Valuation

Measuring and Managing the Value of Companies

5th Edition

Chapter 27 Solutions

Leases, Pensions, and Other Obligations

Version 1.0

April 1, 2010

Chapter 27

Questions 1 & 2

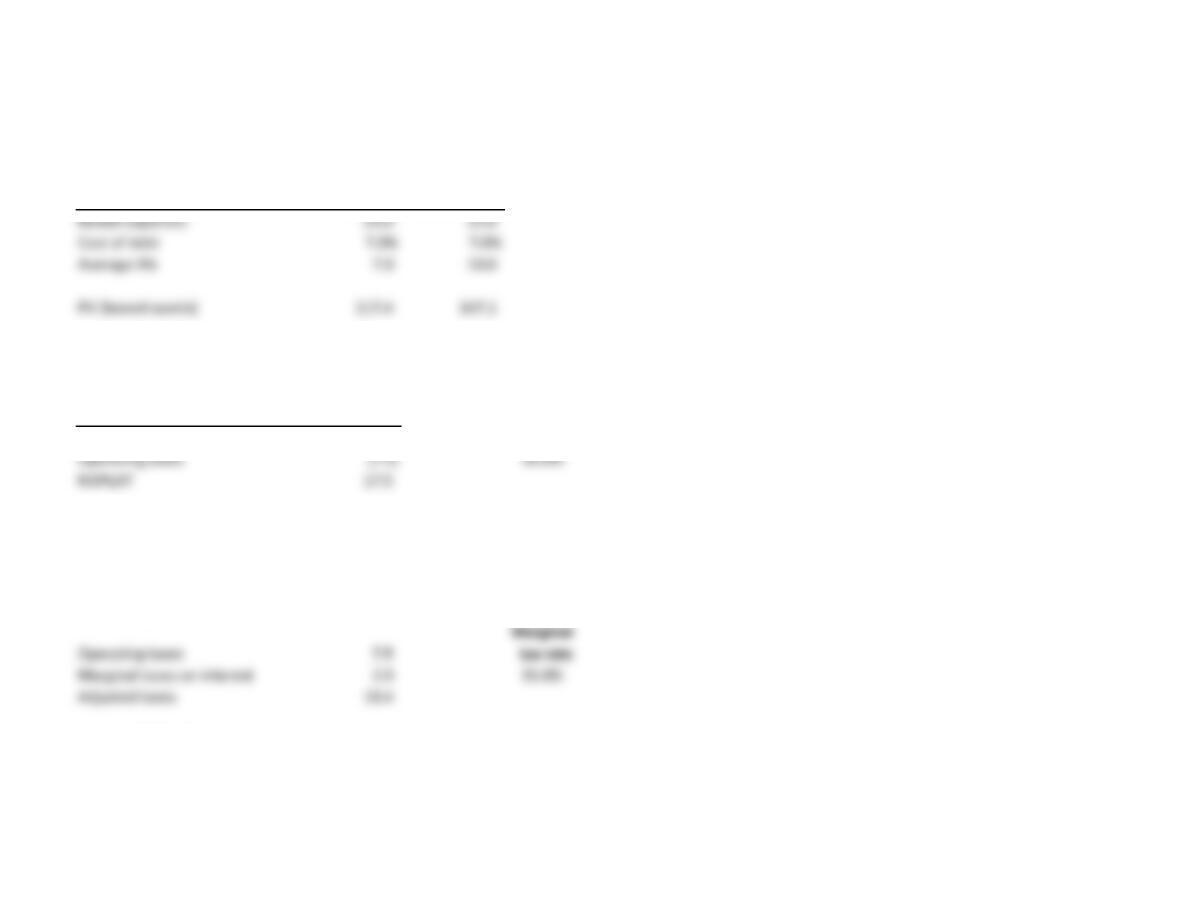

PV (leased assets) Correct Misestimation

Rental expenses 25.0 25.0

Cost of debt 7.0% 7.0%

Average life 7.0 10.0

PV (leased assets) 117.4 147.1

Question 2

NOPLAT Operating

Operating profit 25.0 tax rate

Operating taxes (7.5) 30.0%

NOPLAT 17.5

Adjusted profit

Operating profit 25.0

Lease interest 8.2

Adjusted profit 33.2

Marginal

Operating taxes 7.5 tax rate

Marginal taxes on interest 2.9 35.0%

Adjusted taxes 10.4

Adjusted NOPLAT 22.8

Chapter 27

Question 3

Commentary

Using the present value of reported rental expenses systematically undervalues the asset, since it ignores the residual value returned at

the end of the lease contract. As stated in the text, most would agree that a $1 million asset leased for two years is worth more than the

present value of two payments of $100,000 per year.

Chapter 27

Question 4

Commentary

The cost for securitizing receivables is included in either SG&A expense or interest expense. If the cost is included in interest expense,

then receivables must be securitized; otherwise the cost of securitization will not be captured in the valuation. If the cost is included

in SG&A, then the cost must be removed from SG&A for valuation purposes, if (and only if) receivables are securitized.

Chapter 27

Question 5

Procter & Gamble

Income statement

2009 2008 2007

Operating income 16,123 16,637 15,003

Pension expense 124 14 (39)

Service expense (305) (358) (364)

Prior service cost (credit) amortization 9 7 9

Adjusted operating income 15,942 16,293 14,600

Procter & Gamble, annual report, Note 8

Postretirement benefits and employee stock ownership plan

2009 2008 2007 2009 2008 2007

Service cost 214 263 279 91 95 85

Interest cost 551 539 476 243 226 206

Expected return on plan assets (473) (557) (454) (444) (429) (407)

Prior service cost (credit) amortization 14 14 13 (23) (21) (22)

Net actuarial loss amortization 29 945 2 7 2

Curtailment and settlement gain 6 (36) (176) –(1) (1)

Gross benefit cost (credit) 341 232 183 (131) (123) (137)

Dividends on ESOP preferred stock ––– (86) (95) (85)

Net periodic benefit cost (credit) 341 232 183 (217) (218) (222)

Other retiree benefits

Pension benefits

Source: www.pg.com/en_US/downloads/investors/annual_reports/2009/PG_2009_AnnualReport.pdf.

Chapter 27

Question 6

Commentary

P&G had more than $3.7 billion in unfunded pension benefits and $1.5 billion in unfunded other benefits in 2009.

Procter & Gamble

Annual report, 2009

Classification of net amount recognized

Other retiree benefits

Years ended June 30 2009 2008 2009 2008

Noncurrent assets 133.0 321.0 –200.0

Current liability (41.0) (45.0) (18.0) (16.0)

Noncurrent liability (3,798.0) (3,146.0) (1,516.0) (512.0)

Net amount recognized (3,706.0) (2,870.0) (1,534.0) (328.0)

For instance:

Other noncurrent liabilities, which totaled $9,249 million in 2009, included $3,798 million in unfunded pension liabilities and $1,516 million in unfunded other retiree benefits.

Source: www.pg.com/en_US/downloads/investors/annual_reports/2009/PG_2009_AnnualReport.pdf.

Pension benefits