175

CHAPTER 11

CASH MANAGEMENT

INTRODUCTION

An understanding of the accrual concept of accounting makes one realize that the net income

figure on the income statement is not necessarily the equivalent of cash. For this reason, it is

important for a business to develop cash budgets from budgeted income statements. Chapter 9 on

budgeting will set the foundation and should be reviewed and studied as a necessary prerequisite

to this chapter. Chapter 10 should also provide insight into the techniques used in cash

management.

TRUE OR FALSE QUESTIONS

(Correct answer indicated by T for True and F for False answers)

1. The amount of cash that a company has on hand at any time is constantly fluctuating.

T

2. Cash management implies not only control of the cash account, but also control of all

other working capital accounts.

T

3. The amount of cash on hand at the end of an accounting period should agree with the

amount of net income for that period.

F

4. A cash budget helps in proper cash management.

T

5. Forecast income statements are the usual starting point in cash budgeting.

T

6. If annual property taxes were prepaid in January, and if monthly cash budgets were

being prepared, one twelfth of the taxes would show as a disbursement for each of the

twelve monthly cash budgets.

F

7. To prepare monthly cash budgets, it is necessary to know the normal pattern for

collection of accounts receivable.

T

8. Depreciation would show as a disbursement on a cash budget.

F

9. The main purpose of cash budgeting is to forecast cash surpluses and deficiencies.

T

10. A company preparing cash budgets that show certain months with cash shortages

(negative cash flow) may have difficulty borrowing short-term money.

T

11. Repayment of principal amounts on loans will show as a disbursement on a cash

budget.

T

12. A company should only have sufficient cash on hand on the premises to cover normal

day-to–day operations.

T

13. The difference between a company’s record of cash in the bank and the bank’s record

is known as a bank float.

T

176

14. A method of accelerating the flow of funds from individual units in a chain operation

to the company’s head office bank account is known as concentration banking.

T

15. In a hotel, accounts receivable comprises the city ledger accounts only.

F

16. The procedure of aging accounts receivable is carried out to indicate to management

when to write off accounts as bad debts.

F

17. The use of a bank lockbox is designed to speed up the collection of a company’s

accounts receivable.

T

18. The monthly food inventory turnover rate is calculated by dividing food cost for the

month into average food inventory during the month.

F

19. Average inventory is calculated by adding beginning and ending inventory figures

together and dividing by two.

T

20. Normal food inventory turnover is between two and four times a month.

T

21. A low inventory turnover rate indicates a low investment in inventory.

F

22. No restaurant could ever achieve a food inventory turnover rate as high as 20 or more

times in a month.

F

23. To conserve cash in a business, it is wise to pay accounts payable only after their due

date.

F

24. When converting required cash flow to an after-tax profit amount, loan payments are

deducted from cash flow and depreciation is added to the required cash flow.

F

MULTIPLE CHOICE QUESTIONS

(Correct answer indicated by asterisk)

1. Cash management should be practiced:

(a) To ensure that there is always a surplus of cash on hand

(b) Only buy companies with large inflows of cash

2. Cash management is:

(c) Asking stockholders how much they should be paid in cash dividends

(d) Selling goods and services on a cash basis only

3. If a company has an income of $5,000 (after depreciation but before income tax) during a

particular month, its bank account should have increased by:

(a) $5,000, plus depreciation, plus tax

(b) $5,000, plus depreciation

177

4. In cash budgeting, depreciation expense on the income statement is not shown as a cash

disbursement on a cash budget because:

(a) One has a choice of depreciation methods

(b) Depreciation is not really a business expense

5. Sales revenue in Month 1 of a new restaurant is forecast to be $60,000 and in Month 2

$75,000. Cost of sales is estimated to be 30% of sales revenue, with half the cost paid for in

the month of purchase, the other half in the following month. Month 2’s cash disbursement

for purchases is:

(c) $22,500

(d) $11,250

6. If a cash budget for the next six months showed that in Months 4 and 5 the closing bank

balance figure was negative, the company should:

(c) Use positive closing balances from Months 1, 2, and 3 to offset the Month 4 and 5 figures

(d) Not pay any invoices from Months 4 and 5 until the situation improves

7. Which of the following would not affect the annual cash budget, assuming there will be

disbursements for income tax?

(c) Purchasing new fixed assets

(d) Repaying a stockholder loan

8. Cash conservation implies:

(c) Not taking a discount for prompt payment of an account to conserve the cash for a longer

period in the bank

(d) Not allowing any customers to charge their accounts

9. The difference between a company’s record of cash in the bank and the bank’s record is

known as:

(c) Concentration banking

(d) Deficit financing

10. A method of accelerating the flow of funds from individual units in a chain operation to the

company’s head office is known as:

(c) Using lockboxes

(d) Centralized banking

178

11. A house account in a hotel is:

(a) Another name for a city ledger account

(b) A ledger account for the purchase of a house for employee accommodation

12. A schedule of aging of accounts shows:

(a) The individual balances of all accounts receivable

(b) The ages of guests who have unpaid accounts

13. A bank lockbox is used to:

(a) Avoid having to use bank float

(b) Avoid having to use concentration banking

14. A bar inventory turnover of 1/2 to 1 a month in an establishment, means that the inventory

turnover is:

(c) Twice a month

(d) Once every six months

15. If inventory turnover is increasing over time, and all other things remain equal, this means

that:

(a) More money is being tied up in inventory

(b) Purchases are being made less frequently

EXERCISE SOLUTIONS

E11.1 Determine if the discount on accounts payable should or should not be taken and discuss

your decision.

$7,500 x 3% = $225 if payment is made within 5 days discount period and should be

taken. If borrowing for 25 days at a 12% interest is considered to pay the $7,275 within

the discount period, the interest would be:

E11.2 Calculate sales revenue percentages by category.

March

April

Sales revenue

$48,200 = 100.0%

$50,400 = 100.0%

Cash sales revenue

$14,460 / $48,200 = 30.0%

$14,112 / $50,400 = 28.0%

28.0%

Credit card sales revenue

$31,330 / $48,200 = 65.0%

$34,272 / $50,400 = 68.0%

68.0%

Accounts receivable sales

$ 2,410 / $48,200 = 5.9%

$ 2,016 / $50,400 = 4.0%

4.0%

Cash sales revenue decreased and sales revenue on credit cards increased.

179

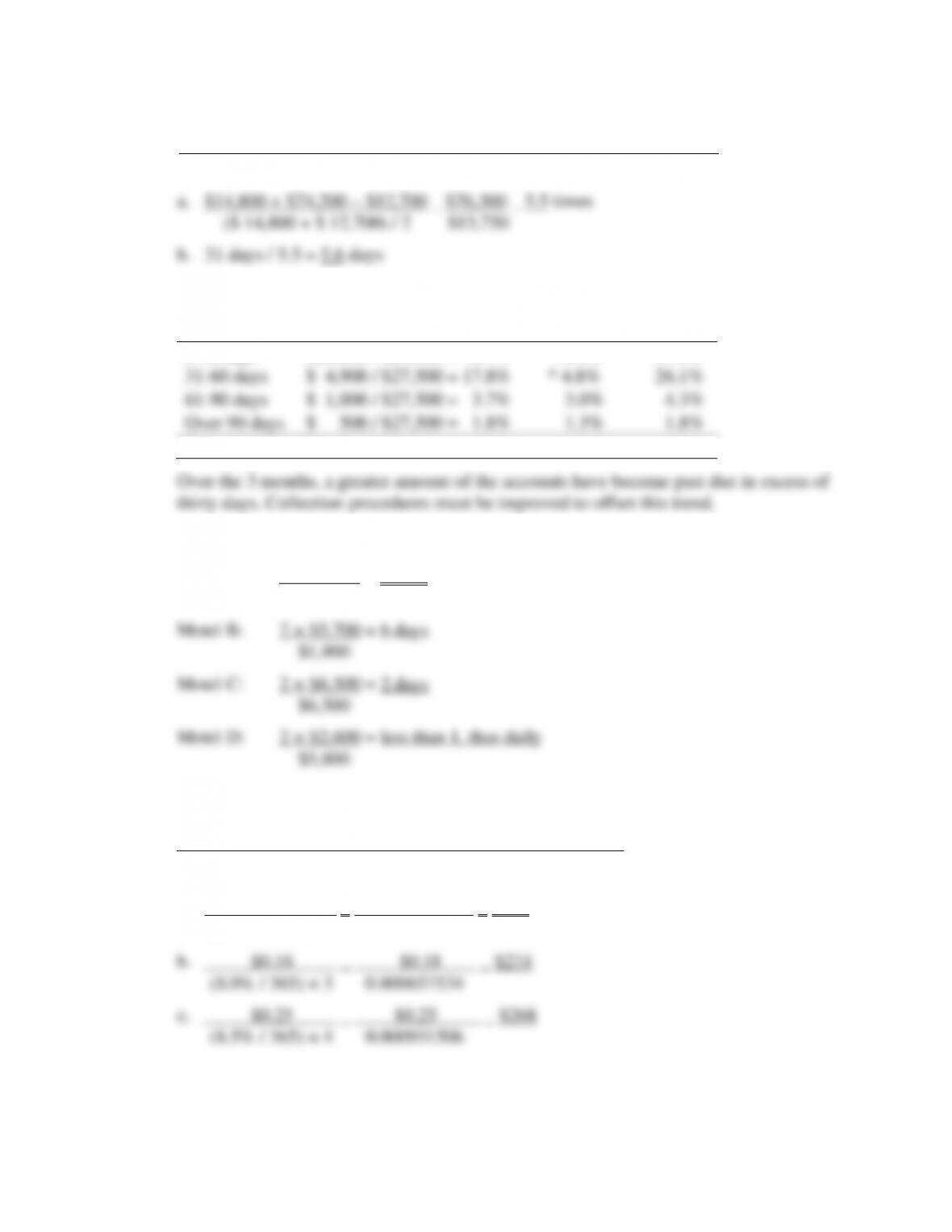

E11.3 Calculate food inventory turnover and days of inventory available for March.

Beginning food inventories + Food purchases − Ending food inventories

Beginning food inventories + Ending food inventories

E11.4 Accounts receivable collections.Calculations are shown for Janauary

January

February

March

0-30 days

$21,100 / $27,500 = 76.7%

71.0%

67.8%

31-60 days

$ 4,900 / $27,500 = 17.8%

* 4.8%

26.1%

61-90 days

$ 1,000 / $27,500 = 3.7%

3.0%

4.3%

Over 90 days

$ 500 / $27,500 = 1.8%

1.3%

1.8%

* Item does not add due to rounding

Over the 3 months, a greater amount of the accounts have become past due in excess of

E11.5 Determine the transfer frequency for four motels.

Motel A: 2 × $3,200 = 4 days

$1,600

E11.6 Determine the minimum accounts receivable payment to make a lockbox system

profitable.

Bank charge per item

Opportunity cost percentage per day × Time savings in days

a. $0.20 $0.20 $365

(10.0% / 365) × 2 0.000547945

180

E11.7 Calculate the cash inflows for the months of April and May.

Cash sales revenue receipts inflows

April

May

Cash sales revenue [32%]

$15,744

$16,896

Credit card sales revenue [64% 94%]

29,599

31,764

Credit card sales revenue, previous month [6%]

1,770

1,889

Accounts receivable, previous month [4%]

1,844

1,968

Total Cash Inflows

$48,957

$52,517

E11.8 Calculate cash outflows for the months of September and October.

Cash payment outflows

September

October

Cost of sales, current [75%]

[1]

$14,216

[5]

$14,592

Cost of sales previous month [25%]

[2]

4,598

[6]

4,739

Operating expenses [98%]

[3]

24,930

[7]

25,590

Operating expenses previous month [2%]

[4]

494

[8]

509

Total cash outflows

$44,238

$45,430

[1] $18,954 × 75% = $14,216 [5] $19,456 × 75% = $14,592

[2] $18,392 × 25% = $ 4,598 [6] $18,954 × 25% = $ 4,739

[3] $25,439 × 98% = $24,930 [7] $26,112 × 98% = $25,590

[4] $24,684 × 2% = $ 494 [8] $25,439 × 2% = $ 509

E11.9 Calculate the ending cash balance of the first month of operations.

Beginning cash balance February

$ 4,448

Cash sales revenue, current [86% × $39,300]

$33,798

Cash sales revenue, previous month [14% × $38,400]

5,376

Total cash receipts

39,174

Total cash available

$43,622

Cash payments

Cost of sales, current [75% × $14,541]

$10,906

Cost of sales previous month [25% × $14,208]

3,552

Wages expense

13,362

Operating expenses

5,895

Total February cash payments

($ 33,715)

Ending February cash balance

$ 9,907

181

PROBLEM SOLUTIONS

P11.1 Prepare a cash budget for the month of December 1, 0007

Cash Budget

For December, Year 0007

Beginning cash

$ 4,800

Cash receipts, operations

Sales revenue, cash [$75,000 × 40%]

$30,000

Credit card sales revenue [$75,000 × 60% × 96%]

43,200

Previous month credit card sales revenue [$80,000 × 60% × 4%]

1,920

Total cash receipts

75,120

Total cash available, December 0007

$79,920

Cash disbursements, operations

December cost of sales [$29,000 × 20%]

$ 5,800

November cost of sales [$30,000 × 80%]

24,000

Wages expense

21,000

Operating expenses

14,000

Total cash disbursements

(64,800)

Ending cash balance

$15,120

* Rent was prepaid and noted as a cash disbursement in January 0007 for the entire year.

Depreciation is a non-cash expense and reduces the book value of related depreciable assets.

P11.2 Calculate the motel’s cash balance at December 31, 0008.

Cash collections for November and December

Year 0008

November sales revenue: $34,500

November cash sales [42%]

$ 14,490

November credit card sales [$34,500 x 58% x 92% ]

18,409

October credit card sales [$32,500 x 58% x 8%]

1,508

December sales revenue: $36,000

December cash sales [42%]

15,120

December credit card sales [$36,000 x 58% x 92%]

19,210

November credit card sales [$34,500 x 58% x 8%]

1,601

$ 70,338

January to October sales

$367,900

Total cash collected in Year 0008

$438,238

182

Cash Reconciliation

Beginning bank balance

$ 7,100

Cash receipts, operations

Cash sales revenue

438,238

Total cash available

$445,338

Cash disbursements, Operations

Operating expenses

$302,300

Management salary expense

23,000

Building rent expense

18,500

Insurance expense

2,400

Interest expense

7,600

Income tax (paid for Yr. 0007)

9,800

Total cash disbursements, operations

( 363,600)

Cash excess (deficiency)

$ 81,738

Cash disbursements, Financing

New furniture

15,600

Bank loan payment [$73,900 – $49,200]

24,700

Total cash disbursements, financing

( 40,300)

Ending Cash Balance

$ 41,438

183

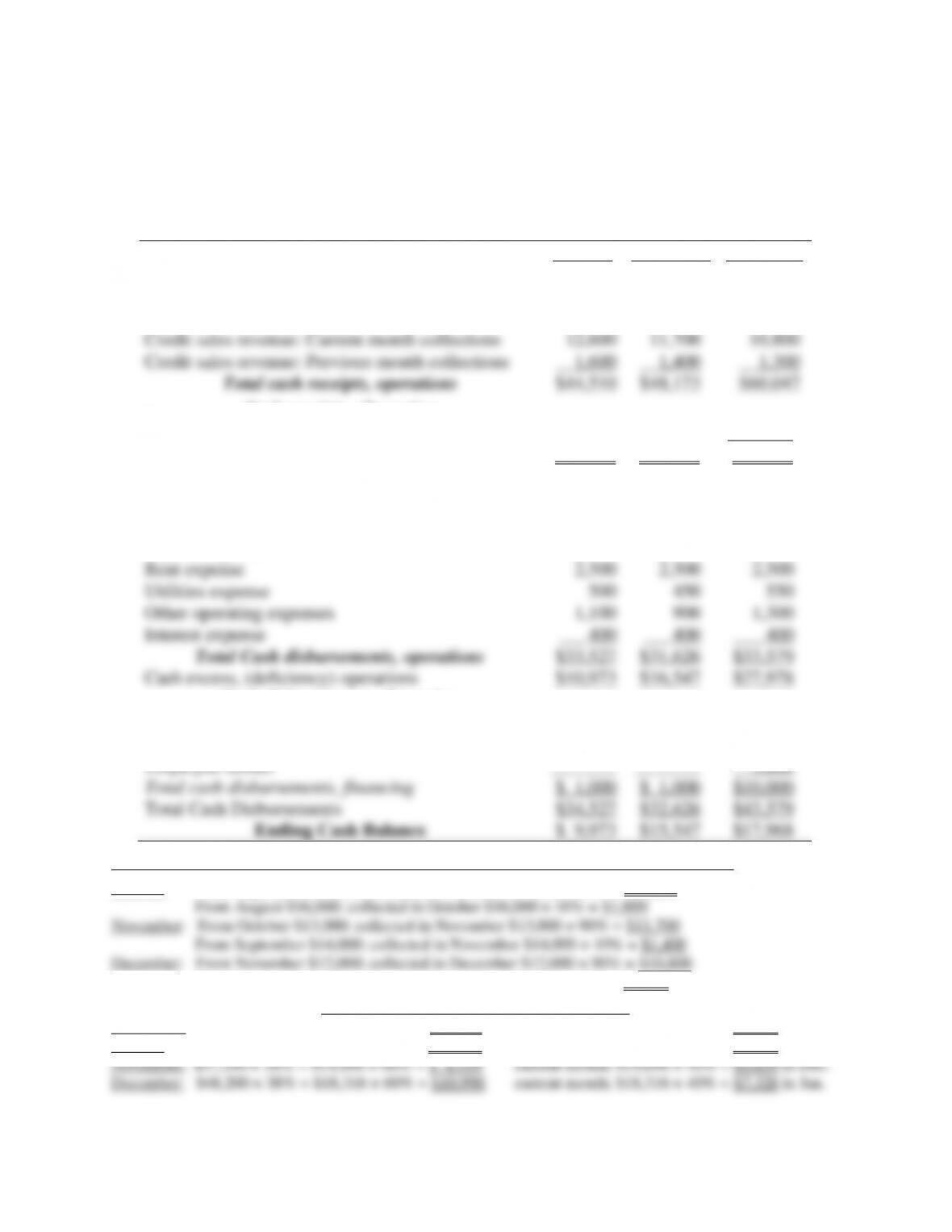

P11.3 Prepare a cash budget for each of the months of October, November, and December.

The beginning cash balance on October 1 is $2,410. Collections on credit sales revenue

averages 90% in the month following credit sales, and 10% in the month following.

Average cost of sales is 38% of total sales revenue. The cost of sales is 60% paid in the

current month and 40% in paid in the following month.

Cash Budget

October

November

December

Opening cash balance

$ 2,410

$ 9,973

$ 15,547

Cash receipts, operations

Sales revenue: Cash

27,900

25,100

32,400

Credit sales revenue: Current month collections

12,600

11,700

10,800

Credit sales revenue: Previous month collections

1,600

1,400

1,300

Total cash receipts, operations

$44,510

$48,173

$60,047

Cash receipts, financing

Sale of equipment

1,500

Total cash receipts, financing

$44,510

$48,173

$61,547

Cash disbursements, operations

Cost of sales: Current month [60%]

$9,325

$8,459

$10,990

Previous month [40%]

6,612

6,217

5,639

Payroll expense

13,100

12,700

12,200

Rent expense

2,500

2,500

2,500

Utilities expense

500

450

550

Other operating expenses

1,100

900

1,300

Interest expense

400

400

400

Total Cash disbursements, operations

$33,527

$31,626

$33,579

Cash excess, (deficiency) operations

$10,973

$16,547

$27,978

Cash disbursements, financing

Equipment

$1,000

$1,000

$1,000

New equipment

5,400

Employee Bonus

_______

_______

3,600

Total cash disbursements, financing

$ 1,000

$ 1,000

$10,000

Total Cash Disbursements

$34,527

$32,626

$43,579

Ending Cash Balance

$ 9,973

$15,547

$17,968

Credit sales receivables collections: 90% following the month of sales and 10% the next month:

October: From September $14,000: collected in October $14,000 × 90% = $12,600

From October $13,000: collected in November $13,000 × 10% = $1,300

Cost of sales cash disbursement calculations:

September: $43,500 × 38% = $16,530 × 60% = $ 9,918 current month; $16,530 × 40% = $6,612 in Oct.

October: $40,900 × 38% = $15,542 × 60% = $ 9,325 current month; $15,542 × 40% = $6,217 in Nov.

184

P11.4 Prepare a budgeted income statement and a cash budget, and comment.

a. Budgeted Income Statement for the month of June, 2008

Sales revenue [30 days × $1,500]

$45,000

Cost of sales [$45,000 × 38%]

( 17,100)

Gross margin

$27,900

Operating expenses

Wages & salaries expense [$45,000 × 37%]

$16,650

Rent expense

2,000

Interest expense

300

Other operating expenses [$45,000 × 10%]

4,500

Depreciation expense

1,800

Total operating expenses

( 25,250)

Operating income

$ 2,650

b. Cash Budget for the Month of June, 2008

Beginning cash balance

$ 1,000

Cash receipts, operations

Cash sales revenue [$45,000 × 40%]

18,000

Credit card sales revenue [$45,000 x 60% x 88%]

23,760

Total cash available

$42,760

Cash disbursements, operations

Cost of sales [$45,000 × 38%]

$17,100

Wages & salaries expense [$45,000 × 37%]

16,650

Rent expense

2,000

Loan interest expense

300

Total cash disbursements, operations

(36,050)

Cash excess (deficiency)

$ 6,710

Cash disbursements, Financing

Loan repayment

( 3,000)

Ending cash balance

$ 3,710

c. The budgeted income statement shows a positive operating income of $2,650, and

the ending cash is also positive at $3,710. However, the ending cash increased to

185

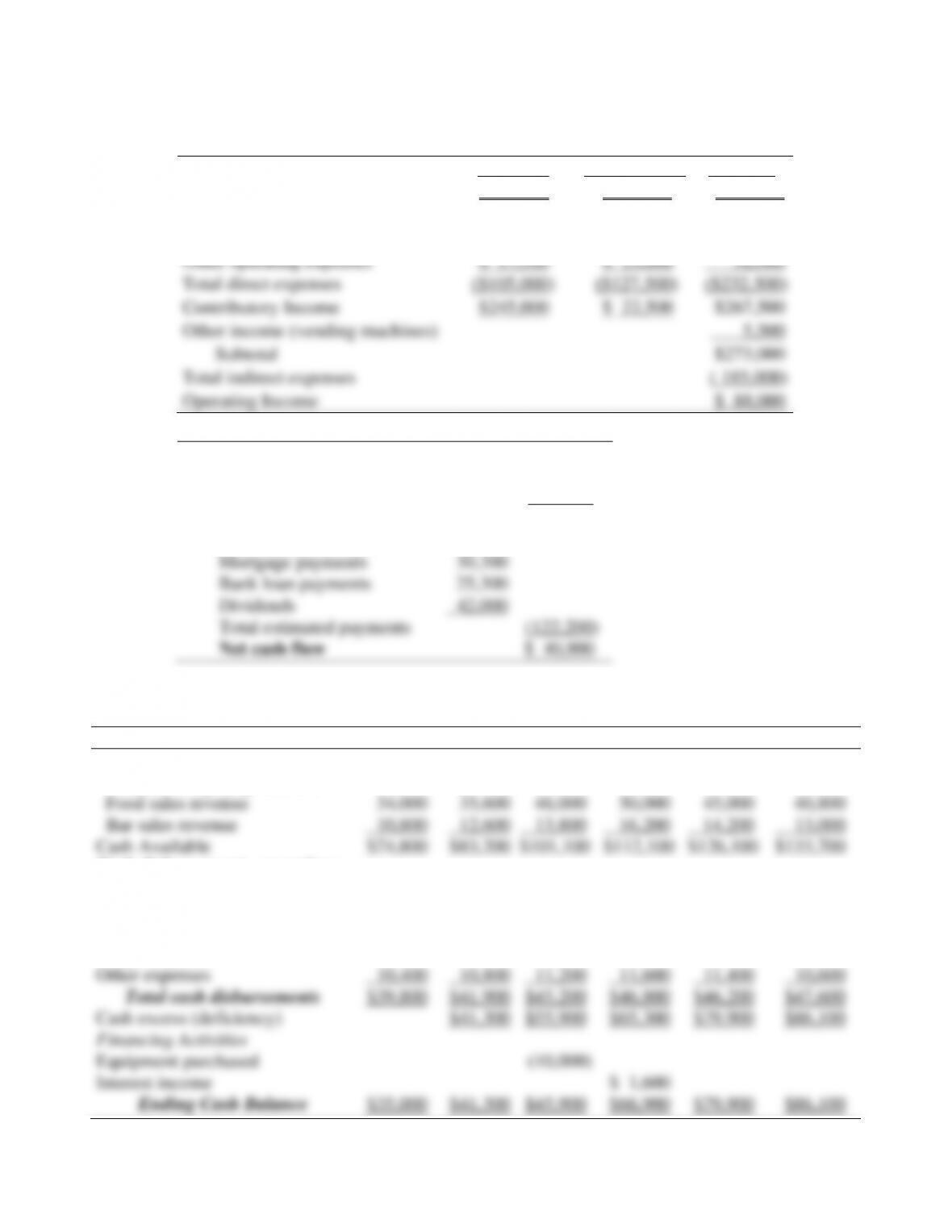

P11.5 Prepare a budgeted income statement for Year 0007 and calculate cash flow.

a. Budgeted Income Statement

Rooms

Dining Room

Total

Sales revenue

$350,000

$150,000

$500,000

Wages expense

$ 87,500

$ 60,000

$147,500

Cost of sales: food

52,500

52,500

Other operating expenses

$ 17,500

$ 15,000

32,500

Total direct expenses

($105,000)

($127,500)

($232,500)

Contributory Income

$245,000

$ 22,500

$267,500

Other income (vending machines)

5,500

Subtotal

$273,000

Total indirect expenses

( 185,000)

Operating Income

$ 88,000

b. Cash Flow for Year 0007

Adjustments

Operating income

$ 88,000

Add back: depreciation

75,000

Subtotal

$163,000

New equipment (net)

$24,600

Mortgage payments

30,300

Bank loan payments

25,300

Dividends

42,000

Total estimated payments

(122,200)

Net cash flow

$ 40,800

P11.6 Prepare a cash budget for six months.

Cash Budget

April

May

June

July

August

September

Beginning balance:

$30,000

$35,000

$ 41,300

$ 45,900

$66,900

$ 79,900

Cash receipts, operations

Food sales revenue

34,000

35,600

46,000

50,000

45,000

40,800

Bar sales revenue

10,800

12,600

13,800

16,200

14,200

13,000

Cash Available

$74,800

$83,200

$101,100

$112,100

$126,100

$133,700

Cash disbursements, operations

Cost of sales purchases:

Cost of sales, Food

$12,000

$12,500

$13,600

$14,000

$14,600

$16,600

Cost of sales, Bar

4,400

4,800

5,400

6,400

6,800

8,200

Wages expense

13,000

13,800

15,000

14,800

13,400

12,200

Other expenses

10,400

10,800

11,200

11,600

11,400

10,600

Total cash disbursements

$39,800

$41,900

$45,200

$46,800

$46,200

$47,600

Cash excess (deficiency)

$41,300

$55,900

$65,300

$79,900

$86,100

Financing Activities

Equipment purchased

(10,000)

Interest income

$ 1,600

Ending Cash Balance

$35,000

$41,300

$45,900

$66,900

$79,900

$86,100

186

P11.7 Calculate beginning cash and prepare a cash budget. Prepare an income statement for

three months and a balance sheet as of March 31, 0008.

Beginning cash:

Cash from stock shares sold [40,000 × $6.00]

$240,000

Cost of building

$120,000

Cost of equipment

90,000

Cost of china, etc.

18,000

Cost of inventory

7,000

Cash disbursements

(235,000)

Beginning cash balance

$ 5,000

(1) Budgeted Income Statement

For the First Quarter Ending March 31, 0008

January

February

March

Sales revenue

$30,200

$60,800

$90,400

Cost of sales

( 11,476)

( 23,104)

(34,352)

Gross Margin

$18,724

$37,696

$56,048

Operating Expenses

Other operating expenses

$ 3,800

$ 3,800

$ 3,800

Salaries & Wages Expense:

Fixed salaries & wages expense

5,200

5,200

5,200

Variable salaries & wages expense

1,560

10,740

19,620

Depreciation Expenses:

Building

500

500

500

Furniture & Equipment

750

750

750

China, Silverware, etc.

300

300

300

Total operating expenses

12,110

21,290

30,170

Operating income

$ 6,614

$16,406

$25,878

(2) Cash Budget

January

February

March

Opening cash balance

$ 5,000

$ 11,260

$20,422

Cash sales receipts, operations

Current month sales revenue

$16,610

$33,440

$49,720

Previous month sales revenue

13,590

27,360

Total cash available

$21,610

$58,290

$97,502

Cash Disbursements

Cost of sales: Current month

$ 4,590

$ 9,242

$13,741

Cost of sales: Previous month

6,886

13,862

Salaries and Wages Expense

Fixed salaries & wages expense

5,200

5,200

5,200

Variable salaries & wages expense

1,560

10,740

19,620

Other operating expenses

3,800

3,800

Total cash disbursements

$11,350

$35,868

$56,223

Cash excess (deficiency)

$11,260

$22,422

$41,279

Financing Activities

Increased inventory

(2,000)

(2,000)

Closing cash

$ 11,260

$20,422

$39,279

187

(3) Balance Sheet, March 31, 0008

Assets

Current Assets

Cash

$ 38,279

Accounts receivable

40,680

Inventory

11,000

Total current assets

$ 89,959

Property Plant & Equipment

Building

$120,000

Less: Accumulated depreciation

( 1,500)

$118,500

Furniture & Equipment

90,000

Less: Accumulated depreciation

( 2,250)

87,750

China, Silverware, etc.

18,000

Less: Accumulated depreciation

( 900)

17,100

Net Property Plant & Equipment

$223,350

Total Assets

$313,309

Liabilities & Stockholders’ Equity

Current Liabilities

Accounts payable

$ 24,411

[($90,400 x 38% x 60%) + $3,800]

Stockholders’ Equity

Common stock

$240,000

Retained earnings [$6,614 + $16,406 + $25,878]

48,898

$288,898

Total Liabilities & Stockholders’ Equity

$313,309

P11.8 a. Budgeted Income statement

For the First Three Months

Month 1

Month 2

Month 3

Sales revenue

$48,000

$66,000

$84,000

Cost of sales

$14,400

$19,800

$25,200

Salaries & wages expense

15,000

16,200

19,800

Other expenses

4,800

6,600

8,400

Rent expense

3,000

3,000

3,000

Depreciation expenses:

Furniture & Equipment

3,000

3,000

3,000

China, glass & silverware

2,100

42,300

2,100

50,700

2,100

61,500

Net income

$ 5,700

$15,300

$22,500

Retained Earnings

$ 5,700

$21,000

$43,500

188

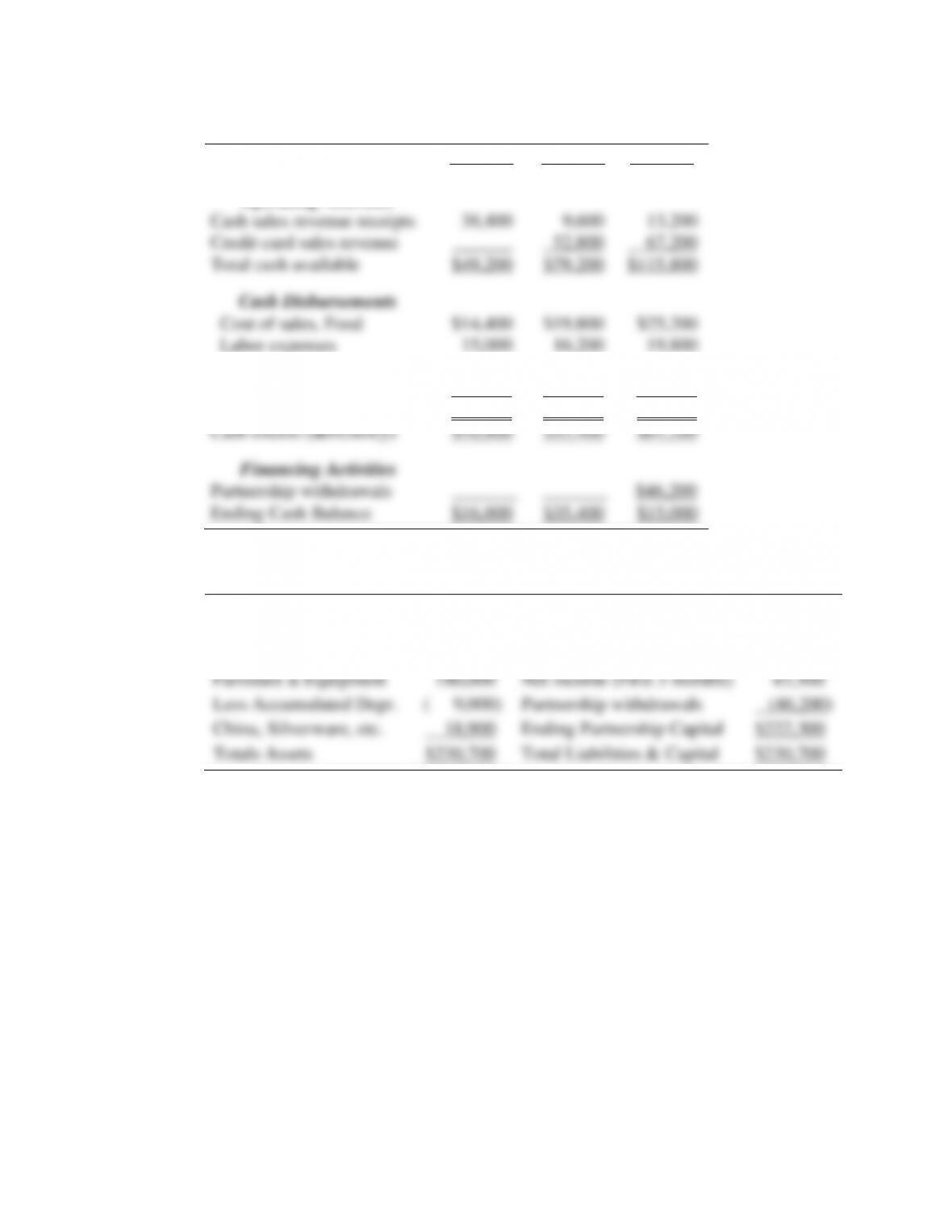

b. Cash Budget

For the First Three Months

Month 1

Month 2

Month 3

Beginning cash balances:

$10,800

$16,800

$ 35,400

Operating Activities

Cash sales revenue receipts

38,400

9,600

13,200

Credit card sales revenue

______

52,800

67,200

Total cash available

$49,200

$79,200

$115,800

Cash Disbursements

Cost of sales, Food

$14,400

$19,800

$25,200

Labor expenses

15,000

16,200

19,800

Other expenses

4,800

6,600

Rent expense

3,000

3,000

3,000

Total cash disbursements

$32,400

$43,800

$54,600

Cash excess (deficiency)

$16,800

$35,400

$61,200

Financing Activities

Partnership withdrawals

_______

_______

$46,200

Ending Cash Balance

$16,800

$35,400

$15,000

c. Balance Sheet (Condensed)

For the First Three Months

Cash

$ 15,000

Accounts payable

$ 8,400

Inventory

9,000

Accounts receivable

16,800

Beginning partnership

capital

225,000

Furniture & Equipment

180,000

Net income (First 3 months)

43,500

Less Accumulated Depr.

( 9,000)

Partnership withdrawals

(46,200)

China, Silverware, etc.

18,900

Ending Partnership Capital

$222,300

Totals Assets

$230,700

Total Liabilities & Capital

$230,700

189

P11.9 Determine the level of sales revenue after tax flow to achieve a cash flow of $27,000.

a. After tax cash flow is: $27,000 + $42,000 fixed costs − $21,000 depreciation. Net

Net Income [AT] $48,000 $48,000 $64,000

1 − tax rate 1 − 25% 75%

b. Confirmation of $170,000 sales revenue level will meet cash flow objective.

Sales revenue

$170,000

Variable cost [30% × $170,000]

$51,000

Fixed costs

55,000

Subtotal

(106,000)

Operating income [BT]

$ 64,000

Tax 25% [$64,000 × 25%]

( 16,000)

Net Income (after tax)

$ 48,000

Add: Depreciation

21,000

Deduct: Loan payments

( 42,000)

Cash flow

$ 27,000

190

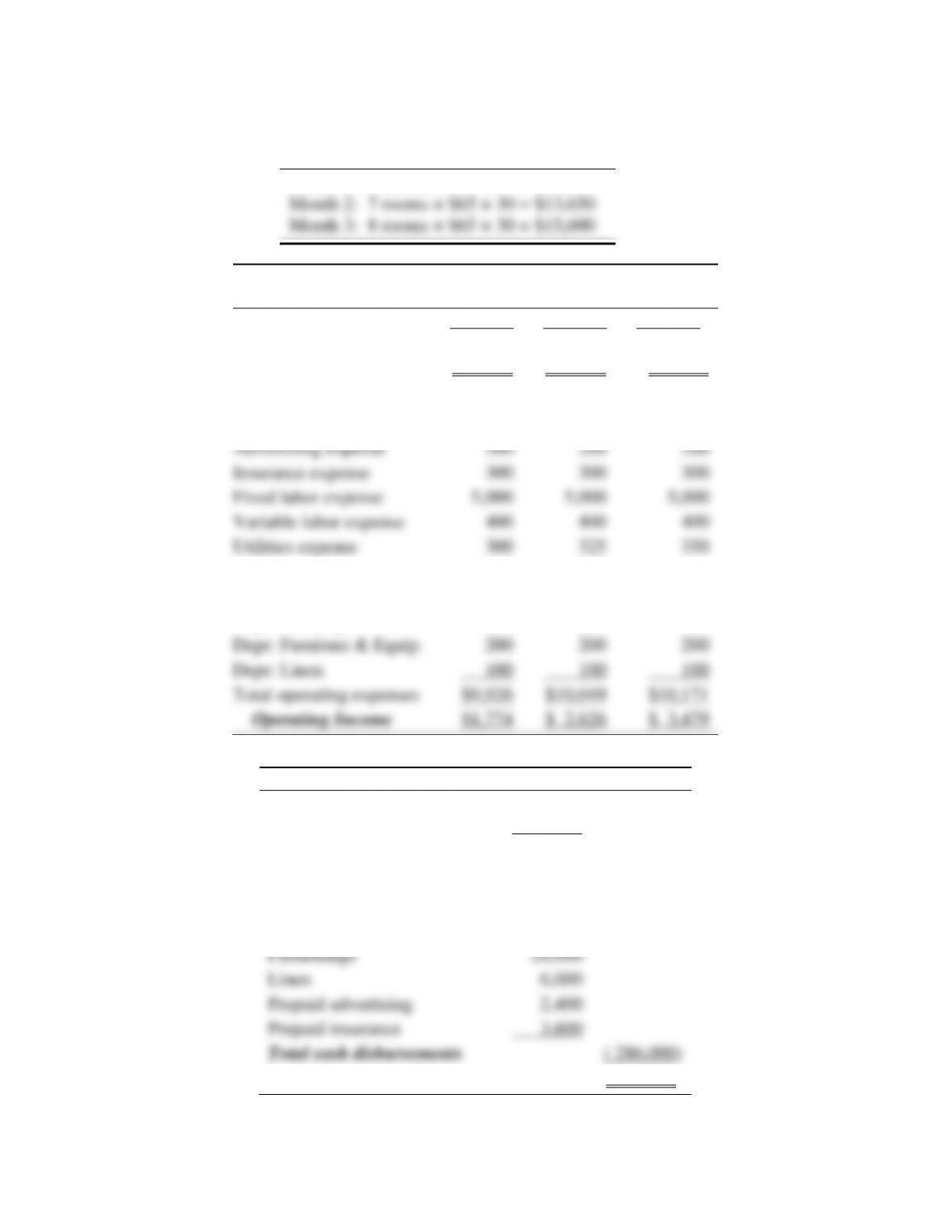

P11.10 For each of three months, prepare an income statement, determine the beginning cash

and complete a cash budget.

Room sales revenue calculations:

Month 1: 6 rooms × $65 × 30 = $11,700

Cece Saw’s Motel

Income Statement for the First Quarter Ending March 31

Month 1

Month 2

Month 3

Occupancy rate

60%

65%

70%

Rooms sales revenue

$11,700

$12,675

$13,650

Operating Expenses

Laundry expense

$1,170

$1,268

$1,365

Advertising expense

200

200

200

Insurance expense

300

300

300

Fixed labor expense

5,000

5,000

5,000

Variable labor expense

400

400

400

Utilities expense

300

325

350

Office supplies expense

100

100

100

Interest expense

1,600

1,600

1,600

Depr: Building

556

556

556

Depr: Furniture & Equip.

200

200

200

Depr: Linen

100

100

100

Total operating expenses

$9,926

$10,049

$10,171

Operating Income

$1,774

$ 2,626

$ 3,479

Beginning Cash Calculation

Cash investment

$ 50,000

Long-term mortgage

240,000

Total Cash Available

$290,000

Cash Disbursements

Land

$ 50,000

Building

200,000

Furnishings

24,000

Linen

6,000

Prepaid advertising

2,400

Prepaid insurance

3,600

Total cash disbursements

( 286,000)

Beginning cash balance

$ 4,000

191

Cece Saw’s Motel

Cash Budget for the First Quarter Ending March 31

January

February

March

Beginning cash balances

$ 4,000

$ 9,930

$15,897

Operating Activities

Cash rooms sales revenue

$11,700

$12,675

$13,650

Cash available

$15,700

$22,065

$29,547

Cash Disbursements

Laundry expense

$ 1,170

$ 1,268

$ 1,365

Salaries expense, fixed

1,500

1,500

1,500

Wages expense, variable

400

400

400

Utilities expense

-0-

300

325

Office supplies expense

100

100

100

Interest expense

1,600

1,600

1,600

Total cash disbursements

$ 4,770

$ 5,168

$ 5,290

Cash excess (deficiency)

$10,930

$16,897

$24,257

Financing Activities

Loan principal repayment

($1,000)

($ 1,000)

( $1,000)

Closing cash

$9,930

$15,897

$23,257

192

Cece Saw’s Motel

Balance Sheet for the First Quarter Ending March 31

Assets

Current Assets

Cash

$23,797

Prepaid advertising

1,800

Prepaid insurance

2,700

Total current assets

$ 28,297

Property Plant & Equipment

Land

$ 50,000

Building

200,000

Less: Accumulated depreciation

( 1,668)

198,332

Furnishings & Equipment

24,000

Less: Accumulated depreciation

( 600)

23,400

Linen

6,000

Less: Accumulated depreciation

( 300)

5,700

Net Property Plant & Equipment

277,432

Total Assets

$305,729

Liabilities and Stockholders’ Equity

Current Liabilities

Accounts payable

$ 350

Wages payable

10,500

Short-term portion mortgage payable

12,000

Total current liabilities

$ 22,850

Long-Term Liabilities

Stockholders’ loan payable

$ 40,000

Mortgage payable

225,000

Total long-term liabilities

$265,000

Stockholders’ Equity

Common stock

$ 10,000

Retained earnings

7,879

Total stockholders’ equity

$ 17,879

Total Liabilities & Stockholders’ Equity

$305,729

193

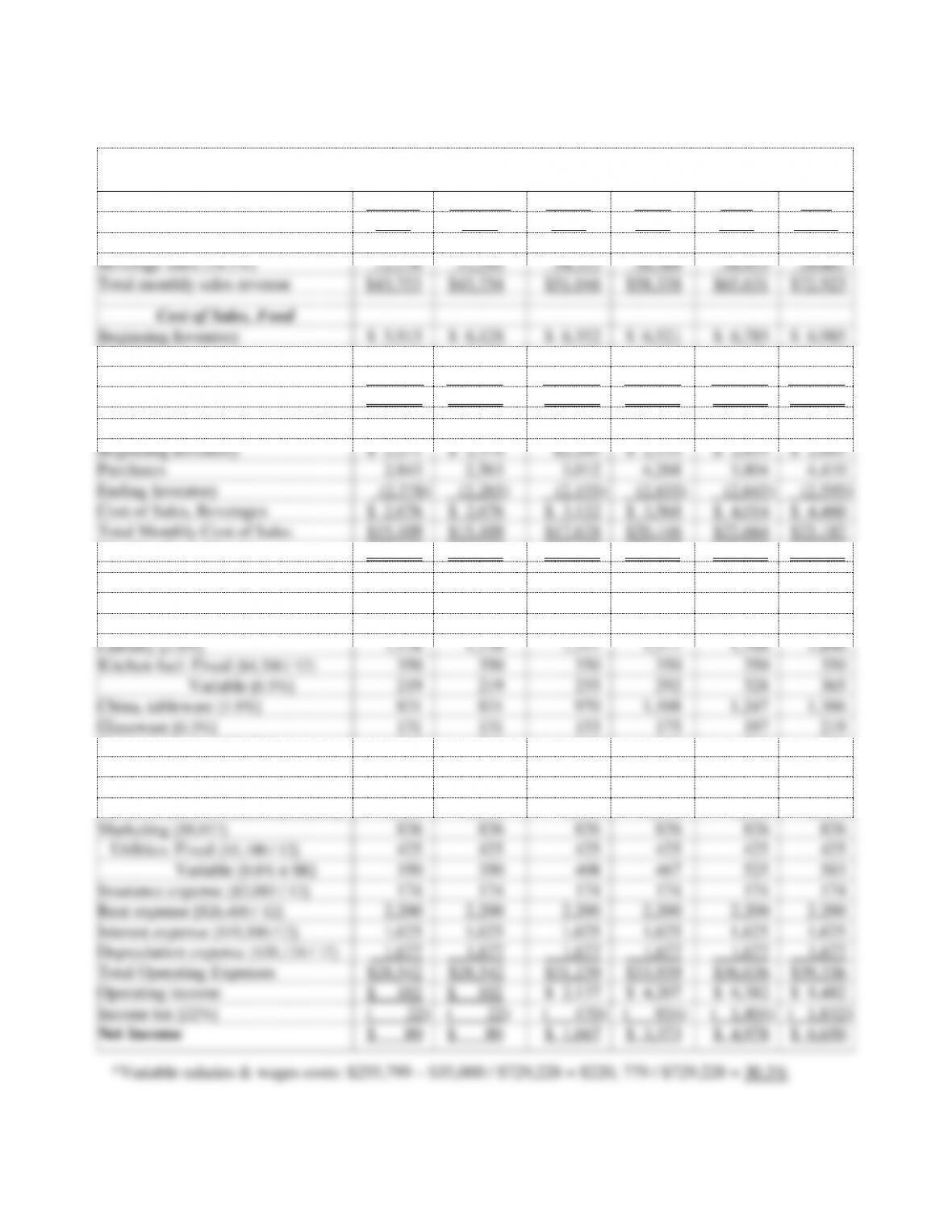

CASE 11 SOLUTIONS

4C Company

Monthly Operating Budget for Months January Through June, Year 2008

Sales Revenue

January

February

March

April

May

June

Monthly sales revenue percentage

6.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Food sales [71.9%]

$31,477

$31,477

$36,723

$41,970

$47,216

$52,462

Beverage sales [28.1%]

12,276

12,295

14,323

16,369

18,415

20,461

Total monthly sales revenue

$43,753

$43,754

$51,046

$58,338

$65,631

$72,923

Cost of Sales, Food

Beginning Inventory

$ 5,915

$ 6,128

$ 6,352

$ 6,521

$ 6,785

$ 6,985

Purchases

12,646

12,657

14,675

16,842

18,850

21,062

Ending Inventory

( 6,128)

( 6,352)

( 6,521)

( 6,785)

( 6,985)

( 7,325)

Cost of Sales, Food [28.4%]

$12,433

$12,433

$14,506

$16,578

$18,650

$20,722

Cost of Sales, Beverage

Beginning Inventory

$ 2,211

$ 2,378

$2,265

$ 2,155

$ 2,855

$ 2,645

Purchases

2,843

2,563

3,012

4,268

3,804

4,410

Ending Inventory

(2,378)

(2,265)

(2,155)

(2,855)

(2,645)

(2,595)

Cost of Sales, Beverages

$ 2,676

$ 2,676

$ 3,122

$ 3,568

$ 4,014

$ 4,460

Total Monthly Cost of Sales

$15,109

$15,109

$17,628

$20,146

$22,664

$25,182

Monthly Gross Margin

$28,644

$28,644

$33,418

$38,192

$42,967

$47,741

Operating Expenses

Salaries,fixed [$35,000]

$ 2,917

$ 2,917

$ 2,917

$ 2,917

$ 2,917

$ 2,917

Wages, variable [30.3%]*

13,257

13,257

15,467

17,676

19,886

22,096

Laundry [2.6%]

1,138

1,138

1,327

1,517

1,706

1,896

Kitchen fuel: Fixed [$4,200 / 12]

350

350

350

350

350

350

Variable [0.5%]

219

219

255

292

328

365

China, tableware [1.9%]

831

831

970

1,108

1,247

1,386

Glassware [0.3%]

131

131

153

175

197

219

Contract cleaning [$6,506]

542

542

542

542

542

542

Licenses [$3,205]

267

267

267

267

267

267

Other operating [$4,375] [.006 x SR]

263

263

306

350

394

438

Administrative & General [$16,204]

1,350

1,350

1,350

1,350

1,350

1,350

Marketing [$9,917]

826

826

826

826

826

826

Utilities: Fixed [$5,100 / 12]

425

425

425

425

425

425

Variable [0.8% x SR]

350

350

408

467

525

583

Insurance expense [$2,085 / 12]

174

174

174

174

174

174

Rent expense [$26,400 / 12]

2,200

2,200

2,200

2,200

2,200

2,200

Interest expense [$19,500 /12]

1,625

1,625

1,625

1,625

1,625

1,625

Depreciation expense [$20,124 / 12]

1,677

1,677

1,677

1,677

1,677

1,677

Total Operating Expenses

$28,542

$28,542

$31,239

$33,939

$36,636

$39,336

Operating income

$ 102

$ 102

$ 2,137

$ 4,207

$ 6,382

$ 8,482

Income tax [22%]

( 22)

( 22)

( 470)

( 934)

( 1,404)

( 1,832)

Net Income

$ 80

$ 80

$ 1,667

$ 3,373

$ 4,978

$ 6,650

*Variable salaries & wages costs: $255,799 – $35,000 / $729,228 = $220, 779 / $729,228 = 30.3%

194

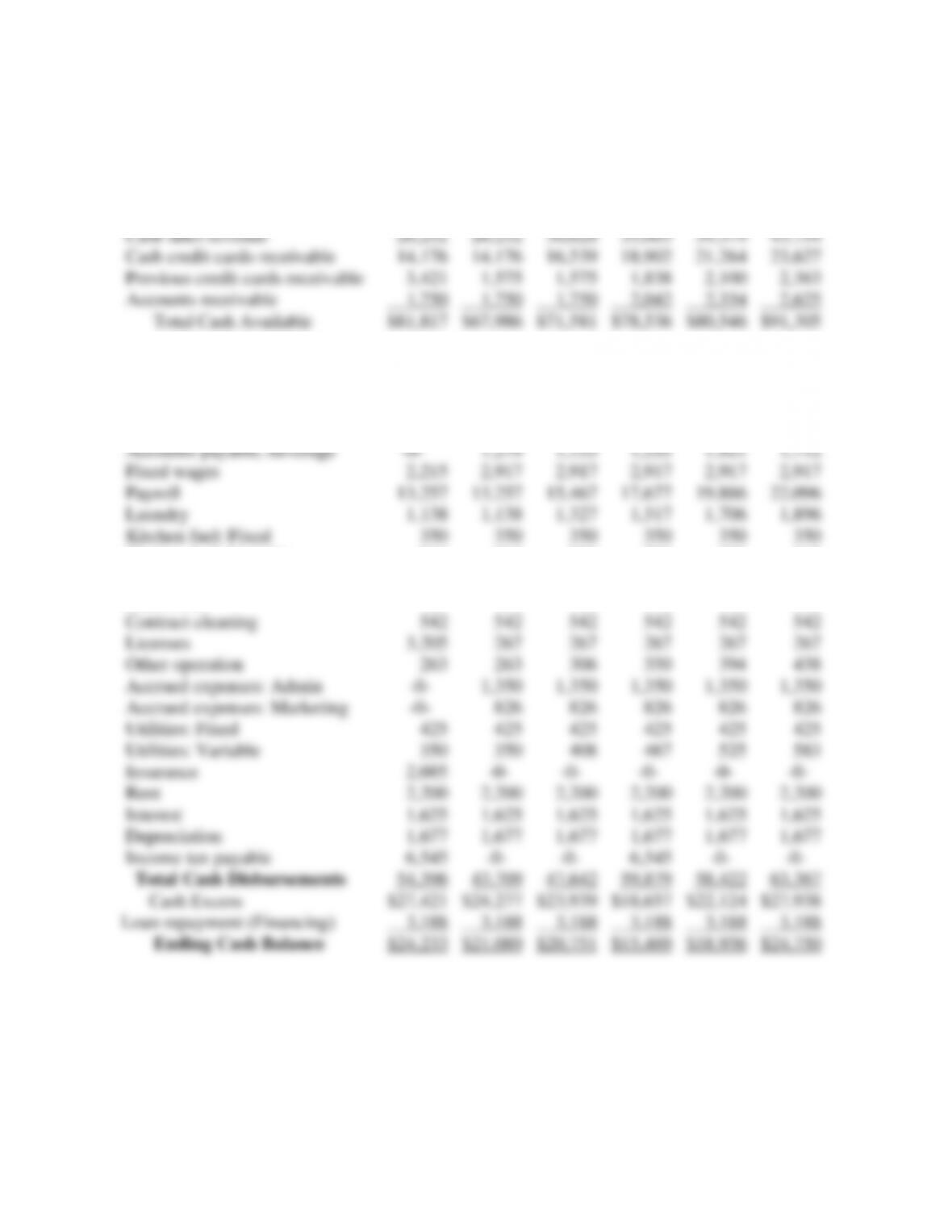

4C Company

Monthly Cash Budget for Months January Through June, Year 2008

January

February

March

April

May

June

Beginning Cash Balance

$36,218

$24,233

$21,089

$20,751

$15,469

$18,936

Cash Receipts

Cash sales revenue

26,252

26,252

30,628

35,003

39,379

43,754

Cash credit cards receivable

14,176

14,176

16,539

18,902

21,264

23,627

Previous credit cards receivable

3,421

1,575

1,575

1,838

2,100

2,363

Accounts receivable

1,750

1,750

1,750

2,042

2,334

2,625

Total Cash Available

$81,817

$67,986

$71,581

$78,536

$80,546

$91,305

Cash Disbursements

Cash food purchases

$6,955

$6,961

$8,071

$9,263

$10,368

$11,584

Accounts payable, food

8,819

5,691

5,696

6,604

7,579

8,483

Cash beverage purchases

1,564

1,410

1,657

2,347

2,092

2,426

Accounts payable, beverage

-0-

1,279

1,153

1,355

1,921

1,712

Fixed wages

2,215

2,917

2,917

2,917

2,917

2,917

Payroll

13,257

13,257

15,467

17,677

19,886

22,096

Laundry

1,138

1,138

1,327

1,517

1,706

1,896

Kitchen fuel: Fixed

350

350

350

350

350

350

Kitchen fuel: Variable

219

219

255

292

328

365

China, tableware

831

831

970

1,108

1,247

1,386

Glassware

131

131

153

175

197

219

Contract cleaning

542

542

542

542

542

542

Licenses

3,205

267

267

267

267

267

Other operation

263

263

306

350

394

438

Accrued expenses: Admin

-0-

1,350

1,350

1,350

1,350

1,350

Accrued expenses: Marketing

-0-

826

826

826

826

826

Utilities: Fixed

425

425

425

425

425

425

Utilities: Variable

350

350

408

467

525

583

Insurance

2,085

-0-

-0-

-0-

-0-

-0-

Rent

2,200

2,200

2,200

2,200

2,200

2,200

Interest

1,625

1,625

1,625

1,625

1,625

1,625

Depreciation

1,677

1,677

1,677

1,677

1,677

1,677

Income tax payable

6,545

-0-

-0-

6,545

-0-

-0-

Total Cash Disbursements

54,396

43,709

47,642

59,879

58,422

63,367

Cash Excess

$27,421

$24,277

$23,939

$18,657

$22,124

$27,938

Loan repayment (Financing)

3,188

3,188

3,188

3,188

3,188

3,188

Ending Cash Balance

$24,233

$21,089

$20,751

$15,469

$18,936

$24,750