Valuation

Measuring and Managing the Value of Companies

5th Edition

Chapter 12 Solutions

Moving from Enterprise Value to Value per share

Version 1.0

April 1, 2010

Chapter 12

Questions 1 & 2 Question 1 Question 2

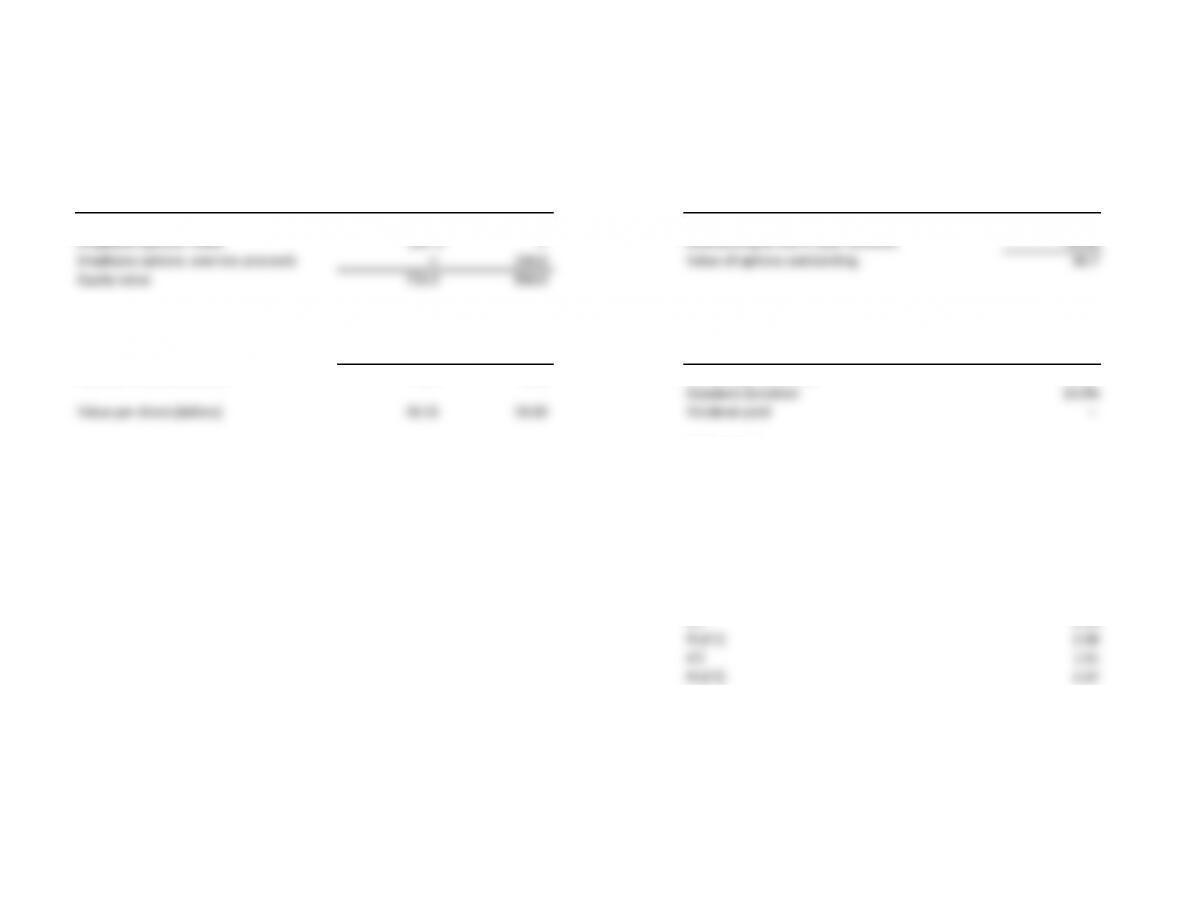

Valuation Sale No sale Nonconsolidated subsidiary Contingent claim

Value of operations 2,500.0 2,500.0 Nonconsolidated subsidiary 500 Contingent claim 100

Nonconsolidated subsidiary 100.0 79.0 Percent ownership 20% Probability of occurrence 10%

Enterprise value 2,600.0 2,579.0 Value to MarineCo 100 Expected claim 10

Unfunded pension liabilities (200.0) (200.0) Gain on sale After-tax cash to MarineCo

Contingent claim (7.0) (7.0) Value to MarineCo 100 Expected claim 10

Equity value 2,393.0 2,372.0 Book value (30) Tax deduction (3)

Gain on sale 70 After-tax expected claim 7

Key data After-tax cash to MarineCo

Marginal tax rate 30% Value to MarineCo 100

Taxes on sale at 30% (21)

After-tax cash to MarineCo 79

Chapter 12

Questions 3 & 4

Manufacturing subsidiary

Customer financing subsidiary

Operating profit Net income Key statistics

Sales of machinery 1,500 Revenues of financial products 400 Return on invested capital 9.5%

Cost of goods sold (1,000) Interest expense of financial products (350) Return on invested capital plus ROE 12.5%

Operating profit 500 Net income 50 Return on equity 21.4%

Reorganized balance sheet Reorganized balance sheet Interest rate to company 10.0%

Operating assets 2,200 Financial receivables 4,000 Interest rate on financing debt 9.7%

Operating liabilities (400)

Invested capital 1,800 Debt related to customer financing 3,600 Operating margin—machinery 27.3%

Allocated equity 400 Operating margin—finance 16.7%

General obligation debt – Liabilities and allocated equity 4,000

Allocated equity #VALUE!

Invested capital 1,800

Return on invested capital 27.8% Return on allocated equity 12.5%

Question 4

MarineCo’s financing subsidiary should be evaluated as a stand-alone entity. Since the subsidiary is owned by a company with other assets (the

manufacturing business), MarineCo could use the manufacturing business as collateral for the finance subsidiary’s debt. In the extreme, a lender

could lend 100 percent of financial receivables as long as additional collateral is pledged, causing allocated equity to equal zero. A pure-play bank

could never raise 100 percent debt. In this case, MarineCo’s equity is understated and ROE is too high.

Chapter 12

Question 5

Weighted Weighted

Enterprise Debt Equity enterprise equity

Scenario value value value Probability value value

Scenario 1 300.0 (200.0) 100.0 25.0% 75 25.0

Scenario 2 200.0 (200.0) – 50.0% 100 –

Scenario 3 100.0 (200.0) – 25.0% 25 –

200 25.0

New management plan

Weighted Weighted

Enterprise Debt Equity enterprise equity

Scenario value value value Probability value value

Scenario 1 300.0 (200.0) 100.0 25.0% 75 25.0

Scenario 2 200.0 (200.0) 0.0 75.0% 150 –

Scenario 3 100.0 (200.0) 0.0 – – –

225 25.0

Difference in enterprise value

25

Difference in debt value 25

Difference in equity value –

The entire value increase accrues to the debt holder, a common problem with distressed companies.

Chapter 12

Question 6

Value of Exercise Exhibit data

outstanding value

options approach Option data Outstanding

Enterprise value 800.0 800.0 European call value ($) 6.67

Employee options: value (66.7) – Outstanding at end of year (million) 10.00

Employee options: exercise proceeds – 150.0 Value of options outstanding 66.7

Equity value 733.3 950.0

Number of shares (million) Option pricing

Number of nondiluted shares 40.0 40.0

New shares issued – 10.0 Stock price inputs Outstanding

Number of diluted shares 40.0 50.0 Underlying asset value 18.33

Standard deviation 10.0%

Value per share (dollars) 18.33 19.00 Dividend yield –

Option inputs

Strike price 15.00

Expiration (in years) 5.00

Market inputs

Risk-free rate 5.00%

Option price calculations

Variance 0.01

d12.13

N(d1) 0.98

d21.91

N(d2) 0.97

European call value 6.67

EXHIBIT 12.8 MarineCo: Income Statement and Balance Sheet

$ million

Income statement Balance sheet

Sales of machinery 1,500 Operating assets 2,200

Revenues of financial products 400 Financial receivables 4,000

Total revenues 1,900 Total assets 6,200

Cost of goods sold (1,000)

Interest expense of financial products (350) Operating liabilities 400

Total operating costs (1,350) General obligation debt –

Debt related to customer financing 3,600

Operating profit 550 Stockholders’ equity 2,200

Interest expense, general obligation (80) Total liabilities and equity 6,200

Net income 470