Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

Valuation

Henkel AG versus Reckitt Benckiser plc

Professor David Wessels © 2010

The Wharton School of the University of Pennsylvania

3620 Locust Walk, Philadelphia, PA 19104

Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

Presentation Overview

• Understanding a company’s past is essential to forecasting its future. For that

reason, we start with an in-depth analysis of historical operating performance.

•For Henkel AG, the company struggles to compete against its European

Household and Personal Care (HPC) counterparts, and specifically Reckitt

Benckiser plc. Henkel lags Reckitt Benckiser in each of the key value drivers:

organic revenue growth, operating margin, capital turnover, and financial

flexibility.

• Part of Henkel’s underperformance can be attributed to the economic

downturn and its reliance on its Adhesives segment, which is highly cyclical.

Yet even controlling for segment performance, Henkel still remains well

below best practices. This presentation examines each component in detail.

Valuation: Measuring and Managing the Value of Companies 2

Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

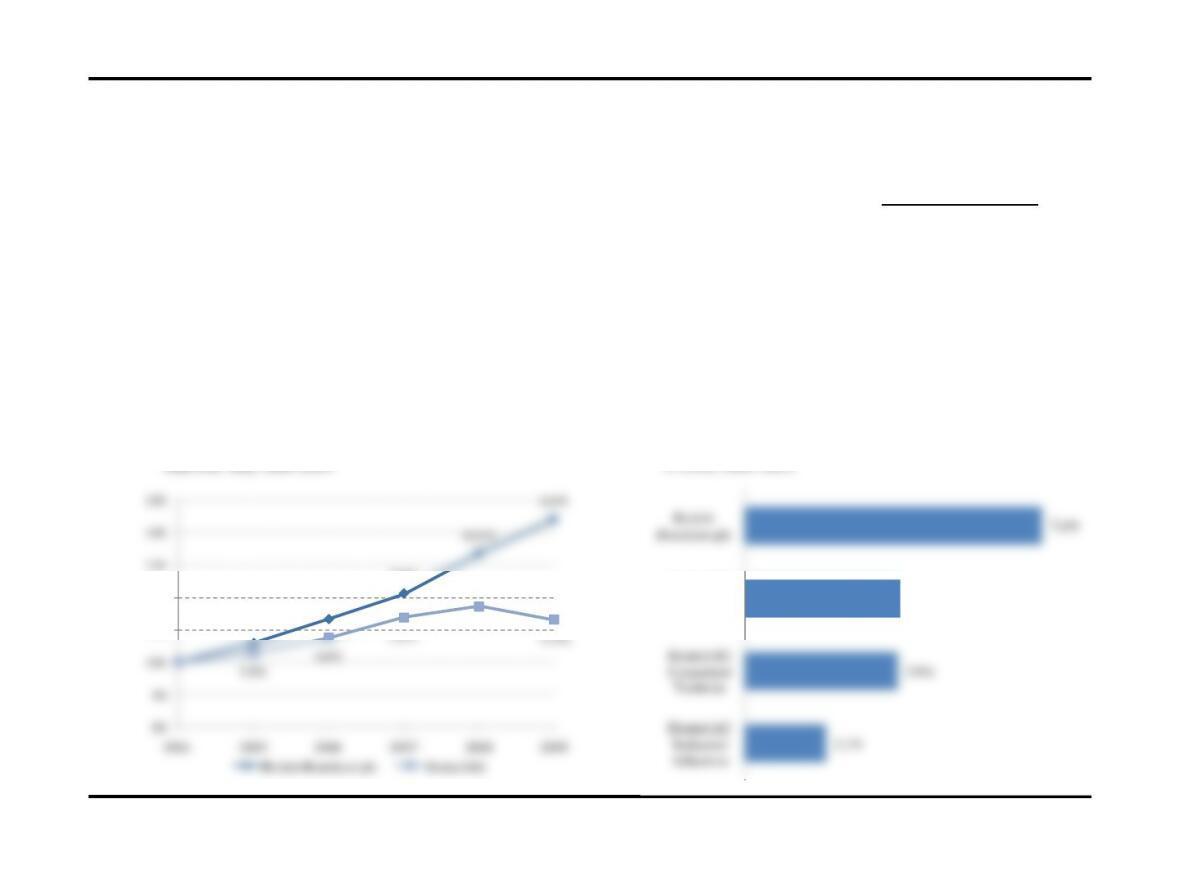

Revenue Growth

•Between 2005 and 2009, Reckitt Benckiser has outgrown Henkel AG each and every

year. Reckitt Benckiser even managed to record 8.0 percent organic revenue growth

during the global recession of 2009, as compared to Henkel’s negative 3.5 percent

growth.

• Henkel’s low organic growth is not caused by any particularly poor-performing segment.

Each division is growing at roughly the same rate.

4.0%

7.6%

Henkel AG

Henkel AG

Laundry &

Home Care

Reckitt

Benckiser plc

Organic Revenue Growth

CAGR, 2005-2009

6.0%

7.0%

7.0%

10.0%

8.0%

4.6%

5.8%

3.0%

-3.5%

110

120

130

140

150

Organic Revenue Growth

Year over Year, 2005-2009

Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

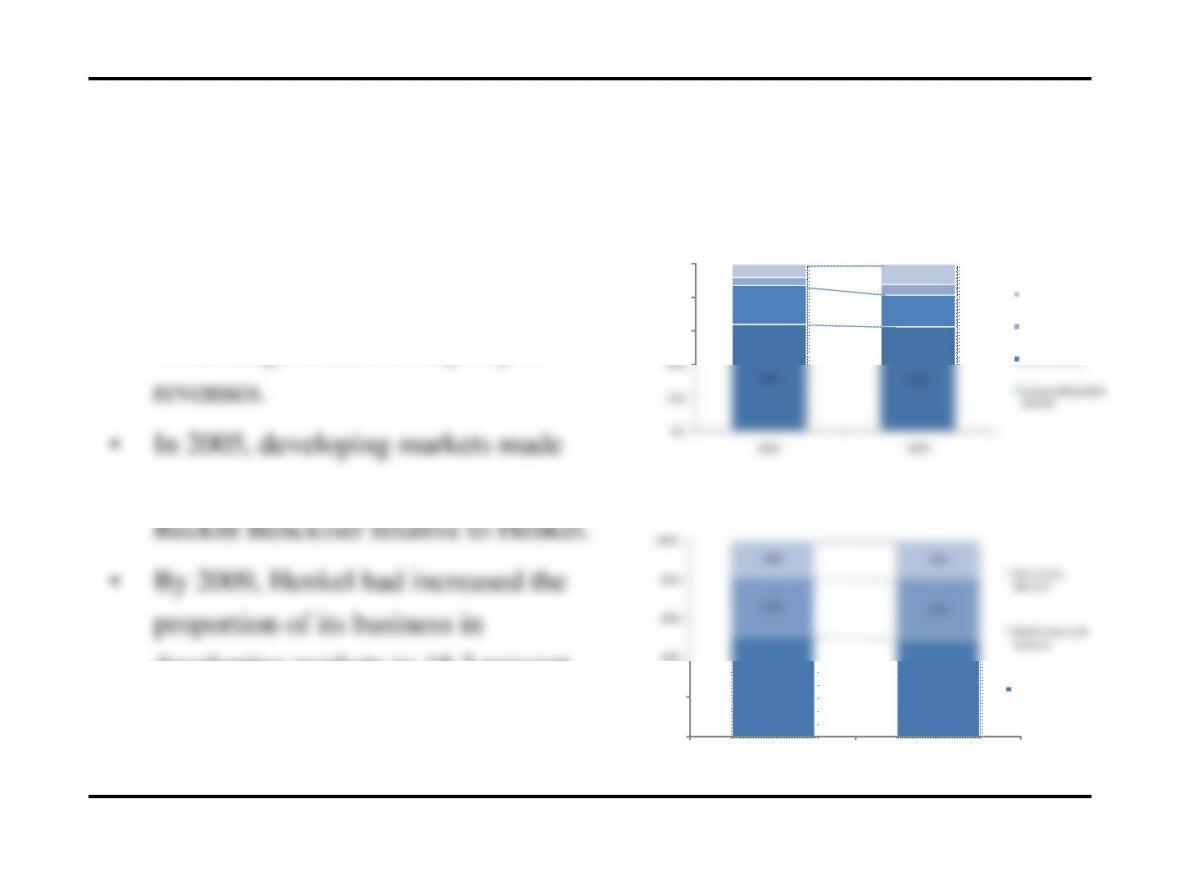

Revenues by Geography

•For both Henkel and Reckitt

Benckiser, Europe and North

America generate the majority of

up a larger portion of revenues for

developing markets to 18.3 percent,

Valuation: Measuring and Managing the Value of Companies 4

64%

62%

23%

19%

40%

60%

80%

100%

Henkel Revenue by Geography

Asia-Pacific

Latin America

North America

Europe/Africa/Mid

51%

49%

20%

40%

Reckitt Benckiser Revenue by Segment

Australia

Europe

Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

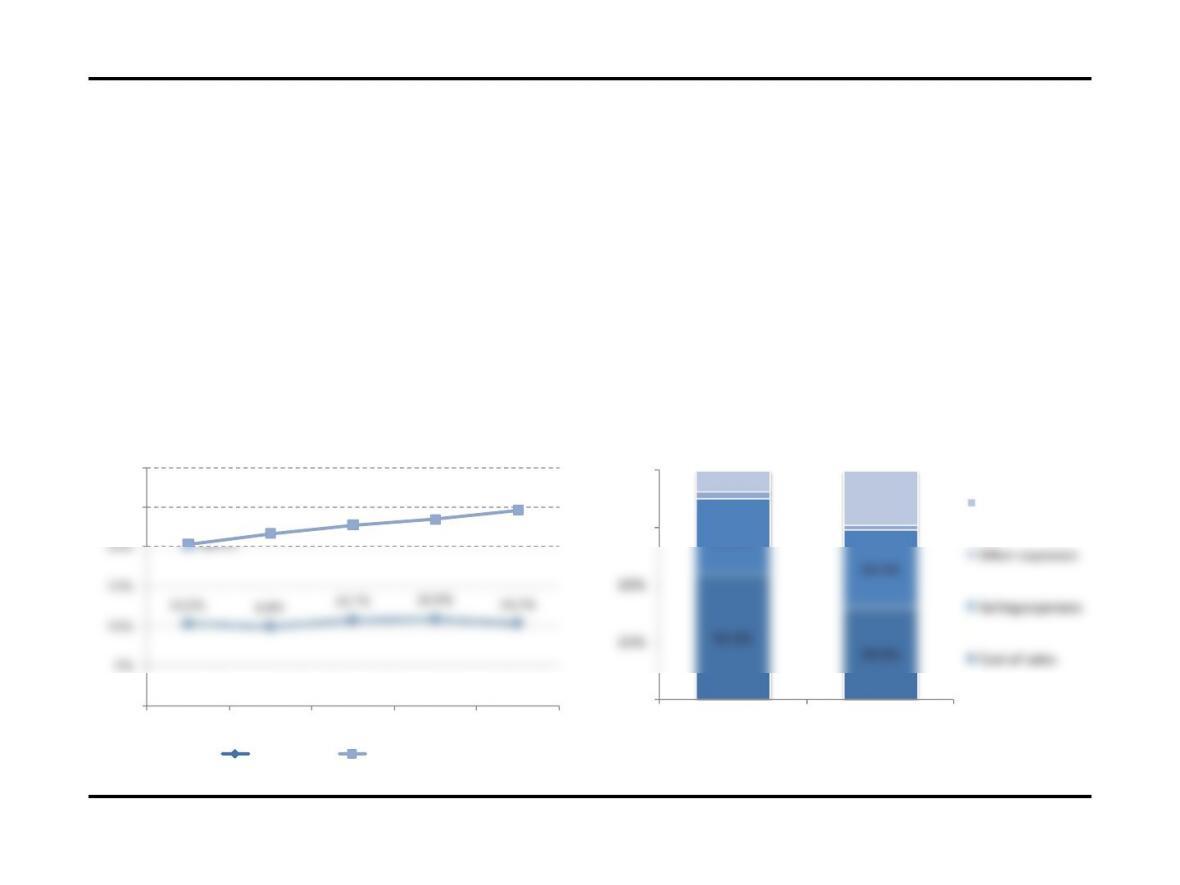

Operating Margins

•Reckitt Benckiser has consistently generated a higher operating margin than Henkel, and

this difference has expanded over the past five years. The company’s higher margins are a

result of its lower costs of sales, likely caused by higher prices from the company’s

premium products.

Valuation: Measuring and Managing the Value of Companies 5

54.1%

39.8%

33.8%

34.4%

9.3%

24.2%

25%

50%

75%

100%

Henkel AG

Reckitt Benckiser

Henkel AG versus Reckitt Benckiser plc

Breakdown of Revenue, 2009

Operating margin

Other expenses

Selling expenses

Cost of sales

10.2%

9.9%

10.7%

10.9%

10.3%

20.3%

21.7%

22.8%

23.5%

24.7%

5%

10%

15%

20%

25%

30%

2005

2006

2007

2008

2009

Henkel AG versus Reckitt Benckiser plc

EBITA (% of revenues), 2005–2009

Henkel AG

Reckitt Benckiser plc

Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

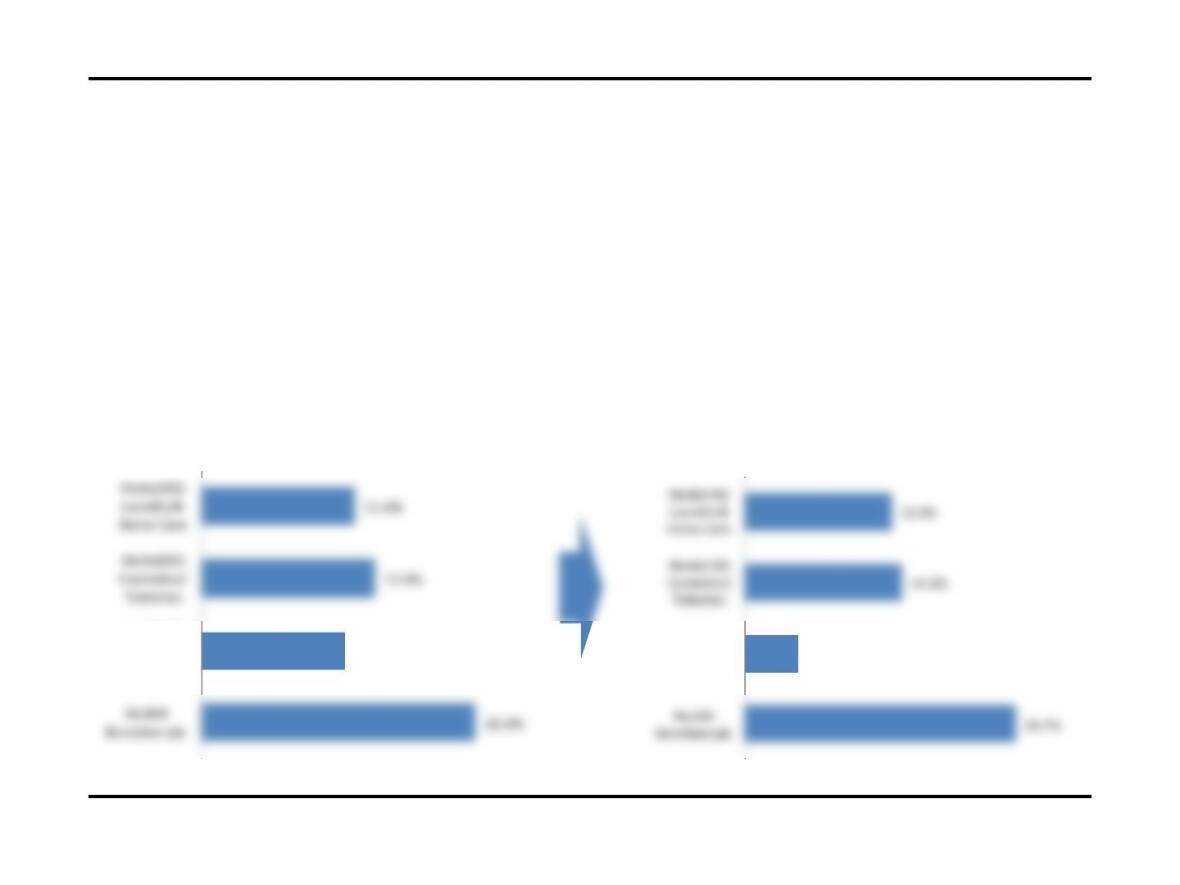

Margins by Segment

• Examining operating margins, and treating Reckitt Benckiser as a “pure play” relative to

Henkel’s individual segments, Reckitt Benckiser is more profitable than each of

Henkel’s segments. Operating margins expanded (somewhat) for Henkel’s

Cosmetics/Toiletries and Laundry/Home Care businesses, but fell for the Industrial

Adhesives business.

11.4%

12.9%

10.6%

20.3%

Henkel AG

Laundry &

Home Care

Henkel AG

Cosmetics/

Toiletries

Henkel AG

Industrial

Adhesives

Benckiser plc

Henkel AG versus Reckitt Benckiser plc

Operating margin (EBITA), 2005

13.4%

14.3%

4.8%

24.7%

Henkel AG

Laundry &

Home Care

Henkel AG

Cosmetics/

Toiletries

Henkel AG

Industrial

Adhesives

Benckiser plc

Henkel AG versus Reckitt Benckiser plc

Operating margin (EBITA,) 2009

Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

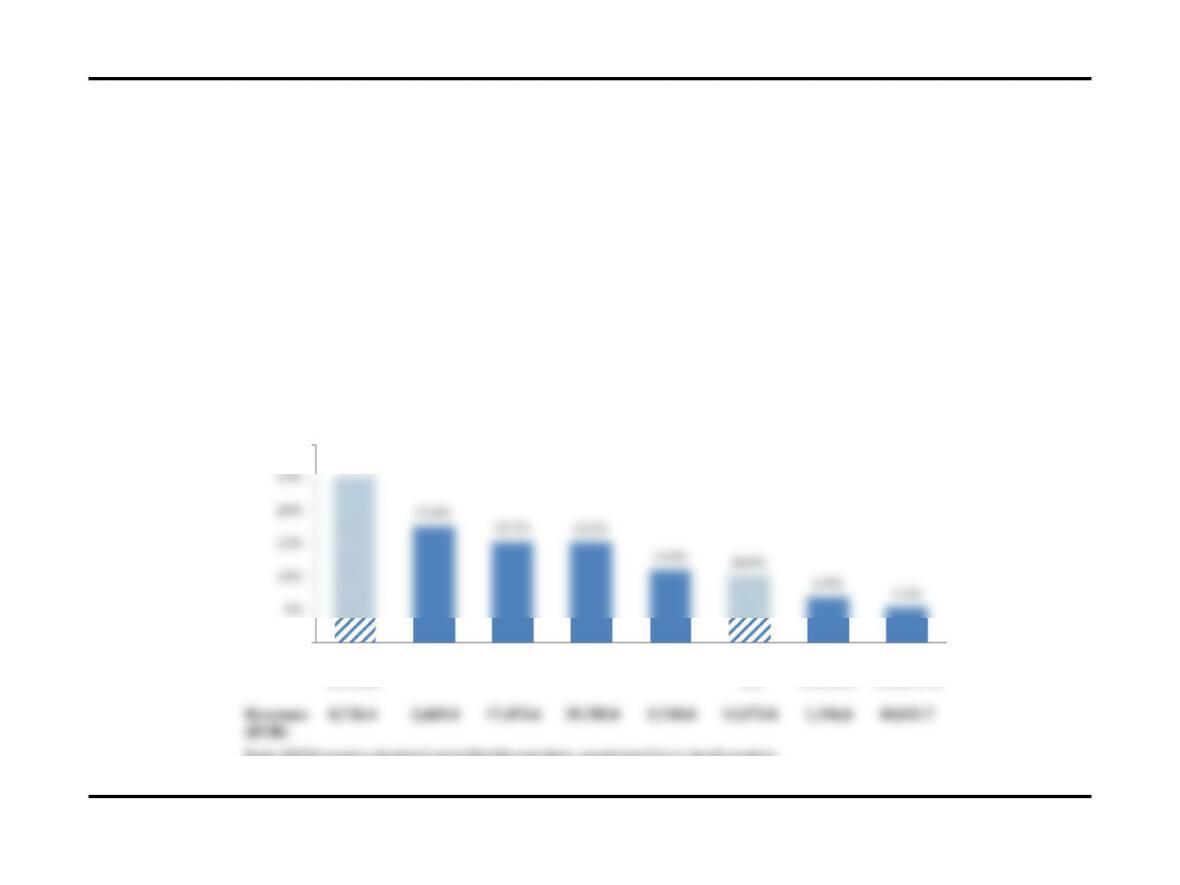

Industry Margins

•Across the European household and personal care industry (European HPC), Reckitt

Benckiser is the clear leader in operating margins. Henkel ranks near the bottom within

the industry, and the company reports slightly lower operating margins than its domestic

competitor, Beiersdorf AG.

Valuation: Measuring and Managing the Value of Companies 7

25.1%

17.6%

15.3%

15.2%

11.0%

10.0%

6.9%

5.4%

0%

5%

10%

15%

20%

25%

30%

Reckitt

Benckiser

Givaudan Sa

L’Oreal Sa

Unilever Plc

Beiersdorf Ag

Henkel Ag

And

Oriflame

Cosmetics

Svenska

Cellulosa Ab

European Household and Personal Care

Operating margin (EBITA), 2009

Revenues 8,726.4 2,669.4 17,472.6 39,785.8 5,748.0 13,573.0 1,316.6 10,821.7

(EUR)

Note: EBITA margin calculated using Worldscope data, unadjusted for in-depth analysis

Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

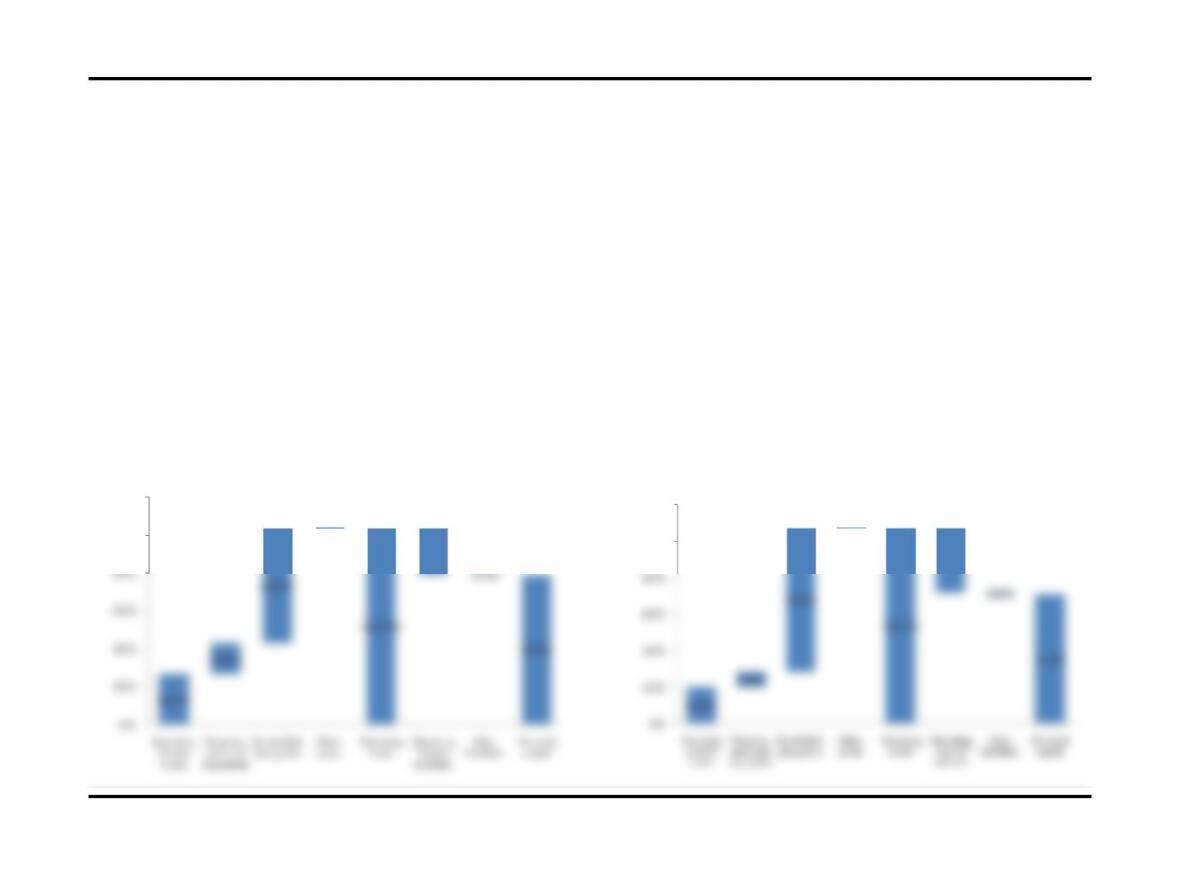

Invested Capital Breakdown

•As a percentage of sales, Henkel and Reckitt Benckiser have a very similar amount of

operating current assets, operating assets, and invested capital.

•The primary difference in capital occurs because of property, plant, and equipment

(PP&E), acquired intangibles, and operating current liabilities. Henkel carries more

PP&E and Reckitt Benckiser carries more acquired intangibles and operating current

liabilities.

Valuation: Measuring and Managing the Value of Companies 8

26.3%

16.6%

60.5%

0.1%

103.5%

24.4%

0.1%

79.0%

20%

40%

60%

80%

100%

120%

Operating

current

assets

Property,

plant and

equipment

Goodwill &

intangibles

Other

assets

Operating

assets

Operating

current

liabilities

Other

liabilities

Invested

capital

Henkel AG

Percent of sales, 2009

20.2%

8.2%

78.6%

0.3%

107.3%

35.6%

0.8%

71.0%

20%

40%

60%

80%

100%

120%

Operating

current

assets

Property,

plant and

equipment

Goodwill &

intangibles

Other

assets

Operating

assets

Operating

current

liabilities

Other

liabilities

Invested

capital

Reckitt Benckiser plc

Percent of sales, 2009

Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

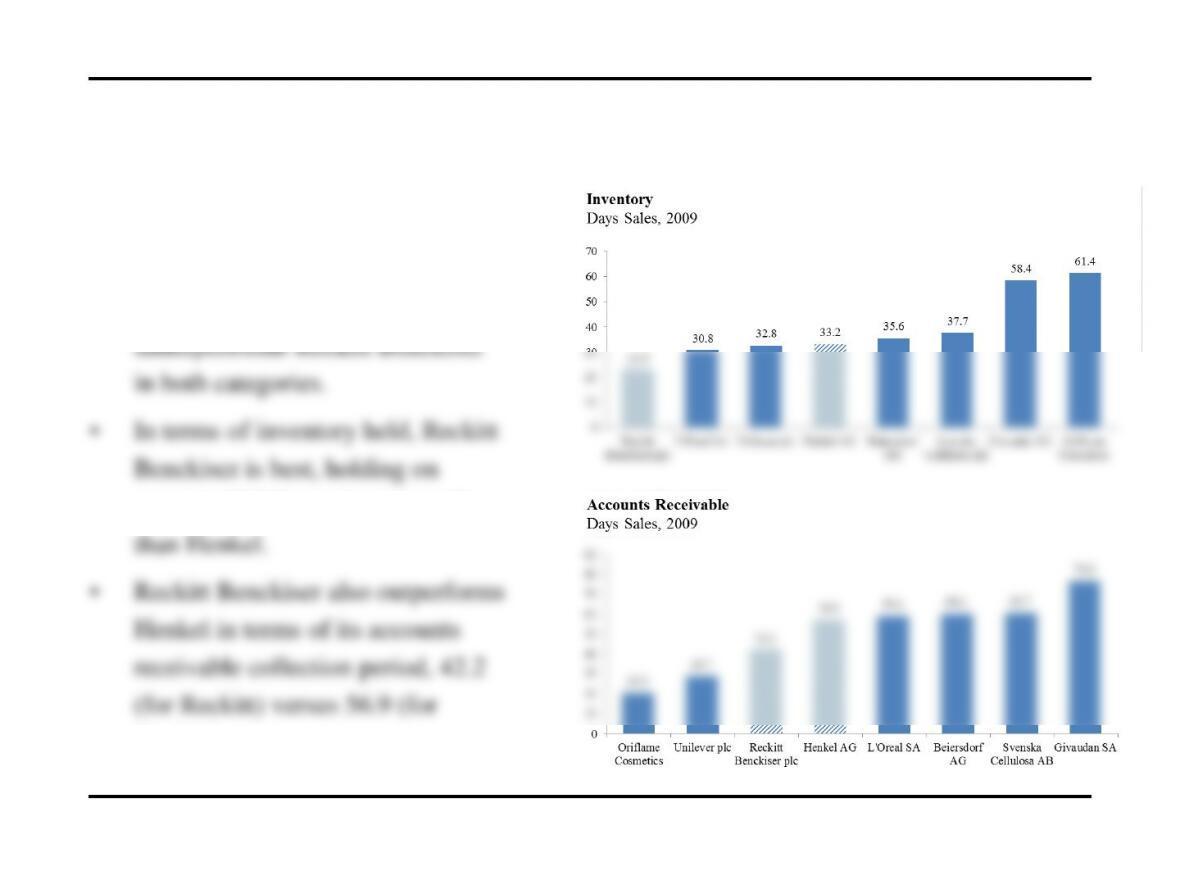

•Henkel holds inventory and

accounts receivable in line with the

European HPC industry, but

average 10.3 fewer inventory days

Henkel).

Inventory and Accounts Receivable

Valuation: Measuring and Managing the Value of Companies 9

Integrative Case: Henkel AG Competitive Benchmarking of Henkel AG

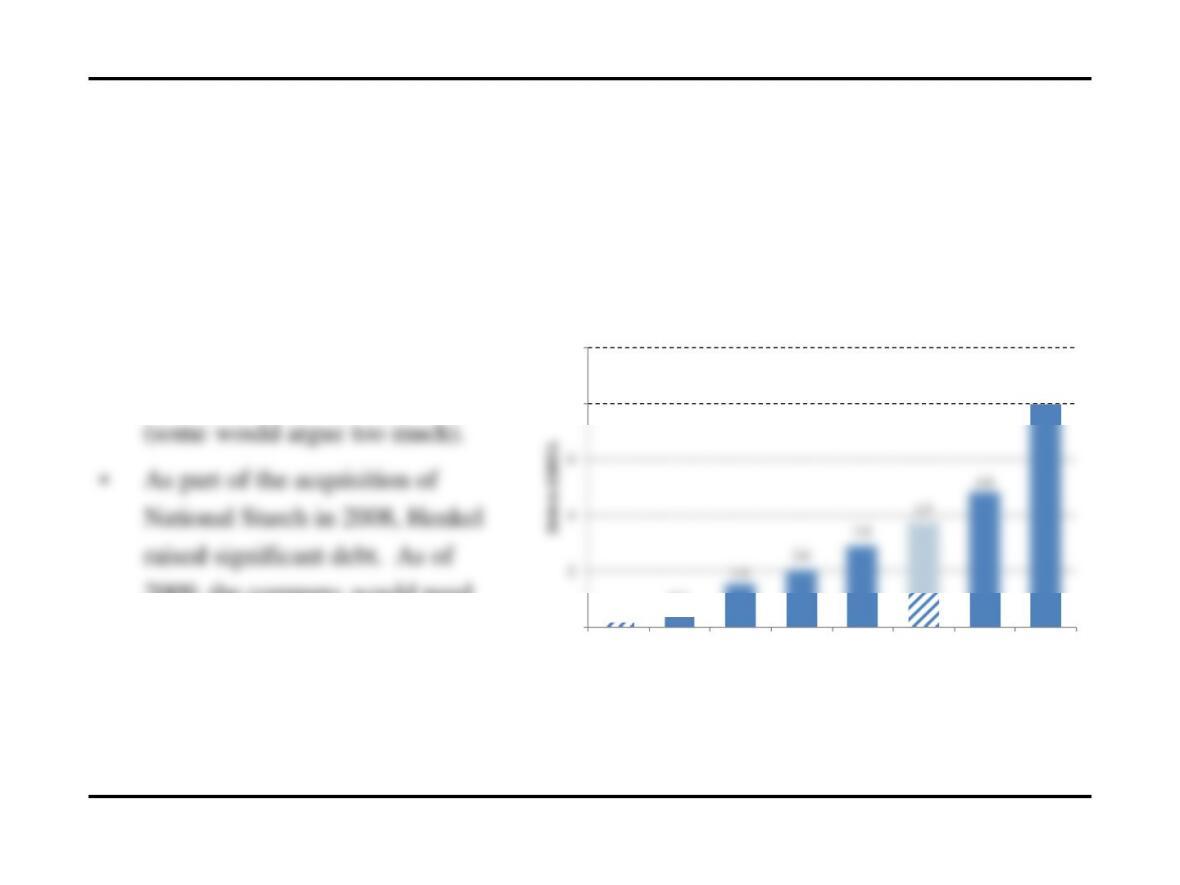

Financial Health: Debt to EBITA

Valuation: Measuring and Managing the Value of Companies 10

•In addition to generating

industry best operating margins,

Reckitt Benckiser has

tremendous financial flexibility

2009, the company would need

3.7 years of EBITA to pay down

debt.

0.2

0.4

1.6

8.0

0

2

8

10

Reckitt

Benckiser

plc

Beiersdorf

AG

L’Oreal

SA

Unilever

plc

Oriflame

Cosmetics

Henkel

AG

Givaudan

SA

Svenska

Cellulosa

AB

European Household & Personal Care

Debt–to-EBITA, 2009