77

Annual Report 2009

Group management report » Forecast

offer our customers added value. And we have a well filled

pipeline of innovative products that we intend to launch

onto the markets of all three business sectors this year.

Further opportunity lies in our strict focus on cost and

our willingness to constantly scrutinize and analyze the sta–

tus quo. From the results of such investigations we regularly

find further potential for cost reductions, capacity adjust-

ments and the elimination of marginal business activities

and minor brands from our portfolio.

Opportunity is also likely to arise from the consistent

pursuit and implementation of our three strategic priorities,

as explained in some detail in the section entitled “Strategy

and financial targets 2012” on pages 34 to 36.

Further specific opportunities and risks are discussed

in the individual business sector reports starting on

page 58.

Outlook for the Henkel Group in 2010

In our opinion, the mildly encouraging market conditions

prevailing in the real economy and on the financial markets

are still fragile. Consequently, we are unable to accurately

gage the overall economic situation and the further devel-

opments that are likely to take place.

Our guidance for the current financial year is based

on the assumption of moderate economic growth overall.

We do not expect to see a sustained upturn or any major

growth dynamic.

It is against this background that our expectations for

the development of the Henkel Group for 2010 should be

considered:

We are confident of again outperforming our relevant

markets in terms of organic sales growth (i.e. after adjusting

for foreign exchange and acquisitions/divestments). The basis

for this confidence is provided by our strong competitive

position. This we have consolidated and further extended

in recent years through our innovative strength, our strong

brands, our leading market positions and the quality of

our portfolio.

In recent years, we have introduced a number of mea–

sures on the operational side which we expect to generate

positive momentum: for example, we anticipate addition–

al contributions to our profitability to emanate from our

“Global Excellence” efficiency enhancement program, the

synergies arising from the integration of the National Starch

businesses, and our strict cost discipline. All these factors

We are more confident about the development of the elec-

tronics industry. The recovery of the sector, which has been

in evidence for some months now, can be expected to con-

tinue, albeit from a still low base. We anticipate that many

companies will be investing more in new communication

and information technologies after their reluctance over

the last year, particularly as a certain degree of backlog

demand has built up.

The metal processing industry will, in 2010, experience

no more than sluggish expansion according to our estimates.

Although investments will be made in new machinery and

equipment for the purpose of rationalization or replace–

ment, more extensive expenditures will be required before

faster growth can be achieved. However, such investments

will only be made in the prospect of a durable upturn, of

which there is as yet little sign.

Growth in the packaging sector will, in our view, be

below that of industry overall. Here, the expected low level

of consumption growth is likely to exert a major influence,

due to the fact that a substantial portion of demand for

packaging comes from the food and semi-luxuries sectors.

The industry-related packaging segment should, by our

reckoning, experience a somewhat stronger increase in

production levels.

Our forecast for the construction industry is for a slight

increase in output. The financial packages of last year will

still generate a positive effect on developments in 2010, and

the building investments of industry should slightly increase

as confidence improves. However, as the year progresses,

the structural problems of both the residential and – due

to increasingly scarce public funds – the publicly financed

building sectors could come more to the forefront.

Opportunities

Accompanying the risks, we also see opportunities for our

businesses:

We perceive the growth regions as holding great poten–

tial for us. These offer above-average growth possibilities

from which we hope to benefit through our local business

activities. This especially applies to the regions of Eastern

Europe and Africa/Middle East, with Asia and Latin America

also part of the group.

We regard our research and development activities as

a great source of opportunity. We are developing a steady

stream of innovative products and product solutions that

78 Annual Report 2009

Group management report » Forecast / Subsequent events

Long-term sales and profits forecast:

Financial targets for 2012

In placing our focus on our three strategic priorities de–

veloped in 2008, and given the progress made to date in

their achievement, we have laid the foundation for future

profitable growth.

We expect that after 2010, during which a degree of moder–

ate growth is likely, the world economy will – in the course

of 2011 and 2012 – return to long-term growth of around

3 to 4 percent per year.

Based on this assumption, we will be aiming in the com–

ing years to achieve an average organic growth rate of 3 to

5 percent above the rate of growth of the markets of rel–

evance to us. Due to the expected savings emanating from

the “Global Excellence” efficiency enhancement program,

the synergies arising from the integration of the National

Starch businesses and numerous additional measures geared

to achieving our full business potential, we are confident

that, by 2012, we will also have met our targets of an ad–

justed1) return on sales (EBIT) of 14 percent and an average

annual increase in adjusted1) earnings per preferred share

(EPS) in excess of 10 percent per year.

Subsequent events

There were no notifiable events between the balance sheet

date (December 31, 2009) and the preparation date (Janu–

ary 29, 2010).

will positively influence the development of our adjusted1)

operating profit (EBIT) and adjusted

1)

earnings per preferred

share (EPS). We expect both metrics to undergo a noticeable

improvement compared to the levels of 2009.

We detail further specific expectations in the business

sector summaries starting on page 58.

Dividends

Our dividends and distribution policy is primarily aligned

to earnings after deducting minority interests and adjusting

for exceptional items. The objective is to maintain a payout

ratio of around 25 percent.

Research and development

Irrespective of the current economic climate, the develop-

ment of innovative products is an essential activity for our

business. Consequently, we plan to invest around 2.8 percent

of our gross sales in R&D.

Capital expenditures

We intend to invest around 350 million euros in the prop-

erty, plant and equipment of our continuing operations

during the current financial year. Major investments at the

Laundry & Home Care and Cosmetics/Toiletries business

sectors are to be channeled into production facilities for the

manufacture of innovative, sustainable product lines, as well

as into structural optimization measures. The 2010 invest-

ment focus in the case of the Adhesive Technologies business

sector will be on further consolidation and rational ization

of our adhesives production capability, and on production

expansion in our growth markets. For structural reasons, a

therefore further strengthen our financial situation, one

of our goals in this context being to achieve and maintain

a credit rating in the “A flat” range.

1) Adjusted for one-time charges/gains and restructuring charges

Financial targets for 2012

Annual organic sales growth (average):

3 – 5 percent

Adjusted1) return on sales (EBIT):

79

Annual Report 2009

84 Group segment report by business sector

85 Group segment report by region

86 Consolidated changes in intangible assets,

property, plant and equipment and financial

assets

87 Accounting principles and methods applied

in preparation of the consolidated financial

statements

91 Notes to the consolidated statement of income

95 Notes to the consolidated balance sheet

119 Supplementary information on the consolidated

statement of income / balance sheet

130 Recommendation for the approval of the annual

financial statements and the appropriation of the

profit of Henkel AG & Co. KGaA

131 Annual financial statements of

Henkel AG & Co. KGaA (summarized)

132 Auditor’s report

133 Responsibility statement

134 Corporate management of Henkel AG & Co. KGaA

80 Consolidated statement of income

81 Consolidated balance sheet

82 Consolidated cash flow statement

83 Statement of comprehensive income

83 Statement of changes in equity

Consolidated financial statements » Subindex

Consolidated financial statements subindex

80 Annual Report 2009

Consolidated financial statements » Consolidated statement of income

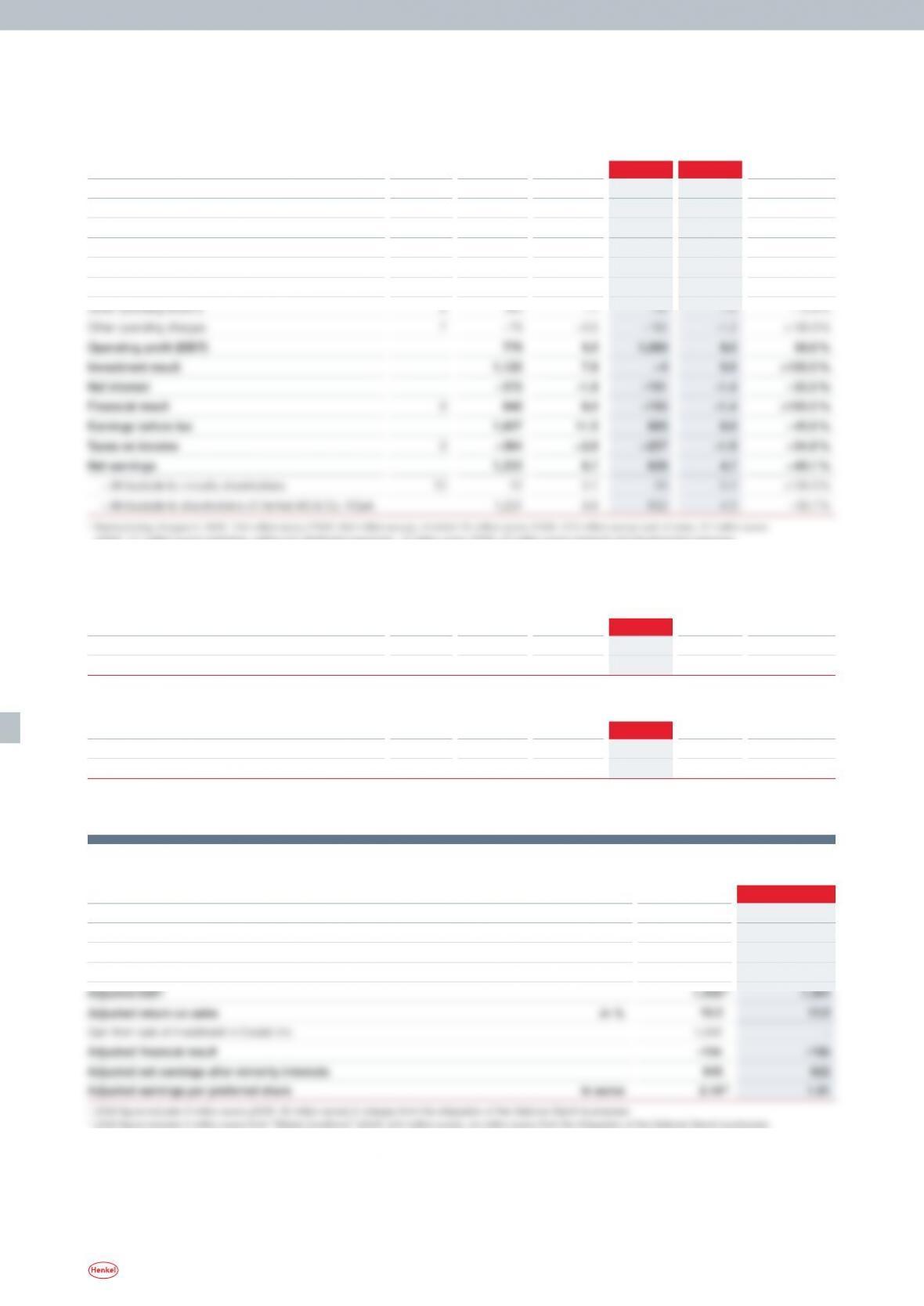

Consolidated statement of income

in million euros Note 2008 % 2009 % Change

Sales

1

14,131 100.0 13,573 100.0 – 3.9 %

Cost of sales1) 2 – 8,190 – 58.0

– 7,411 – 54.6

– 9.5 %

Gross profit 5,941 42.0 6,162 45.4 3.7 %

Marketing, selling and distribution expenses

1) 3 – 3,993 – 28.3

– 3,926 – 28.9

–1.7 %

Research and development expenses

1) 4 – 429 – 3.0

–396 – 2.9

– 7.7 %

Administrative expenses

1) 5 – 825 – 5.8

–735 – 5.4

–10.9 %

(2008: 111 million euros) marketing, selling and distribution expenses, 13 million euros (2008: 52 million euros) research and development expenses,

24 million euros (2008: 127 million euros) administrative expenses

Earnings per share (basic)

in euros Note 2008 2009 Change

Ordinary shares 46

2.81 1.38

– 50.9 %

Non-voting preferred shares 46

2.83 1.40

– 50.5 %

Earnings per share (diluted)

in euros Note 2008 2009 Change

Ordinary shares 46 2.79

1.38

– 50.5 %

Non-voting preferred shares 46 2.81

1.40

– 50.1 %

Additional voluntary information

in million euros 2008 2009

EBIT (as reported) 779 1,080

One-time gains

– 30 – 9

One-time charges

1)

48 134

Restructuring charges

2)

663 159

(2008: 142 million euros), 59 million euros from the reorganization of the Adhesive Technologies businesses in Europe (2008: 0 million euros) and 56 million euros

from ordinary activities (2008: 17 million euros)

3)

Adjusted EBIT 1,495 million euros and adjusted earnings per preferred share 2.26 euros, both before amortization of intangible assets from the acquisition of the National

Starch businesses

81

Annual Report 2009

Consolidated financial statements » Consolidated balance sheet

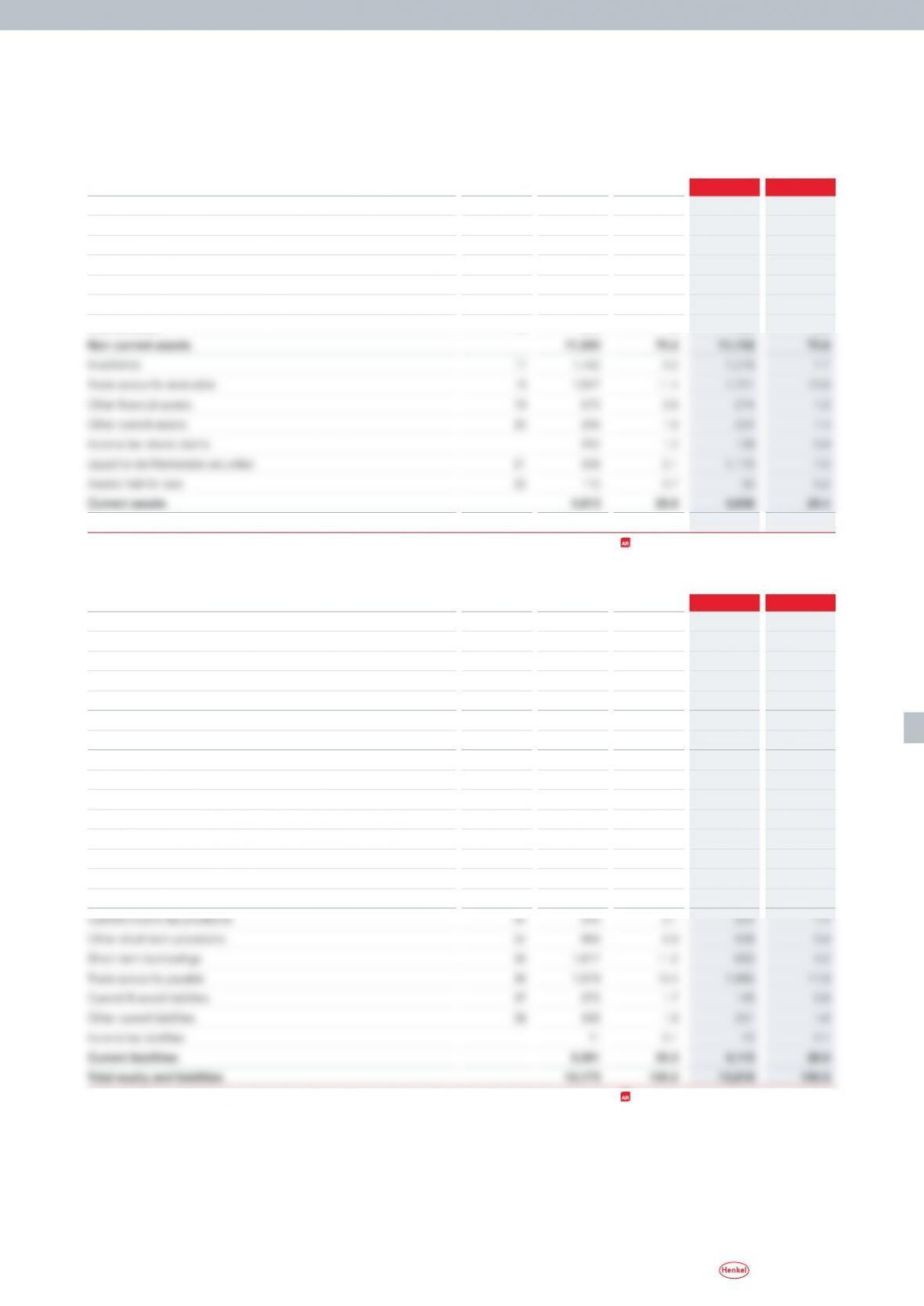

Consolidated balance sheet

Assets

in million euros Note 20081) %2009 %

Intangible assets 11 8,491 52.5

8,218 52.0

Property, plant and equipment 12 2,361 14.6

2,248 14.2

Financial assets 13

24 0.1

20 0.1

Other financial assets

14

172 1.1

340 2.2

Income tax refund claims 3 –

2 –

Other non-current assets

15

4 –

12 0.1

Deferred taxes 16 305 1.9

322 2.0

Total assets 16,173 100.0 15,818 100.0

1)

Adjusted following finalization of purchase price allocation relating to the acquisition of the National Starch businesses, see

page 87 et seq.

Shareholders’ equity and liabilities

in million euros Note 20081) %2009 %

Subscribed capital 23 438 2.7

438 2.8

Capital reserve 24 652 4.0

652 4.1

Retained earnings 25 6,805 42.0

6,908 43.7

Gains and losses recognized in equity 26 –1,411 – 8.7

–1,524 – 9.6

Equity excluding minority interests 6,484 40.0 6,474 41.0

Minority interests 27 51 0.3

70 0.4

Equity including minority interests 6,535 40.3 6,544 41.4

Pensions and similar obligations 28 833 5.2

867 5.5

Long-term income tax provisions 29 177 1.1

152 1.0

Other long-term provisions 29 336 2.1

241 1.5

Long-term borrowings 30 2,402 14.9

3,426 21.7

Non-current financial liabilities

31 77 0.5

88 0.5

Other non-current liabilities

32 9 0.1

20 0.1

Deferred taxes 33 413 2.5

367 2.3

Non-current liabilities 4,247 26.4 5,161 32.6

1)

Adjusted following finalization of purchase price allocation relating to the acquisition of the National Starch businesses, see

page 87 et seq.

82 Annual Report 2009

Consolidated financial statements » Consolidated cash flow statement

See Note 47

in million euros 2008 2009

Operating profit (EBIT) 779 1,080

Income taxes paid

– 412 – 305

Amortization/depreciation/write-ups of non-current assets (excluding financial assets)

546 588

Net gains/losses on disposal of non-current assets (excluding financial assets)

312

Change in inventories

– 78 276

Change in trade accounts receivable

108 136

Change in other receivables and miscellaneous assets

60 –15

Change in trade accounts payable

– 36 208

Change in other liabilities and provisions

195 – 61

Cash flow from operating activities 1,165 1,919

Purchase of intangible assets

– 20 – 28

Purchase of property, plant and equipment

– 473 – 344

Purchase of financial assets/acquisitions

– 3,708 – 8

1)

Proceeds on disposal of subsidiaries and business units

57 90

Proceeds on disposal of other non-current assets

1,752 51

Realization of net investment hedge

119 –

Cash flow from investing activities/acquisitions – 2,273 – 239

Henkel AG & Co. KGaA dividends

– 224 – 224

Subsidiary company dividends (to other shareholders)

– 8 –12

Interest received 90 70

Dividends received

22 –

Interest paid

– 345 – 206

Dividends and interest paid and received – 465 – 372

Change in borrowings

757 –152

Allocation to pension funds

– 262 – 389

Other financing transactions

–10 8

Cash flow from financing activities 20 – 905

Change in cash and cash equivalents due to movements in funds –1,088 775

Change in cash and cash equivalents due to exchange rate movements

–14 – 3

Change in liquid funds and marketable securities –1,102 772

Liquid funds and marketable securities at January 1

1,440 338

Consolidated cash flow statement

Additional voluntary information

Computation of free cash flow

in million euros 2008 2009

Cash flow from operating activities 1,165

1,919

Purchase of intangible assets

– 20 – 28

Purchase of property, plant and equipment

– 473 – 344

Proceeds on disposals of other non-current assets (excluding proceeds from sale of investment in Ecolab Inc.) 40 51

83

Annual Report 2009

Consolidated financial statements » Statement of comprehensive income / Statement of changes in equity

Statement of comprehensive income

in million euros 2008 2009

Net earnings 1,233 628

Foreign exchange effects 103 –104

Financial instruments –100 –11

Actuarial gains/losses –186 – 285

Share of net profits of associates

Effects arising from the current financial year 33 –

Elimination of cumulative foreign exchange effects since initial inclusion –16 –

Other comprehensive income –166 – 400

Total comprehensive income for the period 1,067 228

– Attributable to minority shareholders 16 24

– Attributable to shareholders of Henkel AG & Co. KGaA 1,051 204

Statement of changes in equity

See Notes 23 to 27

in million euros Gains and losses

recognized in equity

Ordinary

shares

Preferred

shares

Trea-

sury

stock

Capital

reserve

Retained

earnings

Translation

differences

Financial

instru-

ments

Minority

interests

Total

At January 1, 2008 260 178 –119 652 6,082 –1,298 –112 63 5,706

Net earnings – – – – 1,221 – – 12

1,233

Foreign exchange effects – – – – – 99 – 4

103

Financial instruments – – – – – – –100 –

–100

Actuarial gains (+) and losses (–)

– – – – –186 – – –

–186

Investments in associates – – – – 17 – – –

17

Total comprehensive

income for the period – – – – 1,052 99 –100 16 1,067

Distributions – – – – – 224 – – – 8

– 232

Sale of treasury stock – – 4 – 1 – – –

5

Other changes in equity – – – – 9 – – –20

–11

At December 31, 2008/

January 1, 2009 260 178 –115 652 6,920 –1,199 – 212 51 6,535

Net earnings – – – – 602 – – 26

628

Foreign exchange effects – – – – – –102 – – 2

–104

Sale of treasury stock – – 6 – 4 – – –

10

Other changes in equity – – – – – – – 7

7

At December 31, 2009 260 178 –109 652 7,017 –1,301 – 223 70 6,544

84 Annual Report 2009

Group segment report

by business sector

1)

Notes to the consolidated financial statements » Group segment report by business sector

See Note 45

in million euros

Laundry &

Home

Care

Cos-

metics/

Toiletries

Adhesives

for Crafts-

men and

Consumers

Industrial

Adhesives

Total

Adhesive

Tech-

nologies

Operating

business

sectors total

Corporate

Henkel

Sales 2009 4,129 3,010 1,738 4,486 6,224 13,363 210 13,573

Change from previous year –1.0 % – 0.2 % –16.9 % – 2.6 % – 7.1 % – 3.8 % – – 3.9 %

Proportion of Group sales 30 % 22 % 13 % 33 % 46 % 98 % 2 % 100 %

Sales 2008 4,172 3,016 2,092 4,608 6,700 13,888 243 14,131

other rights and property, plant

and equipment 2009 121 46 96 282 378 545 43 588

of which impairment losses 2009 10 1 32 105 137

5) 148 27 175

of which write-ups 2009 1 – – 2 2 3 – 3

Amortization/depreciation and

write-ups of trademark rights,

other rights and property, plant

and equipment 2008

112

51

48

168

216

379

167

546

of which impairment losses 2008 58 35 4 33 37 130 23 153

of which write-ups 2008 – – – – – – – –

EBIT 2009 501 387 104 186 290

6) 1,178 – 98

4) 1,080

EBIT 2008

439 376 233 425 658 1,473 – 694 779

Change from previous year

14.0 % 3.1 % – 55.3 % – 56.3 % – 55.9 % – 20.0 % – 38.6 %

Return on sales (EBIT) 2009 12.1 % 12.9

% 6.0

% 4.2

% 4.7

% 8.8

%–8.0

%

Return on sales (EBIT) 2008

10.5 % 12.5 % 11.1 % 9.2 % 9.8 % 10.6 % – 5.5 %

Capital employed 2009

2) 2,562 2,125 1,161 5,874 7,035 11,722 –181 11,541

Capital employed 2008

2)

2,604 2,151 1,299 5,291 6,590 11,345 – 24 11,321

Operating assets 2008

3)

3,893 2,763 1,641 6,439 8,080 14,736 398 15,134

Operating liabilities 2008

1,154 819 423 1,451 1,874 3,847 422 4,269

Net operating assets

employed 2008

3)

2,739 1,944 1,218 4,988 6,206 10,889 – 24 10,865

1) Calculated on the basis of units of 1,000 euros

2) Including goodwill at cost prior to any accumulated amortization in accordance with IFRS 3.79 (b)

3) Including goodwill at net book value

4) Including restructuring charges for the National Starch businesses of 44 million euros; the ongoing restructuring costs are charged to the operating business sectors

5) Including 46 million euros of goodwill impairment losses; see other operating charges

6) Including 59 million euros from the reorganization of the Adhesive Technologies businesses in Europe

85

Annual Report 2009

Notes to the consolidated financial statements » Group segment report by region

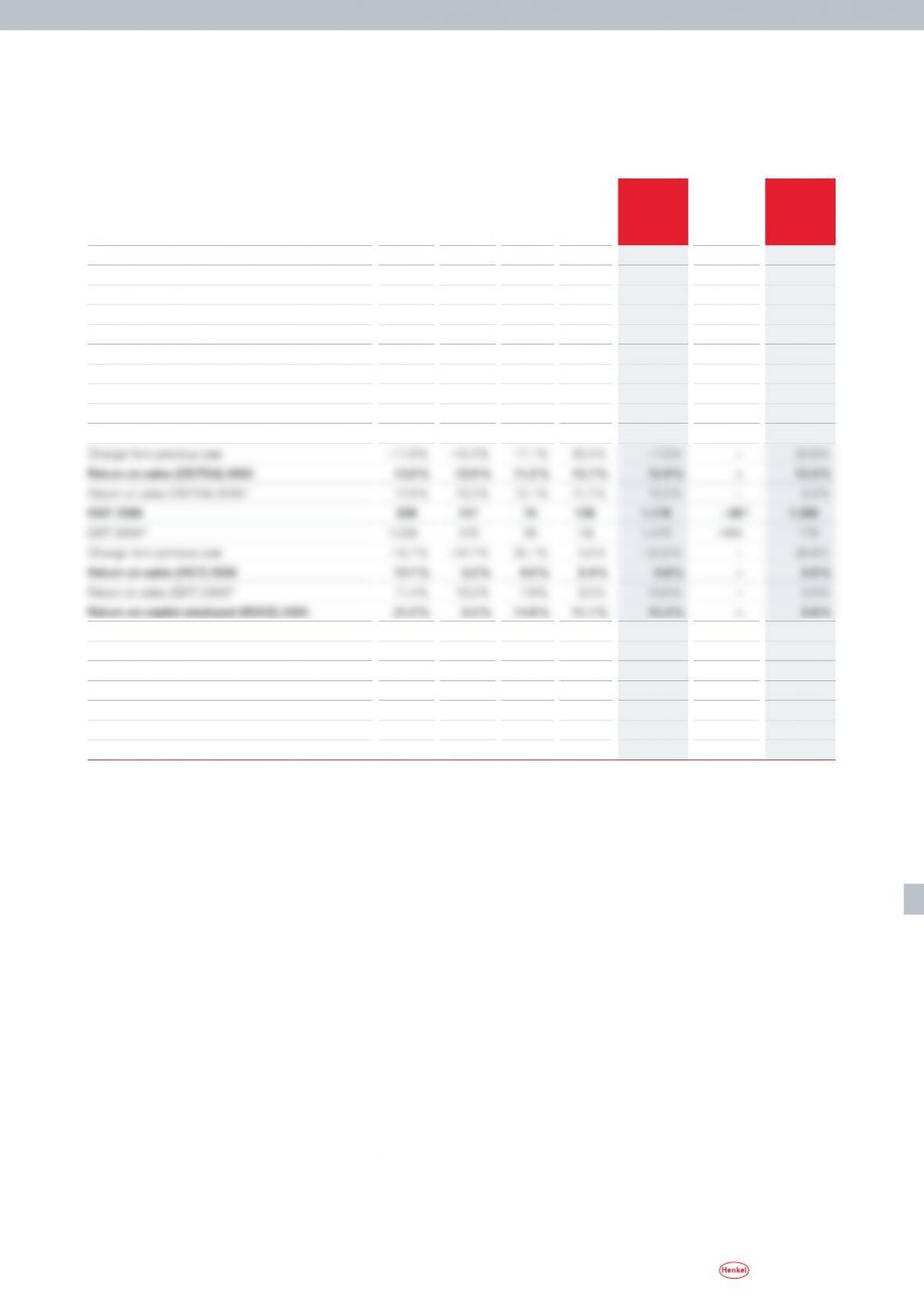

Group segment report

by region1)

See Note 45

in million euros

Europe/

Africa/

Middle

East

North

America

(USA,

Canada)

Latin

America

Asia-/

Pacific

Regions

total

Corporate

Henkel

Sales by location of company 2009 8,335 2,546 825 1,657 13,363 210 13,573

Change from previous year – 6.0 % – 5.7 % 5.8 % 7.3 % – 3.8 % – – 3.9 %

Proportion of Group sales 61 % 19 % 6 % 12 % 98 % 2 % 100 %

Sales by location of company 2008 8,863 2,700 780 1,545 13,888 243 14,131

Sales by location of customer 2009 8,267 2,512 833 1,751 13,363 210 13,573

Change from previous year – 6.0 % – 5.8 % 5.3 % 7.3 % – 3.8 % – – 3.9 %

Proportion of Group sales

61 % 18 % 6 % 13 % 98% 2 % 100 %

Sales by location of customer 2008 8,798 2,668 791 1,631 13,888 243 14,131

EBITDA 2009 1,083 320 92 228 1,723 – 55 1,668

EBITDA 2008

4) 1,228 365 79 180 1,852 – 527 1,325

Return on capital employed (ROCE) 2008

4)

24.9 % 5.2 % 12.1 % 8.7 % 13.0 % – 6.9 %

Operating assets 2009

2)5,749 6,444 652 1,975 14,820 357 15,177

Operating liabilities 2009 2,310 485 178 520 3,493 538 4,031

Net operating assets employed 2009

2)3,439 5,959 474 1,455 11,327 –181 11,146

Operating assets 2008

2)

5,963 6,077 628 2,068 14,736 398 15,134

Operating liabilities 2008

2,480 597 160 610 3,847 422 4,269

Net operating assets employed 2008

2)

3,483 5,480 468 1,458 10,889 – 24 10,865

1)

Calculated on the basis of units of 1,000 euros

2) Including goodwill at net book value

3) Including restructuring charges for the National Starch businesses of 44 million euros; the ongoing restructuring costs are charged to the regions

4) From 2009, corporate charges incurred with respect to regional business management are to be allocated to the individual regions; the prior-year figures have been

adjusted accordingly, which means the 2008 earnings result for the Europe/Africa/Middle East region is 44 million euros higher, while that of the other regions is lower:

by 23 million euros for North America, by 7 million euros for Latin America and by 14 million euros for Asia-Pacific

In the operating business sectors, affiliated companies lo–

cated in Germany, including the parent company, achieved

sales in 2009 of 1,909 million euros (2008: 2,020 million

euros) and reported intangible assets and property, plant

and equipment at December 31, 2009 of 1,087 million euros

(2008: 1,123 million euros).

The affiliated companies domiciled in North America re–

ported intangible assets, property, plant and equipment at

December 31, 2009 of 5,457 million euros (2008: 5,793 mil–

lion euros).

86 Annual Report 2009

Notes to the consolidated financial statements » Consolidated changes in intangible assets, property, plant and equipment and financial assets

Consolidated changes in intangible assets,

property, plant and equipment and financial assets

Cost

in million euros Intangible assets Property, plant

and equipment

Financial

assets

Total

At January 1, 2008 5,424 5,337 546 11,307

Changes in the Group /Acquisitions 3,3212) 342 3 3,666

Additions 20 473 66 559

Disposals1)

– 41 – 389 – 662 –1,092

Reclassifications 6 –6 – –

Translation differences –139 – 27 –1 –167

At December 31, 2009 8,897 5,613 26 14,536

1) of which assets held for sale 2009 – 41 – 46 – – 87

1) of which assets held for sale 2008 –1 –188 –12 – 201

2)

Adjusted following finalization of purchase price allocation relating to the acquisition of the National Starch businesses, see

page 87 et seq.

Accumulated amortization/depreciation

in million euros Intangible assets Property, plant

and equipment

Financial

assets

Total

At January 1, 2008 484 3,260 18 3,762

Changes in the Group /Acquisitions – – 4 –– 4

Write-ups – – – –

Scheduled amortization /depreciation 95 298 – 393

Impairment losses 4 149 3 156

Disposals1) – 63 – 347 – – 410

Reclassifications – – – –

Translation differences – 8 –14 – – 22

At December 31, 2009 679 3,365 6 4,050

1) of which assets held for sale 2009 – 37 – 32 – – 69

1) of which assets held for sale 2008 – –169 – 8 –177

Net book value

in million euros Intangible assets Property, plant

and equipment

Financial

assets

Total

At December 31, 2009 8,218 2,248 20 10,486

At December 31, 2008 8,4911) 2,361 24 10,876

1)

Adjusted following finalization of purchase price allocation relating to the acquisition of the National Starch businesses

The impairment losses are allocated to the relevant functions.

87

Annual Report 2009

General information

The consolidated financial statements of Henkel AG & Co.

KGaA have been prepared in accordance with International

Financial Reporting Standards (IFRS) as adopted by the

European Union.

The individual financial statements of the companies

included in the consolidation are drawn up on the same

accounting date as those of Henkel AG & Co. KGaA.

Members of the KPMG organization or other indepen–

dent firms of auditors instructed accordingly have either

audited the financial statements of companies included

in the consolidation or, in exceptional cases, conducted a

review of those financial statements. On January 29, 2010,

the Management Board of Henkel Management AG – the per–

sonally liable partner of Henkel AG & Co. KGaA – approved

the release of the consolidated financial statements to the

Supervisory Board. The Supervisory Board is responsible

for reviewing the consolidated financial statements and

declaring whether it approves them.

The consolidated financial statements are based on the

principle of historical cost with the exception that certain

financial instruments are accounted for at their fair values.

The Group currency is the euro. Unless otherwise indicated,

all amounts are shown in million euros. In order to im–

prove the clarity and informative value of the consolidated

financial statements, certain items are combined in the

consolidated balance sheet or in the consolidated statement

of income and shown separately in the Notes.

Scope of consolidation

In addition to Henkel AG & Co. KGaA, the consolidated finan–

cial statements at December 31, 2009 include nine domestic

and 202 foreign companies in which Henkel AG & Co. KGaA

has the power to govern the financial and operating policies,

based on the concept of control. This is generally the case

where Henkel AG & Co. KGaA holds, directly or indirectly, a

majority of the voting rights. Companies in which not more

than half of the shares are held are fully consolidated if

Henkel AG & Co. KGaA has the power, directly or indirectly,

to govern their financial and operating policies.

The composition of the Group has undergone only minor

change in the course of 2009 compared to the previous year.

Seven companies have been included in the consolidated

Group figures for the first time, 26 companies were merged

and 14 companies are no longer consolidated.

Acquisition of the National Starch businesses

On April 3, 2008, we acquired the Adhesives and Electron-

ic Materials divisions from the National Starch & Chemi–

cal Company following the takeover of the latter by Akzo

Nobel. The purchase price according to the contract dated

August 13, 2007, a so-called back-to-back agreement, was

3.7 billion euros (2.7 billion pounds sterling).

We valued and converted the acquisition of the Nation–

al Starch businesses using the closing rates of the date of

acquisition.

The allocation of the acquisition costs to the acquired

assets and liabilities (purchase price allocation) has now

been completed based on IFRS 3 “Business Combinations.”

The excess of the acquisition costs over the net book value of

the acquired assets and liabilities is 3,002 million euros.

The purchase price allocation process serves to assign

the acquisition costs to the fair values of the assets, liabili-

ties and contingent liabilities. Also taken into account in

this regard are the fair values of previously unrecognized

intangible assets assignable to the acquired activities,

such as customer relationships, technologies and brands.

It should be noted that purchase price allocation leads to

the recognition of hidden reserves and hidden charges

in the assets, liabilities and contingent liabilities of the

acquired businesses, and thus to additional expenses in the

form of accruing depreciation and amortization charges

against income.

The purchase price and thus the goodwill figure calcu-

lated following purchase price allocation primarily represent

anticipated synergies arising from the integration of the Na–

tional Starch businesses within the Henkel organization.

The table overleaf shows the reconciliation between the

purchase price and the goodwill figure after deduction of

the book values of the acquired assets and liabilities.

In November 2007, we entered into a cash flow hedge to

mitigate the currency risk attached to the purchase price

payable for the National Starch businesses. Settlement of

this transaction in April 2008 gave rise to a fair value of

–332 million euros. In compliance with the requirements of

International Accounting Standard (IAS) 39 “Financial Instru–

ments: Recognition and Measurement,” we have recognized

this amount as a deduction in Group equity and have also

deducted it from the purchase price as of April 3, 2008 in

calculating the excess of the acquisition costs over the net

book value of the acquired assets and liabilities.

Accounting principles and methods applied in

preparation of the consolidated financial statements

Notes to the consolidated financial statements » Accounting principles and methods applied in preparation of the consolidated financial statements

88 Annual Report 2009

The book values of the acquired assets and liabilities corre–

spond to the figures in the audited opening balance sheets

relating to the acquired activities as of April 3, 2008, to

which the accounting principles and methods of the Henkel

Group were applied:

Reconciliation of purchase price with

goodwill as of April 3, 2008

in million euros 2008

Purchase price

3,676

Purchase price adjustment based

Book values of the acquired

assets and liabilities

– 640

Provisional difference 3,002

Customer relationships

289

Technologies

215

Trademarks and brands

98

Other intangible assets

61

Other assets and liabilities

3

Deferred taxes

– 227

Goodwill 2,563

In the course of finalization of the purchase price allocation

in 2009, the goodwill figure rose by 99 million euros.

Other acquisitions and divestments

In April 2009, we acquired the remaining minority shares

in Henkel Alki, Tunisia. The purchase price was 8 mil lion

euros. In September 2009, we acquired the minority shares

in National Organic Kimyasaal in Turkey and merged

this company with Türk Henkel. The purchase price was

16 million euros. In November 2009, following the successive

purchase of further shares, we acquired Henkel Huawei in

China, raising our participating interest to 79.33 percent.

The purchase price was 4 million euros.

In May 2009, we sold the North American consumer

adhesives business under the Duck brand. The divestment

proceeds amounted to 79 million euros.

Consolidation methods

The purchase method is used for the consolidation of capi-

tal. This method stipulates that, for business combinations,

all hidden reserves and hidden charges in the company

acquired must be fully reflected at fair value and all iden-

tifiable intangible assets must be separately disclosed. Any

difference arising between the fair value of the net assets

and the purchase price is recognized as goodwill. Companies

acquired are included in the consolidation for the first time

by offsetting the carrying amount of the parent company’s

All receivables and liabilities, sales, income and expenses,

as well as intercompany profits on non-current assets or

inventories resulting from intra-group transactions, are

eliminated on consolidation. Intra-group transactions are

effected on the basis of market or transfer prices.

Currency translation

The financial statements of the consolidated companies,

including the hidden reserves and hidden charges of Group

companies recognized under the purchase method and

also goodwill arising on consolidation, are translated into

euros using the functional currency method outlined in

IAS 21 “The Effects of Changes in Foreign Exchange Rates.”

The functional currency is the main currency in which the

foreign company generates funds and makes payments. As

the functional currency for all the companies included in

the consolidation is the local currency of the company con–

cerned, assets and liabilities are translated at closing rates,

while income and expenses are translated at the average

rates for the year, based on an approximation of the actual

rates at the date of translation. The differences arising from

using average rather than closing rates are taken to equity

and shown as gains or losses recognized in equity, without

affecting net earnings.

Foreign currency accounts receivable and payable are

translated at closing rates. For the main currencies in the

Group, the following exchange rates have been used based

on one euro:

Notes to the consolidated financial statements » Accounting principles and methods applied in preparation of the consolidated financial statements

89

Annual Report 2009

Accounting estimates and assumptions

Preparation of the consolidated financial statements is

based on a number of accounting estimates and assump–

tions. These have an impact on the reported amounts of

assets, liabilities and contingent liabilities at the balance

sheet date and the disclosure of income and expenses for

the reporting period. The actual amounts may differ from

these estimates.

The accounting estimates and their underlying assump–

tions are continually reviewed. Changes in accounting es–

timates are recognized in the period in which the change

takes place where such change exclusively affects that

period. A change is recognized in the period in which it

occurs and in later periods where such change affects both

the reporting period and subsequent periods. The judgments

of the Management Board regarding the application of those

IFRSs which have a significant impact on the consolidated

financial statements are presented in the explanatory notes

on taxes on income (Note 9), intangible assets (Note 11),

pensions and similar obligations (Note 28), derivatives and

other financial instruments (Note 42) and share-based pay-

ment plans (Note 43).

Accounting standards not applied

in advance of their effective date

The following interpretations and revisions to existing stan–

dards of possible relevance to Henkel, which have since been

adopted into EU law (endorsement mechanism) but are not

yet mandatory, have not yet been applied:

» In January 2008, the International Accounting Standards

Board (IASB) issued a revised version of IFRS 3 “Business

Combinations” and of IAS 27 “Consolidated and Separate

Financial Statements.” IFRS 3 (2008) sets out new rulings

as regards the application of the purchase method in the

case of business combinations. Significant amendments

relate to the measurement of non-controlling interests,

the accounting treatment of step acquisitions, and the

treatment of contingent considerations and acquisition-

related costs that are to be expensed at the time they arise.

Significant amendments to IAS 27 (2008) relate to the re-

porting of transactions in respect of which the company

retains control, and transactions where control is ceded.

Transactions that do not lead to a loss of control must be

reported directly as equity transactions. Residual interests

are to be measured at fair value at the time of loss of con-

trol. The amendments are applicable for financial years

beginning after June 30, 2009, with early application of

both revised standards permitted.

» In July 2008, the IASB issued amendments relating to IAS 39

“Financial Instruments: Recognition and Measurement

– Eligible Hedged Items.” The amendments clarify the ap–

plication of hedge accounting to the inflation component

of financial instruments and to option contracts when

they are used as a hedging instrument. The amendments

are applicable for financial years beginning after June 30,

2009, with early application permitted.

» In October 2009, the IASB issued amendments to IAS 32

“Financial Instruments: Presentation.” The amendments

stipulate the accounting procedure with respect to the

issuers of stock rights, options and warrants for acquiring

a fixed number of equity instruments that are denomi–

nated in a currency other than the functional currency

of the issuer. Such cases were hitherto reported as deriva–

tive liabilities. Stock rights that are issued pro-rata at a

fixed currency amount to the existing shareholders of a

company are in future to be classified as equity. The cur–

rency in which the exercise price is stated is irrelevant.

The amendments are applicable for financial years begin–

ning on or after February 1, 2010, with early application

permitted.

Notes to the consolidated financial statements » Accounting principles and methods applied in preparation of the consolidated financial statements

Currency

Average exchange rate Closing exchange rate

ISO code 2008 2009 2008 2009

90 Annual Report 2009

» IFRIC 12 “Service Concession Arrangements” addresses

the issue of how companies that offer public services com–

missioned by local authorities are to report the rights and

obligations resulting from contractual agreements. The

interpretation is applicable for financial years beginning

after March 29, 2009, with early application permitted.

» IFRIC 15 “Agreements for the Construction of Real Estate”

addresses the accounting practice used by companies that

develop land and, in this capacity, sell buildings such as

houses and apartments before construction is complete.

The interpretation clarifies in particular when agreements

for the construction of real estate fall under the provisions

of IAS 11 “Construction Contracts” or IAS 18 “Revenue.” The

interpretation is applicable for financial years beginning af–

ter December 31, 2009 with early application permitted.

» IFRIC 16 “Hedges of a Net Investment in a Foreign Opera-

tion” clarifies that reporting of hedging instruments is

only possible between the functional currency of the for–

eign operation and the functional currency of the parent

entity. The hedged item can be the amount of net assets

of the foreign operation disclosed in the consolidated

financial statements. The hedging instrument can then

be held by any Group entity (except those of which the for–

eign currency risks are hedged). On disposal of the foreign

operation, the changes in value of the hedging instrument

recognized in equity and the foreign exchange gains or

losses of the foreign operation recognized in the currency

reserve are to be recycled from other comprehensive in–

come into the income statement. IFRIC 16 is applicable for

financial years beginning after June 30, 2009, with early

application permitted.

» IFRIC 17 “Distributions of Non-cash Assets to Owners” clari–

fies how non-cash assets distributed to owners of a com–

pany are to be reported. The amendments are applicable

for the beginning of the first financial year after October

31, 2009, with early application permitted.

» IFRIC 18 “Transfers of Assets from Customers” clarifies

how the transfer of assets or cash for the construction or

acquisition of property, plant or equipment from a cus–

tomer is to be reported. The amendments are applicable for

the beginning of the first financial year after October 31,

2009 at the latest.

All these standards and interpretations will be applied

by Henkel from fiscal 2010 or later. We expect the future

application of amendments to IAS 32, 39 and of IFRIC 12,

15, 16, 17 and 18 not to have a significant impact on the

presentation of the financial statements.

In fiscal 2009, the IASB issued the following standards or

interpretations of and amendments to standards of relevance

to Henkel which still have to be adopted into EU law (en–

dorsement mechanism) before they become applicable:

» Amendment to IFRS 2 “Share-based Payment”

» IFRS 9 “Financial Instruments”

» Amendments to IAS 24 “Related Party Disclosures”

» Collective standard “Annual Improvements to IFRSs”

» Amendment to IFRIC 14 “IAS 19 – The Limit on a Defined

Benefit Asset, Minimum Funding Requirements and their

Interaction”

» IFRIC 19 “Extinguishing Financial Liabilities with Equity

Instruments”

These interpretations and standards will be applied by

Henkel from fiscal 2010 or later. We expect the future appli–

cation of the aforementioned standards and interpretations

not to have a significant impact on the presentation of the

financial statements.

Notes to the consolidated financial statements » Accounting principles and methods applied in preparation of the consolidated financial statements

91

Annual Report 2009

Notes to the consolidated financial statements » Notes to the consolidated statement of income

(1) Sales and principles of income realization

Sales comprise sales of goods and services less sales deduc-

tions. Sales are recognized once the goods have been deliv-

ered or the service has been performed. In the case of goods,

this coincides with the physical delivery and transfer of risk.

It must also be probable that the economic benefits associ-

ated with the transaction will flow to the Group, and the

costs incurred in respect of the transaction must be reliably

measurable. Services are generally provided in conjunction

with the sale of goods and recorded once the service has

been performed. No sale is recognized if there are signifi–

cant risks relating to the receipt of the consideration or it

is likely that the goods will be returned.

Interest income is recognized on a time-proportion basis

that takes into account the effective yield on the asset and

the interest rate in force. Dividend income from investments

is recognized when the shareholder’s right to receive pay-

ment is established.

An analysis of sales by business sector and geographical

region is shown in the Group segment reports on pages 84

and 85.

(2) Cost of sales

(3) Marketing, selling and distribution expenses

In addition to marketing organization and distribution costs,

this item comprises mainly advertising, sales promotion

and market research costs. Also included here are the costs

of technical advisory services for customers and amounts

written off accounts receivable.

(4) Research and development expenses

Research expenses may not be recognized as an asset. De–

velopment costs are recognized as an asset if all the criteria

for recognition are met, the research phase can be clearly

distinguished from the development phase and the expendi–

ture can be attributed to distinct individual project phases.

Currently, the criteria set out in IAS 38 “Intangible Assets”

for recognizing development costs are not all being met, due

to a high level of interdependence within the development

projects and the difficulty of assessing which products will

eventually be marketable.

(5) Administrative expenses

Administrative expenses include personnel and non-person–

nel costs of Group management and costs relating to the Hu–

man Resources, Purchasing, Accounts and IT departments.

(6) Other operating income

Other operating income

in million euros 2008 2009

Gains on disposal of non-current assets

14 10

Profits on sale of businesses 8 –

fair value of operating derivative hedge transactions of 19 million euros

Effective fiscal 2009, the net loss on translation of operating

receivables and liabilities in foreign currency and the net

gain on measurement to fair value of operative derivative

hedging instruments are reported in the financial result, as

currency management is controlled centrally by Corporate

Treasury.

Profits on sale of businesses recognized in 2008 related

to the sale of our water treatment business. Sundry operat–

ing income refers to a number of individual transactions

from our operating business, for example payments on in-

surance claims, grants and subsidies, bonus credits and

similar income.

Notes to the

consolidated statement of income

92 Annual Report 2009

Notes to the consolidated financial statements » Notes to the consolidated statement of income

(7) Other operating charges

Other operating charges

in million euros 2008 2009

Write-downs of miscellaneous assets

4 –

Sundry operating expenses relate to a number of individual

transactions from our operating business, for example con–

Financial result

in million euros 2008 2009

Share of net profits of associates

83 –

Net result from other investments

in million euros 2008 2009

Income from other investments

3 1

Write-downs of shares in

non-consolidated affiliated

companies and investments

at amortized cost

– 3

–

Other

– 2 – 5

Total – 2 – 4

Net interest

in million euros 2008 2009

Interest and similar income

from third parties

54 47

Other financial income

37 23

Total interest income 91 70

147 million euros (2008: interest expense of 179 million euros and expected

interest income of 166 million euros)

Included in the total amount is the net result from the trans–

lation of accounts receivable and payable in the amount

of 22 million euros (2008: –101 million euros) and the net

result from the measurement to fair value of derivative

hedging instruments in the amount of –57 million euros

Earnings before taxes on income and analysis of taxes

in million euros 2008 2009

Main components of tax expense and income

in million euros 2008 2009

Current tax expense / income in the

reporting year

583 259

Increase / decrease in valuation

allowances on deferred tax assets

8 –13

In accordance with IAS 12 “Income Taxes,” deferred tax as-

sets and liabilities are recognized with respect to temporary

differences between the balance sheet valuation of an asset

or liability and its tax base, and with respect to consolida-

tion procedures affecting earnings. Deferred tax assets with

respect to unused tax losses and tax credits are measured

insofar as it is likely that sufficient taxable income will be

generated in future to realize the corresponding benefit.

Deferred taxes are calculated on the basis of the tax rates

that are applicable or anticipated in the individual countries

at the time of realization or utilization. In Germany there is

a uniform corporation tax rate of 15 percent plus a solidarity

liabilities related to the following items and unused tax

losses:

93

Annual Report 2009

Notes to the consolidated financial statements » Notes to the consolidated statement of income

Allocation of deferred taxes

in million euros Deferred tax assets Deferred tax liabilities

Dec. 31, 2008 Dec. 31, 2009 Dec. 31, 20081) Dec. 31, 2009

Intangible assets

127 144 665 643

Property, plant and equipment

37 24 86 84

Financial assets

69 29 4 6

Inventories

29 36 8 4

Other receivables and miscellaneous assets

62 56 107 94

The deferred tax assets amounting to 446 million euros

(2008: 409 million euros) reported under provisions result

primarily from recognition and measurement differences

with respect to pensions and similar obligations.

The deferred tax liabilities amounting to 643 million

euros (2008: 665 million euros) reported under intangible

assets can be attributed chiefly to business combinations

such as the acquisition of the National Starch businesses

in 2008.

The valuation allowances on deferred tax assets of

62 million euros (2008: 60 million euros) are in respect of

temporary differences between the balance sheet valuation

of an asset or liability and its tax base, and are based on a

reassessment of future utilization.

Deferred taxes have not been recognized with respect

to unused tax losses of 347 million euros (2008: 358 mil–

lion euros), as it is not sufficiently probable that taxable

profit will be available against which they may be utilized.

Deferred taxes of 14 million euros (2008: 2 million euros)

have been recognized with respect to tax credits.

A deferred tax income of 78 million euros was recog–

nized directly in equity (2008: tax expense of 55 million

euros). This deferred tax income results in the amount of

70 million euros from actuarial losses with respect to pen-

sion obligations of 355 million euros, and in the amount

of 8 million euros from losses from cash flow hedges of

19 million euros.

The table below summarizes the expiry dates of un–

used tax losses and tax credits. This table includes unused

tax losses arising from the disposal of assets amounting

to 11 million euros (2008: 9 million euros) which may be

carried forward without restriction. In many countries,

different tax rates apply to losses on the disposal of assets

and to operating profits, and in some cases losses on the

disposal of assets may only be offset against profits on the

disposal of assets.

Expiry dates of unused tax losses and tax credits

Unused tax losses Tax credits

Dec. 31, 2008 Dec. 31, 2009 Dec. 31, 2008 Dec. 31, 2009

Must be utilized within

1 year

37 36 – –

2 years

32 63 – –

94 Annual Report 2009

Notes to the consolidated financial statements » Notes to the consolidated statement of income

The individual company reconciliations – prepared on the

basis of the tax rates applicable in each country and taking

into account consolidation procedures – have been sum–

marized in the statement below. The estimated tax charge,

based on the tax rate applicable to Henkel AG & Co. KGaA of

31 percent, is reconciled to the tax charge disclosed.

Calculation of the tax charge disclosed

in million euros 2008 2009

Earnings before taxes on income

1,627 885

Tax rate (including trade tax) on income

of Henkel AG & Co. KGaA

31 %

31 %

Estimated tax charge 504 274

Tax increases/reductions due

to differences between local tax

Effects of different tax rates

on net result from investments

(at-equity investments)

– 25 –

Tax increases/reductions due to

tax-free income and other items

– 22 – 22

Tax increases/reductions due to

non-deductible expenses and

other items

52 74

of which

Non-deductible write-down

of intangible assets

– 14

Trade tax additions

10 13

Non-deductible withholding tax

14 14

Other non-deductible expenses

28 33

Tax effect of sale of Ecolab shares

– 43 –

Tax charge disclosed 394 257

Effective tax rate 24.22 % 29.04 %

The increase in the effective tax rate in 2009 to 29.04 per–

cent (2008: 24.22 percent) can be attributed inter alia to the

non-deductible write-down of intangible assets and to the

absence of the effect resulting from the at-equity stake in

Ecolab (in 2008: –1.5 percentage points). The normalized

effective tax rate for 2009 is 27.5 percent.

Deferred tax liabilities have not been recognized on the

retained profits of foreign subsidiaries. The retained profits

are available to the subsidiaries for further investment.

(10) Minority interests

The amount shown here represents the share of profits and

losses attributable to minority shareholders.

95

Annual Report 2009

Notes to the consolidated financial statements » Notes to the consolidated balance sheet

Non-current assets

All non-current assets with definite useful lives are amor–

tized or depreciated using the straight-line method on the

basis of estimated useful lives standardized throughout

Useful life

in years

Intangible assets with definite useful lives 3 to 20

Residential buildings 50

Office buildings 40

(11) Intangible assets

Cost

in million euros Trademark rights and other rights

Assets with

indefinite

useful lives

Assets with

definite

useful lives

Internally generated

intangible assets with

definite useful lives

Goodwill

Total

At January 1, 2008 1,057 852 123 3,392 5,424

Changes in the Group/Acquisitions 86 597 – 2,638

2)

3,321

Additions – 10 10 –

20

Disposals1) – – 41 – – – 41

Reclassifications – 5 7 4 –

6

Translation differences 63 43 –1 192

297

At December 31, 2008/

January 1, 2009 1,201 1,468 136 6,222

2) 9,027

Changes in the Group/Acquisitions – – –1 40

39

Additions – 11 16 1

28

Notes to the consolidated balance sheet

The accounting policies for balance sheet items are described in the relevant Note.

96 Annual Report 2009

Notes to the consolidated financial statements » Notes to the consolidated balance sheet

Accumulated amortization

in million euros Trademark rights and other rights

Assets with

indefinite

useful lives

Assets with

definite

useful lives

Internally generated

intangible assets with

definite useful lives

Goodwill

Total

At January 1, 2008 4 457 23 – 484

Changes in the Group/Acquisitions – – – – –

Write-ups – – – – –

Scheduled amortization – 78 17 – 95

Impairment losses – 4 – – 4

Disposals – – 39 – – – 39

Reclassifications – – – – –

Translation differences – – 8 – – – 8

Net book value

in million euros Trademark rights and other rights

Assets with

indefinite

Assets with

definite

Internally generated

intangible assets with

Goodwill

Total

Trademarks and other rights acquired for valuable consider–

ation are stated initially at acquisition cost, while internally

generated software is stated at production cost. Thereafter,

goodwill and trademark rights and other rights with in–

definite useful lives are subject to an impairment test at

least once a year (impairment-only approach). In the course

of our annual impairment test, we reviewed the carrying

values of goodwill and trademark rights and other rights

with indefinite useful lives. The following table shows the

cash-generating units together with the associated goodwill

and trademark rights and other rights with indefinite useful

lives at book value at the balance sheet date.