Valuation

Measuring and Managing the Value of Companies

5th Edition

Chapter 25 Solutions

Taxes

Version 1.0

April 1, 2010

Chapter 25

Question 1

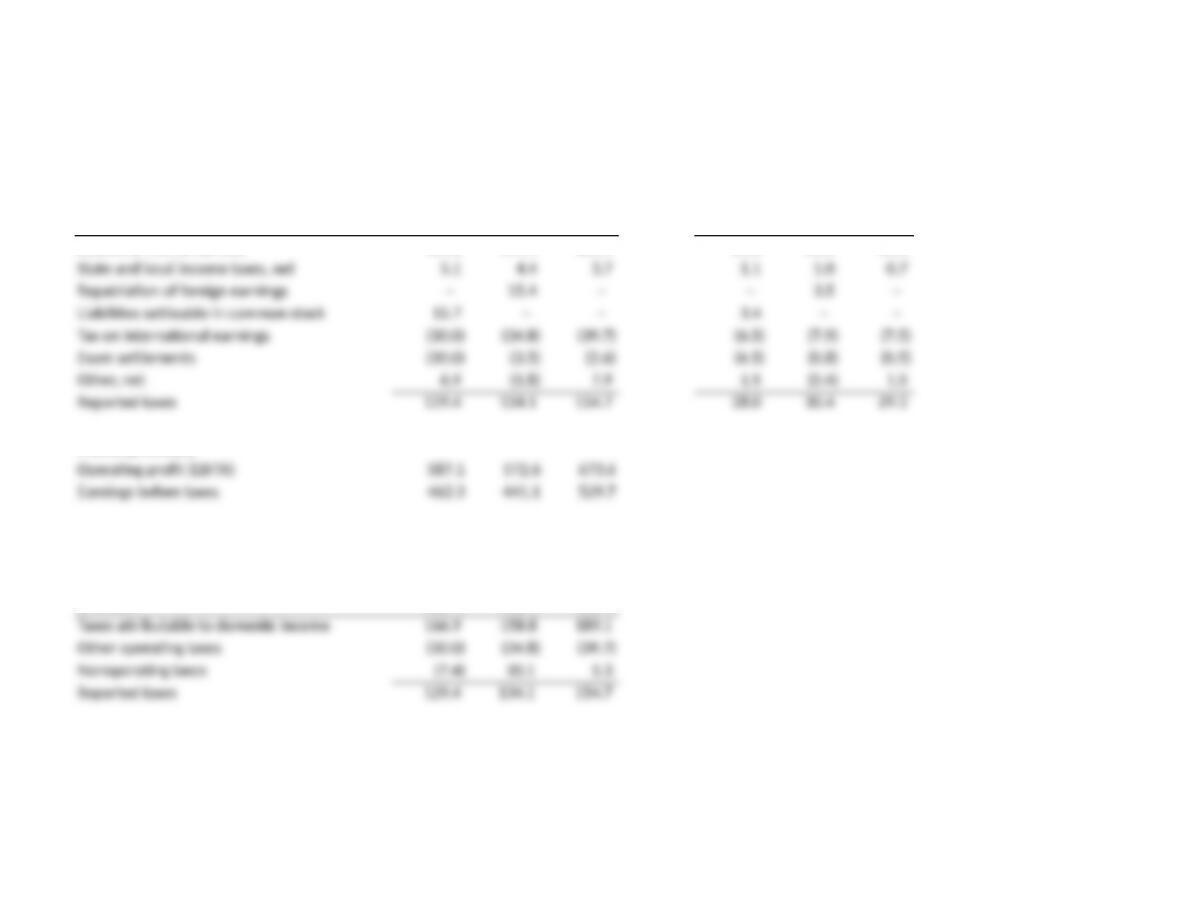

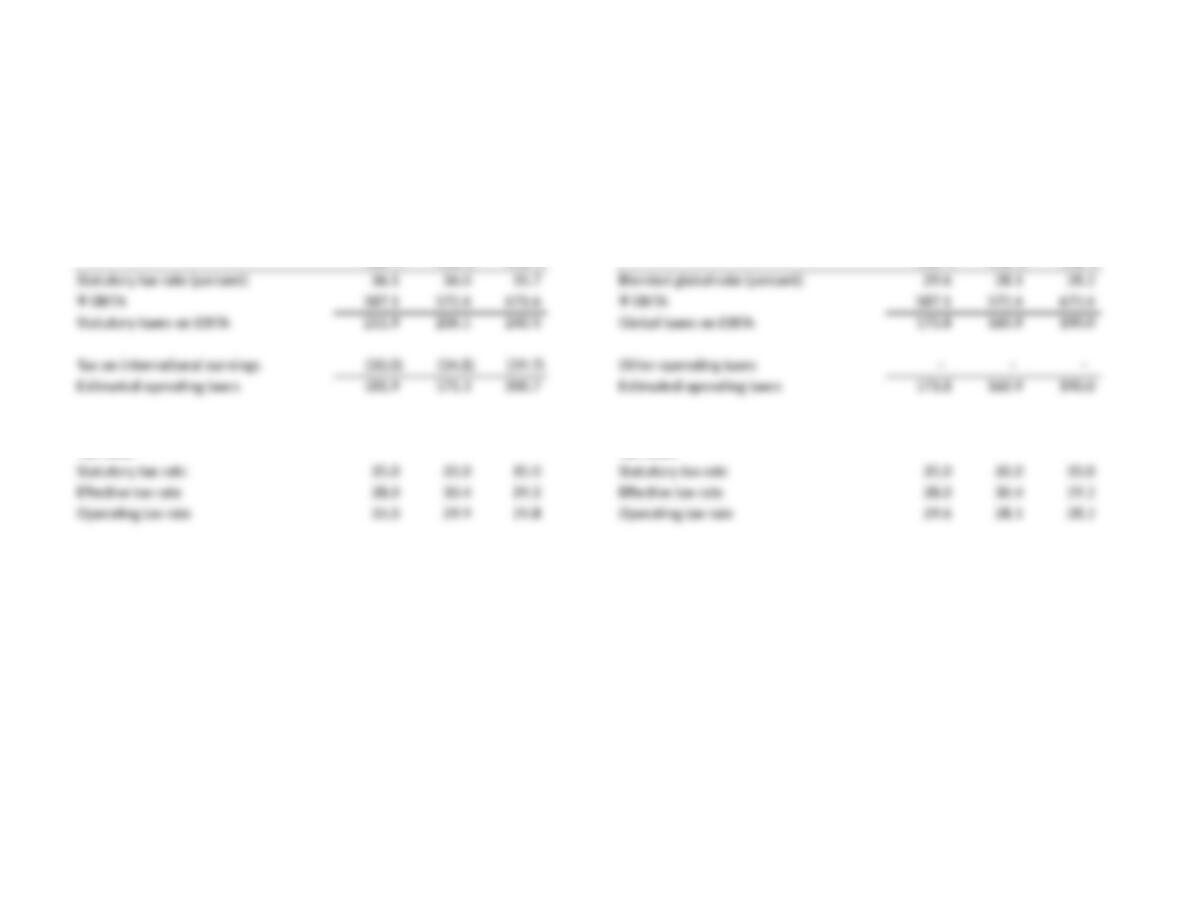

Tax reconciliation table in $ millions Tax reconciliation table in percent

$ million Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Statutory income tax rate 161.8 154.4 185.4 35.0 35.0 35.0

Protits ($ million)

Tax reconciliation table in $ millions

$ million Year 1 Year 2 Year 3

Chapter 25

Question 2

Panel A Panel B

Assumption: Nonoperating items recognized domestically Assumption: Nonoperating items recognized globally

Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Tax rates Tax rates

Chapter 25

Question 3

Companies can avoid high domestic tax rates by maintaining earnings in foreign countries inde2nitely. For some companies,

this has led to large cash balances abroad. For instance, Oracle Corporation held 89 percent of its $11.3 billion in cash and

the company pay the difference between local and foreign taxes. But will it? In 2004, the United States passed a temporary

For companies that repatriate in a given year, we do not recommend treating the repatriation as operating. This will distort

the ongoing tax rate for use in performance appraisal and forecasting. If you decide to treat the repatriation as operating, the

tax should be spread over the years incurred.

equivalents overseas of 2009, according to the Wall Street Journal. If a company repatriates earnings, tax law requires that

Losses and tax credit carry-forwards Tax rates

Nonoperating deferred tax liabilities

Check

Chapter 25

Question 5

ToyCo

Total funds invested

Chapter 25

Question 6

When companies grow, they add fixed assets. By using accelerated depreciation on the tax books for new assets, companies can defer taxes.

These deferrals are likely to be highest when organic growth is high. As growth falls and new equipment merely replaces old equipment,

deferrals will drop. In fact, cash taxes can be higher than reported taxes when growth is negative. The company may not pay this higher

rate, however, as shrinking companies oHen generate losses and consequently do not pay taxes.

percent

Year 1 Year 2 Year 3

EXHIBIT 25.9 ToyCo: Tax Reconciliation Table

$ million

Year 1 Year 2 Year 3

Deferred tax assets

Deferred tax liabilities

EXHIBIT 25.10 ToyCo: Deferred Tax Assets and Liabilities