Valuation

Measuring and Managing the Value of Companies

5th Edition

Chapter 11 Solutions

Estimating the Cost of Capital

Version 1.0

April 1, 2010

Chapter 11

Questions 1 & 2

Question 1

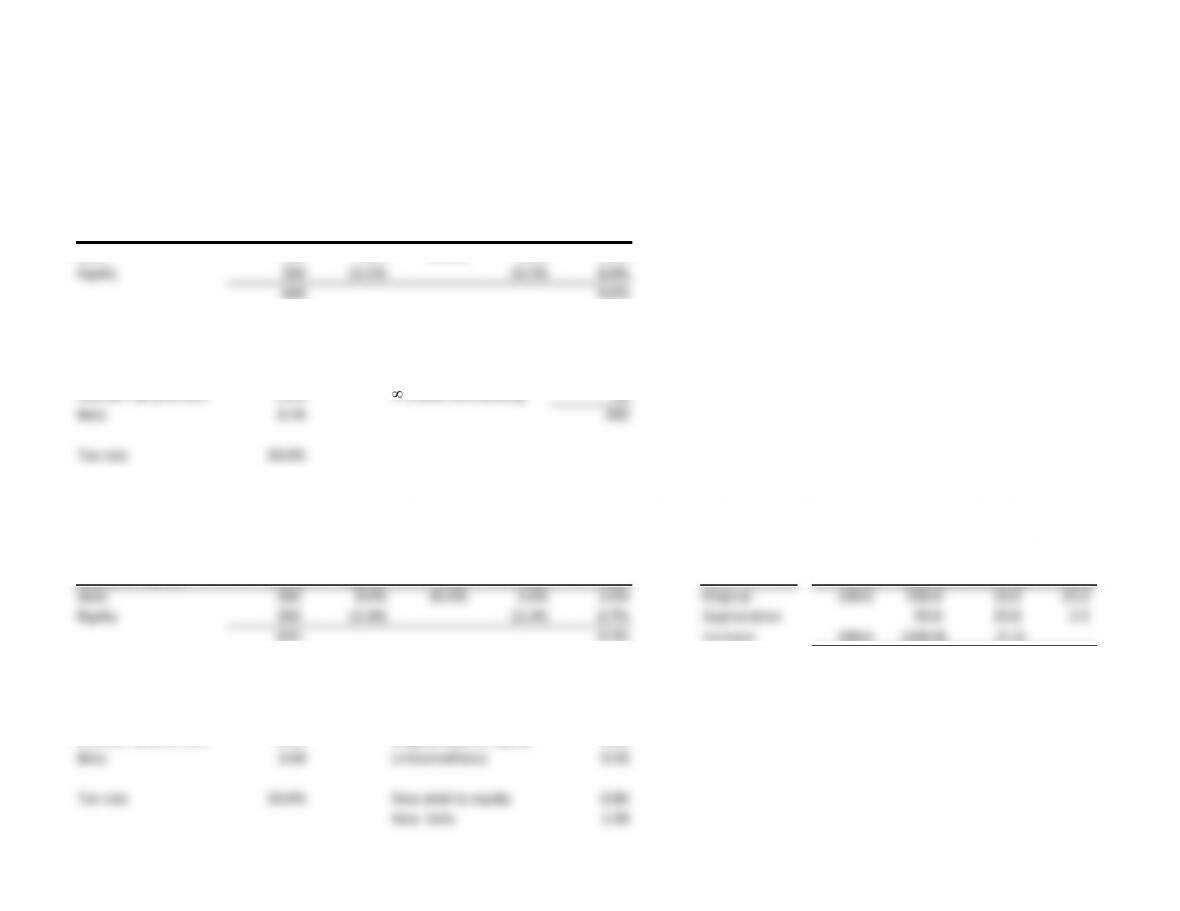

Market Cost of Tax After-tax Weighted

Source of capital value capital rate cost cost

Debt 100 7.5% 30.0% 5.3% 0.9%

Equity 500 10.5% 10.5% 8.8%

600 9.6%

Key inputs Market capitalization

Risk-free rate 7.0% Share price 25

Market risk premium 5.0% Shares outstanding 20

Beta 0.70 500

Tax rate 30.0%

Question 2 Capital structure changes

.Market Cost of Tax After-tax Weighted Shares

Source of capital value capital rate cost cost Debt Equity

Outstanding

Price

Debt 300 8.0% 30.0% 5.6% 2.6% Original 100.0 500.0 20.0 25.0

Equity 350 12.4% 12.4% 6.7% Appreciation 50.0 20.0 2.5

650 9.3% Increase 200.0 (200.0) (7.3)

Total 300.0 350.0 12.7 27.5

Key inputs Unlevered beta

Risk-free rate 7.0% Original beta 0.70

Market risk premium 5.0% Original debt to equity 0.20

Beta 1.08 Unlevered beta 0.58

Tax rate 30.0% New debt to equity 0.86

New beta 1.08

Chapter 11

Question 3

Commentary

Since the financial projections for São Paolo Foods are in Brazilian reais (R$), the risk-free rate should be the Brazilian rate, not the German

rate. The beta for EuropeCo is also irrelevant, since the company’s composition (and consequently risk) does not match that of São Paolo Foods.

Chapter 11

Question 4

In Chapter 11, ke is estimated using:

Key inputs

Price-to-earnings ratio 11.1

Return on equity 13.5%

Long-run growth in cash flow 6.7%

Implied cost of equity 11.2%

=+

=ROE

–1Earningsbecause

Price

ROE

–1Earnings g

CFg

g

kee

Chapter 11

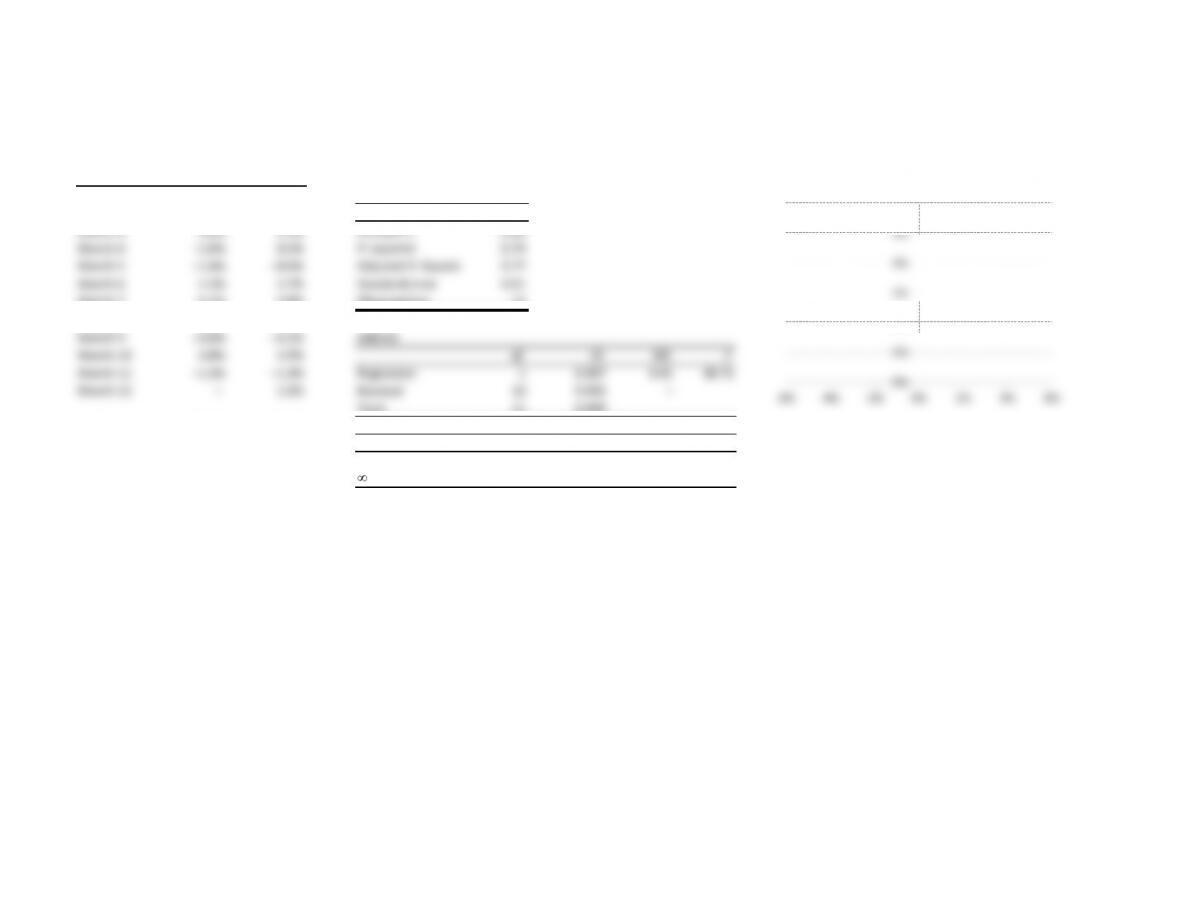

Question 5

Company Market Summary output

Month 1 1.3% 1.0%

Month 2 2.0% 1.2% Regression s tatistics

Month 3 5.0% 3.4% Multiple R0.89

Month 4 –1.0% 0.3% R-squared 0.79

Month 5 –1.4% –0.6%

Adjusted R-Squared

0.77

Month 6 2.2% 3.7% Standard error 0.01

Month 7 6.1% 4.8% Observations 12

Month 8 0.3% –2.3%

Month 9 –4.0% –4.5% ANOVA

Month 10 3.8% 3.9% df SS MS F

Month 11 –1.2% –1.3% Regression 1 0.007 0.01 38.75

Month 12 – 1.8% Residual 10 0.002 –

Total 11 0.009

Average 2.96% 2.51%

Volatility 2.14% 1.64%

Coefficients

Standard error

t-Stat P-value

Intercept – – 0.49 0.63

Variable 1 0.93 0.15 6.22 –

0%

1%

2%

3%

4%

5%

6%

-6% -4% -2% 0% 2% 4% 6%

Regression Data

Chapter 11

Question 6

Market price Solutions

Price 80.0 Yield to maturity 31.3%

Cost of debt 7.2%

Promised final cash flow

Face 100.0

Coupon 5.0

Final cash flow 105.0

Expected final cash flow

Bond paid 105.0

Bond defaults 50.0

Expected value 85.8

Key data

Coupon 5.0%

Probability of default 35.0%