161

CHAPTER 10

STATEMENT OF CASH FLOWS

AND

WORKING CAPITAL ANALYSIS

INTRODUCTION

The statement of cash flows and working capital analysis are discussed in this chapter. As you

will see, both statements have in common the analysis and evaluation of current assets and

current liabilities. The statement of cash flows (indirect method) converts an accrual income

statement to a cash basis statement. It adjusts net income (or net loss) by identifying cash inflows

and outflows as positive or negative adjustments. Non-cash expenses and non-operating gains or

losses from the disposal of non-current assets adjust the cash balance based on their effect on the

cash account. Day-to–day management of working capital is an important aspect of managing

any enterprise and such an analysis shares the same concept of identifying cash inflows and

outflows that increase or decrease working capital (current assets minus current liabilities). This

chapter demonstrates how a statement of cash flows and a statement of source inflows and use

outflows of working capital are developed. A good grasp of Chapters 2 and 3 will serve as a

solid foundation for this chapter. The discussion of working capital analysis in this chapter will

be of great assistance in Chapter 11 that discusses cash management.

TRUE or FALSE QUESTIONS

(Correct answer indicated by T for True answers and F for False answers)

1. Total current assets − total current liabilities = working capital.

T

2. The SCF is considered a major financial statement as is the balance sheet and the

income statement.

T

3. The financing activities section of a SCF evaluates transactions between the company

and its creditors and owners.

T

4. The operating activities section of a SCF, indirect method, evaluates only the disposal

of depreciable assets.

F

5. If a current asset account balance increases over an accounting period, the increase is

treated as a negative number in a SCF.

T

6. Depreciation and amortization for the period are treated as positive numbers and

added back in the operating section of a SCF, indirect method.

T

7. Gains on the disposal of non-current assets are treated as a positive number and losses

are treated as a negative number on a SCF.

F

8. The three sections of a SCF are: operating activities, investing activities and financing

activities.

T

162

9. The payment of cash dividends is treated as a positive number in the financing

activities section of a SCF.

F

10. The operating activities section of a SCF, indirect method, generally evaluates current

assets, and liabilities, non-cash expenses, and gains or losses on the disposal of non–

current assets.

T

11. The increasing or decreasing of long-term debt is evaluated in the financing activity

section of a SCF.

T

12. The difference between the direct and indirect methods of preparing a SCF only

affects the operating section of the statement.

T

13. The statement of source inflows and use outflows of working capital shows certain

transactions that occurred at a specific point in time.

F

14. One of the purposes of a statement of source inflows and use outflows of working

capital is to provide prospective investors with information.

T

15. Depreciation expense is a use of working capital.

F

16. The purchase of a fixed asset is a source of working capital.

F

17. A loss from operations is a use of working capital.

T

18. Payment of dividends will decrease working capital.

T

19. A transaction affecting a current asset and a current liability account only will not

affect working capital.

T

20. When compiling a statement of source inflows and use outflows of working capital,

detailed information from the current asset and liability accounts on the balance sheet

is required.

F

21. Information in addition to that provided by the income statement, the retained earn–

ings statement, and the balance sheets is sometimes required to compile a statement of

source inflows and use outflows of working capital.

T

22. The net change in working capital figure from the statement of source inflows and use

outflows of working capital need not be reconciled with any other figures.

F

23. If an establishment sold a long-term asset for $3,000 and purchased a new one for

$20,000, only the difference of $17,000 will appear as a use of funds in the statement

of source inflows and use outflows of working capital.

F

24. The statement of changes in working capital accounts shows how individual current

asset and liability accounts increased or decreased during the period.

T

25. If the statement of changes in individual working capital accounts shows an increase

in current liabilities during the period, this will cause a decrease in total working

capital.

T

26. A statement of changes in individual working capital accounts must be prepared

before a statement of source inflows and use outflows of funds can be compiled.

F

163

27. The actual amount of working capital is not as indicative of a company’s debt paying

ability as is its current ratio.

T

28. The current ratio is total current liabilities divided by total current assets.

F

29. The current ratio in a hotel or restaurant should be higher than 2:1.

F

MULTIPLE CHOICE QUESTIONS

(Correct answer indicated by asterisk)

1. Working capital is:

(a) The amount of cash one has in the bank

(b) The amount of cash required for purchase of capital or fixed assets

2. The three major activities evaluated in a SCF are:

(c) Operating, investing, and managing

(d) Operating, profiting, and financing

3. If kitchen equipment were purchased for $24,400 during the current period, the cost of the

purchase would be shown as a:

(c) Negative number in the financing section of the SCF

(d) Positive number in the investing section of the SCF

4. Restaurant furnishings with an original cost of $38,000 and accumulated depreciation

account of $32,000, was sold for $4,200 cash. How will the proceeds of the sale be reported

in a SCF, indirect method?

(a) In the financing section, cash inflow of $1,800

(b) In the investing section, cash inflow of $1,800

5. A restaurant owner borrowed $150,000 from a bank on a long-tem note. This transaction

would be shown on a SCF as $150,000 cash?

(a) Inflow in the operations section

6. Depreciation expense on the income statement was $8,000. Which of the following

statements is correct?

(c) Depreciation is not reported in a SCF

(d) Accumulated depreciation is debited for $8,000

164

7. The source inflows and use outflows of a working capital statement shows:

(c) How current assets and liabilities were increased during the year

(d) The source inflows and use outflows of the cash account during the period

8. A small corporate restaurant repurchased 5,000 shares of its own stock for $50,000 cash

during the current period. How is this shown in a SCF?

(a) A positive cash flow in the investing section

(b) A positive cash flow in the operating section

9. One of the following is not a use of working capital:

(c) Payment of principal on a long-term liability

(d) Loss from operations

10. Which of the following is not a source of working capital?

(a) Sale of a fully depreciated asset for $1,000

(b) Issuance of new stock

11. If marketable securities owned by a company were sold for cash, this would be a/an:

(a) Source of working capital

(b) Increase in current assets

12. If the furniture and equipment account balance was $50,000 at the beginning of the period

and $40,000 at the end of the period, we could assume that:

or more purchases and sales of assets

(c) More than $10,000 of assets were sold and some new assets were purchased

(d) Working capital has been decreased by $10,000

13. The statement of changes in working capital is a:

(a) Part of the statement of source inflows and use outflows of working capital

(b) Statement showing increases in current asset accounts and decreases in current liability

accounts

165

14. If the statement of changes in working capital showed that a bank loan had been decreased

from the beginning to the end of the period, this would be a/an:

(c) Source of working capital

(d) Use of working capital

15. It is important to know the dollar amount of working capital at any time because it:

(a) Shows a company’s apparent ability to pay off current liabilities

(b) Is indicative of a company’s collection rate on accounts receivable

16. If two different companies had the same dollar amounts of working capital:

(c) They would be equally good short-term credit risks

(d) They will have identical statements of source and use of working capital

17. A motel can operate with a relatively low current ratio because:

(c) It operates on cash rather than a charge basis

(d) Its inventory turns over very rapidly

18. If current assets are $75,000 and current liabilities are $100,000, the current ratio is?

(a) 1:0.75

(b) Too low to continue in business

EXERCISE SOLUTIONS

E10.1 Identify category of account and the effect of a balance change.

Category

Account Balance

Account Title

CA or CL

Increased

Decreased

Credit card receivables

CA

Use

Source

Accounts payable

CL

Source

Use

Inventory (for resale)

CA

Use

Source

Accounts receivable

CA

Use

Source

Prepaid expenses

CA

Use

Source

Accrued payroll payable

CL

Source

Use

Interest payable

CL

Source

Use

Marketable securities

CA

Use

Source

166

E10.2 Net income was $180,000. Inventory (for resale) increased $12,000 and Accounts

payable increased by $9,000. Determine the net cash flow from operations, indirect

method.

Net income $180,000

E10.3 Net income $280,000, depreciation expense $38,000, accounts receivable decreased

$2,400; credit card receivables decreased $2,600; prepaid insurance increased $2,880;

inventory decreased $3,700; accounts payable increased $4,700; other accrued payables

decreased $3,600. Complete net cash flow from operations, indirect method.

Net Income

$280,000

Depreciation expense

$38,000

Accounts receivable

2,400

Credit card receivables

2,600

Prepaid insurance

( 2,880)

Inventory

3,700

Accounts payable

4,700

Other accrued payables

( 3,600)

Net adjustments

44,920

Net cash flow from operations

$324,920

E10.4 Identify the inflows and outflows of working capital.

Net income

Inflow

Sale of equity stock

Inflow

Net loss

Outflow

Purchase of equipment

Outflow

Depreciation

Inflow

Repayment long-term debt

Outflow

Cash dividends

Outflow

Increasing long-term debt

Inflow

Sales of equipment

Inflow

Redemption of stock

Outflow

E10.5 Cash flow ratios: Cash flow from operating activities $178,200; average CL $58,800,

average total liabilities $666,500; sales revenue $2,555,450; and interest $59,000.

a. The cash flow from operating activities to current liabilities ratio

$178,200 / $58,800 = 3.03 times or 303%

=

+

=

Liabilities

Capital

January 1, 2008

$137,500

=

E10.6 Identify whether the transaction belongs to investing or financing and its effect as an

increase or decrease in a Statement of Cash Flows.

Investing or

Financing

Increase (+) or

Decrease (−)

Investing

Decrease (−)

Purchase equipment.

Financing

Increase (+)

Sold shares of equity stock.

Investing

Increase (+)

Sold office furniture.

Investing

Decrease (−)

Purchased a long-term investment.

Financing

Decrease (−)

Declared and paid a cash dividend.

Financing

Decrease (−)

Repurchased equity stock.

Financing

Increase (+)

Increased long-term debt.

E10.7 Determine the cash from operations by adjusting specific items of working capital.

Working capital $87,500; accounts receivable increased $4,600, inventory decreased

$7,754, and accounts payable increased by $3,737.

168

E10.11 Determine the net cash flows from investing and financing activities.

Investing Activities

a. Equipment purchased: ($44,480)

Old equipment sold: $ 1,200

E10.12 Analyze each transaction and comment on transactional effects on working capital.

a. No effect to working capital (WC); Purchased inventory (CA) on account (CL).

The addition of both a CA and a CL of the same value does not change WC.

d. Working capital will increase since cash (CA) and marketable securities (CA)

would be reduced by the cost of the securities. The resulting gain of $4,800 is

charged to a non-current account.

PROBLEM SOLUTIONS

P10.1 Complete an evaluation of cash flows for operating activities only, using the indirect

method.

Net income

$43,900

Adjustments to reconcile Net Income:

Operating Activities

Accounts receivable, increased

($10,420)

Inventory, increased

( 1,875)

Depreciation (Automatic add back)

8,000

Accounts payable, decreased

( 5,782)

Other current liabilities, increased

3,500

Tax payable, decreased

( 1,970)

Net adjustments

( 8,547)

Net cash flow, operating activities

$35,353

169

P10.2 Complete a SCF using the indirect method.

Statement of Cash Flows, Indirect Method

Net income

$112,400

Adjustments to reconcile Net Income:

Operating Activities

Credit card receivables, increased

($ 680)

Accounts receivable, increased

( 1,500)

Inventories, increased

( 1,200)

Prepaid expenses, decreased

800

Accounts payable, decreased

( 2,100)

Accrued payroll payable, increased

2,400

Taxes payable, decreased

( 900)

Depreciation expense

120,000

Gain on disposal, furnishings

( 3,200)

Loss on disposal of equipment

800

Net adjustments to reconcile Net Income

114,420

Net cash flow, operating activities

$226,820

Investing Activities

Sold furnishings

$ 8,600

Sold equipment

2,000

Purchased new furnishings

(16,800)

Purchased new equipment

(24,200)

Net Cash Flow from Investing Activities

($ 30,400)

Financing Activities

Reduction to long-term debt

($ 54,800)

Cash dividends declared and paid

( 122,400)

Net cash flow, financing activities

($177,200)

Net cash flow, increase

$ 19,220

Cash balance, December 31, 0007

$ 12,020

Cash balance, December 31, 0008

$ 31,240

P10.3 Calculate a statement of changes in working capital and prepare a statement of source-

inflows and uses-outflows for the year ended December 31, 0008.

Change in Working Capital

Year 0007

Year 0008

Current assets

$31,000

$33,000

Current liabilities

( 7,000)

( 8,000)

Working capital

$24,000

$25,000

Increase in working capital

1,000

$25,000

$25,000

170

P10.3 (Continued)

Statement of Source Inflows and Use Outflows of Working Capital

Source inflows of working capital

Net income

$7,000

Depreciation expense

1,000

New shares of equity stock

1,000

Increase in loan

2,000

Total source inflows of working capital

$11,000

Use outflows of working capital

Purchase of new equipment

$4,000

Payment of cash dividends

6,000

Total use outflows of working capital

($10,000)

Net increase in working capital

$ 1,000

P10.4 Using information from P10.3, complete a SCF using the indirect method.

Statement of Cash Flows for the Year Ended December 31, 0008

Net income

$ 7,000

Adjustments to reconcile Net Income:

Operating Activities

Credit card receivables, decreased

$ 66

Accounts receivable, decreased

534

Food inventories, increased

( 1,350)

Beverage inventories, increased

( 450)

Depreciation expense

1,000

Accounts payable, increased

2,300

Accrued expenses payable, decreased

( 100)

Income tax payable, decreased

( 1,200)

1,100)

Net adjustments to reconcile Net Income

800

Net cash flow, operating activities

$ 7,800

Investing Activities

Purchased equipment

($4,000)

Net cash flow, investing activities

($ 4,000)

Financing Activities

Cash dividend distributed

($6,000)

Issued new shares of equity stock for cash

1,000

Loan-term loan increased

2,000

Net cash flow, financing activities

($ 3,000)

Net cash flow increase

$ 800

Cash balance, December 31, 0007

14,800

Cash balance, December 31, 0008

$15,600

171

P10.5

Changes in Working Capital

Effect on Working Capital

12-31-07

12-31-08

Increase (WC)

Decrease (WC)

Current Assets

Cash

$ 4,100

$ 5,200

$1,100

Credit card receivables

4,700

5,500

800

Accounts receivable

1,200

700

500

Inventory

3,000

3,600

600

Marketable securities

8,000

7,000

$1,000

Prepaid expenses

1,200

1,500

300

Totals

$22,200

$23,500

$2,800

$1,500

Current Liabilities

Accounts payable

$ 6,900

$ 7,000

100

Accrued expenses payable

1,400

1,700

300

Income tax payable

2,000

1,500

500

Current mortgage payable

11,500

10,400

1,100

______

Totals

$21,800

$20,600

$4,400

$1,900

Net working capital

$ 400

$ 2,900

Net change

2,500

_______

2,500

Totals

$ 2,900

$ 2,900

$4,400

$4,400

P10.6 Prepare a statement of source-inflows and use-outflows of working capital for the year

ending December 31, 0008.

Statement of Source Inflows and Use Outflows of Working Capital

Source inflows of working capital

Net income

$ 6,800

Depreciation [From P10.5: $8,300 + $3,700]

12,000

12,000

Total source inflows of working capital

$18,800

Use outflows of working capital

Cash dividends distributed

$ 3,200

Purchased new furniture [From P10.5: $25,400 – $22,700]

2,700

Mortgage reduction

10,400

Total use outflows of working capital

($16,300)

Net change, increase to working capital

$ 2,500

172

P10.7 Prepare a SCF, indirect method. P10.5 and P10.6 are referred to for the necessary

information.

Statement of Cash Flows for the Year Ended December 31, 0008

Net income

$ 6,800

Adjustments to reconcile Net Income

Operating Activities

Credit card receivables, increased

(800)

Accounts receivable, decreased

500

Inventory, increased

(600)

Marketable securities, decreased

1,000

Prepaid expenses, increased

(300)

Depreciation, building

8,300

Depreciation, furniture and equipment

3,700

Accounts payable, increased

100

Accrued expenses payable, increased

300

Income taxes payable, decreased

(500)

Current mortgage payable, decreased

( 1,100)

Net adjustments to reconcile Net Income

10,600

Net cash flow, operating activities

$17,400

Investing Activities

Purchased furniture and equipment

($2,700)

Net cash flow, investing activities

( 2,700)

Financing Activities

Reduced long-term mortgage

($11,500)

Cash dividends paid

( 3,200)

Net cash flow, financing activities

(14,700)

Net cash flow increase

$ 1,100

Cash balance, December 31, 0007

4,100

Cash balance, December 31, 0008

$ 5,200

P10.8 Determine the changes in working capital and prepare the catering company’s statement

of source inflows and use outflows for the year ended December 31, 0008.

Change in Working Capital

Year 0007

Year 0008

Current assets

$35,700

$38,800

Current liabilities

( 28,700)

( 41,300)

$ 7,000

($ 2,500)

Decrease in working capital

9,500

$ 7,000

$ 7,000

173

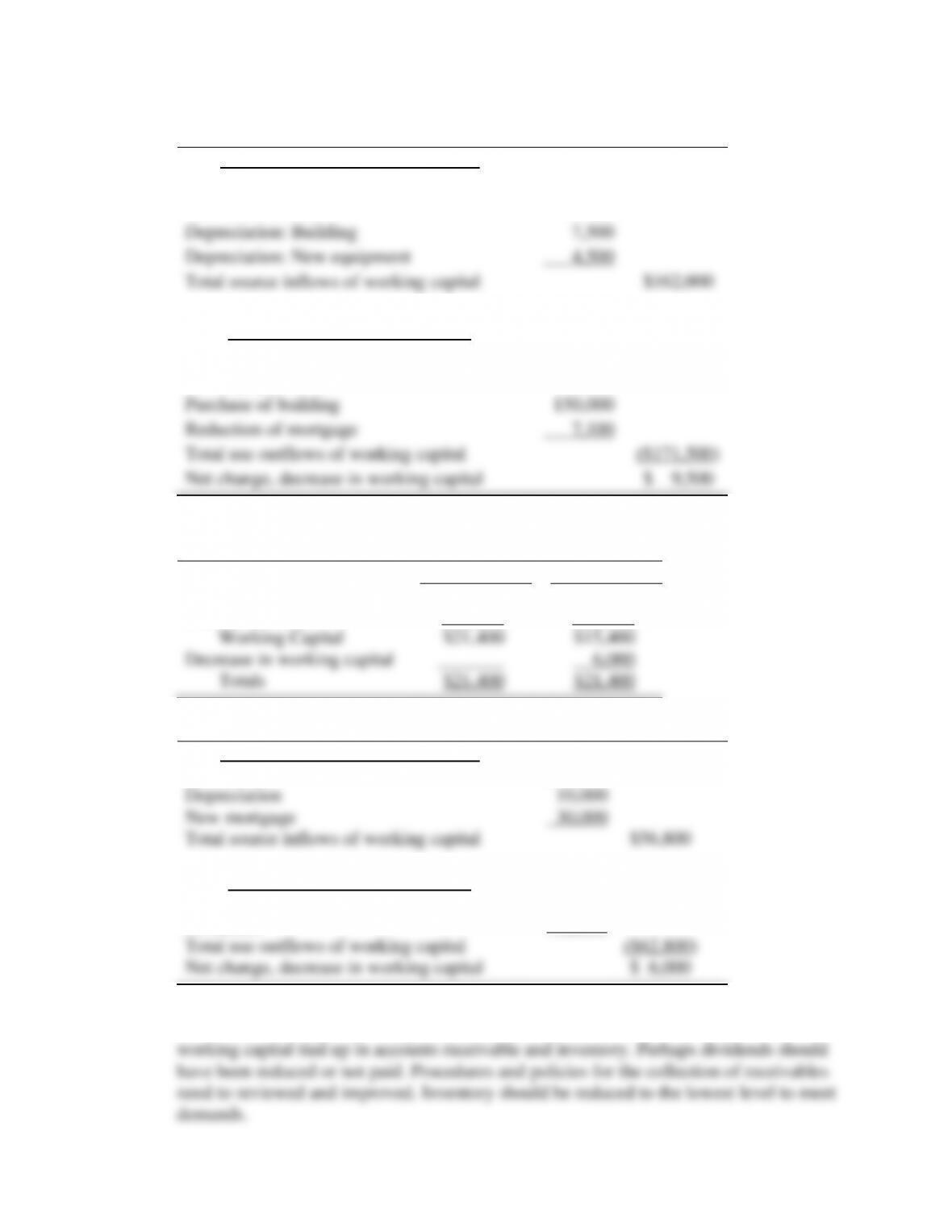

Statement of Source Inflows and Use Outflows of Working Capital

Source inflows of working capital

Net mortgage

$140,000

New stock shares

10,000

Depreciation: Building

7,500

Depreciation: New equipment

4,500

Total source inflows of working capital

$162,000

Use outflows of working capital

Operating loss

$ 8,100

New equipment

6,300

Purchase of building

150,000

Reduction of mortgage

7,100

Total use outflows of working capital

($171,500)

Net change, decrease in working capital

$ 9,500

P10.9 Change in Working Capital

Year 0007

Year 0008

Current assets

$28,100

$36,100

Current liabilities

( 6,700)

( 20,700)

Working Capital

$21,400

$15,400

Decrease in working capital

6,000

Totals

$21,400

$21,400

Statement of Source Inflows and Use Outflows of Working Capital

Source inflows of working capital

Net income

$16,800

Depreciation

10,000

New mortgage

30,000

Total source inflows of working capital

$56,800

Use outflows of working capital

Purchase of building

$50,000

Dividends

12,800

Total use outflows of working capital

($62,800)

Net change, decrease in working capital

$ 6,000

The working capital was reduced by $6,000 during the year even though net income was

earned. As well, liquidity was greatly reduced. Reduction of liquidity is due to more

174

CASE 10 SOLUTION

Complete a SCF from the pro-forma balance sheet for Year 2008 (Case 2 balance sheet).

4C Company

Statement of Cash Flows for Year Ending, December 31, 2008

Cash Flows from Operations

Net income

$46,410

Adjustments to reconcile Net Income

Operating Activities

Depreciation

$20,124

Credit card receivables, increased

( 3,819)

Accounts receivable, increased

( 2,413)

Food inventory, increased

( 437)

Beverage inventory, decreased

16

Prepaid expenses, increased

( 40)

Accounts payable, decreased

( 2)

Accrued payroll, increased

702

Income tax payable, increased

3,404

Net adjustments to reconciled net income

17,535

Net cash flow, operating activities

$63,945

Financing Activities

Common stock repurchased

($20,000)

Repayment of long-term debt

( 38,260)

Net cash flows, financing activities

($58,260)

Net cash flow increase

$ 5,685

Beginning cash, December 31, 2007

$36,218

Ending cash, December 31, 2008

$41,903