19

CHAPTER 2

UNDERSTANDING FINANCIAL STATEMENTS

INTRODUCTION

For students who have recently completed an introductory accounting course most of this chapter

will be review material. However, the chapter explains financial statements in the specific terms

used by hospitality industry enterprises; terms that may not be learned in a general business

accounting course. Departmental income statements are discussed with emphasis on the

calculation of cost of sales for food and beverages as well as the sales revenue mix. Changes in

sales revenue mix between departments may affect the overall net income of the business

enterprise. If course time does not permit complete coverage of the material in this chapter, it

should at least be assigned for self-study. This chapter, along with Chapter 1, provides the

foundation for most of the remaining chapters in the textbook.

TRUE OR FALSE QUESTIONS

(Correct answer indicated by T for True answers and F for False answers)

1. Financial statements provide information useful to management for decision-making.

T

2. The uniform system of accounts ensures that the financial statement figures of an

individual establishment are the same as national average figures.

F

3. The income statement gives a picture of the financial position of a business at a point

in time.

F

4. Departmental income statements are typical of the hotel industry.

T

5. Direct expenses are generally the responsibility of, and controllable by the department

head concerned.

T

6. The term FIFO stands for first-in, first-ordered.

F

7. When a hotel practices responsibility accounting, departments can be identified as

either cost centers or production centers.

F

8. Contributory income is the income for a department, after indirect expenses have

been deducted.

F

9. Indirect expenses should be allocated to the various departments only on a ratio of

departmental sales revenue to total sales revenue basis.

F

10. Indirect expenses are usually controllable by department managers.

F

11. A department with a high contributory income percent will, with an increase in sales

revenue, yield more net income to the overall establishment, than would a department

with a lower contributory income percentage having the same sales revenue increase.

T

12. The balance sheet shows the operating results of a business over a specific period.

F

20

13. Marketable and short-term securities are current assets.

T

14. A hotel’s inventory of china, glass, and silver is usually shown as a current asset.

F

15. The two common methods of balance sheet presentation are known as the account

form and the T form.

F

16. Accumulated depreciation, like the allowance for uncollectible accounts, is a form of

contra accounts shown on the balance sheet.

T

17. The unexpired portion of a long-term lease paid in advance should be shown as an

asset.

T

18. Credit balances on guests’ accounts receivable should be shown on the balance sheet

as a reduction of accounts receivable.

F

19. A mortgage is a type of long-term liability.

T

20. Paid in capital, excess of par is the amount by which the present value of a fixed asset

exceeds its original purchase price.

F

21. The only type of stock issued by hotel companies is common stock.

F

22. Retained earnings represent the accumulation of net incomes, less losses, and

dividends, since a company started.

T

23. Retained earnings are part of the income statement.

F

24. Retained earnings are the link between the income statement and the balance sheet.

T

25. The liability and equity sections of a balance sheet show how the company’s assets

are currently financed.

T

26. Ownership withdraws and dividends to stockholders’ are contra accounts.

T

27. A trial balance that is not in balance always indicates an error exists.

T

MULTIPLE CHOICE QUESTIONS

(Correct answer indicated by asterisk)

1. A direct expense is:

(a) controllable by the accountant employed by the business

(b) deducted from a department’s contributory income

2. Contributory incomes are:

(c) sales revenues less indirect expenses

(d) income before income tax

21

3. Net cost of sales food is calculated by adjusting cost of sales food by:

(c) adding opening and closing inventory to purchases

(d) adding transfers in, adding employee meals, and deducting transfers out

4. Gross margin is:

(a) income before income tax

(b) sales revenue less indirect expenses

5. Which of the following is not an inventory valuation method?

(a) Specific item cost

(b) FIFO

6. A decentralized departmental operation where managers are made accountable for their

performance and the performance of employees in their department is known as:

(c) performance accounting

(d) accounting decentralization

7. indirect expenses:

(a) should be allocated to the operating departments on a square foot basis

(b) should be allocated to the operating departments based on sales revenue

8. departmental sales revenue mix refers to the:

(c) ratio of direct expenses allocated to departments based on sales revenue

(d) deduction of indirect expenses from a department’s sales revenue to arrive at contributory

income

9. Which of the following is not normally considered a current asset in a hotel?

(c) Prepaid expense

(d) Marketable securities

(c) not shown as an expense if the company has a loss

(d) not shown as an expense until the company is liquidated

22

11. Deposits sent in by hotel room guests to hold rooms for some future period are shown on the

balance sheet as a (an):

(a) asset

(b) reduction of accounts receivable

12. paid in capital, excess of par or stated value (capital surplus) is:

(c) net income less net losses of the business since it began

(d) the difference between current market value of fixed or capital assets and the original cost

price

13. retained earnings are:

(c) reduced by any deficits before being recorded on the balance sheet

(d) represented by an equivalent amount of cash in the bank

14. Beginning retained earnings were $86,300. During the year, the company had a net loss of

$10,200 and paid dividends of $16,800. Ending retained earnings are:

(a) $92,900

15. The two basic formats of balance sheet presentation are the:

(a) “T” account form and report form

16. Catering equipment was purchased at a cost of $24,400 that has an estimated life of 10 years

and a residual value of $1,400. Using double-declining balance, calculate the depreciation

(c) $3,680

(d) $4,600

EXERCISE SOLUTIONS

E2.1 To be classified as a current asset account, inventories must be purchased for resale.

E2.2 The key word is Traceable. Direct costs are said to be directly traceable, and indirect

costs are considered non-traceable to a specific operating department.

E2.3 Determine the value of the ending inventory and cost of sales for M & B for March

using: a. FIFO, b. LIFO, and c. Weighted average methods.

March 02: 12 units @ $12.50 = $150.00 March sales were: 32 units sold

E2.4 Find the missing purchases in an additive sequence by reversing the additive function:

Beginning Inventory

+

Purchases

−

Ending Inventory

=

Cost of Sales

$38,000

+

$88,000

−

$24,000

=

$102,000

E2.5 Beginning retained earnings (BRE) were $146,000 and during the year, cash dividends

of $100,000 were paid to the owners. NI for the year was $228,000. Determine the

ending retained earnings (ERE) using NI and NL.

a.

BRE

+

NI

−

Dividends

=

ERE

$146,000

+

$228,000

−

$100,000

=

$274,000

b.

BRE

+

NL

−

Dividends

=

ERE

$146,000

−

$12,200

−

$100,000

=

$33,800

E2.6 Sales revenue reported is $128,800 and direct costs of $68,200.

Determine: a. contributory income and b. contributory income percentage.

24

E2.7 A department has two operating divisions: Food service with sales revenue of $880,000

and a bar-lounge with sales revenue of $440,840. Calculate the sales revenue of each

division as a percentage of total departmental sales revenue.

E2.8 Match each of the terms to account categories.

a. Total assets − Total liabilities 4. Owners’ equity (Net assets)

E2.9 Allocate Indirect undistributed cost on the basis of square footage to two departments.

(Cost / Allocation % = the amount allocated)

Department 1: Basis, Sq. footage: $14,000 × 54% = $7,560

E2.10 Find the sales revenue percentage of four different divisions of a department based on

total sales revenue.

Departmental Sales Revenue

/

Total SR

=

SR Percentages

Rooms:

$1,555,632

/

$2,880,800

=

54.0%

Food service:

921,856

/

$2,880,800

=

32.0%

Beverage:

403,312

/

$2,880,800

=

14.0%

Total sales revenue $2,880,800

100.0%

E2.11 A food division had beginning inventory of $4,400, purchases of $8,400 and ending

inventory of $2,880. Determine the cost of goods available and cost of sales (CS):

BI + Purchases = Goods available − EI = CS

E2.12 Cost of sales (CS) is $198,680. Employee meals were $1,225 and complimentary meals

$142. Transfers-in was $82. Determine net cost of sales.

CS − Employee meals − Complimentary meals + Transfers-in = Net CS

E2.13 Sales revenue food division was $337,218 and the sales revenue for the bar lounge was

$206,682. Allocate $52,400 of indirect to each division on the basis of sales revenue.

[Food %: $337,218 / $543,900 = 62.0% Bar %: $206,682 / $543,900 = 38.0%]

25

E2.14 Assume the following: Beginning retained earnings (BRE) were $125,000, ending

retained earnings (ERE) were $150,000, and cash dividends of $77,000 were paid

during the year. What was net income for the year?

BRE

+

NI

−

Dividends

=

ERE

$125,000

+

?

−

$77,000

=

$150,000

ERE

+

Dividends

−

BRE

=

NI

$150,000

+

$77,000

−

$125,000

=

$102,000

Proof:

BRE

+

NI

−

Dividends

=

ERE

$125,000

+

$102,000

−

$77,000

=

$150,000

PROBLEM SOLUTIONS

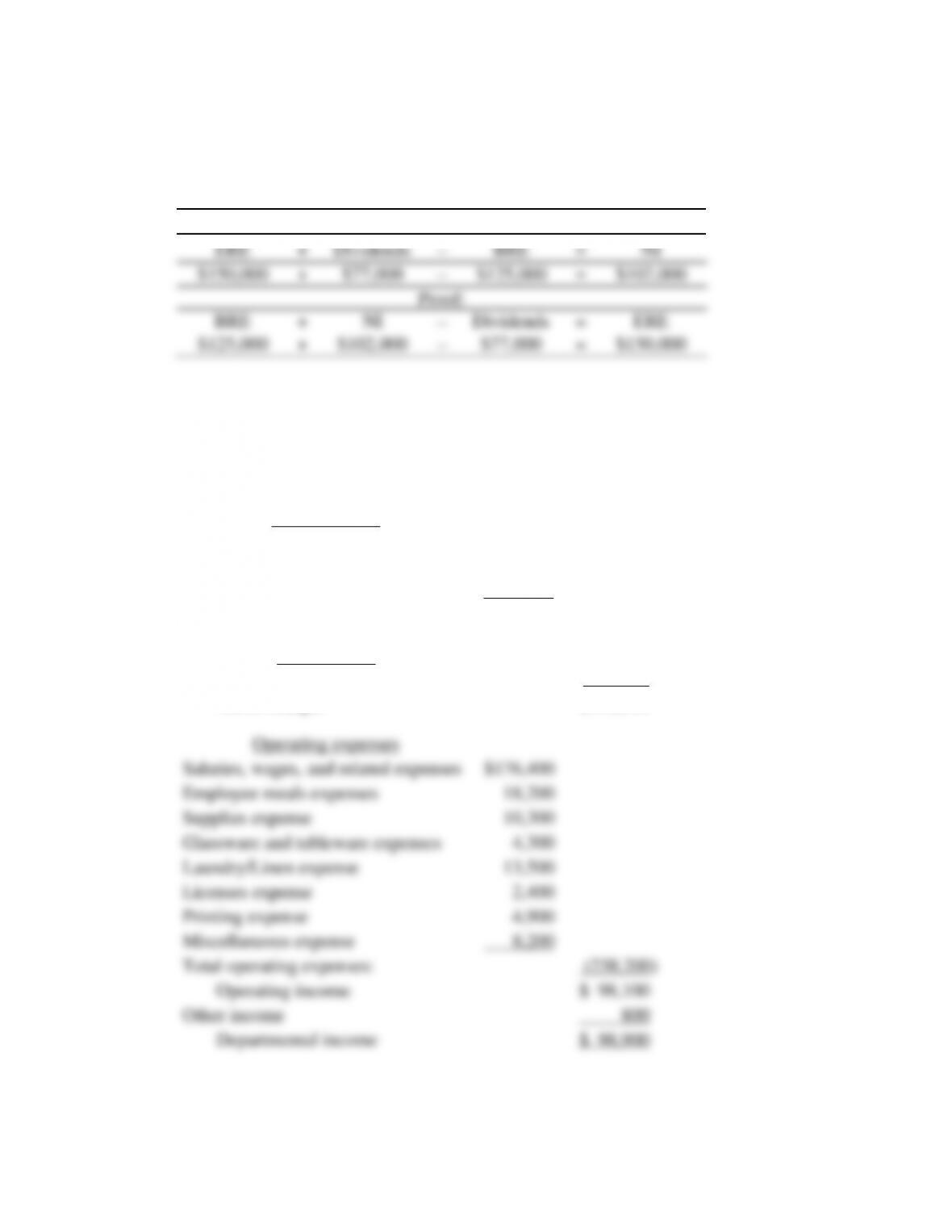

P2.1 Food Department

Income Statement

For the first Quarter ended March 31, 0007

Sales Revenue

Grill Room

$183,200

Coffee Garden

82,900

Banquets

294,400

Total Sales Revenue:

$560,500

Cost of Sales

Net food costs:

224,200)

Gross Margin

$336,300

Operating expenses

Salaries, wages, and related expenses

$176,400

Employee meals expenses

18,200

Supplies expense

10,300

Glassware and tableware expenses

4,300

Laundry/Linen expense

13,500

Licenses expense

2,400

Printing expense

4,900

Miscellaneous expense

8,200

Total operating expenses:

(238,200)

Operating income

$ 98,100

Other income

800

Departmental income

$ 98,900

P2.2 Calculate cost of sales food, and net cost of sales.

Beginning inventory

$2,782

Purchases

9,807

Goods available

$12,589

Less: Ending inventory

( 2,612)

Cost of sales (food)

$ 9,977

Less: Employee meals

219

Less: Promotional meals

288

( 507)

Cost of sales (net)

$ 9,470

P2.3 Calculate cost of sales food and net cost of sales.

Beginning inventory

$15,357

Purchases

47,879

Goods available

$63,236

Less: Ending inventory

(12,887)

Cost of sales

$50,349

Add: Transfers in

68

Subtotal

$50,417

Less: Employee meals

$1,828

Less: Promotional meals

219

Less: Complimentary meals

140

Less: Transfers out

128

( 2,315)

Net Cost of Sales

$ 48,102

27

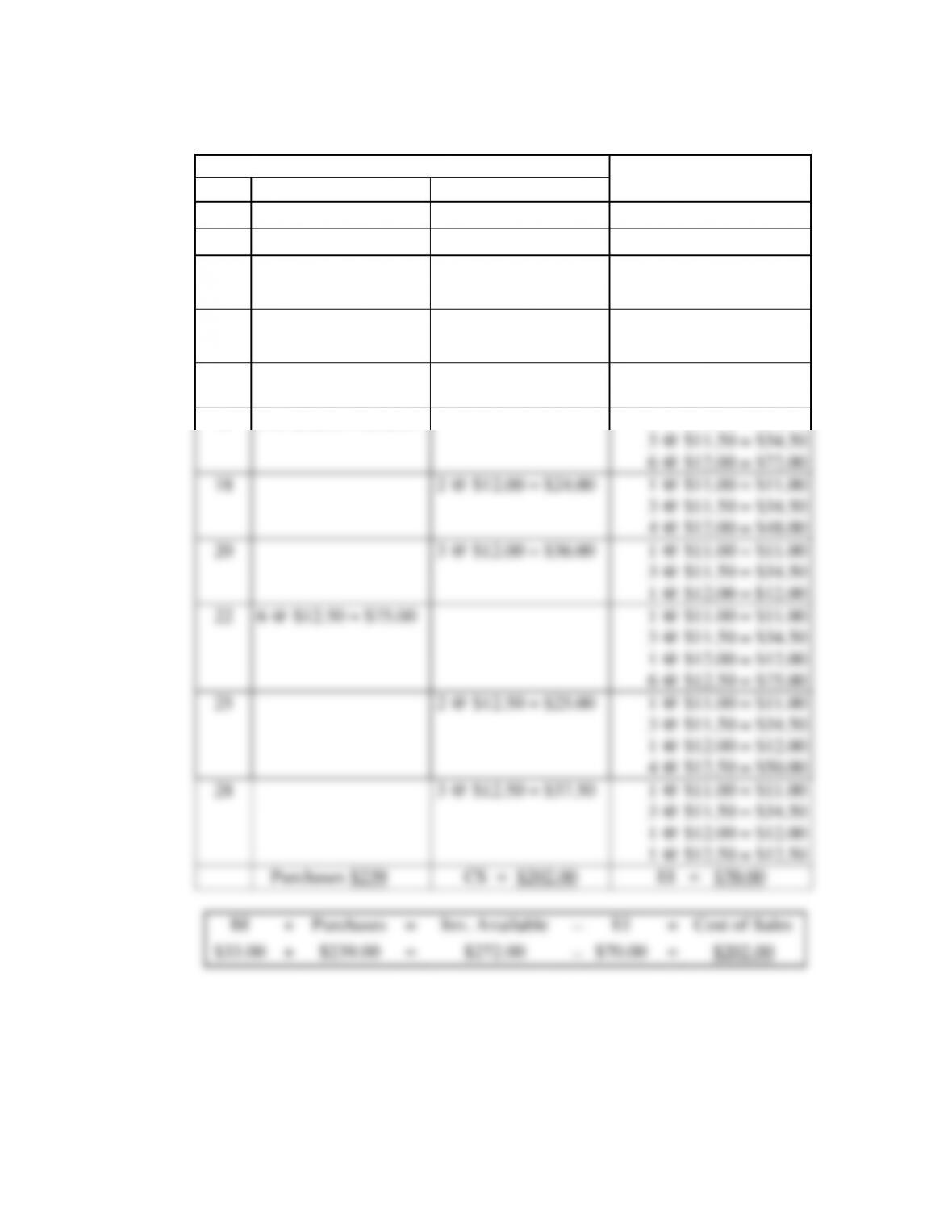

P2.4 a. FIFO perpetual inventory control record:

Item Description: M & B Supreme

Balance Available

June

Purchase-Received

Issued-Sales

Units × Cost = Total

Cost

01

Bal. Fwd.

3 @ $11.00 = $33.00

04

2 @ $11.00 = $22.00

1 @ $11.00 = $11.00

06

8 @ $11.50 = $92.00

1 @ $11.00 = $11.00

8 @ $11.50 = $92.00

09

1 @ $11.00 = $11.00

6 @ $11.50 = $69.00

2 @ $11.50 = 23.00

12

2 @ $11.50 = $23.00

4 @ $11.50 = $46.00

15

6 @ $ 12.00 =$72.00

4 @ $11.50 = $46.00

6 @ $12.00 = $72.00

18

2 @ $11.50 = $23.00

2 @ $11.50 = $23.00

6 @ $12.00 = $72.00

20

2 @ $11.50 = $23.00

5 @ $12.00 = $60.00

1 @ $12.00 = 12.00

22

6 @ $12.50 = $75.00

5 @ $12.00 = $60.00

6 @ $12.50 = $75.00

25

2 @ $12.00 = $24.00

3 @ $12.00 = $36.00

6 @ $12.50 = $75.00

28

3 @ $12.00 = $36.00

6 @ $12.50 = $75.00

E

n

d

Purchases $239.00

CS = $197.00

EI = $75.00

BI

+

Purchases

=

Inv. Available

−

EI

=

CS

$33.00

+

$239.00

=

$272.00

−

$75.00

=

$197.00

28

b. LIFO perpetual inventory control record:

Item Description: M & B Supreme

Balance Available

June

Purchase-Received

Issued-Sales

Units × Cost = Total

01

Bal. Fwd.

3 @ $11.00 = $33.00

04

2 @ $11.00 = $22.00

1 @ $11.00 = $11.00

06

8 @ $11.50 = $92.00

1 @ $11.00 = $11.00

8 @ $11.50 = $92.00

09

3 @ $11.50 = $34.50

1 @ $11.00 = $11.00

5 @ $11.50 = $57.50

12

2 @ $11.50 = $23.00

1 @ $11.00 = $11.00

3 @ $11.50 = $34.50

15

6 @ $12.00 = $72.00

1 @ $11.00 = $11.00

3 @ $11.50 = $34.50

6 @ $12.00 = $72.00

18

2 @ $12.00 = $24.00

1 @ $11.00 = $11.00

3 @ $11.50 = $34.50

4 @ $12.00 = $48.00

20

3 @ $12.00 = $36.00

1 @ $11.00 = $11.00

3 @ $11.50 = $34.50

1 @ $12.00 = $12.00

22

6 @ $12.50 = $75.00

1 @ $11.00 = $11.00

3 @ $11.50 = $34.50

1 @ $12.00 = $12.00

6 @ $12.50 = $75.00

25

2 @ $12.50 = $25.00

1 @ $11.00 = $11.00

3 @ $11.50 = $34.50

1 @ $12.00 = $12.00

4 @ $12.50 = $50.00

28

3 @ $12.50 = $37.50

1 @ $11.00 = $11.00

3 @ $11.50 = $34.50

1 @ $12.00 = $12.00

1 @ $12.50 = $12.50

E

n

d

Purchases $239

$239.00

CS = $202.00

EI = $70.00

BI

+

Purchases

=

Inv. Available

−

EI

=

Cost of Sales

$33.00

+

$239.00

=

$272.00

−

$70.00

=

$202.00

29

c. Weighted average perpetual inventory control record:

Item Description: M & B Supreme

Balance available

June

Purchase-Received

Issued-Sales

Units × Cost = Total

01

Bal. Fwd.

3 @ $11.00 = $ 33.00

04

2 @ $11.00 = $22.00

1 @ $11.00 = $ 11.00

06

8 @ $11.50 = $92.00

{$103.00 / 9 = 11.44}

9 @ $11.44 = $102.96

09

3 @ $11.44 = $34.32

6 @ $11.44 = $ 68.64

12

2 @ 11.44 = $22.88

4 @ $11.44 = $ 45.76

15

6 @ $12.00 = $72.00

{$117.76 / 10 = $11.78}

10 @ $11.78 = $117.80

18

2 @ 11.78 = $23.56

8 @ $11.78 = $ 94.24

20

3 @ 11.78 = $35.34

5 @ $11.78 = $ 58.90

22

6 @ $12.50 = $75.00

{$133.90 / 11 = $12.17}

11 @ $12.17 = $133.87

25

2 @ 12.17 = $24.34

9 @ $12.17 = $109.53

28

3 @ 12.17 = $36.51

6 @ $12.17 = $ 73.02

E

n

d

Purchases $239.00

CS = $198.98

EI = $73.02

BI

+

Purchases

=

Inv. Available

−

EI

=

Cost of Sales

$33.00

+

$239.00

=

$272.00

−

$73.02

=

$198.98

*Cost of sales per the control record is $198.95 or $0.03 short of the $198.98, which

is the correct amount, and the amount to be reported. The cumulative error results

from rounding to the nearest cent when each cost of sales item was calculated.

/

=

/

=

Total %

5,020

2,710

2,270

10,000

4,848

6,060

1,212

12,120

5,600

7,000

1,400

14,000

1,600

2,000

Less: Indirect Costs

( 25,092)

+

( 23,522)

+

( 8,506)

=

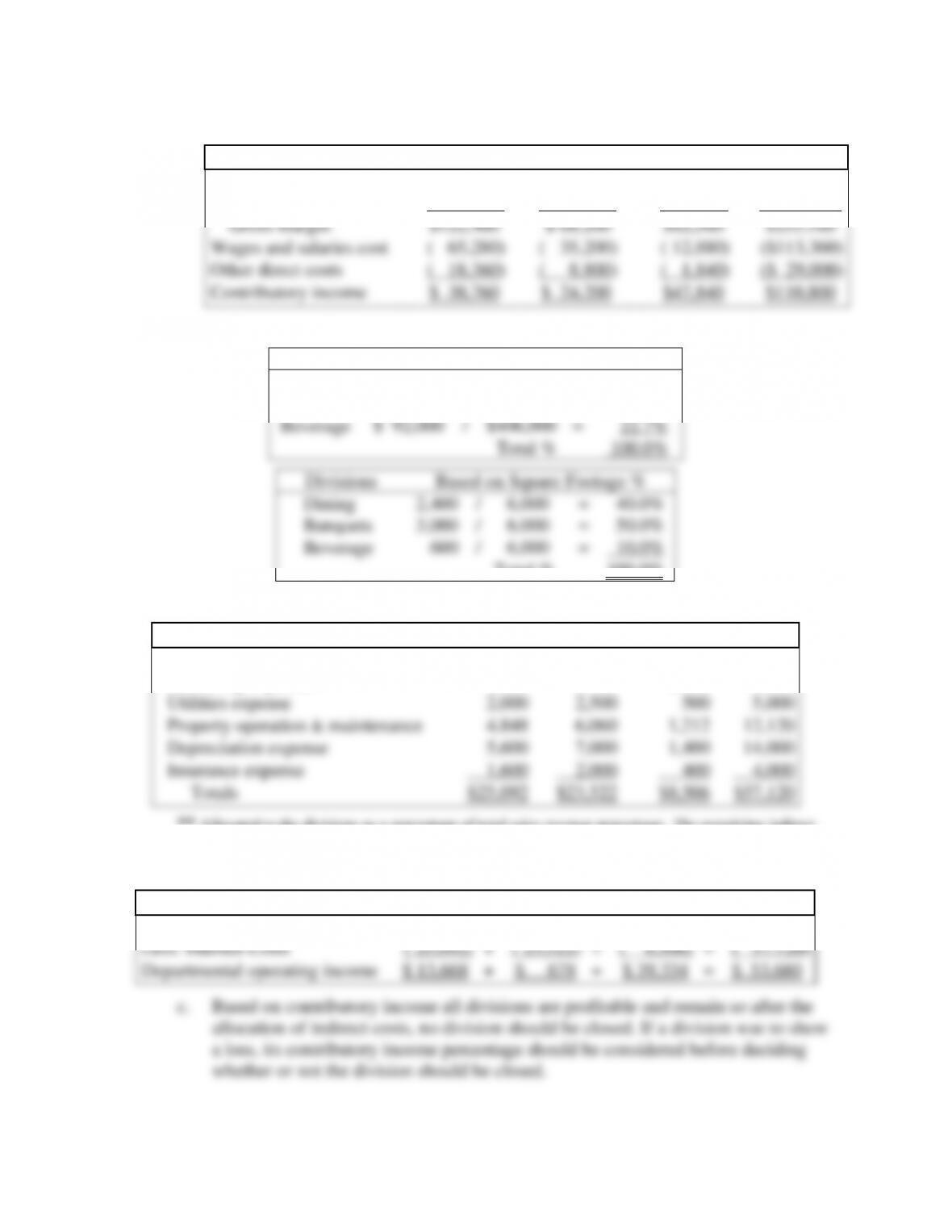

P2.5 a. Consolidated Departmental Contributory Income Statement.

Department

a.

Dinning

Room

Banquets

Beverages

Totals

Sales revenue

$204,000

$110,000

$92,000

$406,000

Cost of sales

( 81,600)

( 41,800)

( 29,440)

($152,840)

Gross margin

$122,400

$ 68,200

$62,560

$253,160

Wages and salaries cost

( 65,280)

( 35,200)

( 12,880)

($113,360)

Other direct costs

( 18,360)

( 8,800)

( 1,840)

($ 29,000)

Contributory income

$ 38,760

$ 24,200

$47,840

$110,800

b. Indirect costs allocation percentages on the basis of SR and sq. footage.

Divisions

Basis: Sales Revenue %

Dining

$204,000

/

$406,000

=

50.2%

Banquets

$110,000

/

$406,000

=

27.1%

Beverage

$ 92,000

/

$406,000

=

22.7%

Total %

100.0%

31

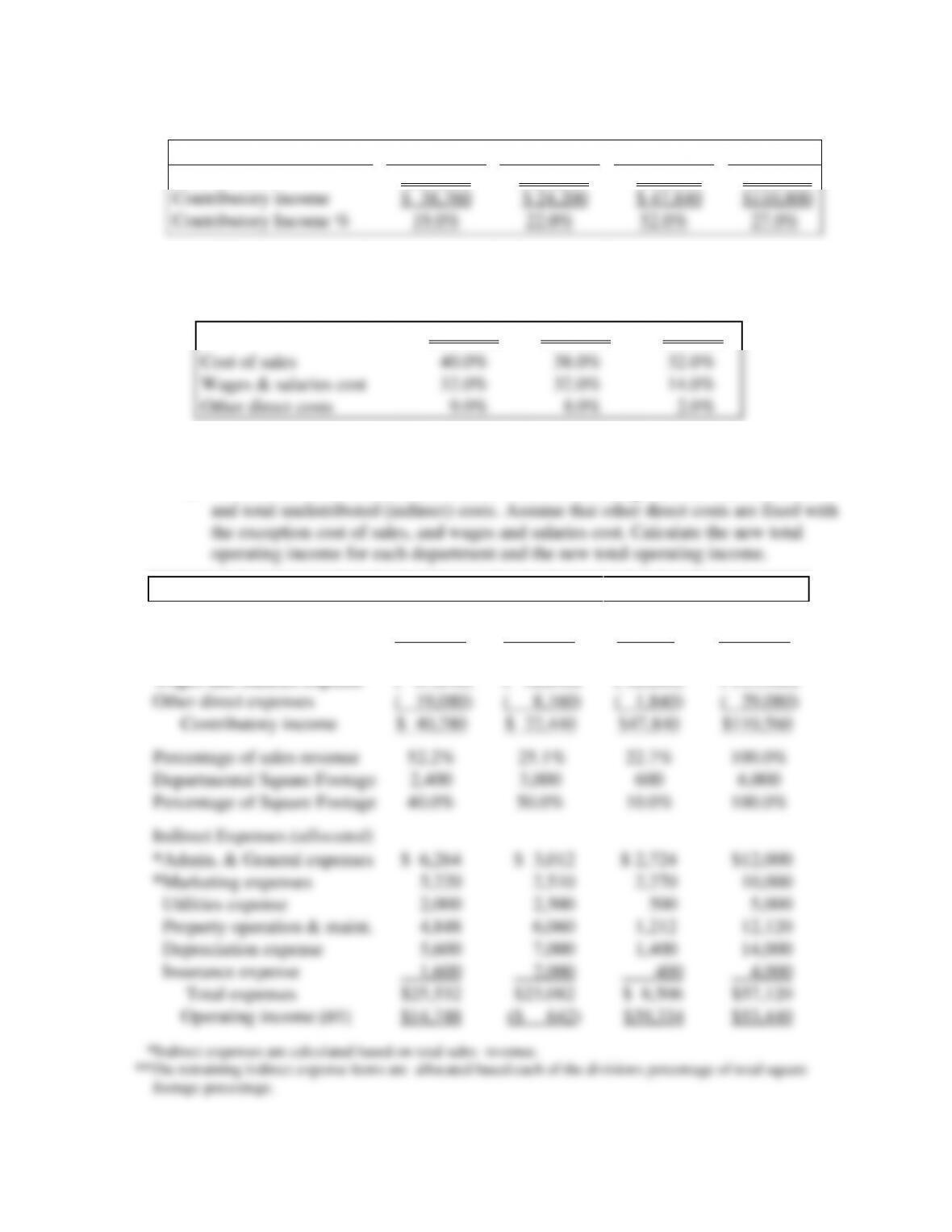

P2.6 a. Calculate each division and the department’s contributory income percentages.

Departmental Divisions

c.

Dining

Banquets

Beverages

Totals

Sales revenue

$204,000

$110,000

$ 92,000

$406,000

Contributory income

$ 38,760

$ 24,200

$ 47,840

$110,800

Contributory Income %

19.0%

22.0%

52.0%

27.0%

b. Calculate the cost of sales, wages and salaries, and direct costs as a percentage on

the basis of sales revenue for each division of the department.

Departmental Divisions

d.

Dinning

Banquet

Beverages

Sales revenue

$204,000

$110,000

$92,000

Cost of sales

40.0%

38.0%

32.0%

Wages & salaries cost

32.0%

32.0%

14.0%

Other direct costs

9.0%

8.0%

2.0%

c. The overall operating income would decrease because the contributory income

from the dining room as a percentage of sales revenue is lower than from banquets.

d. Assume the shift of $8,000 does occur. There is no change in total sales revenue

Department

Dining

Banquets

Beverages

Totals

Sales revenue

$212,000

$102,000

$92,000

$406,000

Cost of Sales

( 84,800)

( 38,760)

(29,440)

( 153,000)

Gross Margin

$127,200

$ 63,240

$62,560

$253,000

Wages and Salaries expense

( 67,840)

( 32,640)

( 12,880)

( 113,360)

Other direct expenses

( 19,080)

( 8,160)

( 1,840)

( 29,080)

Contributory income

$ 40,280

$ 22,440

$47,840

$110,560

Percentage of sales revenue

52.2%

25.1%

22.7%

100.0%

Departmental Square Footage

2,400

3,000

600

6,000

Percentage of Square Footage

40.0%

50.0%

10.0%

100.0%

Indirect Expenses (allocated)

*Admin. & General expenses

$ 6,264

$ 3,012

$ 2,724

$12,000

*Marketing expenses

5,220

2,510

2,270

10,000

Utilities expense

2,000

2,500

500

5,000

Property operation & maint.

4,848

6,060

1,212

12,120

Depreciation expense

5,600

7,000

1,400

14,000

Insurance expense

1,600

2,000

400

4,000

Total expenses

$25,532

$23,082

$ 8,506

$57,120

Operating income [BT]

$14,748

($ 642)

$39,334

$53,440

*Indirect expenses are calculated based on total sales revenue.

**The remaining indirect expense items are allocated based each of the divisions percentage of total square

footage percentage.

32

e. Do not close any department. Each department is making positive contributory income.

P2.7 Completed balance sheet.

Balance Sheet

For the First Quarter Ended March 31, 0007

ASSETS

Current Assets

Cash

$ 10,109

Credit card receivables

1,554

Accounts receivable

1,882

Inventories

7,225

Prepaid expenses

2,800

Total Current Assets

$ 23,570

Property Plant & Equipment

Land

$ 80,000

Building

$712,800

Less: Accumulated Depreciation

( 186,400)

526,400

Equipment

$119,080

Less: Accumulated Depreciation

( 35,625)

83,455

Furnishings

$ 64,120

Less: Accumulated depreciation

( 11,875)

52,245

Net Property Plant & Equipment

$742,100

Other assets

China and Tableware

$ 8,780

Glassware

2,620

Total other assets

$ 11,400

Total assets

$777,070

Liabilities & Stockholders’ Equity

Current Liabilities

Accounts payable

$ 5,070

Accrued expenses payable

2,900

Income taxes payable

8,770

Current portion of mortgage payable

13,030

Total Current Liabilities

$ 29,770

Long-term Liabilities

Mortgage payable

$406,800

Total Liabilities

$436,570

Stockholders’ Equity

Capital Stock

$152,000

Retained earnings

188,500

Total Stockholders’ Equity

$340,500

Total Liabilities & Stockholders’ Equity

$777,070

33

P2.8 Prepare a quarterly income statement.

Jarvis Trailer Park Income Statement

For the First Quarter Ended March 31, 0007

Trailer rental revenue [$60,000 + $200 – $1,575]*

$58,625

Expenses

Insurance expense [ $4,800 × 3/12 ]

$ 1,200

Wages expense [(5 × $9.95 × 8) + $4,500]

4,898

Maintenance expense [$80 + $400]

480

Office supplies expense [$300 – $100]

200

Utilities expense [$900 + $400]

1,300

Property tax expense [($6,000 / 12) × 3]

1,500

Salary expense [ given ]

10,500

Mortgage interest expense [$4,667 + $2,333]

7,000

Depreciation expense: Building [($216,000 / 240) × 3]

2,700

Depreciation expense: Office Equip. [($7,500 / 60) × 3]

375

Total Operating Expenses

( 30,153)

Operating Income [BT]

28,472

Income tax (25%) [$28,472 × 25%]

( 7,118)

Net Income

$21,354

*Sales revenue adjustment: (a) Yearly rent of $2,100 (at $175 a month) was prepaid for

the year. Nine months of the $2,100, or $1,575, remains unearned and must be deducted

from the reported sales revenue. (b) One rental tenant owes $200 in rent and it is added

to trailer rental revenue.

34

P2.8 (Continued) Jarvis Trailer Park

Balance Sheet

For the Quarter Ending March 31, 0007

Assets

Current Assets

Cash [$510,000 – $426,667]

$ 83,333

Accounts Receivable [ given ]

200

Office Supplies [$200 – $100 ]

100

Prepaid Insurance [$4,800 x 9/12]

3,600

Prepaid Property Tax [$6,000 x 9/12]

4,500

Total Current Assets

$ 91,733

Property Plant & Equipment

Land

$168,600

Building [ given ]

$216,000

Less: Accumulated depreciation *

( 2,700)

$213,300

Office equipment [ given ]

$ 8,000

Less: Accumulated depreciation **

( 375)

$ 7,625

Net Property Plant & Equipment

389,525

Total Assets

$481,258

Liabilities & Stockholders’ Equity

Current Liabilities

Accounts payable [ $80 + $400 ]

$ 480

Wages payable [ $9.95 x 8 hrs x 5 days ]

398

Interest payable [ given ]

2,333

Unearned rental revenue [ $175 x 9 ]

1,575

Income tax payable [ $28,472 x 25%]

7,118

Current portion mortgage payable [given ]

12,000

Total Current Liabilities

$ 23,904

Long Term Liabilities

Long Term Mortgage Payable

$336,000

$336,000

Total Liabilities

$359,904

Stockholders’ Equity

Capital stock

$100,000

Retained earnings

21,354

Total Stockholders’ Equity

121,354

Total Liabilities & Stockholders’ Equity

$481,258

35

CASE 2 SOLUTION

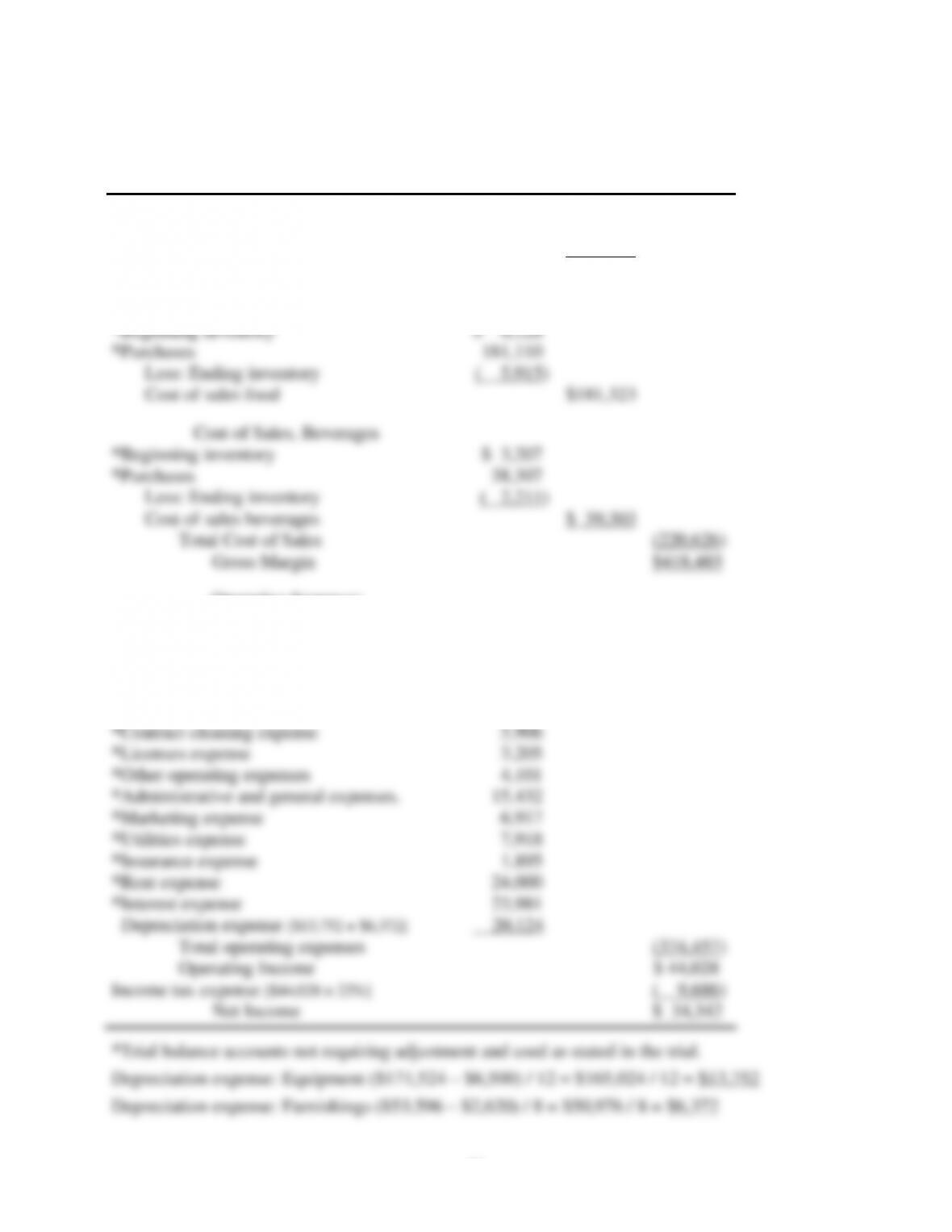

Part (1) 4C Company Income Statement

For the year ended December 31, 2007

Sales Revenue

*Food operations

$458,602

*Beverage operations

180,509

Total sales revenue

$639,111

Cost of Sales, Food

*Beginning inventory

$ 6,128

*Purchases

181,110

Less: Ending inventory

( 5,915)

Cost of sales food

$181,323

Cost of Sales, Beverages

*Beginning inventory

$ 3,207

*Purchases

38,307

Less: Ending inventory

( 2,211)

Cost of sales beverages

$ 39,303

Total Cost of Sales

(220,626)

Gross Margin

$418,485

Operating Expenses

Salaries and wages expense [$221,328 + $2,215]

$223,543

*Laundry expense

16,609

*Kitchen fuel expense

7,007

*China and tableware expenses

12,214

*Glassware expense

1,605

*Contract cleaning expense

5,906

*Licenses expense

3,205

*Other operating expenses

4,101

*Administrative and general expenses.

15,432

*Marketing expense

6,917

*Utilities expense

7,918

*Insurance expense

1,895

*Rent expense

24,000

*Interest expense

23,981

Depreciation expense [$13,752 + $6,372]

20,124

Total operating expenses

(374,457)

Operating Income

$ 44,028

Income tax expense [$44,028 × 22%]

( 9,686)

Net Income

$ 34,342

*Trial balance accounts not requiring adjustment and used as stated in the trial.

Depreciation expense: Equipment ($171,524 – $6,500) / 12 = $165,024 / 12 = $13,752

Depreciation expense: Furnishings ($53,596 – $2,620) / 8 = $50,976 / 8 = $6,372

36

Part (2) 4C Company

Balance Sheet

For the Year Ended December 31, 2007

Assets

Current Assets

*Cash

$ 36,218

*Credit Card Receivables

13,683

*Accounts Receivable

3,421

Inventories Food

$ 5,915

Inventories, Beverages

2,211

Total Inventories

8,126

*Prepaid Expenses

2,136

Total Current Assets

$ 63,584

Property Plant & Equipment

*Equipment

$171,524

Less: Accumulated Depreciation

( 13,752)

157,772

Furnishings

53,596

*Less Accumulated Depreciation

( 6,372)

47,224

Net Property Plant & Equipment

204,996

Total Assets

$268,580

Liabilities & Stockholders’ Equity

Current Liabilities

*Accounts payable

$ 8,819

Accrued payroll payable

2,215

Current portion Bank Loan Payable

38,260

Income taxes payable

9,686

Total Current Liabilities

$ 58,980

Long Term Liabilities

Bank Loan Payable

125,258

Total Liabilities

$184,238

Stockholders’ Equity

*Common Stock

$50,000

Retained Earnings

34,342

Total Stockholders’ Equity

$ 84,342

Total Liabilities & Stockholders’ Equity

$268,580

*Trial balance accounts not requiring adjustment and used as stated in the trial.