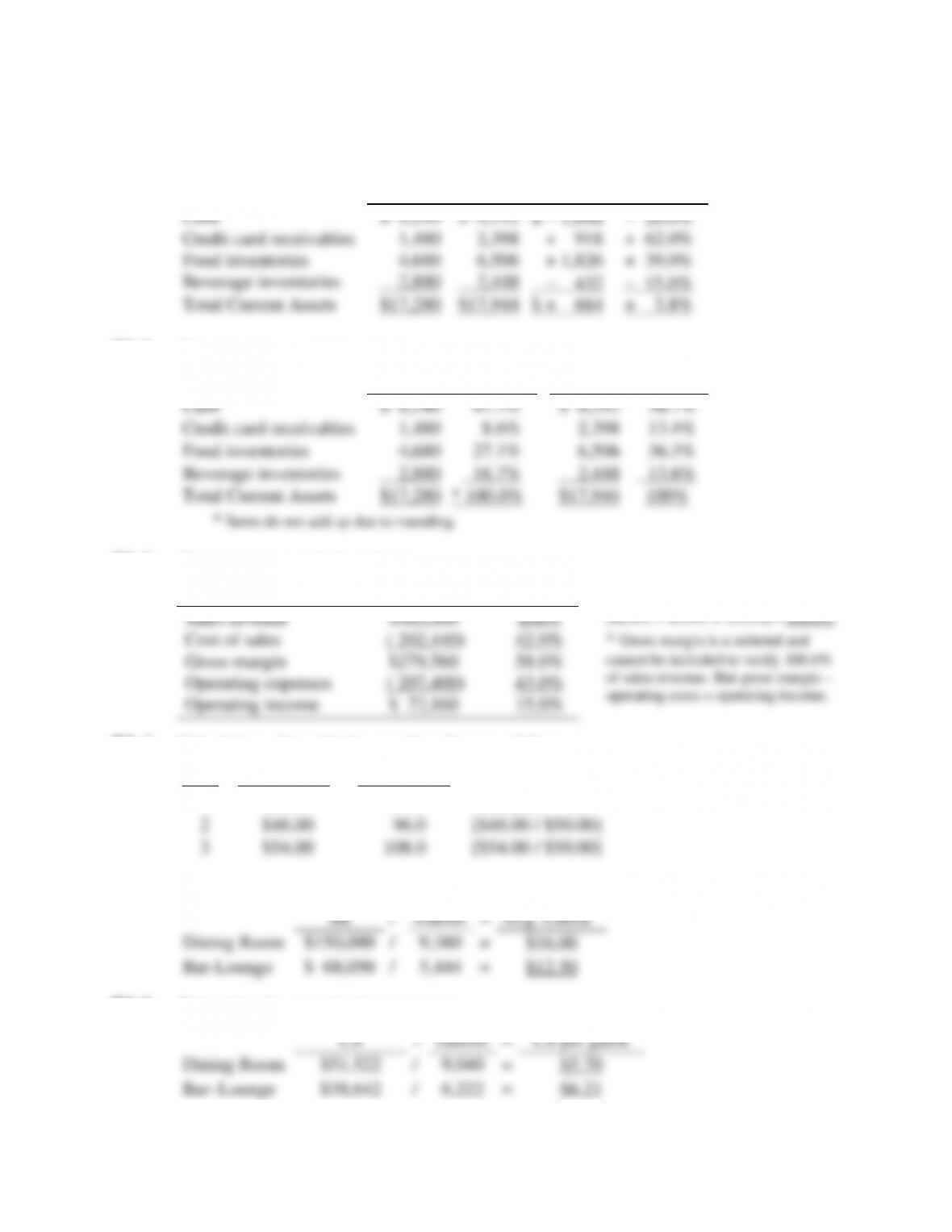

E3.1 Comparative horizontal analysis:

July

August

Change

Change %

Cash

$ 8,240

$ 6,592

$ − 1,648

− 20.0%

Credit card receivables

1,480

2,398

+ 918

+ 62.0%

Food inventories

4,680

6,506

+ 1,826

+ 39.0%

Beverage inventories

2,880

2,448

− 432

− 15.0%

Total Current Assets

$17,280

$17,944

$ + 664

+ 3.8%

E3.2 Common-size vertical analysis:

July

August

Cash

$ 8,240

47.7%

$ 6,592

36.7%

Credit card receivables

1,480

8.6%

2,398

13.4%

Food inventories

4,680

27.1%

6,506

36.3%

Beverage inventories

2,880

16.7%

2,448

13.6%

Total Current Assets

$17,280

* 100.0%

$17,944

100%

* Items do not add up due to rounding.

E3.3 Common-size vertical analysis:

Condensed Income Statement

Sales revenue

$482,000

100%

[42.0% + 43.0% + 15.0%] = 100.0%

Cost of sales

( 202,440)

42.0%

* Gross margin is a subtotal and

cannot be included to verify 100.0%

of sales revenue. But gross margin –

operating costs = operating income.

Gross margin

$279,560

58.0%

Operating expenses

( 207,400)

43.0%

Operating income

$ 72,160

15.0%

E3.4 Calculation of trend index numbers for two of three years.

Year

Room Rates

Trend Index

1

$50.00

100.0

Base year = 100

2

$48.00

96.0

[$48.00 / $50.00]

3

$54.00

108.0

[$54.00 / $50.00]

E3.5 Determine the average check per guest for two sales revenue divisions.

SR

/

Guests

=

Avg. Check

Dining Room

$150,080

/

9,380

=

$16.00

Bar-Lounge

$ 68,050

/

5,444

=

$12.50

E3.6 Determine the cost of sales per guest.

CS

/

Guests

=

CS per guest

Dining Room

$51,522

/

9,040

=

$5.70

Bar–Lounge

$38,642

/

6,222

=

$6.21

41

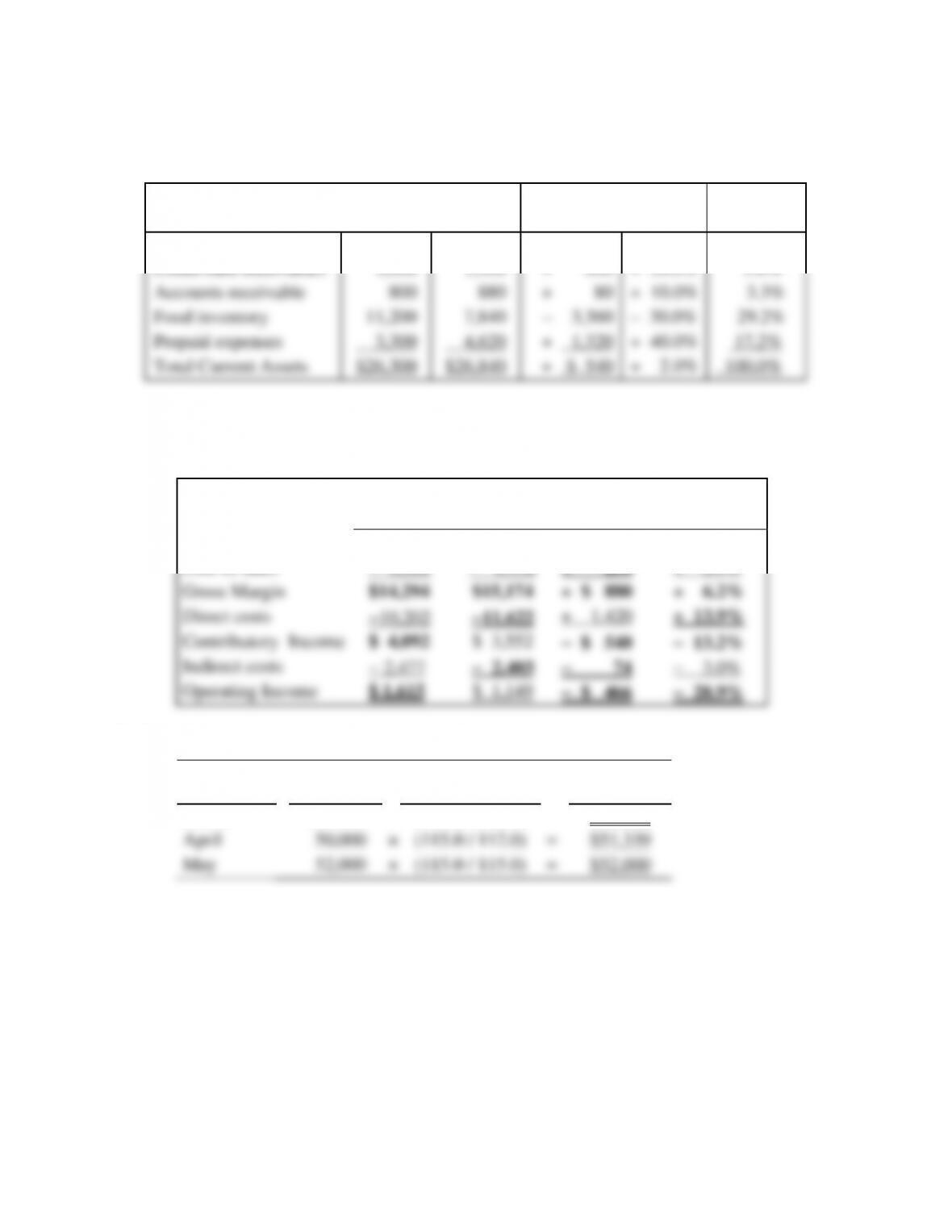

E3.7 Complete a horizontal analysis for Years 0007 to 0008 and a common-sized vertical

analysis for Year 0008.

Horizontal Analysis

Vertical

Current Assets

Yr. 0007

Yr. 0008

▲ Dollars

▲ %

Yr. 0008

Cash

$10,000

$12,000

+ $2,000

+ 20.0%

44.7%

Credit card receivables

1,000

1,500

+ 500

+ 50.0%

5.6%

Accounts receivable

800

880

+ 80

+ 10.0%

3.3%

Food inventory

11,200

7,840

– 3,360

– 30.0%

29.2%

Prepaid expenses

3,300

4,620

+ 1,320

+ 40.0%

17.2%

Total Current Assets

$26,300

$26,840

+ $ 540

+ 2.0%

100.0%

E3.8 Complete comparative horizontal statement analysis. Determine the missing dollar

values and the missing percentages; show the plus (+) or negative (–) effects.

Changes

Year 0007

Year 0008

Dollars

Percentage

Sales Revenue

$23,502

$24,612

+ $1,110

+ 4.7%

Cost of sales

− 9,208

− 9,438

+ 230

+ 2.5%

Gross Margin

$14,294

$15,174

+ $ 880

+ 6.2%

Direct costs

−10,202

−11,622

+ 1,420

+ 13.9%

Contributory Income

$ 4,092

$ 3,552

− $ 540

− 13.2%

Indirect costs

− 2,477

− 2,403

− 74

− 3.0%

Operating Income

$ 1,615

$ 1,149

− $ 466

− 28.9%

E3.9 Convert historic dollars to current dollars.

Year 0007

Month

Sales

Revenue

×

Conversion

=

Current

Dollars

March

$48,000

×

(115.0 / 110.0)

=

$50,182

April

50,000

×

(115.0 / 112.0)

=

$51,339

May

52,000

×

(115.0 / 115.0)

=

$52,000

42

PROBLEM SOLUTIONS

P3.1 Complete a comparative horizontal analysis of balance sheets for Years 0007 – 0008.

Comparative horizontal Analysis Year 0007 Year 0008

Assets

Dollar ▲

Percent ▲

Current Assets

Cash

+ 4,100

+ 36.3 %

Credit card receivables

+ 1,800

+ 40.0 %

Accounts Receivable

+ 7,800

+ 70.3 %

Vending Inventories

+ 900

+ 12.0 %

Prepaid Expenses

– 100

– 2.4 %

Total Current Assets

+ 14,500

+ 37.6 %

Property Plant & Equipment

Land

-0-

-0-

Building

+ 37,200

+ 4.9 %

Furnishings

+ 9,700

+ 11.6 %

Equipment

-0-

-0-

Accumulated Depreciation

+(20,300)

+ (6.4 %)

Glassware, linen inventories

+ 3,100

+ 25.4 %

Net Total Property & Equipment

+ 29,700

+ 4.2 %

Total Assets

+ 44,200

+ 5.9 %

Liabilities & Stockholders’ Equity

Current Liabilities

Accounts Payable

+ 3,000

+ 32.6 %

Accrued Expenses Payable

+ 750

+ 18.1 %

Taxes Payable

+ 3,350

+ 27.6 %

Current portion, mortgage payable

− 2,300

− 17.0 %

Total Current Liabilities

+ 4,800

+ 12.3 %

Long Term Liabilities

Mortgage payable

− 11,500

− 2.7 %

Total Liabilities

− 6,700

− 1.4 %

Stockholders’ Equity

Capital stock

+ 20,000

+ 16.0 %

Retained earnings

+ 30,900

+ 19.2 %

Total Stockholders’ Equity

+ 50,900

+ 17.8%

Total Liabilities & Stockholders’ Equity

+ 44,200

+ 5.9 %

Comments: Accounts receivable increased by 70.3% and total current assets increased by

37.6%. Credit issuing and collection policies need to be checked because they are risking an

increase in bad debt expense. Inventories of glassware and linen has increased by 25.4%.

Unless they recently received a shipment or had to purchase a large quantity because the

43

P3.2 Calculate a common-size vertical analysis of balance sheets for years 0007 – 0008

from P3.1.

Common-Size Vertical Balance Sheet Analysis

Assets

Year 0007

Year 0008

Current Assets

Cash

1.5%

1.9%

Credit card receivables

0.6%

0.8%

Accounts receivable

1.5%

2.4%

Vending inventories

1.0%

1.1%

Prepaid expenses

0.6%

0.5%

Total Current Assets

5.2%

6.7%

Property Plant and Equipment

Land

10.8%

10.2%

Building

101.2%

100.3%

Furnishings

11.2%

11.8%

Equipment

12.1%

11.4%

Accumulated Depreciation

(42.1%)

(42.3%)

Glassware, linen inventories

1.6%

1.9%

Net Property Plant and Equipment

94.8%

93.3%

Total Assets

100.0%

100.0%

Liabilities & Stockholders’ Equity

Current Liabilities

Accounts payable

1.2%

1.5%

Accrued expenses payable

0.6%

0.6%

Taxes payable

1.6%

2.0%

Current portion, mortgage payable

1.8%

1.4 %

Total Current Liabilities

5.2%

5.5%

Long Term Liabilities

Mortgage payable

56.6 %

52.0 %

Total Liabilities

61.8 %

57.5 %

Stockholders’ Equity

Capital stock

16.7%

18.3%

Retained earnings

21.5%

24.2%

Total Stockholders’ Equity

38.2%

42.5%

Total Liabilities & Stockholders’ Equity

100.0%

100.0%

in the accounts that the comparative horizontal analysis does. Total current assets increased

44

P3.3 a. Calculate the average check per guest for each operating division for August and

September.

Month of August

Month of September

Departmental

Sales

Avg.

Sales

Avg.

Divisions

Revenues

/

Guests

=

Check

Revenues

/

Guests

=

Check

Room Service

$ 22,600

/

927

=

$24.38

$ 18,000

/

756

=

$23.81

Dining room

118,500

/

4,628

=

25.61

95,500

/

3,765

=

25.37

Bar-Lounge

5,500

/

846

=

6.50

4,100

/

637

=

6.44

Coffee shop

53,400

/

9,709

=

5.50

48,700

/

8,604

=

5.66

Banquets

198,600

/

6,687

=

29.70

211,500

/

6,805

=

31.08

Totals

$398,600

/

22,797

=

$17.48

$377,800

/

20,567

=

$18.37

b. Calculation of average cost per guest and total average per guest for the months of

August and September.

Month of August

Month of September

Total

Total

Avg.

Total

Total

Avg.

Operating expenses

Cost

/

Guests

=

Cost

Cost

/

Guests

=

Cost

Cost of sales

$136,200

/

22,797

=

$ 5.97

$127,800

/

20,567

=

$ 6.21

Wages & salaries exp.

107,900

/

22,797

=

4.73

101,500

/

20,567

=

4.94

Benefits expenses

14,000

/

22,797

=

0.61

14,500

/

20,567

=

0.71

Linen expense

6,400

/

22,797

=

0.28

6,000

/

20,567

=

0.29

China expense

10,600

/

22,797

=

0.46

9,800

/

20,567

=

0.48

Supplies expense

9,800

/

22,797

=

0.43

9,400

/

20,567

=

0.46

Other expenses

19,200

/

22,797

=

0.84

17,600

/

20,567

=

0.86

Total expenses

$304,100

/

22,797

=

$13.34

$286,600

/

20,567

=

$13.93

* Items do not add up due to rounding in the average costs columns.

c. Determine the departmental income per guest for August and September.

Departmental Totals

August

September

Total sales revenue

$398,600

$377,800

Total operating expenses

( 304,100)

( 286,600)

Total operating income

$ 94,500

$ 91,200

Operating Income per Guest

$94,500 / 22,797 = $4.15

$91,200 / 20,567 = $4.43

* Items do not add up due to rounding in the average costs columns.

45

P3.4 Common-size vertical analysis of two similar restaurants:

Restaurant

“A”

Restaurant

“B”

Sales revenue

100.0%

100.0%

Cost of sales

( 39.0%)

(38.3%)

Gross Margin

61.0%

61.7%

Direct Expenses

Wages & salaries expense

29.6%

34.2%

Supplies expense

8.2%

8.2%

Other expenses

2.9%

3.0%

Total Direct Expenses

(40.7%)

(* 45.3%)

Contributory Income

20.3%

16.4%

Indirect Expenses

Rent expense

4.2%

4.4%

Insurance expense

1.3%

1.5%

Other indirect expenses

2.1%

1.7%

Total Indirect Expenses

( 7.6%)

( 7.6%)

Operating Income

12.7%

* 8.9%

* Items do not add up due to rounding

The operating income of “A” is 3.8% above “B” (12.7% − 8.9%). The difference in

operating income appears to be the cost of wages. “B” has a 4.6% higher wage cost than

A (34.2% − 29.6%). Since both “A” and “B” are in the same town, the cost of wages

should be evaluated further.

This situation can result from a difference in employee staffing, salaries and hourly

wage rates, which have been lumped into combined wages and salaries expense. It is

×

=

Current $

$ 96,200

×

(124.9

/

100.0)

=

$120,154

×

(124.9

/

113.8)

=

121,278

×

(124.9

/

118.8)

=

118,907

×

(124.9

/

121.2)

=

122,530

×

(124.9

/

124.9)

=

123,700

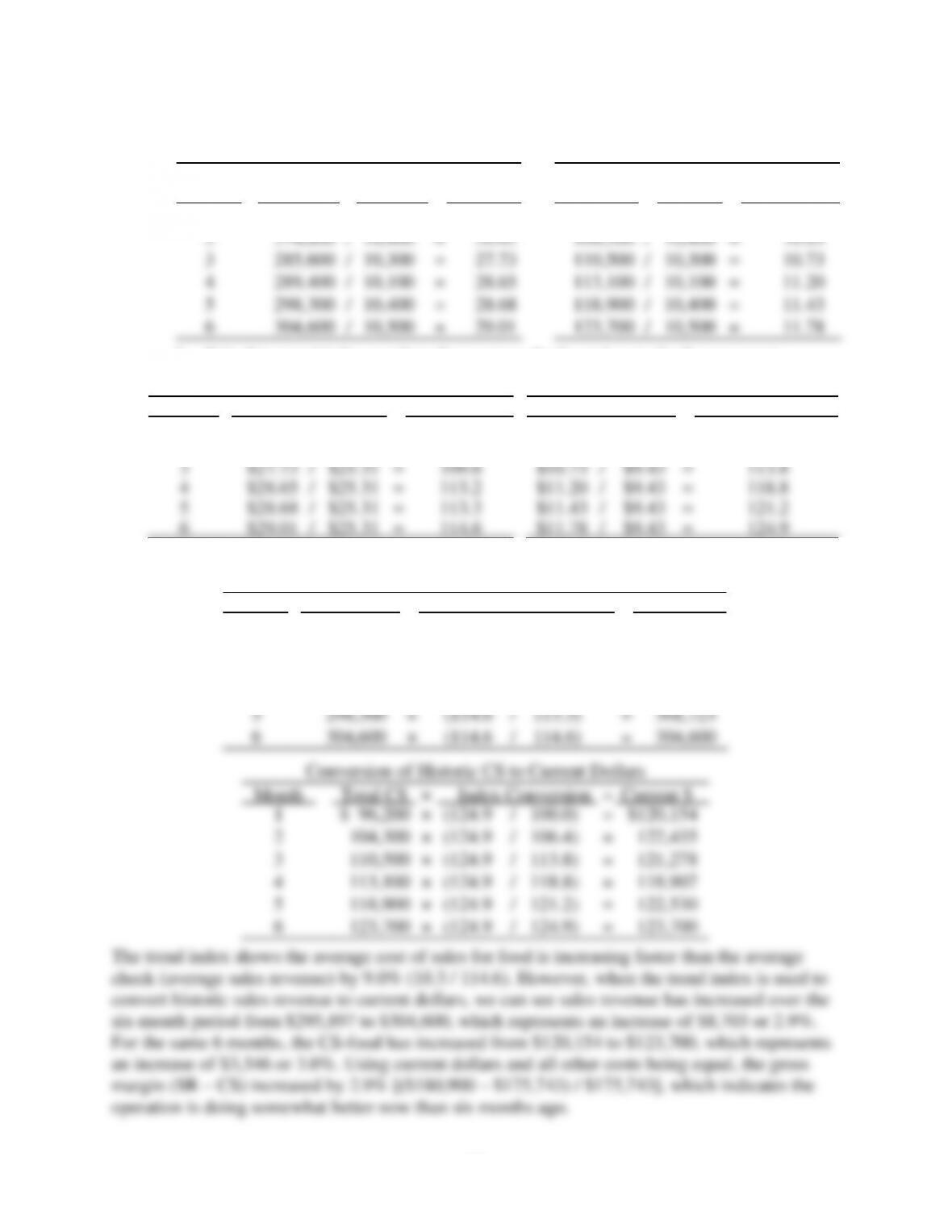

P3.5 a. Calculate the average check and average cost of sales food per guest.

Average Check per Guest

Average CS Food per Guest

Total

Avg.

Total

CS per

Month

SR

/

Guests

=

Check

CS

/

Guests

=

Guest

1

$258,200

/

10,200

=

$25.31

$ 96,200

/

10,200

=

$ 9.43

2

274,800

/

10,400

=

26.42

104,300

/

10,400

=

10.03

3

285,600

/

10,300

=

27.73

110,500

/

10,300

=

10.73

4

289,400

/

10,100

=

28.65

113,100

/

10,100

=

11.20

5

298,300

/

10,400

=

28.68

118,900

/

10,400

=

11.43

6

304,600

/

10,500

=

29.01

123,700

/

10,500

=

11.78

b. Calculate trend index numbers for average checks and cost of sales per guest.

Trend Index Calculations, Average Checks

Trend Index Calculations, CS per Guest

Month

Conversion

Trend Index

Conversion

Trend Index

1

$25.31

/

$25.31

=

100.0

$ 9.43

/

$9.43

=

100.0

2

$26.42

/

$25.31

=

104.4

$10.03

/

$9.43

=

106.4

3

$27.73

/

$25.31

=

109.6

$10.73

/

$9.43

=

113.8

4

$28.65

/

$25.31

=

113.2

$11.20

/

$9.43

=

118.8

5

$28.68

/

$25.31

=

113.3

$11.43

/

$9.43

=

121.2

6

$29.01

/

$25.31

=

114.6

$11.78

/

$9.43

=

124.9

c. Convert historic sales revenue and cost of sales to current dollars.

Conversion of Historic SR to Current Dollars

Month

Total SR

×

Trend Index Conversion

=

Current $

1

$258,200

×

(114.6

/

100.0)

=

$295,897

2

274,800

×

(114.6

/

104.4)

=

301,648

3

285,600

×

(114.6

/

109.6)

=

298,629

4

289,400

×

(114.6

/

113.2)

=

292,979

5

298,300

×

(114.6

/

113.3)

=

301,723

6

304,600

×

(114.6

/

114.6)

=

304,600

47

P3.6 a. Prepare a room rate index trend based on average room rates.

Conversion of room rates to Trend Index numbers

Year

Room Rates

/

Rm. Rate Yr. 1

=

Trend Index Numbers

1

$75.00

/

$75.00

=

100.0

2

76.30

/

75.00

=

101.7

3

77.60

/

75.00

=

103.5

4

78.50

/

75.00

=

104.7

5

79.90

/

75.00

=

106.5

b. Using room rate trend index numbers, convert annual SR to current dollars.

Conversion of Historic Sales Revenue to Current Dollars

Year

Annual SR

Conversion Equation

Current $

1

$1,401,429

×

(106.5

/

100.0)

=

$1,492,522

2

1,429,367

×

(106.5

/

101.7)

=

1,496,830

3

1,480,552

×

(106.5

/

103.5)

=

1,523,467

4

1,520,700

×

(106.5

/

104.7)

=

1,546,844

5

1,553,091

×

(106.5

/

106.5)

=

1,553,091

current dollars. Given this limited analysis, a review of cost of sales and operating costs

should also be carried out.

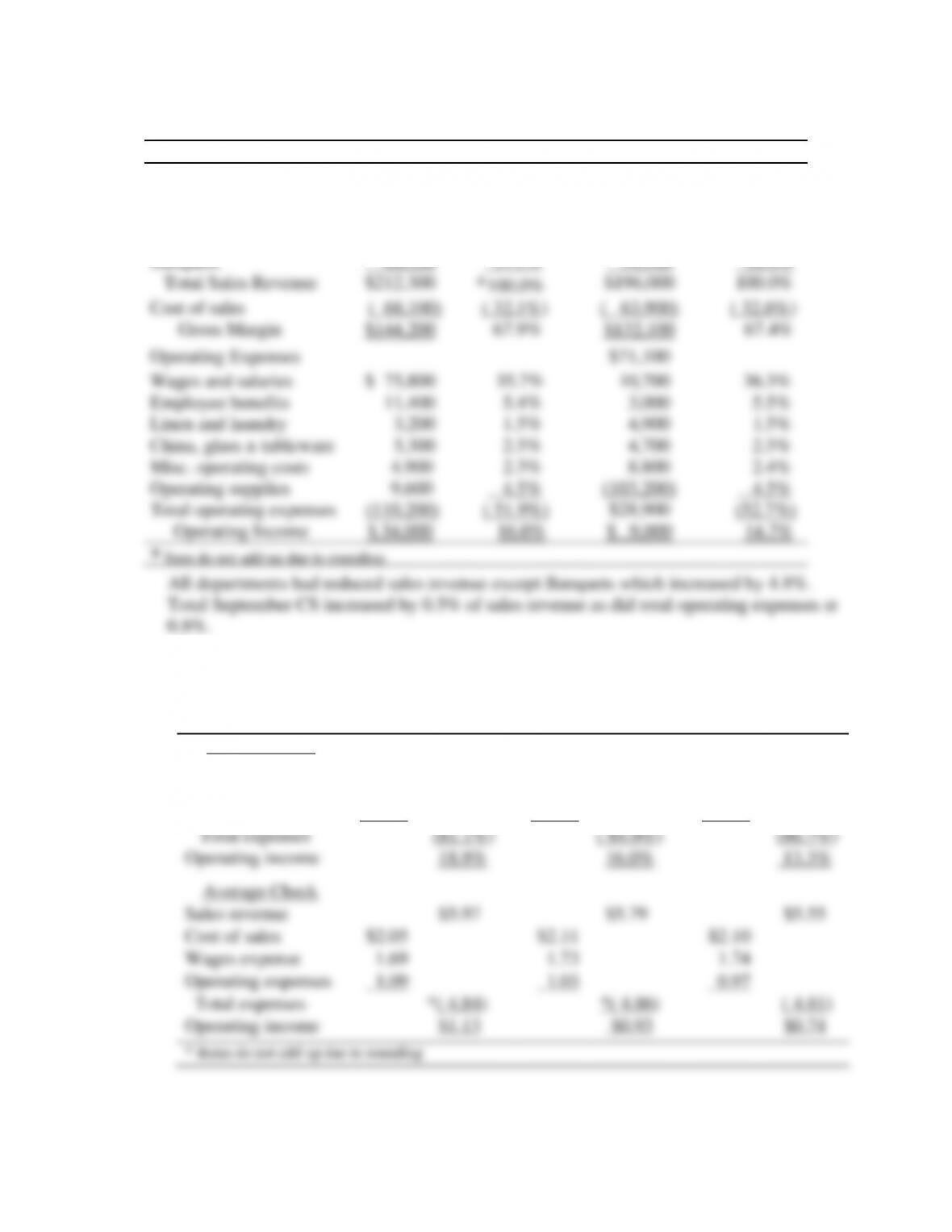

P3.7 Complete a balance sheet comparative horizontal analysis for August and September

Sales Revenue

August

September

Dollar ▲

% ▲

Room service

$ 11,300

$ 9,000

−

2,300

−

20.4%

Dining room

75,900

63,700

−

12,200

−

16.1%

Bar-lounge

5,500

4,100

−

1,400

−

25.5%

Coffee shop

53,400

48,700

−

4,700

−

8.8%

Banquets

66,200

70,500

+

4,300

+

6.5%

Total sales revenue

$212,300

$196,000

−

16,300

−

7.7%

Cost of Sales

( 68,100)

( 63,900)

−

( 4,200)

−

( 6.2%)

Gross Margin

$144,200

$132,100

−

12,100

−

8.4%

Operating Expenses

Wages and salaries

$ 75,800

$71,100

−

4,700

−

6.2%

Employee benefits

11,400

10,700

−

700

−

6.1%

Linen and laundry

3,200

3,000

−

200

−

6.3%

China, glassware & tableware

5,300

4,900

−

400

−

7.5%

Miscellaneous operating costs

4,900

4,700

−

200

−

4.1%

Operating supplies

9,600

8.800

−

800

−

8.3%

Total operating expenses

(110,200)

(103,200)

−

(7,000)

−

( 6.4%)

Operating Income

$ 34,000

$28,900

−

5,100

−

15.0%

Only Sept. banquets SR increased; SR, CS, GM, operating expenses, and operating income.

48

P3.8 Using P3.7 information, complete common-size vertical income statement analysis.

Sales Revenue

August

September

Room service

$ 11,300

5.3%

$ 9,000

4.6%

Dining room

75,900

35.8%

63,700

32.5%

Bar-lounge

5,500

2.6%

4,100

2.1%

Coffee shop

53,400

25.2%

48,700

24.8%

Banquets

66,200

31.2%

70,500

36.0%

Total Sales Revenue

$212,300

*100.0%

$196,000

100.0%

Cost of sales

( 68,100)

( 32.1%)

( 63,900)

( 32.6%)

Gross Margin

$144,200

67.9%

$132,100

67.4%

Operating Expenses

$71,100

Wages and salaries

$ 75,800

35.7%

10,700

36.3%

Employee benefits

11,400

5.4%

3,000

5.5%

Linen and laundry

3,200

1.5%

4,900

1.5%

China, glass & tableware

5,300

2.5%

4,700

2.5%

Misc. operating costs

4,900

2.3%

8.800

2.4%

Operating supplies

9,600

4.5%

(103,200)

4.5%

Total operating expenses

(110,200)

( 51.9%)

$28,900

(52.7%)

Operating Income

$ 34,000

16.0%

$ 9,000

14.7%

* Item do not add up due to rounding

All departments had reduced sales revenue except Banquets which increased by 4.8%.

Total September CS increased by 0.5% of sales revenue as did total operating expenses at

0.8%.

P3.9 Convert the consolidated income statements to common-size vertical analysis income

statements and determine the average check for each month.

April

May

June

Sales Revenue

100.0%

100.0%

100.0%

Cost of sales

34.4%

36.4%

37.9%

Wages expense

28.4%

29.8%

31.3%

Operating expenses

18.3%

17.8%

17.5%

Total expenses

(81.1%)

( 84.0%)

(86.7%)

Operating income

18.9%

16.0%

13.3%

Average Check

Sales revenue

$5.97

$5.79

$5.55

Cost of sales

$2.05

$2.11

$2.10

Wages expense

1.69

1.73

1.74

Operating expenses

1.09

1.03

0.97

Total expenses

*( 4.84)

*( 4.86)

( 4.81)

Operating income

$1.13

$0.93

$0.74

* Items do not add up due to rounding

49

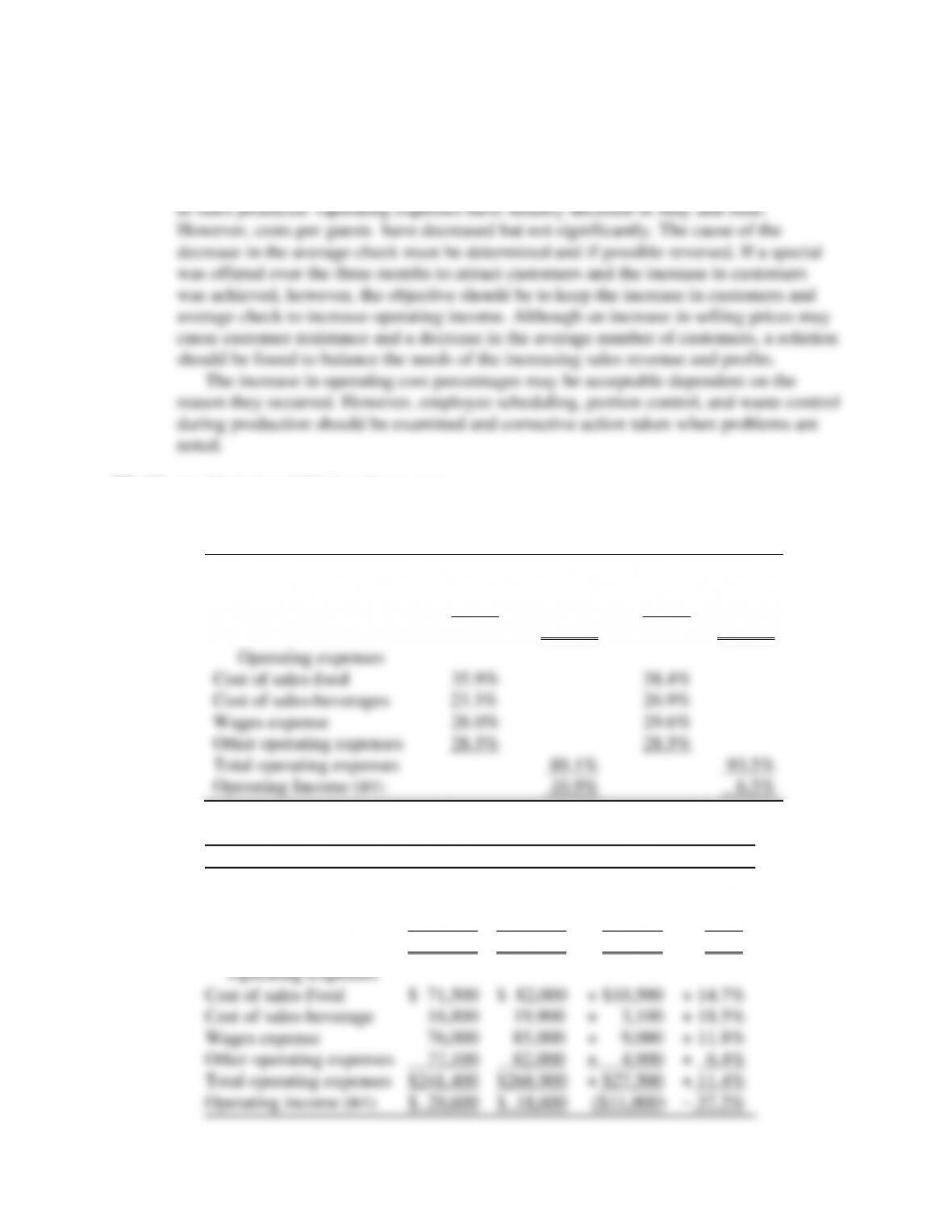

The trend percentages for this operation need to be investigated. The number of guests

has increased considerably from April (May was 4,200 and 5,500 in June) over the 3

months beginning in April. The sales revenue and operating income per guest have both

declined in May and June; however, cost of sales and wages expense increased relative

P3.10 Freddie’s Fried Chicken Restaurant:

a. Prepare a common-size vertical analysis income statement for 2 months.

April Percentages

May Percentages

Sales Revenue

Sales revenue-food

73.4%

74.3%

Sales revenue-beverages

26.6%

25.7%

Total Sales Revenue

100.0%

100.0%

Operating expenses

Cost of sales-food

35.9%

38.4%

Cost of sales-beverages

23.3%

26.9%

Wages expense

28.0%

29.6%

Other operating expenses

28.5%

28.5%

Total operating expenses

89.1%

93.5%

Operating Income (BT)

10.9%

6.5%

b. Prepare a comparative horizontal analysis income statement.

April

May

$ Change

% Change

Sales Revenue

Sales revenue-food

$199,000

$213,500

+ $14,500

+ 7.3%

Sales revenue-beverages

72,000

74,000

+ 2,000

+ 2.8%

Total Sales Revenue

$271,000

$287,500

+ $16,500

+ 6.1%

Operating Expenses

Cost of sales-Food

$ 71,500

$ 82,000

+ $10,500

+ 14.7%

Cost of sales-beverage

16,800

19,900

+ 3,100

+ 18.5%

Wages expense

76,000

85,000

+ 9,000

+ 11.8%

Other operating expenses

77,100

82,000

+ 4,900

+ 6.4%

Total operating expenses

$241,400

$268,900

+ $27,500

+ 11.4%

Operating income (BT)

$ 29,600

$ 18,600

($11,000)

– 37.2%

50

c. Calculate the average check, cost and operating income per guest.

April

May

[20,000 Guests]

[22,000 Guests]

Sales revenue

Sales revenue–food

$9.95

$9.70

Sales revenue–beverages

3.60

3.36

Total Sales Revenue

$13.55

*$13.07

Operating expenses

Cost of sales–food

$3.58

$3.73

Cost of sales–beverages

0.84

0.90

Wages expense

3.80

3.86

Other operating expenses

3.86

3.73

Total operating expenses

*(12.07)

(12.22)

Operating Income [BT]

$ 1.48

$ 0.85

* Items do not add up due to rounding

d. Comments:

In May the restaurant has 10% or 2,000 (22,000 − 20,000 / 20,000) more guests,

May sales revenue increased slightly by 6.1% or $16,500 [($287,500 – $271,000) /

$271,500]. However, total average check per guest decreased by $0.48 cents ($13.55

guests to buy more or menu items with a higher gross margin percentage and

therefore increase the average check?

The average cost per guest has also increased except for other operating costs.

Freddie needs to investigate why costs have increased. If there are control problems

such as portion control, wasted food, poor quality products, or the employees are not

being productive, then Freddie needs to take corrective action. If costs have

increased and there is no waste, consideration must be given to raising the menu

51

P3.11 Calculate sales revenue average check, expenses and operating income on a per guest

basis. Comment on the dinning room’s operating results.

Sales Revenue

October

November

Sales revenue-Food

$31.09

$30.90

Sales revenue-Beverages

13.08

15.37

Total sales revenue

$22.43

$23.44

Operating Expenses

Cost of sales-Food

$11.84

$11.15

Cost of sales-Beverage

3.93

4.72

Wages expense

6.12

6.11

Other operating expenses

4.00

4.04

Total operating expenses

(18.15)

(18.21)

Department Operating Income (BT)

$ 4.28

$ 5.23

While the total sales revenue in November increased slightly by $592 ($119,273 –

$118,681) the number of guests have decreased by 201 (5290 – 5089). In addition, the

November departmental operating income has increased $3,958 ($26,608 – $22,650)

and the operating income per guest was $0.95 ($5.23 – $4.28). A change in sales mix

increases departmental operating income. Both labor costs and other costs are the same

per guest in both months.

The manager of the dining room needs to determine why the number of guests has

decreased. This decrease could be a normal seasonal decrease or it could also be the

52

P3.12 Calculation of trend percentages:

Period

SR Food

Trend %

CS Food

Trend %

A/R

Trend %

1

$210,200

$60,330

$20,020

2

233,322

11.0%

72,275

19.8%

24,200

20.9%

3

243,821

4.5%

81,400

12.6%

25,800

6.6%

4

253,574

4.0%

84,200

3.4%

27,400

6.2%

5

267,521

5.5%

90,768

7.8%

31,400

14.6%

6

273,406

2.2%

93,128

2.6%

33,600

7.0%

Calculations of food sales revenue trend percentages

Pd 1: $210,200

Pd 2: $233,322 – $210,200 = $23,122 / $210,200 = 11.0%

Pd 3: $243,821 – $233,322 = $10,499 / $233,322 = 4.5%

Pd 4: $253,574 – $243,821 = $ 9,753 / $243,821 = 4.0%

Pd 5: $267,521 – $253,574 = $13,947 / $253,574 = 5.5%

Pd 6: $273,406 – $267,521 = $ 5,885 / $267,521 = 2.2%

Calculations of cost of sales trend percentages

Pd 1: $60,330

Pd 2: $72,275 – $60,330 = $11,945 / $60,330 = 19.8%

Pd 3: $81,400 – $72,275 = $ 9,125 / $72,275 = 12.6%

Pd 4: $84,200 – $81,400 = $ 2,800 / $81,400 = 3.4%

Pd 5: $90,768 – $84,200 = $ 6,568 / $84,200 = 7.8%

Pd 6: $93,128 – $90,768 = $ 2,360 / $90,768 = 2.6%

Calculations of accounts receivable percentages

Pd 1: $20,020

Pd 2: $24,200 – $20,020 = $4,180 / $20,020 = 20.9%

Pd 3: $25,800 – $24,200 = $1,600 / $24,200 = 6.6%

Pd 4: $27,400 – $25,800 = $1,600 / $25,800 = 6.2%

Pd 5: $31,400 – $27,400 = $4,000 / $27,400 = 14.6%

Pd 6: $33,600 – $31,400 = $2,200 / $31,400 = 7.0%

The rate at which sales is increasing has slowed down over time from period 2 which

had a 11.0% increase and the sales revenue slowed down to 2.2% at the end of period 6;

the average increase from period 3 to period 6 was 4.05%. Food cost is increasing more

quickly than the food sales from 19.8% in period 2 to 2.6% in period 6; the average

increase of 9.24% from period 2 to period 6. Accounts receivable are increasing at a

faster rate than food cost. Accounts receivable increased from 20.9% period 2 to 7.0% at

the end of period 6. These trends are not desirable. The need exists to investigate the

reason for the slow down in the growth of sales and see if we can increase sales more in

the future. We need to check on food control to find out if food is being wasted or if

there is a problem with purchasing. If we find any problems, we need to correct them.

The increasing accounts receivable increases the risk of bad debt expense. We need to

check and make sure that accounts receivable collection procedures are being followed

and correct any problems we find.

53

P3.13 Conversion of historic sales revenue and cost of sales to current dollars for the six periods

referred to in P3.12.

Historic

Conversion

Current

Period

SR Food

×

Equation

=

Dollars

1

$210,200

×

147.0 / 107.0

=

$288,779

2

233,322

×

147.0 / 114.0

=

300,863

3

243,821

×

147.0 / 121.0

=

296,212

4

253,574

×

147.0 / 130.0

=

286,734

5

267,521

×

147.0 / 144.0

=

273,094

6

273,406

×

147.0 / 147.0

=

273,406

Historic

Conversion

Current

Period

Food Cost

×

Equation

=

Dollars

1

$60,330

×

151.0 / 121.0

=

$75,288

2

72,275

×

151.0 / 125.0

=

87,308

3

81,400

×

151.0 / 131.0

=

93,827

4

84,200

×

151.0 / 137.0

=

92,804

5

90,768

×

151.0 / 144.0

=

95,180

6

93,128

×

151.0 / 151.0

=

93,128

P3.14 a. Calculate index numbers from the average room rates using the first period as the

base index number.

Room

First

Index

Year

Rate

Year

Numbers

1

$85.00

/

$85.00

=

100.0

2

88.60

/

85.00

=

104.2

3

89.70

/

85.00

=

105.5

4

91.40

/

85.00

=

107.5

5

93.80

/

85.00

=

110.4

54

b. Using the index numbers from part a., convert the annual sales revenue of year 1

through year 5 to current dollars, and comment on your analysis.

Conversion of Annual Sales Revenue

Historic

Conversion

Current

Year

Dollars

×

Equation

=

Dollars

1

$2,205,952

×

(110.4 / 100.0)

=

$2,435,371

2

2,254,695

×

(110.4 / 104.2)

=

2,388,851

3

2,299,526

×

(110.4 / 105.5)

=

2,406,328

4

2,334,484

×

(110.4 / 107.5)

=

2,397,461

5

2,380,856

×

(110.4 / 110.4)

=

2,380,856

55

CASE 3 SOLUTIONS

a. 4 C Company

Common-Size (Vertical) Income Statement

For the Year Ended December 31, 2007

Sales Revenue

Food Operations [$458,602 / $639,111]

71.8%

Beverage Operations [$180,509 / $639,111]

28.2%

Total Sales Revenue

100.0%

Cost of Sales

Cost of Sales Food [$181,323 / $458,602]

39.5%

Cost of Sales Beverages [$39,303 / $180,509]

21.8%

Total Cost of Sales [$220,626 / $639,111]

(34.5%)

Gross Margin [$418,485 / $639,111]

65.5%

Operating Expenses

Salaries and Wages expense [$223,543 / $639,111]

35.0%

Laundry expense [$16,609 / $639,111]

2.6%

Kitchen Fuel expense [$7,007 / $639,111]

1.1%

China and tableware expenses [$12,214 / $639,111]

1.9%

Glassware expense [$1,605 / $639,111]

0.3%

Contract Cleaning expense [$5,906 / $639,111]

0.9%

Licenses expense [$3,205 / $639,111]

0.5%

Other Operating expenses [$4,101 / $639,111]

0.6%

Administrative-General expenses [$15,432 / $639,111]

2.4%

Marketing expense [$6,917 / $639,111]

1.1%

Energy expense [$7,918 / $639,111]

1.2%

Insurance expense [$1,895 / $639,111]

0.3%

Rent expense [$24,000 / $639,111]

3.8%

Interest expense [$23,981 / $639,111]

3.8%

Depreciation expense [$20,124 / $639,111]

3.1%

Total Operating Expenses [$374,457 / $639,111]

(58.6%)

Operating Income [$44,028 / $639,111]

6.9%

Income tax expense [$9,686 / $639,111]

( 1.5%)

Net Income [$34,342 / $639,111]

5.4%

For similar type restaurants, the range of operating income (income before tax) ranges from a

low of 1.5% to a high of 12.0% of sales revenue. 4C Company’s operating income of 6.9%

appears to be acceptable since it is slightly above the mid range of 6.75%. Since this is the

first year of operations for 4C Company, there may be current costs that will not be repeated

in future years. Therefore, one may expect operating income to increase next year. It will

take time to see growth toward achieving full sales revenue potential.

56

b. The average check for food is $6.88 ($458,602 / 66,612) and average total sales revenue per

4C Company is split at 71.8% for food and 28.2% for beverages and the percentages are in

line with industry averages for this type of restaurant.

c. Cost of Sales Food is [Cost of sales food / Total sales revenue food]:

$181,323 / $458,602 = 39.5% (The mid range is 35%)

better value. If the guests think they are getting good value for their money, they may buy

more beverages and thus, increase total gross margin. Since beverages take very little labor to

produce, he is unlikely to increase labor costs. If Charlie can increase average check, he will

increase his gross margin and, therefore, his operating income.

d. It is generally preferred to have a higher percentage of beverage sales revenue to food sales

revenue, since beverage cost of sales is lower per dollar of sales revenue generated. A lower