Valuation

Measuring and Managing the Value of Companies

5th Edition

Chapter 7 Solutions

Reorganizing the Financial Statements

Version 1.0

April 1, 2010

Chapter 7

Questions 1-3

Ratio Company A Company B Company C

Return on assets 14.3% 13.0% 11.4%

Return on equity 15.8% 14.3% 21.8%

Return on invested capital 15.8% 15.8% 15.8%

Question 1

Return on invested capital best measures operating performance. All three companies have the same operating performance!

Question 2

Companies that hold less than 20% of another company (or subsidiary) only record income when dividends are paid. Therefore,

profits will be under reported. This causes return on assets to be distorted downwards. Since Company B

has $50 million in equity investments, but no corresponding income, its ROA is lower than Company A.

Question 3

Company C’s return on equity outpaces both Company A and Company B because the company uses leverage. Leverage

will magnify operating results. Leverage makes good results look great, but can bankrupt companies with poor performance.

Chapter 7

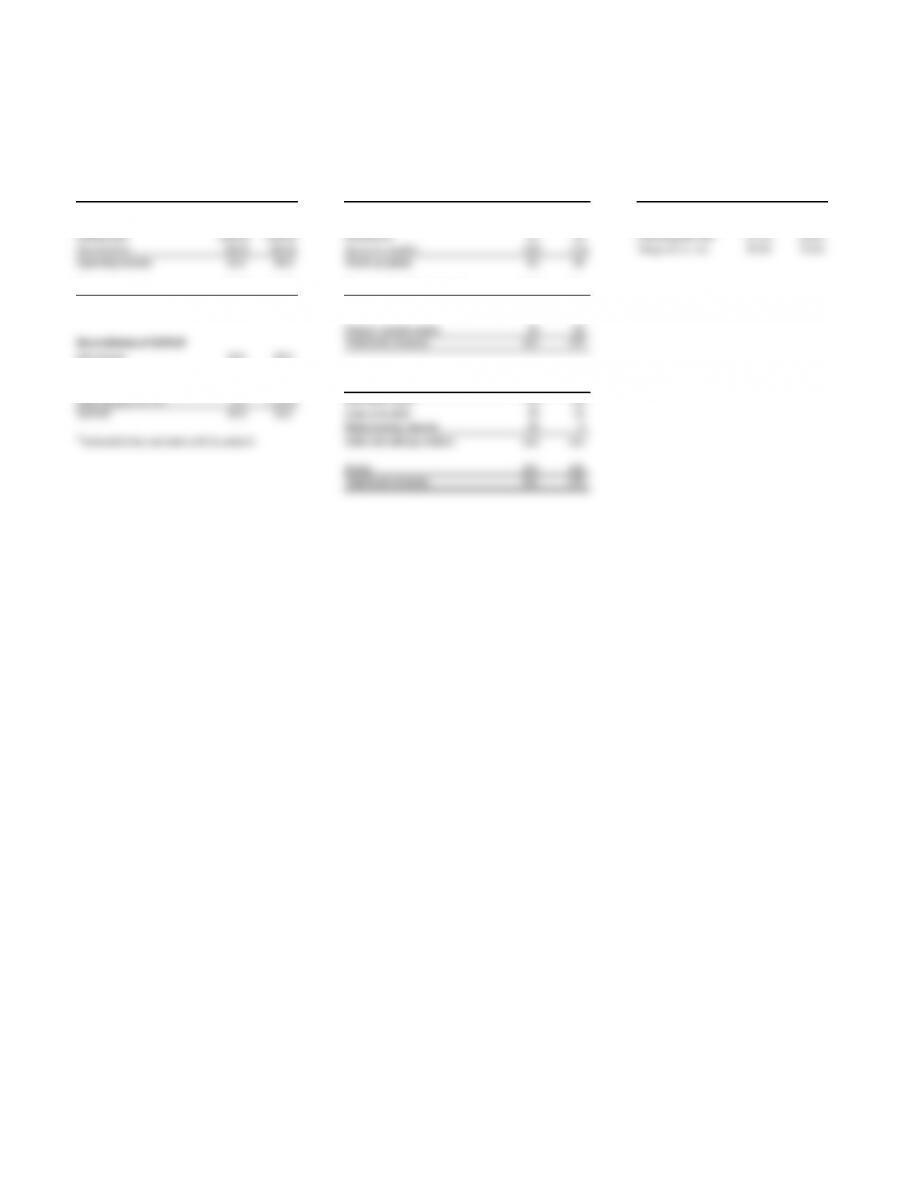

Question 4

HealthCo HealthCo

Reorganized financial statements Ratio Analysis

Prior Current Prior Current Prior Current

NOPLAT Year Year Total funds invested Year Year Ratio Year Year

Revenues 605.0 665.0 Working cash 5 5 ROIC 15.5% 19.5%

Cost of sales (200.0) (210.0) Accounts receivable 45 55

Selling costs (300.0) (320.0) Inventories 15 20 Operating tax rate 27.3% 29.4%

Depreciation (40.0) (45.0) Accounts payable (10) (15) Marginal tax rate 35.0% 35.0%

Operating income 65.0 90.0 Working capital 55 65

Operating taxes (17.8) (26.5) Property, plant & equipment 250 260

NOPLAT 47.3 63.5 Invested capital 305 325

Prepaid pension assets 10 50

Reconciliation of NOPLAT Total funds invested 315 375

Net income 44.0 60.0

Tax audit10.0 0.0

After-tax interest expense 3.3 9.8 Reconciliation of total funds invested

After-tax gain on sale 0.0 (16.3) Short-term debt 20 40

NOPLAT 47.3 53.5 Long-term debt 70 70

Restructuring reserves 20 0

1 Included to be consistent with Question 6 Debt and debt equivalents 110 110

Equity 205 265

Total funds invested 315 375

Chapter 7

Question 5

HealthCo HealthCo

Cash flow available to investors

Reconciliation of cash flow available to investors

Current Current

year year

Revenues 665.0 After-tax interest expense 9.8

Cost of sales (210.0) Decrease in short-term debt (20.0)

Selling costs (320.0) Decrease in long-term debt 0.0

Depreciation (45.0) Restructuring reserves 20.0

Operating income 90.0 9.8

Operating taxes (26.5) Dividends 0

NOPLAT 63.5 Cash flow available to investors 9.8

Depreciation 45.0

Gross cash flow 108.5

Increase in working capital (10.0)

Capital expenditures (55.0)

Free cash flow 43.5

Prepaid pension assets (40.0)

After-tax gain on sale 16.3

Cash flow available to investors 19.8

Chapter 7

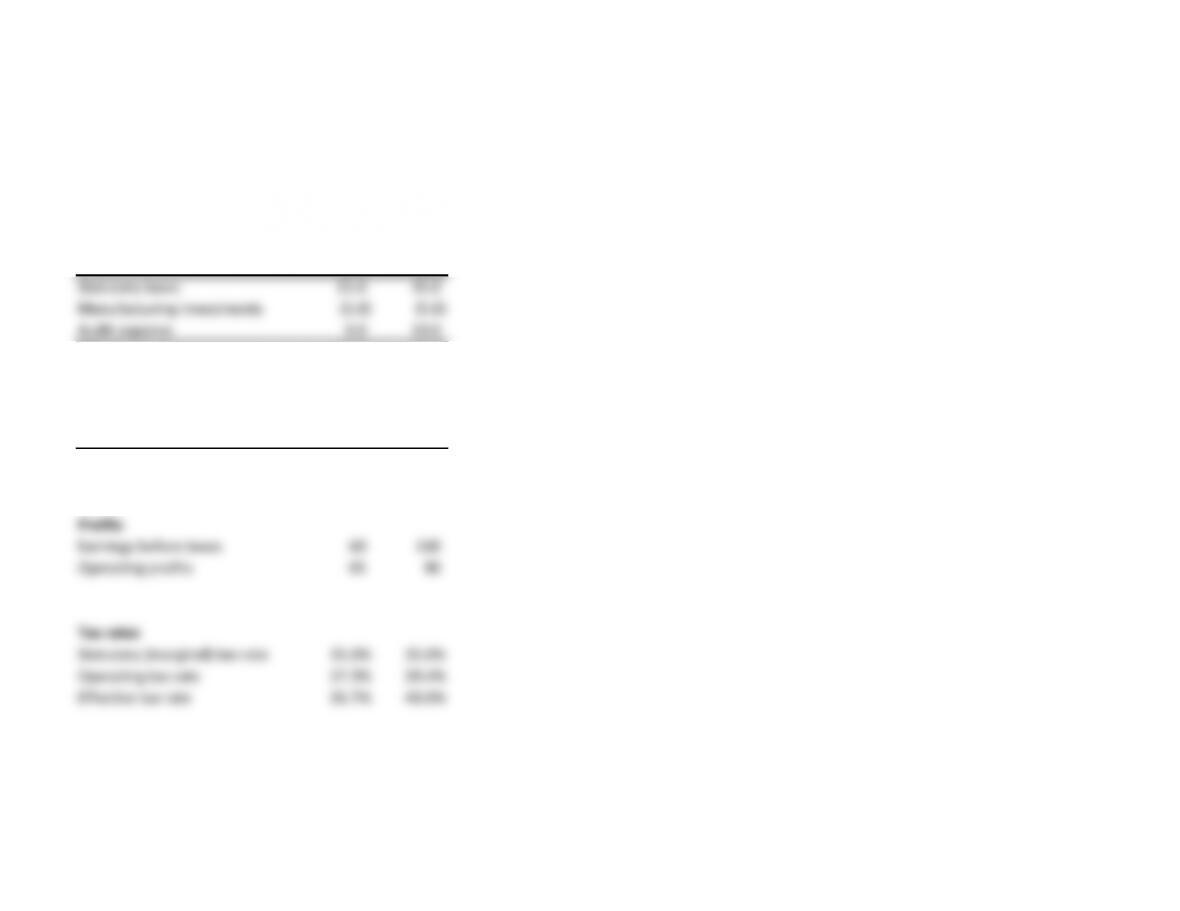

Question 6

HealthCo

Reconciliation of effective taxes

Prior Current

year year

Statutory taxes 21.0 35.0

Manufacturing investments (5.0) (5.0)

Audit expense 0.0 10.0

Effective taxes 16.0 40.0

Statutory taxes 35.0% 35.0%

Manufacturing investments -8.3% -5.0%

Audit expense 0.0% 10.0%

Effective taxes 26.7% 40.0%

Profits

Earnings before taxes 60 100

Operating profits 65 90

Tax rates

Statutory (marginal) tax rate 35.0% 35.0%

Operating tax rate 27.3% 29.4%

Effective tax rate 26.7% 40.0%

Chapter 7

Question 7

Commentary

Excess cash is not “invested” capital, and is not necessary for core

operations. Therefore, it should be analyzed and valued

separately. Including cash in the computation of ROIC will

incorrectly depress the ROIC.

EXHIBIT7.15 Ratio Analysis: Consolidated Financial Statements

$ millions

CompanyA CompanyB CompanyC

Operatingprofit 100 100 100

Interest 0 0 (20)

Earningsb eforetaxes 100 100 80

Taxes (25) (25) (2 0)

Net income 75 75 60

Balances heet:

Inventory 125 125 125

Propertyand equ ipment 400 400 400

Equityin vestments 0 50 0

Total assets 525 575 525

Accounts payable 50 50 50

Debt 0 0 200

Equity 475 525 275

Liabilities and equity 525 575 525

ExhibitData:

Taxrate 25%