Valuation

Measuring and Managing the Value of Companies

5th Edition

Chapter 14 Solutions

Using Multiples to Triangulate Results

Version 1.0

April 1, 2010

Chapter 14

Questions 1 & 2

$ million Company 1 Company 2 Company 3

Share price ($) 25 16 30

Shares outstanding (millions) 5 8 15

Equity value 125 128 450

Short-term debt 25 15 30

Long-term debt 50 70 40

Total debt 75 85 70

Gross enterprise value 200 213 520

Nonconsolidated subsidiaries – – (50)

Core operating value1200 213 470

EBITDA will be lower for Company 1 if the company outsources

Operating income production. This causes its enterprise-value-to-EBITDA

EBITDA 25 30 59 multiple to be higher than the EV-to-EBITDA multiples of

EBITA 22 23 51 competitors that produce internally.

Multiples

Enterprise value to EBITDA 8.0 7.1 8.0

Enterprise value to EBITA 9.1 9.3 9.2

1 Also known as net enterprise value

Chapter 14

Questions 3 & 4

Driver Company A Company B Company C Other input

Operating profit 160.0 100.0 120.0 Tax rate 25%

Operating taxes 40.0 25.0 30.0

NOPLAT 120.0 75.0 90.0

Growth 2.0% 6.0% 5.0%

ROIC 15.0% 10.0% 12.0%

WACC 10.0% 10.0% 10.0%

Value 1,300.0 750.0 1,050.0

EV-to-EBITA multiple 8.1 7.5 8.8

Company A versus Company B

Company B has an ROIC equal to its cost of capital, so growth fails to create value. Consequently, no premium

is paid for growth and the company trades at a lower multiple.

Company A versus Company C

Both Company A and Company C have ROIC above their cost of capital, so growth leads to higher value. Company C

also has a lower ROIC, but this is more than offset by the higher growth rate.

Chapter 14

Question 5

If future cash flows (and the cost of capital) are the same for two companies, their valuations will be the same. If one

company has lower short-term earnings, then enterprise value to EBITA will be higher for that company since value

remains the same but earnings drop. This can make multiples analysis confusing. A higher multiple doesn’t always

mean better long-term prospects. It could just represent a short-term depression in earnings.

Chapter 14

Question 6

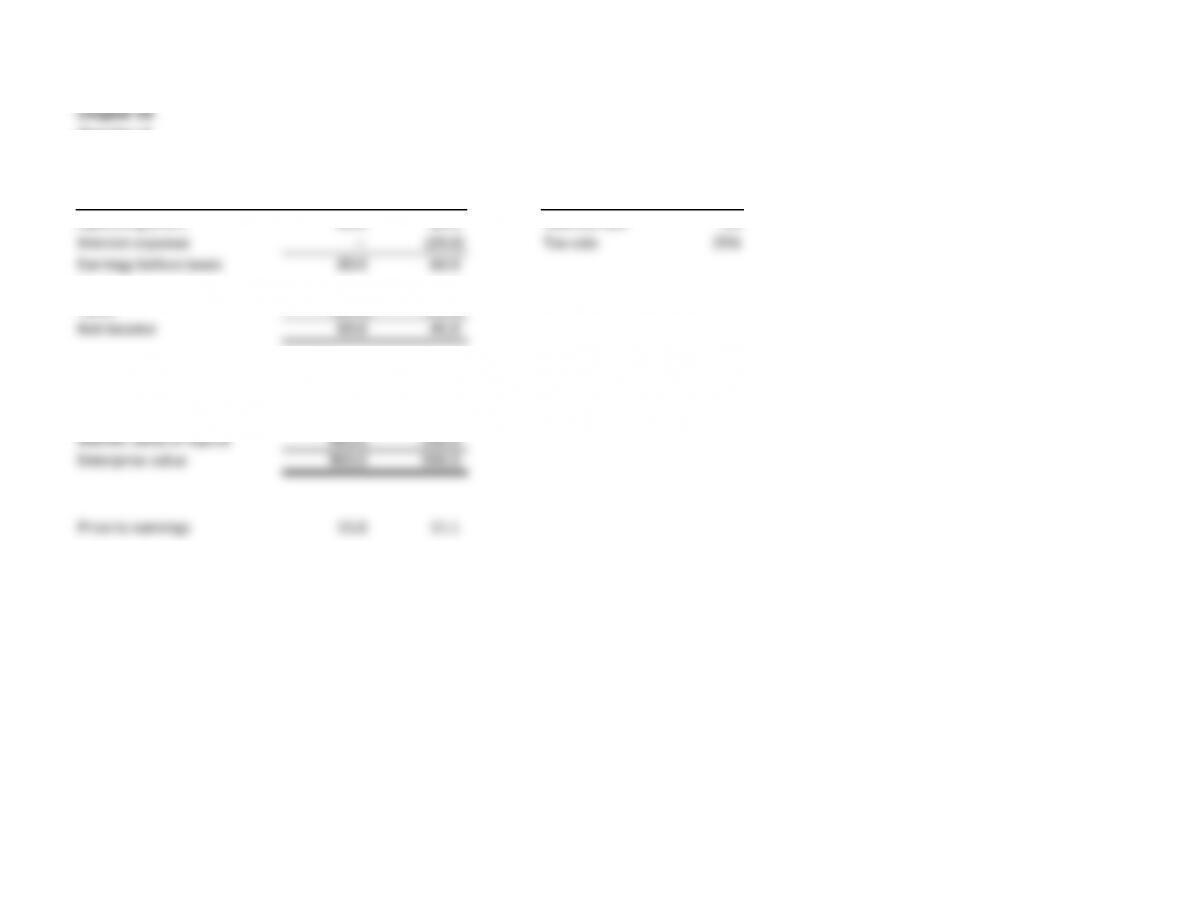

All

Income statement equity Levered Other inputs

Operating profit 80.0 80.0 Interest rate 5%

Interest expense – (20.0) Tax rate 25%

Earnings before taxes 80.0 60.0

Taxes (20.0) (15.0)

Net income 60.0 45.0

Enterprise value

Debt – 400.0

Market value of equity 900.0 500.0

Enterprise value 900.0 900.0

Price to earnings 15.0 11.1

Exhibit 14.12 Multiples Analysis: Market and Profit Data

$ million

Company 1 Company 2 Company 3

Market data

Share price (dollars) 25 16 30

Shares outstanding (millions) 5 8 15

Short-term debt 25 15 30

Long-term debt 50 70 40

Operating profit

EBITDA 25 30 59

EBITA 22 23 51