1

CHAPTER 1

BASIC FINANCIAL ACCOUNTING REVIEW

INTRODUCTION

This chapter reviews basic accounting principles and procedures. It is a necessary chapter for

those whose accounting background is poor. If students have recently completed an introductory

accounting course, this chapter could be omitted, or assigned for self review. Chapters 1 and 2

lay the foundation for most of the remaining chapters in the textbook.

TRUE OR FALSE QUESTIONS

(Correct answer indicated by T for True answers and F for False answers)

1. Accounting principles and concepts are broad rules developed to create a common

language used by accountants.

T

2. A business owner’s personal assets should be included with the assets of the business

entity.

F

3. The cost principle of valuing assets may not indicate the true value of the assets as time

goes by.

T

4. Accrual accounting is based on the principle of matching sales revenue with expenses.

T

5. Cash basis accounting is never used in business.

F

6. The full-disclosure principle states that all accounting records should be available at

any time to anyone who wants to look at them.

F

7. Changing depreciation methods from one period to the next would not conform to the

principle of consistency.

T

8. The materiality of a particular transaction may need to be considered in deciding

whether or not to conform to other accounting principles.

T

9. Depreciation is a method of allocating the cost of a long-lived asset to an expense over

the life of the asset.

T

10. Straight-line depreciation allocates the cost of a long-lived asset in equal units of time

over the life of the asset.

T

11. Assets plus liabilities equal ownership equity.

F

12. Sales revenue − Cost of sales = Gross Margin.

T

13. The term operating income identifies operating income before income tax.

T

14. Assets − ownership equity equals liabilities.

T

15. Double-entry-accrual accounting ensures the balance sheet equation is always kept in

balance, as long as no errors are made in recording and posting transactions.

T

2

16. The debit side of a ledger account is always the left column. It is used to post debit

values of a transaction.

T

17. A debit entry to a debit balanced ledger account will decrease the balance of the

account.

F

18. A credit entry to a credit balanced account will increase the account balance.

T

19. An expense account carries a normal debit balance.

T

20. A trial balance showing the total of the debit and credit balanced accounts are equal at

the end of an accounting period indicates all entries have been correctly posted.

F

21. Adjusting entries are normally necessary at the end of an accounting period to conform

to the matching principle.

T

22. Beginning inventory + Purchases − Ending inventory = Cost of goods sold.

T

23. A sales revenue account is debit balanced.

F

24. The portion of a prepaid account to be expensed will require a debit to the prepaid

account and a credit to an expense account.

F

25. End of period adjusting entries is recorded in a journal before the adjustments are

posted to the ledger accounts.

T

MULTIPLE CHOICE QUESTIONS

(Correct answers indicated by asterisk)

1. A cocktail lounge owner who takes home liquor for private parties at home without reflecting

this in the lounge’s accounting records is violating the:

(a) Matching principle

(b) Going concern concept

2. A restaurant that records all purchases of food and beverages as an expense at the time of

purchase and does not consider the end of period inventories would be violating the:

(a) Cost principle

(b) Materiality concept

3. The cost principle is concerned with:

(c) Valuing long-lived assets at their current market value rather than at cost

(d) Setting menu prices at a certain mark-up over cost

3

4. The balance sheet equation can be expressed as:

(a) Assets = Liabilities + Owners’ equity

(b) Assets − Liabilities = Owners’ equity

5. A restaurant purchased a new point of sale terminal by paying one-half of its cost in cash and

owing the balance on account. The journal entry requires a:

(c) debit to an asset, a debit to a liability, and a credit to a liability

(d) debit to two assets and a credit to a liability account

6. The length of the period of an accounting cycle is:

(c) Monthly for all hospitality enterprises

(d) Quarterly for a resort hotel

7. If cash was paid for a two-year $3,600 insurance policy on July 1, the amount of the

insurance expensed on December 31 is:

(c) $2,700

(d) $ 600

8. A five-year depreciable asset cost $10,000 and had a residual value of $1,000. What is the

balance of its accumulated depreciation account at the end of two years using straight-line

depreciation?

(a) $6,000

(b) $4,000

9. Which of the following is correct?

(a) Debits decrease assets

(b) Debits decrease assets; credits increase liabilities

10. Cost of goods sold is calculated as:

(c) Beginning inventory − Ending inventory − Purchases

(d) Beginning inventory + Ending inventory + Purchases

4

11. The normal balance of each of the five basic categories of balance sheet and income

statement accounts are either debit or credit balanced. Which of the following is not correct?

(c) Expense: A debit balanced account

(d) Asset: Debit balanced account

12. The inflow of assets as a result of business operations occurs from:

(a) A capital investment

(b) Borrowing through long-term debt

13. The posting of a transaction refers to:

(c) Comparing postings from the general journal to the ledger accounts

(d) Recording transactions in a general journal

14. The outflow of assets as a result of business operations are called:

(c) Ownership equity

(d) Receivables

15. A restaurant purchased an ice machine for $4,000 paying $1,000 in cash with the balance

carried on account. The journal entry to record this transaction is which of the following?

(c) Debit equipment $1,000, credit accounts payable $3,000

(d) Debit equipment $3,000, credit cash $4,000

16. A ledger shows:

(a) A chronological record of all accounting transactions

(b) A balance of all balance sheet accounts

EXERCISE SOLUTIONS

E1.1 a. The Full Disclosure principle

b. The Full Disclosure and the Consistency principles

5

E1.2 Write a short explanation of the following terms:

a. Operating Income: Describes income before income taxes when sales revenue is

greater than total costs.

E1.3 Identify the normal balance as Debit or Credit for each of each the following:

Ownership

Sales

Operating

Account:

Assets

Liabilities

Equity

Revenue

Expenses

Balance:

Debit

Credit

Credit

Credit

Debit

E1.4 Write the abbreviated linear equation for the balance sheet and income statement.

E1.5 At the end of an accounting period, it was determined that wages of employees $858 and

management salaries $1,400 have been earned. Journalize the entry to accrue the wages

E1.6 A restaurant reported the following for the first quarter of year 0007: Sales revenue (SR)

of $420,680, cost of sales (CS) $201,928, and total expenses (TE) of $175,170. Find the

E1.7 For the month of March, a restaurant reported a beginning food inventory (BI) of

$18,662, ending food inventory (EI) of $16,882 and food purchases (P) for resale was

6

E1.8 Restaurant had $8,480 supplies on hand at the beginning April. During the month

$11,222 of supplies was purchased. At the end of the month a check of the supplies

indicated that $8,104 of supplies was on hand. Determine the amount of supplies used

E1.9 Equipment was purchased for $70,468. The equipment is estimated to have a serviceable

life of 8 years and a residual value of $2,500. Using straight-line depreciation, answer the

following:

E1.10 A new van was purchased for $40,000 and was estimated to have a life of 4 years or

110,000 miles; trade in (residual) value is estimated to be $4,800. In the first year, the

van was driven for 27,500 miles. a. Use the units-of-production method to determine

E1.11 Equipment was purchased for $46,400 with an estimated life of 8 years and a residual

value of $4,000. What is depreciation expense for the first year, a. Using Sum of the

8/36 × ($46,400 − $4,000) = 8/36 × $42,400 = $9,422.22 $9,422

7

E1.12 A restaurant paid $9,120 cash in advance for liability and casualty insurance for two

years of coverage:

a. Journalize the transaction for the prepaid.

Account Titles

Debit

Credit

Prepaid Insurance

$ 9,120

Cash

$ 9,120

b. What is the insurance expense for one year and for one month?

Prepaid cost / Prepaid life (years) = Insurance expense per year

$9,120 / 2 years = $4,560 per year

Prepaid cost / Prepaid life (months) = Insurance expense per month

$9,120 / 24 months = $380 per month

c. Record journal entry for six months of insurance expense

Account Titles

Debit

Credit

Insurance Expense (6 × $380)

$ 2,280

Prepaid Insurance

$ 2,280

E1.13 Referring to the journal entries you completed for E1.12 (a) and (c), name and post the

journal entries using the modified T account format as shown below.

Name: Cash

Name: Prepaid Insurance

Name: Insurance Expense

Debit

Credit

Balance

Debit

Credit

Balance

Debit

Credit

Balance

(Beginning

Balance)

$24,400

(Beginning

Balance)

$ -0-

(Beginning

Balance)

$ -0-

$9,120

15,280

$9,120

9,120

$2,280

$2,280

$ 2,280

6,840

E1.14 A business using the cash basis of accounting cannot locate all of its records for one

month of operations. Beginning cash $22,260, ending cash $18,388, and cash payments

were $162,800. Determine the unknown cash sales revenue:

Beginning Cash

Cash

+

Cash Sales?

−

Cash Payments

=

Ending Cash

$22,260

+

Unknown?

–

$162,800

=

$18,388

Reverse the functions of (+) and (−) beginning with Ending Cash

Ending Cash

+

Cash Payments

–

Beginning Cash

=

Cash Sales?

$18,388

+

$162,800

–

$22,260

=

$158,928

Proof

Beginning Cash

+

Cash Sales

−

Cash Payments

=

Ending Cash

$22,260

+

158,928

–

$162,800

=

$18,388

E1.15 A restaurant pays $10,800 in advance for six months’ building rent in advance and

recognizes rental expense every month.

a. What is the monthly rental expense?

9

g. Owner purchased supplies for $2,650 cash.

Account Titles

Debit

Credit

Supplies

$ 2,650

Cash

$ 2,650

h. Owner purchased $3,800 of food inventory on account.

Account Titles

Debit

Credit

Food Inventory

$ 3,800

Accounts Payable

$ 3,800

i. Owner paid $2,700 for a one-year liability and casualty insurance policy.

Account Titles

Debit

Credit

Prepaid Insurance

$ 2,700

Cash

$ 2,700

j. Employees were paid wages $12,800 and salaries $2,400.

Account Titles

Debit

Credit

Wages Expense

$ 12,800

Salaries Expense

2,400

Cash

$ 15,200

cards, and 2% on accounts receivable.

Account Titles

Debit

Credit

Cash

$ 38,520

Credit Card Receivables

3,424

Accounts Receivable

856

Sales Revenue

$ 42,800

l. Owner paid $16,600 on accounts payable.

Account Titles

Debit

Credit

Accounts Payable

$ 16,600

Cash

$ 16,600

m. Owner paid $8,000 on note payable, plus interest of $960.

Account Titles

Debit

Credit

Notes Payable

$ 8,000

Interest Expense

960

Cash

$ 8,960

10

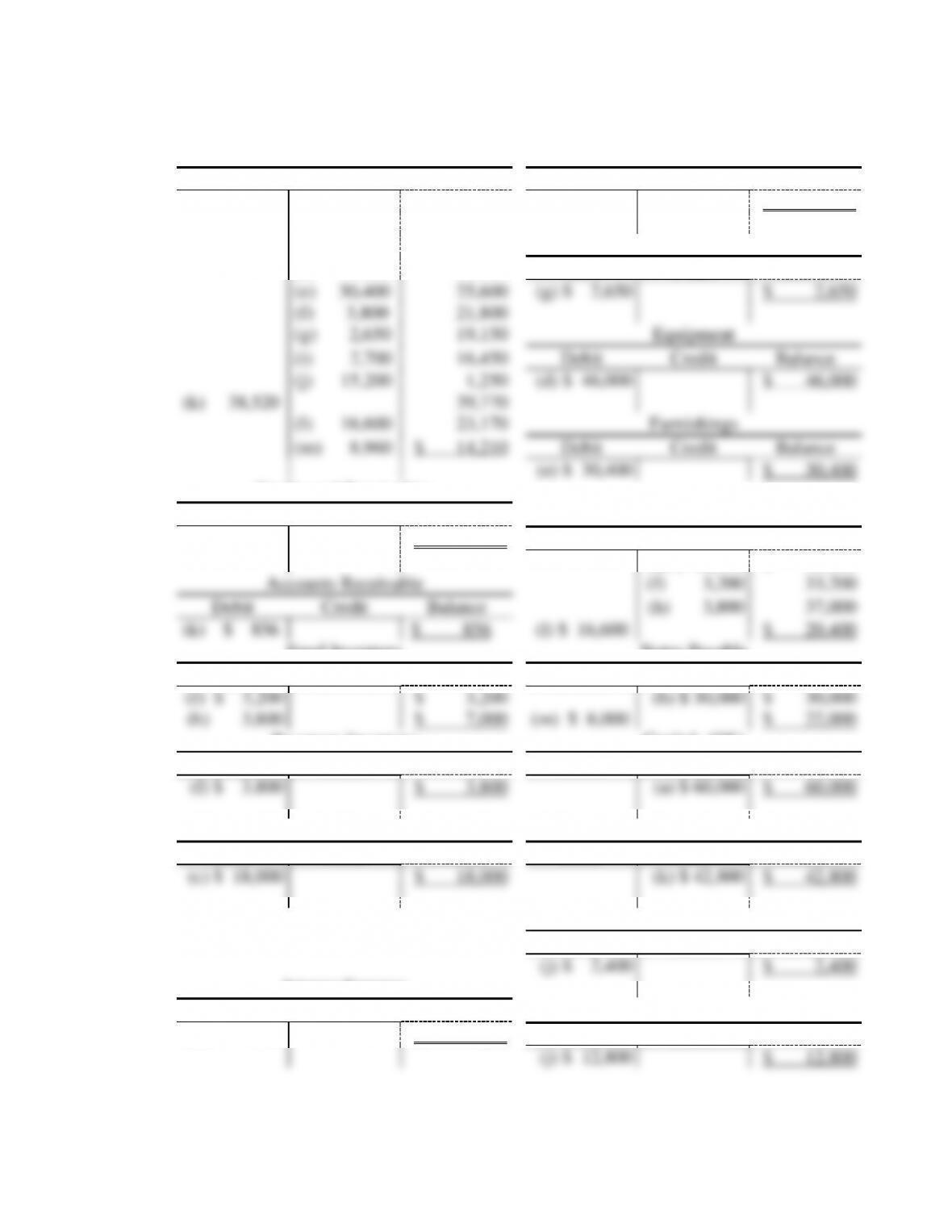

P1.1, Part 2: Solution posting journal entries to the General Ledger.

Cash

Prepaid Insurance

Debit

Credit

Balance

Debit

Credit

Balance

(a) $ 60,000

$ 60,000

(i) $ 2,700

$ 2,700

(b) 30,000

90,000

(c) $ 18,000

72,000

Supplies

(d) 16,000

56,000

Debit

Credit

Balance

(e) 30,400

25,600

(g) $ 2,650

$ 2,650

(f) 3,800

21,800

(g) 2,650

19,150

Equipment

(i) 2,700

16,450

Debit

Credit

Balance

(j) 15,200

1,250

(d) $ 46,000

$ 46,000

(k) 38,520

39,770

(l) 16,600

23,170

Furnishings

(m) 8,960

$ 14,210

Debit

Credit

Balance

(e) $ 30,400

$ 30,400

Credit card Receivables

Debit

Credit

Balance

Accounts Payable

(k) $ 3,424

$ 3,424

Debit

Credit

Balance

(d) $ 30,000

$ 30,000

Accounts Receivable

(f) 3,200

33,200

Debit

Credit

Balance

(h) 3,800

37,000

(k) $ 856

$ 856

(l) $ 16,600

$ 20,400

Food Inventory

Notes Payable

Debit

Credit

Balance

Debit

Credit

Balance

(f) $ 3,200

$ 3,200

(b) $ 30,000

$ 30,000

(h) 3,800

$ 7,000

(m) $ 8,000

$ 22,000

Beverage Inventory

Capital, (OE)

Debit

Credit

Balance

Debit

Credit

Balance

(f) $ 3,800

$ 3,800

(a) $ 60,000

$ 60,000

Prepaid Rent

Sales Revenue

Debit

Credit

Balance

Debit

Credit

Balance

(c) $ 18,000

$ 18,000

(k) $ 42,800

$ 42,800

Salaries Expense

Debit

Credit

Balance

(j) $ 2,400

$ 2,400

Interest Expense

Debit

Credit

Balance

Wages Expense

(m) $ 960

$ 960

Debit

Credit

Balance

(j) $ 12,800

$ 12,800

11

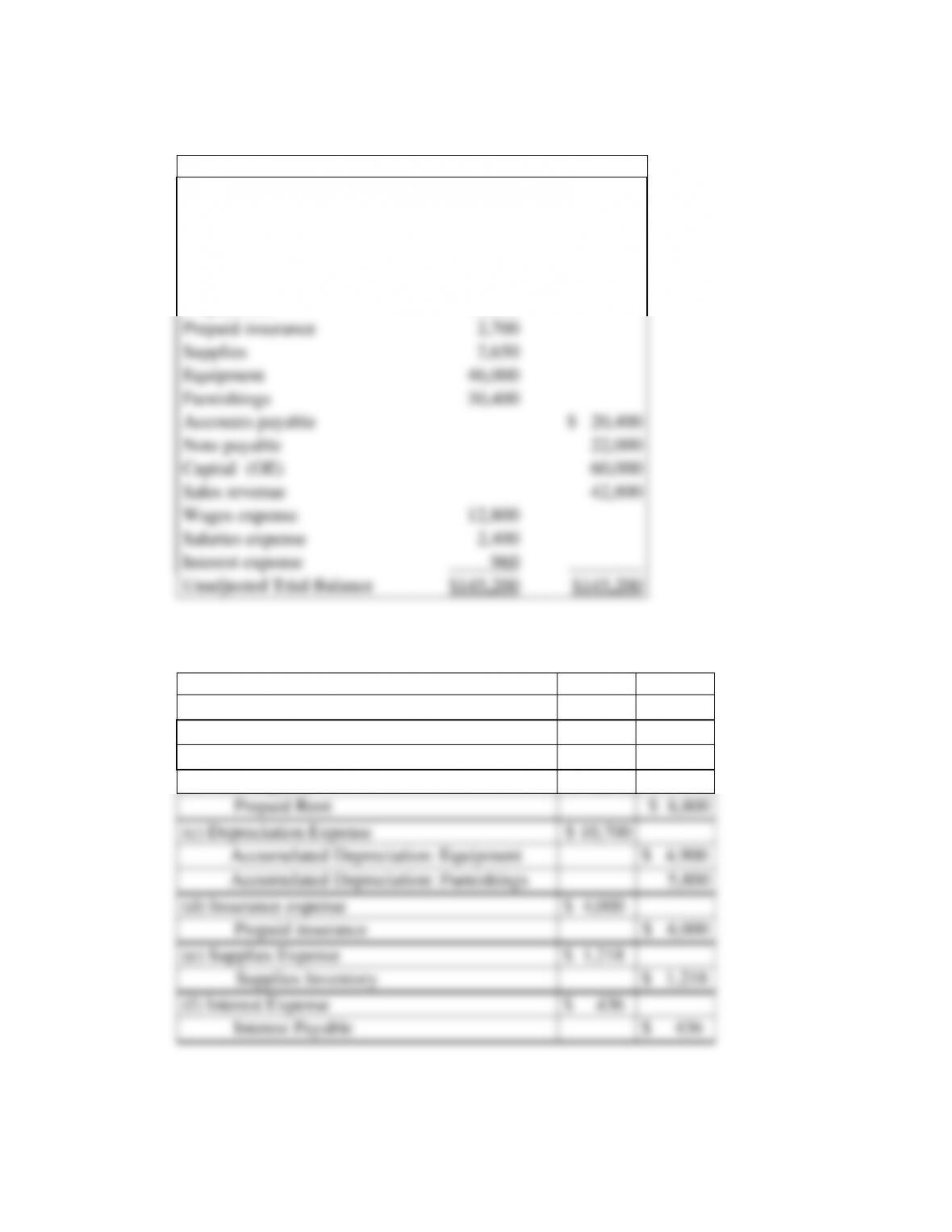

P1.1, Part 3: Solution: Unadjusted Trial Balance

March 31, 0006

Debit

Credit

Cash

$ 14,210

Credit card receivables

3,424

Accounts receivable

856

Food inventory

7,000

Beverage inventory

3,800

Prepaid rent

18,000

Prepaid insurance

2,700

Supplies

2,650

Equipment

46,000

Furnishings

30,400

Accounts payable

$ 20,400

Note payable

22,000

Capital (OE)

60,000

Sales revenue

42,800

Wages expense

12,800

Salaries expense

2,400

Interest expense

960

Unadjusted Trial Balance

$145,200

$145,200

P1.2 Solutions, Adjusting Journal Entries (single compound entry)

Account Titles

Debit

Credit

(a) Wages expense

$ 2,877

Salaries expense

1,400

Payroll payable

$ 4,277

(b) Rent Expense

$ 8,800

Prepaid Rent

$ 8,800

(c) Depreciation Expense

$ 10,700

Accumulated Depreciation: Equipment

$ 4,900

Accumulated Depreciation: Furnishings

5,800

(d) Insurance expense

$ 4,000

Prepaid insurance

$ 4,000

(e) Supplies Expense

$ 1,218

Supplies Inventory

$ 1,218

(f) Interest Expense

$ 436

Interest Payable

$ 436

12

P1.3 Part 1: Solutions, Journal Entries.

a. Owner invested $250,000 cash deposited in the business bank account.

Account Titles

Debit

Credit

Cash

$ 250,000

Capital

$ 250,000

b. Owner paid $108,000 cash for land.

Account Titles

Debit

Credit

Land

$ 108,000

Cash

$108,000

c. Owner borrowed $300,000 on a mortgage payable.

Account Titles

Debit

Credit

Cash

$ 300,000

Mortgage Payable

$ 300,000

d. Owner paid cash for a building, $285,400.

Account Titles

Debit

Credit

Building

$ 285,400

Cash

$ 285,400

e. Equipment was purchased for $48,000, paying $12,000 cash, and the

balance owed on a note payable.

Account Titles

Debit

Credit

Equipment

$ 48,000

Cash

$ 12,000

Notes Payable

36,000

f. Furnishings were purchased for $120,000 cash.

Account Titles

Debit

Credit

Furnishings

$ 120,000

Cash

$ 120,000

g. Linen inventory was purchased for $7,894 cash.

Account Titles

Debit

Credit

Linen Inventory

$ 7,894

Cash

$ 7,894

h. Supplies were purchased $3,200 of supplies on account.

Account Titles

Debit

Credit

Supplies

$ 3,200

Accounts Payable

$ 3,200

13

i. Vending inventory was purchased for $540 cash.

Account Titles

Debit

Credit

Vending Inventory

$ 540

Cash

$ 540

j. Room sales revenue during the month was $58,740; 98% cash and

2% credit cards receivable.

Account Titles

Debit

Credit

Cash

$ 57,565

Credit card receivables

1,175

Room Sales Revenue

$ 58,740

k. Vending sales revenue from vending machines was $880 cash.

Account Titles

Debit

Credit

Cash

$ 880

Vending Sales Revenue

$ 880

l. Wages of $3,120 cash were paid.

Account Titles

Debit

Credit

Wages Expense

$ 3,120

Cash

$ 3,120

m. Owner paid $3,200 cash on accounts payable.

Account Titles

Debit

Credit

Accounts Payable

$ 3,200

Cash

$ 3,200

n. Owner paid $4,200 annual casualty and liability insurance policy.

Account Titles

Debit

Credit

Prepaid Insurance

$ 4,200

Cash

$ 4,200

o. Owner paid $1,600 on the mortgage payable and interest of $1,728.

Account Titles

Debit

Credit

Mortgage Payable

$ 1,600

Interest Expense

1,728

Cash

$ 3,328

14

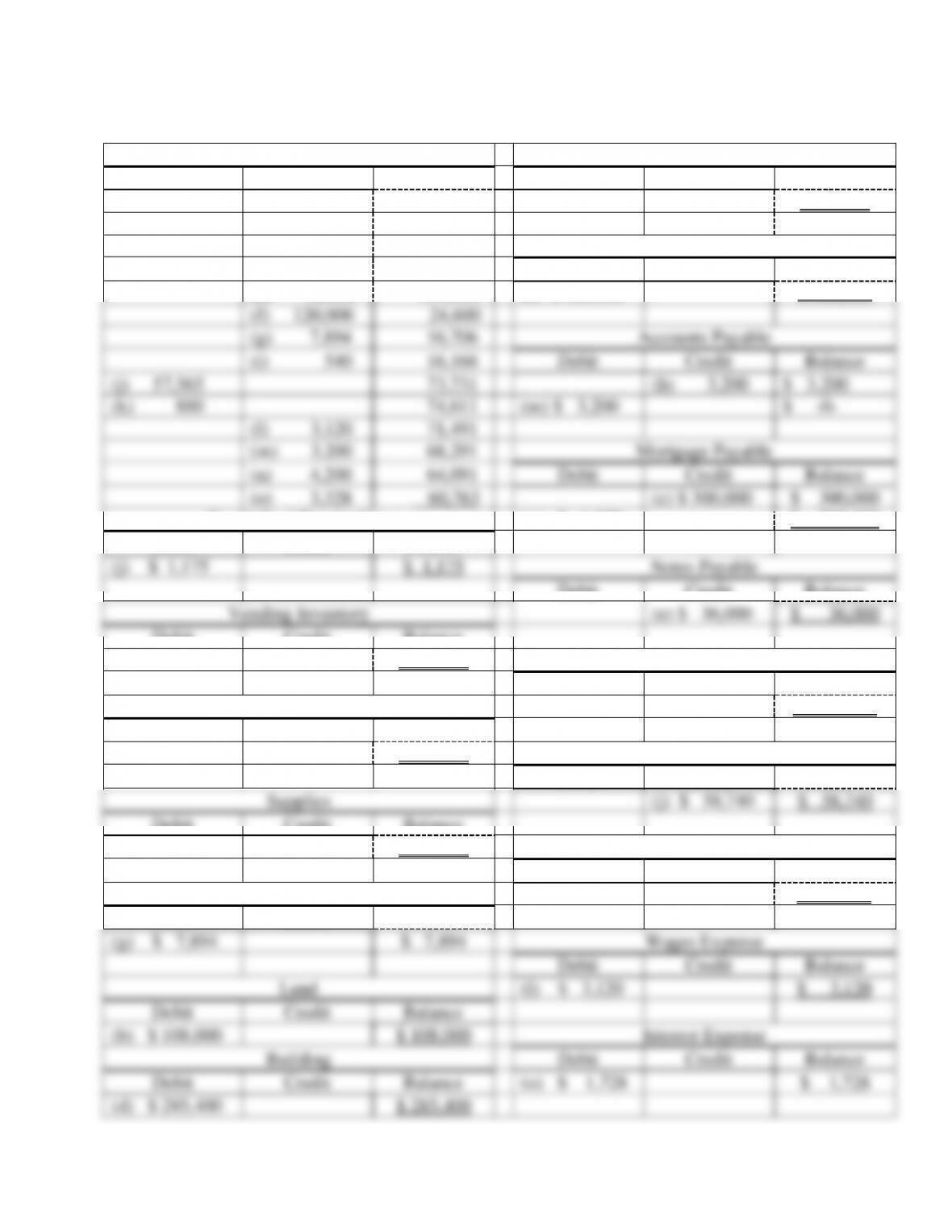

P1.3, Part 2: Solution, posting journal entries to the general ledger.

Cash

Equipment

Debit

Credit

Balance

Debit

Credit

Balance

(a) $250,000

$250,000

(e) $ 48,000

$ 48,000

(b) $ 108,000

142,000

(c) $300,000

442,000

Furnishings

(d) 285,400

156,600

Debit

Credit

Balance

(e) 12,000

144,600

(f) $ 120,000

$ 120,000

(f) 120,000

24,600

(g) 7,894

16,706

Accounts Payable

(i) 540

16,166

Debit

Credit

Balance

(j) 57,565

73,731

(h) 3,200

$ 3,200

(k) 880

74,611

(m) $ 3,200

$ -0-

(l) 3,120

71,491

(m) 3,200

68,291

Mortgage Payable

(n) 4,200

64,091

Debit

Credit

Balance

(o) 3,328

60,763

(c) $ 300,000

$ 300,000

Credit Card Receivables

(o) $ 1,600

$ 298,400

Debit

Credit

Balance

(j) $ 1,175

$ 1,175

Notes Payable

Debit

Credit

Balance

Vending Inventory

(e) $ 36,000

$ 36,000

Debit

Credit

Balance

(i) $ 540

$ 540

Capital (OE)

Debit

Credit

Balance

Prepaid Insurance

(a) $ 250,000

$ 250,000

Debit

Credit

Balance

(n) $ 4,200

$ 4,200

Room Sales Revenue

Debit

Credit

Balance

Supplies

(j) $ 58,740

$ 58,740

Debit

Credit

Balance

(h) $ 3,200

$ 3,200

Vending Sales Revenue

Debit

Credit

Balance

Linen Inventory

(k) $ 880

$ 880

Debit

Credit

Balance

(g) $ 7,894

$ 7,894

Wages Expense

Debit

Credit

Balance

Land

(l) $ 3,120

$ 3,120

Debit

Credit

Balance

(b) $ 108,000

$ 108,000

Interest Expense

Building

Debit

Credit

Balance

Debit

Credit

Balance

(o) $ 1,728

$ 1,728

(d) $ 285,400

$ 285,400

15

P1.3 Part 3: Solutions, Adjusting Journal Entries (separate entries for clarity).

1. The linen account balance is $7,894. Linen inventory on hand is $7,220.

$7,894 − $7,220 = $674 linen used.

Account Titles

Debit

Credit

Linen Expense

$ 674

Linen Inventory

$ 674

2. Wages earned by employees but unpaid is $416.

Account Titles

Debit

Credit

Wages Expense

$ 416

Wages Payable

$ 416

3. One month of prepaid insurance consumed ($4,200 /12) = $350

Account Titles

Debit

Credit

Insurance Expense

$ 350

Prepaid Insurance

$ 350

4. Accrued interest is 1% of note payable ($36,000 × 0.01) = $360

Account Titles

Debit

Credit

Interest Expense

$ 360

Interest Payable

$ 360

5. Equipment depreciation: ($48,000 − $3,000) / 120 mo. = $375

Account Titles

Debit

Credit

Depreciation Expense

$ 375

Accumulated Depreciation: Equipment

$ 375

6. Furnishings depreciation: ($120,000 − $7,000) / 96 mo. = $1,177

Account Titles

Debit

Credit

Depreciation Expense

$ 1,177

Accumulated Depreciation: Furnishings

$ 1,177

7. Building depreciation: ($285,400 − $42,000) / 240 mo. = $1,014

Account Titles

Debit

Credit

Depreciation Expense

$ 1,014

Accumulated Depreciation: Building

$ 1,014

Note: A compound depreciation expense entry will be used in the future.

Account Titles

Debit

Credit

Depreciation Expense

$ 2,566

Accumulated Depreciation: Equipment

$ 375

Accumulated Depreciation: Furnishings

1,177

Accumulated Depreciation: Building

1,014

9. Supplies used during the first month are $533.

Account Titles

Debit

Credit

Supplies Expense

$ 533

Supplies

$ 533

16

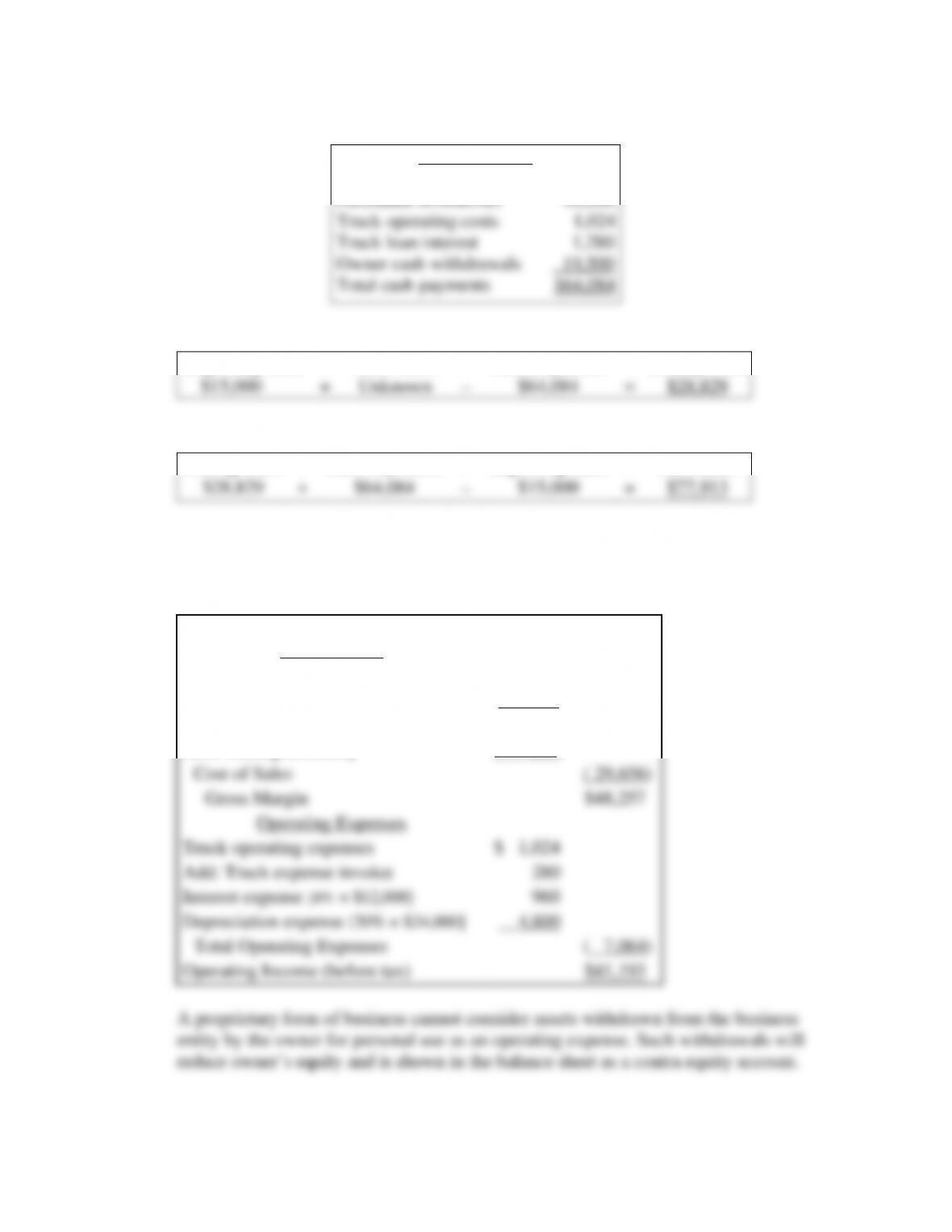

P1.4, Task 1: Find the total of cash payments, which are stated in the problem:

Cash Payments

Purchased truck

$ 12,000

Purchased inventories

30,280

Truck operating costs

1,024

Truck loan interest

1,280

Owner cash withdrawals

19,500

Total cash payments

$64,084

Task 2: Set up the known information in a linear statement

Beginning Cash

+

Cash Sales?

−

Cash Payments

=

Ending Cash

$15,000

+

Unknown

−

$64,084

=

$28,829

Task 3: Find the missing cash sales by reversing the linear additive functions.

Ending Cash

+

Cash Payments

−

Beginning Cash

=

Cash Sales

$28,829

+

$64,084

−

$15,000

=

$77,913

Task 4: Complete an Accrual Income Statement.

Fast Snacks

Income Statement

For the Year Ended 12-31-2006

Sales Revenue

$77,913

Cost of Sales:

Beginning Inventory

– 0 –

Purchases

$30,280

Goods Available for sale

$30,280

Less: Ending Inventory

( 624)

Cost of Sales

( 29,656)

Gross Margin

$48,257

Operating Expenses

Truck operating expenses

$ 1,024

Add: Truck expense invoice

280

Interest expense [8% × $12,000]

960

Depreciation expense [20% × $24,000]

4,800

Total Operating Expenses

( 7,064)

Operating Income (before tax)

$41,193

A proprietary form of business cannot consider assets withdrawn from the business

entity by the owner for personal use as an operating expense. Such withdrawals will

reduce owner’s equity and is shown in the balance sheet as a contra equity account.

17

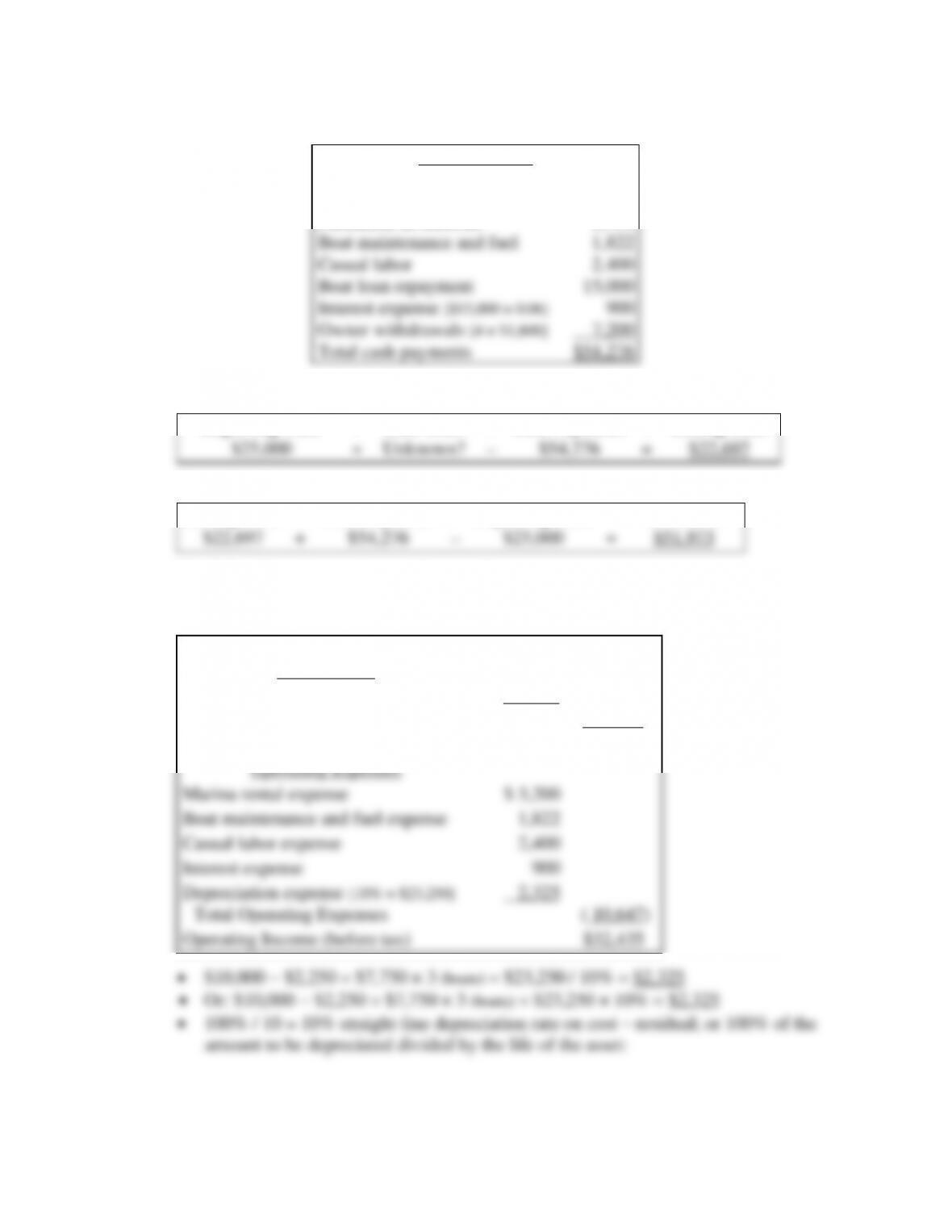

P1.5, Task 1: Find total cash payments, which are stated in the problem.

Cash Payments

Marina rental [4 × $800]

$ 3,200

3,200

New boats [3 x $5,000]

15,000

Purchased inventories

8,754

Boat maintenance and fuel

1,822

Casual labor

2,400

Boat loan repayment

15,000

Interest expense [$15,000 × 0.06]

900

Owner withdrawals [4 × $1,800]

7,200

Total cash payments

$54,276

Task 2: Set up the known information in a linear statement

Beginning Cash

+

Cash Sales

−

Cash Payments

=

Ending Cash

$25,000

+

Unknown?

−

$54,276

=

$22,697

Task 3: Find the missing cash sales by reversing the additive functions.

Ending Cash

+

Cash Payments

−

Beginning Cash

=

Cash Sales

$22,697

+

$54,276

−

$25,000

=

$51,973

Task 4: Complete an Accrual Income Statement.

Income Statement

For the Period Ending 09-15-2006

Sales Revenue

$ 51,973

Cost of Sales

Purchases [$8,754 + $137 invoice]

$ 8,891

Cost of Sales

( 8,891)

Gross Margin

$ 43,082

Operating Expenses

Marina rental expense

$ 3,200

Boat maintenance and fuel expense

1,822

Casual labor expense

2,400

Interest expense

900

Depreciation expense [10% × $23,250]

2,325

Total Operating Expenses

( 10,647)

Operating Income (before tax)

$32,435

• $10,000 − $2,250 = $7,750 × 3 (boats) = $23,250 / 10% = $2,325

• Or: $10,000 − $2,250 = $7,750 × 3 (boats) = $23,250 × 10% = $2,325

• 100% / 10 = 10% straight-line depreciation rate on cost – residual; or 100% of the

amount to be depreciated divided by the life of the asset:

18

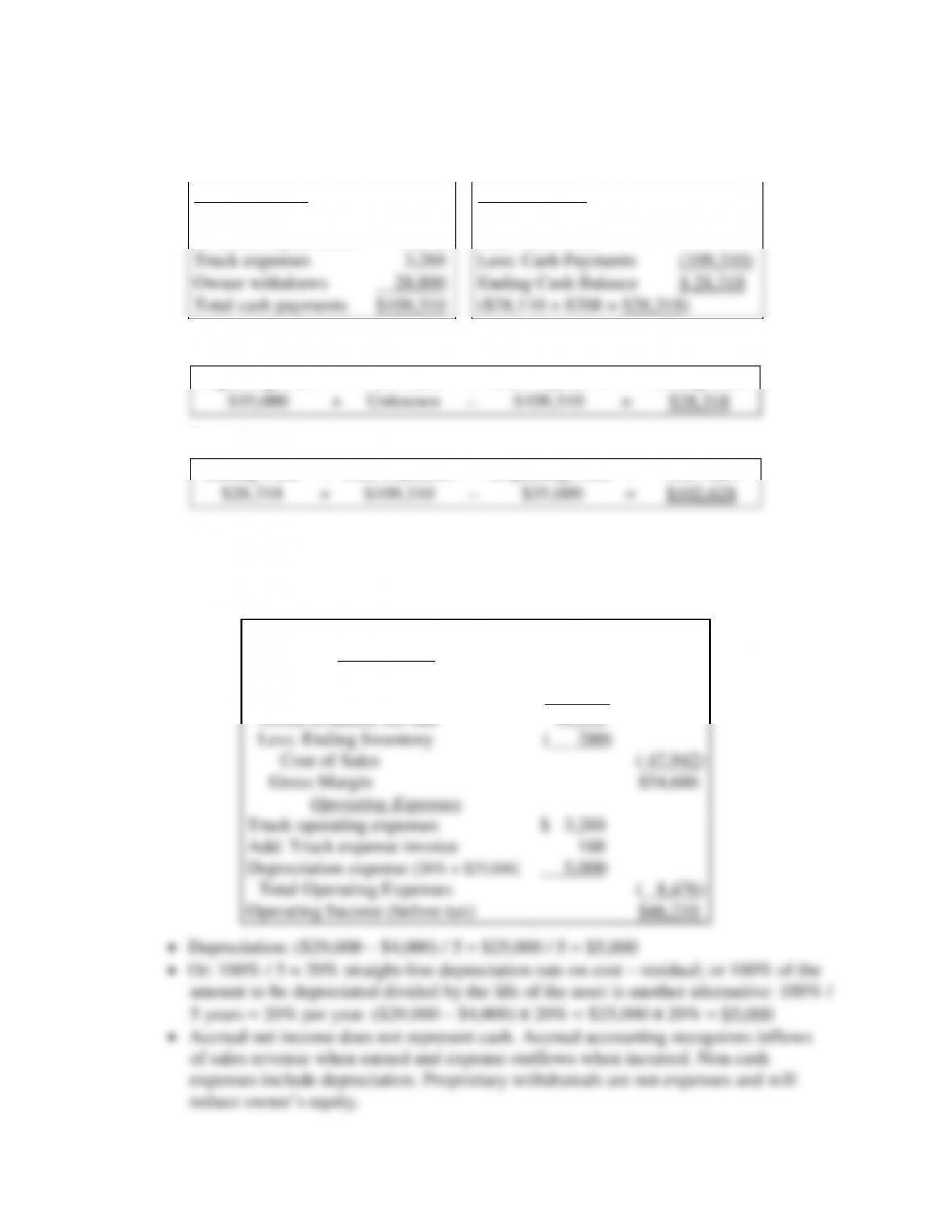

CASE 1 SOLUTION

Task 1: The missing cash sales represent Sales Revenue.

Cash Payments

Reconciliation

Purchased truck

$ 29,000

Beginning Cash Balance

$ 35,000

Inventories purchased

48,222

Add: Cash Sales

Unknown

Truck expenses

3,288

Less: Cash Payments

(109,310)

Owner withdraws

28,800

Ending Cash Balance

$ 28,318

Total cash payments

$109,310

($28,110 + $208 = $28,318)

Task 2: Set up the known information in a linear statement.

Beginning Cash

+

Cash Sales

−

Cash Payments

=

Ending Cash

$35,000

+

Unknown

−

$109,310

=

$28,318

Task 3: Find the missing cash sales by reversing the linear additive functions.

Ending Cash

+

Cash Payments

−

Beginning Cash

=

Cash Sales

$28,318

+

$109,310

−

$35,000

=

$102,628

Task 4: Complete an Accrual Income Statement.

3C Company

Income Statement

For the Year Ended 12-31-2005

Sales revenue

$102,628

Cost of Sales

Beginning inventory

– 0 –

Purchases

$48,222

Goods available for sale

48,222

Less: Ending Inventory

( 280)

Cost of Sales

( 47,942)

Gross Margin

$54,686

Operating Expenses

Truck operating expenses

$ 3,288

Add: Truck expense invoice

188

Depreciation expense [20% × $25,000]

_ 5,000

Total Operating Expenses

( 8,476)

Operating Income (before tax)

$46,210

• Depreciation: ($29,000 – $4,000) / 5 = $25,000 / 5 = $5,000

• Or: 100% / 5 = 20% straight-line depreciation rate on cost – residual; or 100% of the

amount to be depreciated divided by the life of the asset is another alternative: 100% /

5 years = 20% per year. ($29,000 – $4,000) x 20% = $25,000 x 20% = $5,000

• Accrual net income does not represent cash. Accrual accounting recognizes inflows

of sales revenue when earned and expense outflows when incurred. Non-cash

expenses include depreciation. Proprietary withdrawals are not expenses and will

reduce owner’s equity.