193

CHAPTER 12

CAPITAL BUDGETING AND

THE INVESTMENT DECISION

INTRODUCTION

Most of the matters discussed in the preceding eleven chapters concerned techniques, tools, and

methods available to management for short-run (generally defined as less than one year) decision

making. This chapter is concerned with long-run decision making for capital assets or fixed

assets. For this reason, the chapter may be studied relatively independently of others in the book,

as long as the student has a good basic knowledge of accounting and terminolgy.

TRUE OR FALSE QUESTIONS

(Correct answers indicated by T for True and F for False answers)

1. Decisions concerning investment in long-life assets are no more complex than

decisions concerning day-to-day matters.

F

2. The ARR formula is: net annual savings divided by average investment.

T

3. With the ARR method, if there is a trade-in value of the asset, that value is deducted

from initial investment (before dividing by two) to arrive at average investment.

F

4. The payback period method formula is: initial investment divided by net annual cash

savings.

T

5. Net annual cash saving in the payback period method is calculated by deducting

depreciation from net annual savings.

F

6. The payback period method measures the speed of recovering the cash put into an

investment.

T

7. Under the payback period method, the possible trade-in value of the asset at the end

of its useful life is ignored.

T

8. Both the payback period and the ARR methods ignore the time value of cash flows.

T

9. $1,000 today at 10% interest is worth more than $1,090 a year from now.

T

10. Discounted cash flow expresses future cash flows in terms of today’s value.

T

11. Discounted cash flow factors cannot be used if future cash flows are negative.

F

12. The discount rate used with the NPV investment method will be the same as the

current bank savings account interest rate.

F

13. The IRR investment method determines the interest (discount) rate that will equate

total discounted cash inflows with the initial investment.

T

194

14. A mutually exclusive alternative means that, if only one of a number of proposals is

to be accepted, the others will be rejected.

T

15. Capital rationing means that there is sufficient money to handle only a limited number

of investments in any budget period.

T

16. If both NPV and IRR are used to evaluate various alternative investments, their

ranking of these investments will always be identical.

F

17. In investment decision-making, one should ignore non-quantifiable factors.

F

18. Renting an asset, from a cash flow point of view, may be more profitable than

purchasing.

T

19. If a company leases an asset, it will have a cash flow advantage because depreciation

can be deducted and produces savings on income tax.

F

20. If, for a particular company, a purchase versus rental decision shows that the asset

should be purchased, then all future similar decisions should dictate purchase.

F

21. In deciding to purchase or lease an asset, any asset trade-in value under the ownership

option can be ignored.

F

22. In considering the leasing of an asset using discounted cash flow, the depreciation

method selected will affect the calculations.

F

MULTIPLE CHOICE QUESTIONS

(Correct answer indicated by asterisk)

1. Decisions about investing in fixed assets differ from day-to-day expense decisions because:

(a) The investment decision is affected by the future

(b) Only the general manager can be involved in the decision

(c) The relationship between increased net income from the investment and the actual

investment

(d) Year by year the additional cash flows from the investment

3. If an equipment investment was $10,000 with a 5-year life using straight-line depreciation

and provided additional annual sales revenue of $3,500 and expenses (excluding

depreciation) of $300, and the company is in a 50% tax bracket, the payback period is:

(c) 1.67 years

(d) 16.7 years

195

4. Given the facts in the preceding question, the ARR is:

(c) 6.0%

(d) 2.6%

5. A Company is trading in a fully depreciated old asset for a new one. Cost of the new asset is

$5,000 with a 5-year life and straight-line depreciation will be used. The company receives a

$500 allowance for the asset traded in. Additional sales revenue from the investment will be

$2,100 and expenses of $400 (excluding depreciation). The company is in a 25% tax

bracket. The payback period is:

(a) 7.50 years

(b) 8.33 years

6. Given the facts in the preceding question, the ARR is:

(c) 8.9%

(d) 8.0%

7. One of the criticisms of the ARR method is that it:

(c) Gives results that are not as satisfactory as the payback period method

(d) Does not allow two comparable investments to be considered at the same time

8. Average investment for the ARR method is calculated by:

(c) Dividing opening investment by 2 and adding trade-in value

(d) Dividing trade-in value by 2 and adding opening investment

9. The NPV method has an advantage over the payback period and ARR methods because:

(a) The forecasts of sales revenue and expenses are more accurate

(b) It uses discounted cash flow factors compiled by computer

10. Two alternative $15,000 investments are being considered. A 10% discount rate is used

because the company never invests at a lower rate than this. The NPV of Alternative A

shows a total present value of $12,400 and Alternative B a total present value of $12,800.

Given this information one should select:

(a) Neither, until one has used the ARR method to obtain the true rate of return

(b) B because it has a higher total present value

196

11. If the total present value of a 5-year investment using NPV and a 15% rate is $82,300, and

the initial investment is $100,000, one should:

(c) Determine the IRR and decide if one would be satisfied with that rate under the

circumstances

(d) Use the payback period and ARR methods to help make the decision

12. Purchasing is always preferable to leasing an asset because:

(a) The asset will have a trade-in value at the end of its useful life

(b) By purchasing and owning the asset, one can claim depreciation expense in excess of

rental expense and thus reduce income tax

EXERCISE SOLUTIONS

E12.1 Calculate an Accounting Rate of Return (ARR):

Net Annual Saving / Average Investment = $1,400 / $5,620 = 24.9%

E12.3 Calculate the payback period.

Net annual saving: $2,900

E12.4 Calculate the Net Present Value of a specific amount of cash flow.

Year 1: $4,285 × 0.9009 = $3,860

Year 2: $4,285 × 0.8166 = $3,499

E12.5 Repayment schedule with an item cost of $22,800 requiring a principle payment of

$4,560 per year plus interest at 12%:

Yr.

Interest

Principle

Balance

0

$22,800

1

$2,736

$4,560

18,240

2

2,189

4,560

13,680

3

1,642

4,560

9,120

4

1,094

4,560

4,560

5

547

4,560

-0-

197

E12.6 Determine payback periods for two alternatives.

Alternative 1

Alternative 2

Cost of investment

$33,000

$33,000

Cash recovery:

Years 1, 2, & 3

(25,400)

Years 1, 2, 3, & 4

( 30,000)

Balance

$ 7,600

$ 3,000

Alternative 1’s payback: $7,600 / $8,200 = 0.93 + 3 = 3.93 years

Alternative 2’s payback: $3,000 / $12,100 = 0.25 + 4 = 4.25 years

E12.7 Using the information in E12.6, determine the net present values

Alternative 1

Alternative 2

Year

Factor 12%

Total PV

Total PV

1

0.8929

$ 7,143

$ 3,750

2

0.7972

6,856

4,624

3

0.7118

6,264

6,050

4

0.6355

5,211

7,308

5

0.5674

2,326

6,866

Total 5 year PV

$27,800

$28,598

Initial Investment

( 33,000)

( 33,000)

NPV

($ 5,200)

($ 4,402)

Neither alternative is a good investment because NPV is negative in both cases.

PROBLEM SOLUTIONS

P12.1 a. Determine the best purchase between three different registers using ARR.

Register A

Register B

Register C

Annual saving

$2,000

$2,000

$2,000

Annual operating costs

$ 400

$ 300

$ 300

Depreciation expense

1,160

1,200

1,280

Total cost

(1,560)

(1,500)

(1,580)

$ 440

$ 500

$ 420

Income tax

(132)

( 150)

( 126)

Net saving

$ 308

$ 350

$ 294

Register A: [$308 / ($6,300 + $500 / 2)] = $308 / $3,400 = 9.1%

Register B: [$350 / ($6,000 / 2)] = $350 / $3,000 = 11.7%

Register C: [$294 / ($6,700 + $300 / 2)] = $294 / $3,500 = 8.4%

*Register B has the highest ARR.

b. Register B should be purchased because it exceeds the 10% limit.

198

P12.2 Using information from P12.1, determine the best investment using the payback period.

A

B

C

Net annual saving

$ 308

$ 350

$ 294

Depreciation

1,160

1,200

1,280

Annual cash savings

$1,468

$1,550

$1,574

Register A: $6,300 / $1,468 = 4.3 years

P12.3 Calculate net cash flow.

Year

Cash Flow

Factor 13%

Total PV

1

$37,500

0.8850

$ 33,188

2

43,800

0.7831

34,300

3

46,300

0.6931

32,091

4

50,000

0.6133

30,665

5

60,000

0.5428

32,568

6

18,500

0.5428

10,042

Total PV

$172,854

If a 13% return is wanted, it is not achieved since the total PV is considerably less than

the initial investment of $205,000. By trial and error an IRR of 7% gives a total present

value of $205,213.

P12.4 a. Alternative 1 payback will be in Year 5, and Alternative 2 in Year 4.

Alternative 1

Alternative 2

Cost of investment

$70,000

$70,000

Cash recovery:

Years 1, 2, 3 & 4

( 60,000)

Years 1, 2, & 3

(61,200)

Balance

$ 10,000

$ 8,800

Alternative 1: $10,000 / $24,000 = 0.42 + 4 = 4.42 years.

Alternative 2: $8,800 / $10,800 = 0.81 + 3 = 3.81 years.

b. Determine net present values.

Alternative 1

Alternative 2

Year

Factor 10%

Total PV

Total PV

1

0.9091

$ 7,636

$22,000

2

0.8264

9,586

16,362

3

0.7513

12,772

12,922

4

0.6830

15,709

7,376

5

0.6209

14,902

4,967

Total 5 year PV

$60,605

$63,627

Initial Investment

( 70,000)

( 70,000)

Alternatives NPV

($ 9,395)

($ 6,373)

Neither alternative is a good investment because NPV is negative in both cases.

199

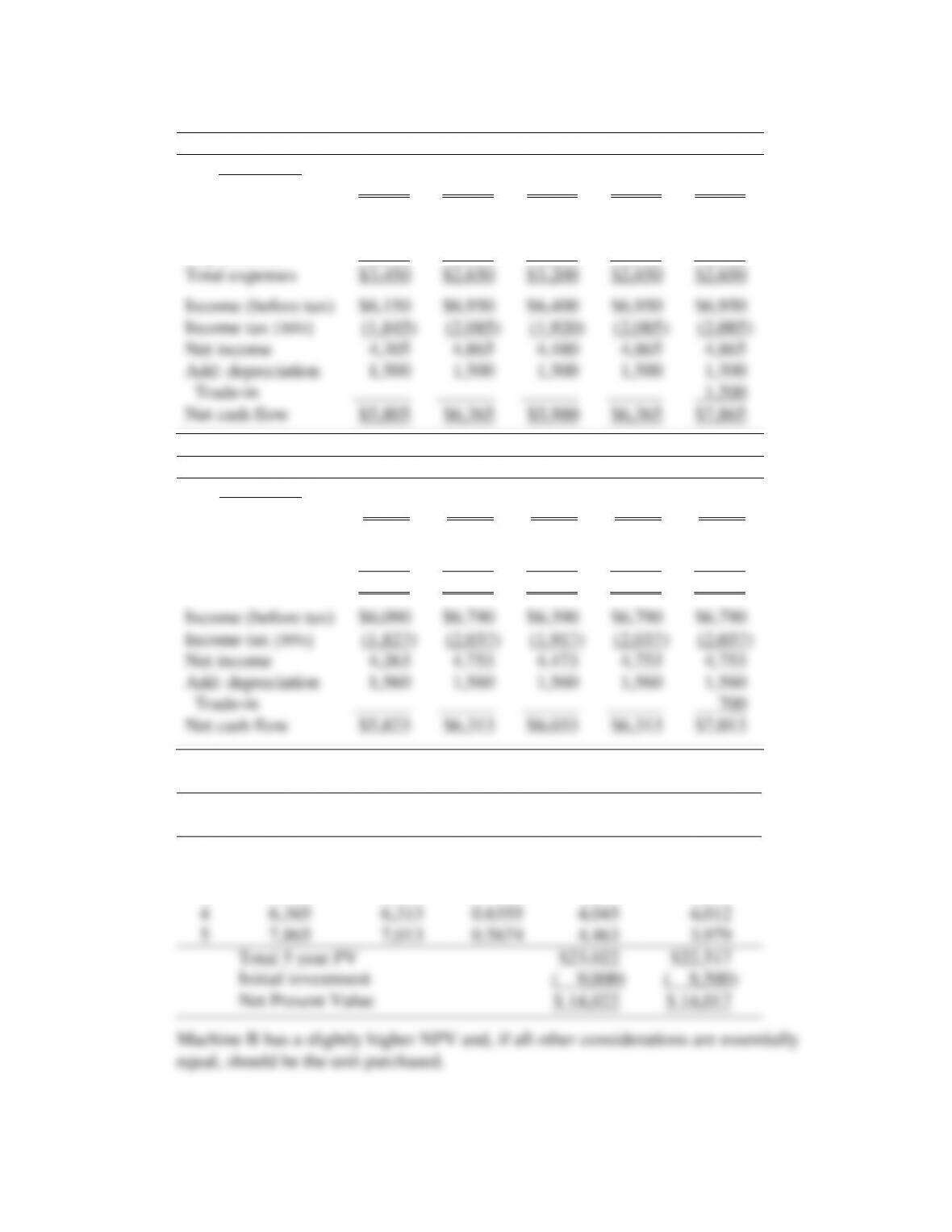

P 12.5 Determine net cash flow for Machine A and Machine B alternatives.

Year 1

Year 2

Year 3

Year 4

Year 5

Machine A

Wage saving

$9,600

$9,600

$9,600

$9,600

$9,600

Operating costs

$1,950

$1,150

$1,700

$1,150

$1,150

Depreciation

1,500

1,500

1,500

1,500

1,500

Total expenses

$3,450

$2,650

$3,200

$2,650

$2,650

Income (before tax)

$6,150

$6,950

$6,400

$6,950

$6,950

Income tax [30%]

(1,845)

(2,085)

(1,920)

(2,085)

(2,085)

Net income

4,305

4,865

4,480

4,865

4,865

Add: depreciation

1,500

1,500

1,500

1,500

1,500

Trade-in

1,500

Net cash flow

$5,805

$6,365

$5,980

$6,365

$7,865

Year 1

Year 2

Year 3

Year 4

Year 5

Machine B

Wage saving

$9600

$9600

$9600

$9600

$9600

Operating costs

$1,950

$1,250

$1,650

$1,250

$1,250

Depreciation

1,560

1,560

1,560

1,560

1,560

Total expenses

$3,510

$2,810

$3,210

$2,810

$2,810

Income (before tax)

$6,090

$6,790

$6,390

$6,790

$6,790

Income tax [30%]

(1,827)

(2,037)

(1,917)

(2,037)

(2,037)

Net income

4,263

4,753

4,473

4,753

4,753

Add: depreciation

1,560

1,560

1,560

1,560

1,560

Trade-in

700

Net cash flow

$5,823

$6,313

$6,033

$6,313

$7,013

Net NPV

Machine A

Machine B

Factor

Machine A

Machine B

Year

Cash Flow

Cash Flow

@ 12%

Total NPV

Total NPV

1

$5,805

$5,823

0.8929

$ 5,183

$ 5,199

2

6,365

6,313

0.7972

5,074

5,033

3

5,980

6,033

0.7118

4,257

4,294

4

6,365

6,313

0.6355

4,045

4,012

5

7,865

7,013

0.5674

4,463

3,979

Total 5 year PV

$23,022

$22,517

Initial investment

( 9,000)

( 8,500)

Net Present Value

$ 14,022

$ 14,017

Machine B has a slightly higher NPV and, if all other considerations are essentially

equal, should be the unit purchased.

200

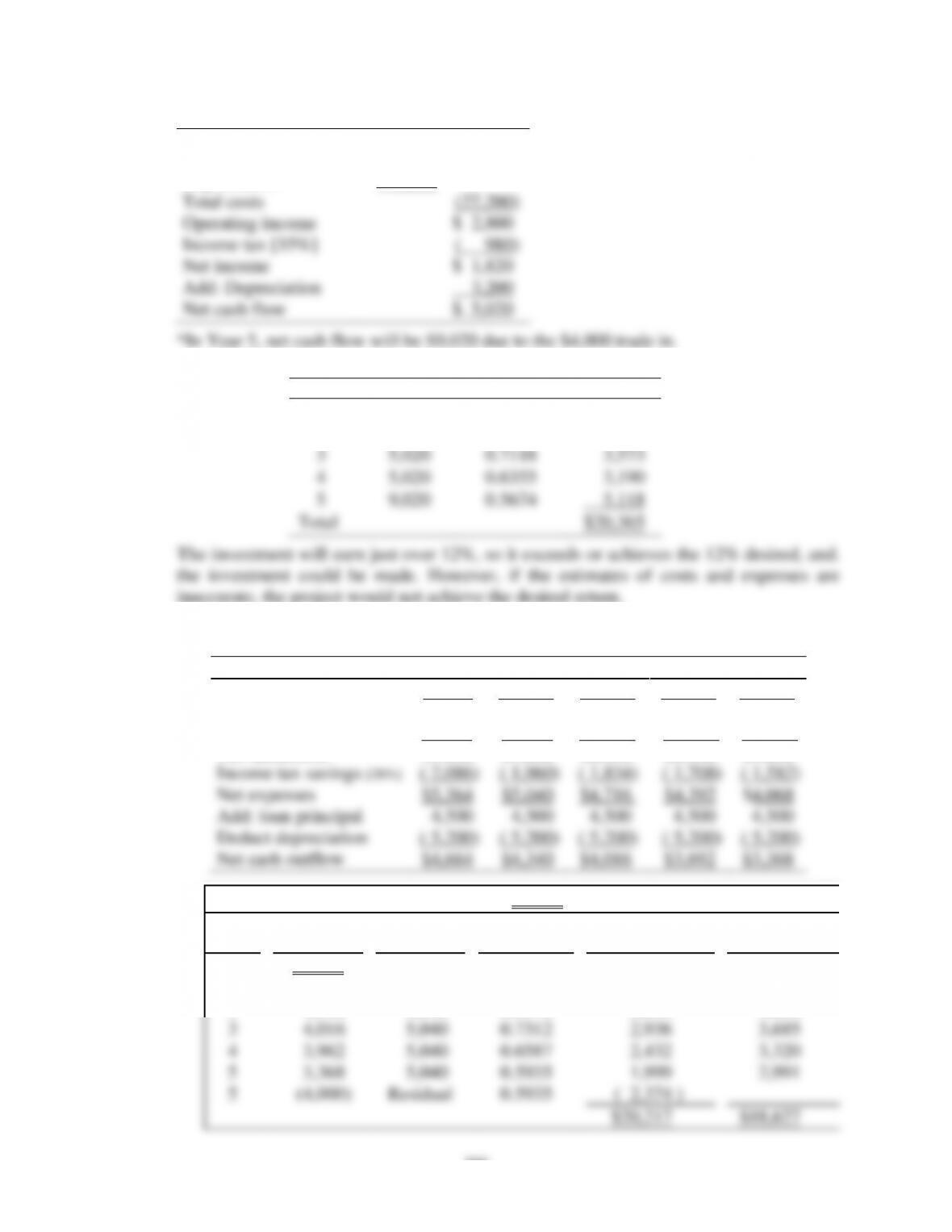

P12.6 Incremental average annual cash flow for years 1 through 4.

Sales revenue

$30,000

Variable costs [80%]

$24,000

Depreciation

3,200

Total costs

(27,200)

Operating income

$ 2,800

Income tax [35%]

( 980)

Net income

$ 1,820

Add: Depreciation

3,200

Net cash flow

$ 5,020

*In Year 5, net cash flow will be $9,020 due to the $4,000 trade in.

IRR analysis at 12% is:

Year

Cash flow

Factor 12%

Total PV

1

$5,020

0.8929

$ 4,482

2

5,020

0.7972

4,002

3

5,020

0.7118

3,573

4

5,020

0.6355

3,190

5

9,020

0.5674

5,118

Total

$20,365

The investment will earn just over 12%, so it exceeds or achieves the 12% desired, and.

the investment could be made. However, if the estimates of costs and expenses are

inaccurate, the project would not achieve the desired return.

P12.7 a. Calculation of net cash flow:

Purchasing Alternative

Year 1

Year 2

Year 3

Year 4

Year 5

Interest expense

$2,250

$1,800

$1,350

$ 900

$ 450

Depreciation

5,200

5,200

5,200

5,200

5,200

Tax deductible

$7,450

$7,000

$6,550

$6,100

$5,650

Income tax savings [28%]

( 2,086)

( 1,960)

( 1,834)

( 1,708)

( 1,582)

Net expenses

$5,364

$5,040

$4,716

$4,392

$4,068

Add: loan principal

4,500

4,500

4,500

4,500

4,500

Deduct depreciation

( 5,200)

( 5,200)

( 5,200)

( 5,200)

( 5,200)

Net cash outflow

$4,664

$4,340

$4,016

$3,692

$3,368

Rental alternative: Net cash outflow = $5,040 [$7,000 – (28% x 7,000)] per year.

Cash flow

Cash flow

Discount

Total

Total

Year

Purchase

Rental

Factor 11%

Purchase NPV

Rental NPV

0

$7,500

$ 7,500

1

4,664

$5,040

0.9009

4,202

$ 4,541

2

4,340

5,040

0.8116

3,522

4,090

3

4,016

5,040

0.7312

2,936

3,685

4

3,962

5,040

0.6587

2,432

3,320

5

3,368

5,040

0.5935

1,999

2,991

5

(4,000)

Residual

0.5935

( 2,374 )

$20,217

$18,627

201

Under these circumstances, leasing the equipment appears to be the best alternative

because total NPV of cash outflows is $1,570 less ($20,217 – $18,627).

b. 1. Use of an accelerated depreciation method rather than straight line: An

accelerated method increases depreciation expense in the early years of the

asset’s life.

2. Arrange different payment terms, such as an initial down payment less than

$7,500, and offset the lower down payment by increased yearly loan repayments.

3. Negotiations of an interest rate lower than 11%.

4. The information does not consider the cost of repairs and maintenance of the

equipment. These costs should have been considered.

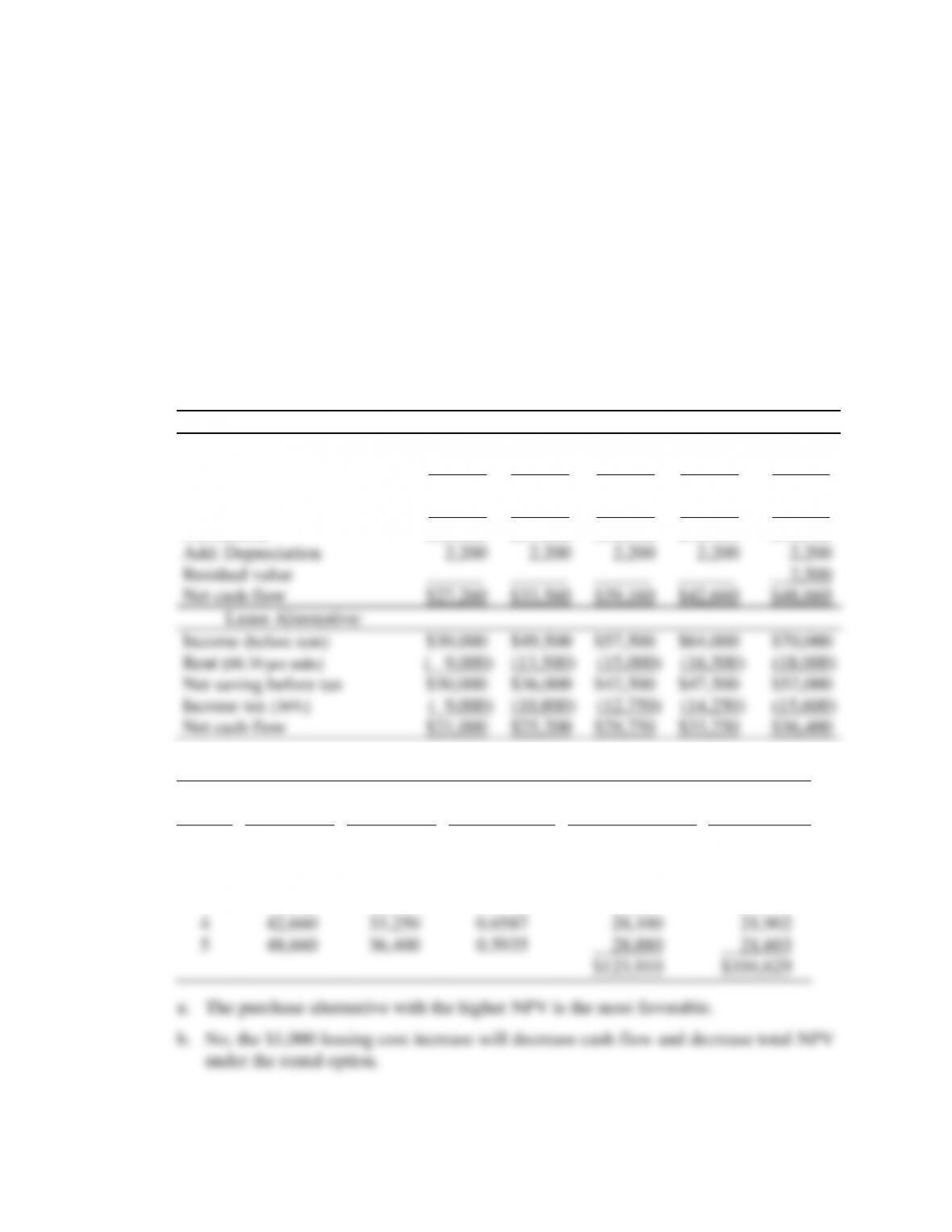

P12.8 Determine net cash flow and net present values for alternatives.

Purchase Alternative:

Year 1

Year 2

Year 3

Year 4

Year 5

Income (before depreciation)

$38,000

$47,000

$55,000

$60,000

$65,000

Depreciation

( 2,200)

( 2,200)

( 2,200)

( 2,200)

( 2,200)

Operating Income [BT]

$35,800

$44,800

$52,800

$57,800

$62,800

Income tax [30%]

(10,740)

(13,440)

(15,840)

(17,340)

(18,840)

Net income

$25,060

$31,360

$36,960

$40,460

$43,960

Add: Depreciation

2,200

2,200

2,200

2,200

2,200

Residual value

2,500

Net cash flow

$27,260

$33,560

$39,160

$42,660

$48,660

Lease Alternative:

Income (before rent)

$39,000

$49,500

$57,500

$64,000

$70,000

Rent [$0.30 per mile]

( 9,000)

(13,500)

(15,000)

(16,500)

(18,000)

Net saving before tax

$30,000

$36,000

$42,500

$47,500

$52,000

Income tax [30%]

( 9,000)

(10,800)

(12,750)

(14,250)

(15,600)

Net cash flow

$21,000

$25,200

$29,750

$33,250

$36,400

NPV evaluation:

Cash flow

Cash flow

Discount

Total

Total

Year

Purchase

Rental

Factor 11%

Purchase NPV

Rental NPV

0

($13,500)

($ 13,500)

1

27,260

$21,000

0.9009

$ 24,559

$ 18,919

2

33,560

25,200

0.8116

27,237

20,452

3

39,160

29,750

0.7312

28,634

21,753

4

42,660

33,250

0.6587

28,100

21,902

5

48,660

36,400

0.5935

28,880

21,603

$123,910

$104,629

a. The purchase alternative with the higher NPV is the most favorable.

b. No, the $1,000 leasing cost increase will decrease cash flow and decrease total NPV

under the rental option.

202

P12.9 Calculate the payback period, ARR and NPV.

Income will be from:

Elimination of previous loss

$2,150

10% of soft drink sales revenue of $25,550

2,555

$4,705

Expenses will be:

Depreciation [($7,000 − $1,000) / 5 years]

$1,200

Machine maintenance

100

( 1,300)

Savings before income tax

$3,405

Income tax [30%]

( 1,022)

Net annual saving

$2,383

Add back depreciation

1,200

Net annual cash flow

$3,583

a. Payback period: $7,000 / $3,583 = 1.95 or 2 years

b. NPV:

Annual

Discount

Total

Year

Cash flows

Factor 12%

NPV

1

$3,583

0.8929

$3,199

2

3,583

0.7972

2,856

3

3,583

0.7118

2,550

4

3,583

0.6355

2,277

5

3,583

0.5674

2,033

5

1,000

0.5674

567

Total 5 year PV

$13,482

Less: Initial investment

( 7,000)

Net Present Value

$ 6,482

The investment should be made because the NPV is positive.

P12.10 Calculate NPV and determine whether to operate or lease.

Lease Option

Sales

Tax rate

Net Cash

Discount

Total

Year

Revenue

@ 25%

Flow

Factor 10%

PV

1

$24,000

$6,000

$18,000

0.9091

$16,364

2

24,000

6,000

18,000

0.8264

14,875

3

24,000

6,000

18,000

0.7513

13,523

4

30,000

7,500

22,500

0.6830

15,368

5

30,000

7,500

22,500

0.6209

13,970

Total NPV:

$74,100

203

Operate Option

Year 1

Year 2

Year 3

Year 4

Year 5

Sales revenue

$700,000

$750,000

$800,000

$850,000

$900,000

Operating Expenses

Variable costs [90% of SR]

$630,000

$675,000

$720,000

$765,000

$810,000

Other expenses

32,000

34,000

36,000

38,000

40,000

Depreciation

8,000

8,000

8,000

8,000

8,000

Total expenses

$670,000

$717,000

$764,000

$811,000

$858,000

Operating Income [BT]

$30,000

$33,000

$37,000

$39,000

$40,000

Income tax [25%]

( 7,500)

( 8,250)

( 9,000)

( 9,750)

(10,500)

Net Income

$22,500

$24,750

$27,000

$29,250

$31,500

Add: Depreciation

8,000

8,000

8,000

8,000

8,000

Net cash inflows

$30,500

$32,750

$35,000

$37,250

$39,500

Net Cash Flow

Cash

Discount

Total

Year

Flows

Factor 10%

PV

1

$30,500

0.9091

$27,728

2

32,750

0.8264

27,065

3

35,000

0.7513

26,296

4

37,250

0.6830

25,442

5

39,500

0.6209

24,526

Total 5 year PV

$131,057

Less: Initial investment:

( 35,000)

Net Present Value

$ 96,057

The motel, on the basis of NPV, should operate the restaurant since there is a projected

gain of $21,957 ($96,057 less $74,100).

204

CASE 12 SOLUTION

Assuming Year 2009:

Keep present arrangement: Pay monthly rent

Year

Rent

22% Tax

Net Amount

Factor 12%

Total PV

2009

$29,040

00

$6,389

$22,651

0.8929

$20,225

2010

31,944

7,028

24,916

0.7972

19,861

2011

35,138

7,730

27,408

0.7118

19,509

2012

38,652

8,503

30,149

0.6355

19,160

$78,757

Prepay $80,000 rent: If the rent is prepaid for the next four years and $80,000 is borrowed from

the bank, the interest expense at the end of the first year will be 12% × $80,000 = $9,600. The

interest will decrease by $2,400 per year.

Interest

Tax

Net

Principle

Total Cash

Factor

Total

Year

Expense

Savings

Expense

Payment

Outflow

12%

PV

1

$9,600

$2,112

$7,488

$20,000

$27,488

0.8929

$24,544

2

7,200

1,584

5,616

20,000

25,616

0.7972

20,421

3

4,800

1,056

3,744

20,000

23,744

0.7118

16,901

4

2,400

528

1,872

20,000

21,872

0.6355

13,900

$75,766

a. The offer should be accepted. The NPV of prepaying the rent is $2,997 less ($78,757 –

$75,760)