Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

57

Annual Report 2009

Group management report » Sustainability / Corporate social responsibility

corruption. Our understanding of socially responsible behav-

ior has been specified and communicated to our employees

throughout the entire Group through our Code of Corpo-

rate Sustainability and our Code of Conduct. From these

codes are derived our more detailed internal SHE standards

(governing safety, health and environmental protection),

our social standards and our Group purchasing standards.

Compliance with these rules and requirements is regularly

monitored throughout the Group by Internal Audit. In ad-

dition, Henkel companies have their management systems

externally certified. As of the end of 2009, 58 percent of

our production volume was generated at sites certified in

accordance with the international environmental manage-

ment standard ISO 14001.

As a responsible corporate citizen, Henkel provides

financial and in-kind support for activities aligned to social

needs, the environment, education, science, health, sport,

art and culture. Since 1998, we have also actively supported

the volunteer work performed by our employees and retirees

through our MIT Initiative (Make an Impact on Tomorrow).

In 2009, we supported a total of 1,143 charitable MIT projects

in 76 countries, of which 349 were children-related.

Future-capable solutions promoting sustainability can

only be developed in dialogue with all social groups. In order

to be able to consider and evaluate the interests of the vari-

ous parties involved, we constantly seek dialogue with our

stakeholders at the local, regional and international level.

These include our employees, shareholders, customers and

suppliers, public authorities, politicians, associations and

non-governmental organizations as well as representatives

of academia, the sciences and the public at large.

We deploy a wide range of communication instruments

in order to meet the specific information requirements of

our stakeholders. More details and background information

on the subject of sustainability including our value added

statement can be found in our Sustainability Report. With

this, we document the high priority assigned to the prin-

ciples of sustainable development by our company, at the

same time satisfying the reporting obligations laid down

in the United Nations Global Compact.

Further information, reports, background details and

the latest news on sustainable development at Henkel can

be found on our website www.henkel.com/sustainability.

» To reduce waste per ton of output by a further 10 percent

» To reduce occupational accidents per million hours worked

by a further 20 percent

Again in the year under review, we were able to improve

our sustainability performance on a number of important

points. For example, the savings we have made with respect

to energy consumption have helped to mitigate the effect

of rising energy prices. Further, the associated reduction in

carbon dioxide emissions contributes to the achievement

of climate protection targets.

In addition to optimizing our own production processes,

we focus particularly on the development of products and

technologies that save energy in the use phase – for the ma-

jority of the energy consumption and the associated carbon

dioxide emissions occur once our products have been sold

and put into use. One example is laundry detergent. Energy

savings made by washing at low temperatures can make an

important contribution to climate protection. Appropriate

methods of measurement have yet to be developed in order

to communicate these contributions in a persuasive and

credible manner, and this is an area in which we are keen

to drive progress forward. We are therefore currently taking

part with products from all three of our business sectors

in the “Product Carbon Footprint” pilot project with full

participation in the national and international dialogue

relating to this issue.

Organization and dialogue

The Henkel Management Board bears overall responsibility

for our sustainability policy. Our Sustainability Council

steers our global sustainability activities in collaboration

with our operating business sectors, our corporate functions

and our regional and national companies.

By joining the United Nations Global Compact in July

2003, we publicly underscored our commitment to respect

human rights and fundamental labor standards, to promote

environmental protection and to work against all forms of

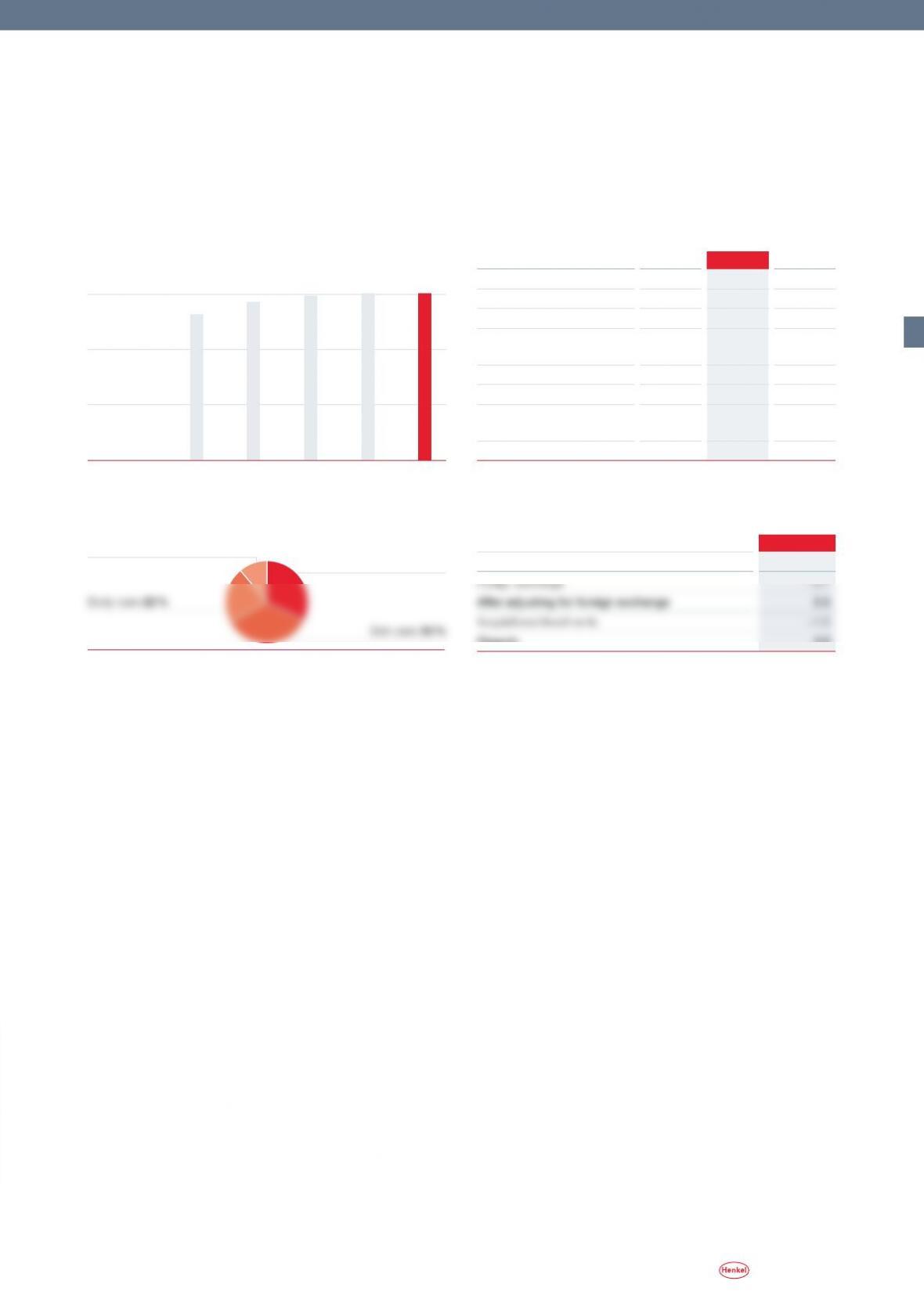

Sustainability performance 2005 to 2009

Environmental indicators per ton of output

Energy consumption – 26 %

Waste – 37 %

Water consumption –12 %

Occupational accidents1)

– 57 %

1) Per million hours worked

Group management report » Laundry & Home Care

Purex is the USA’s number one in the rapidly growing segment of mid-priced liquid laundry detergents. Now Purex

Complete 3-in-1, launched in 2009, has also been enthusiastically received by retailers and consumers alike. This

innovation combines the performance of detergents and softeners with an anti-static compound to prevent wash

static in the drier. And it was developed by the interdisciplinary team pictured here in Scottsdale, Arizona, USA.

From the left:

Thomas Britt Keith Cardinal Katherine Yu Stephen Koven Jack Hudson Margaret Heyer Kristopher Stathakis

Director –

Supply Chain

Manager,

Package Engineering –

Laundry Care

Senior Scientist –

Product Research

and Development

Brand Manager –

Laundry Care

Engineering Fellow –

Process Development

Manager, Contract

Manufacturing –

Supply Chain

Senior Project

Manager –

Supply Chain

59

Annual Report 2009

Group management report » Laundry & Home Care

Laundry & Home Care

Sales development

in percent 2009

Change versus previous year –1.0

Foreign exchange

– 3.9

After adjusting for foreign exchange 2.9

Acquisitions/divestments

0.0

Organic 2.9

Key financials1)

in million euros 2008 2009 +/–

Sales 4,172

4,129

–1.0 %

Proportion of Henkel sales 30 %

30

%

0.0 pp

Operating profit (EBIT) 439

501

14.0 %

Adjusted operating

profit (EBIT)

2) 450

530

17.8 %

Return on sales (EBIT) 10.5 %

12.1

%

1.6 pp

Adjusted return on sales (EBIT)

2) 10.8 %

12.8

%

2.0 pp

Return on capital employed

(ROCE)

16.9 %

19.6

%

2.7 pp

EVA®166

232

39.8 %

1) Calculated on the basis of units of 1,000 euros

2) Adjusted for one-time charges/gains and

restructuring charges

pp = percentage points

e

» Organic sales growth of 2.9 percent

» Adjusted operating profit improved to 530 mil-

lion euros

» Adjusted EBIT margin increased by 2.0 percentage

points to 12.8 percent

Economic environment and market position

The volume of the world market for laundry and home care

products in 2009 amounted to around 91 billion euros. The

markets of relevance to Henkel remained robust, expand-

ing slightly despite the difficult world economic situation.

Once again, market growth from a world perspective was

more price than volume-driven. In the course of the year,

however, price levels came under pressure as the general

economic climate deteriorated.

Western Europe saw a moderate expansion in the market

for detergents and household cleaners in the year under

review. The economic slump caused uncertainty among

consumers. This led to increased price sensitivity and, as

a result, a rise in the market share of private labels and

also an increase in the share of the market attributable to

discounters. Despite these rather unfavorable competitive

conditions for brand manufacturers, we were able to main-

tain our leading position in the overall Western European

market.

Many countries in Eastern Europe were unable to repeat

the double-digit percentage growth rates exhibited in previ-

ous years, reflecting particularly clearly the impact of the

global economic and financial crisis. This had the effect

of restricting growth and appreciably influenced the pur-

chasing behavior of consumers. In this challenging market

environment, we nevertheless succeeded in expanding our

market share and further reducing the gap to our biggest

competitor.

In the growth regions of Africa/Middle East, Latin Amer-

ica and Asia, the markets of relevance to us underwent, in

some cases, double-digit growth rates. And with our strong

market position, we were able to benefit from the dynamic

developments encountered in the Middle East and also in

North Africa.

The laundry and home care market in North America

remained generally stable last year, albeit with a mixed set of

developments across the individual categories. While we no-

ticed a small degree of growth in the detergents market, sales

4,000

3,000

2,000

1,000

4,129

4,172

4,088 4,117 4,148

2009

2008200720062005

0

Sales

in million euros

Detergents 53 %

World market for laundry and home care products

Insecticides 6 %

Air fresheners 6 %

Cleaning products 35 %

as a whole. Our local brands offering high inherent brand

identity in terms of positioning, formulation and packaging

are being more closely associated with these focus brands.

This enables us to generate synergies in both production

and in our advertising investments. Through this strategy,

our ten top brand clusters account for almost 80 percent

of our sales, effectively utilizing both the strength of our

international brand concepts and those of our well estab-

lished local brands.

Sales and profits

Sales nominally decreased by 1.0 percent to 4,129 million

euros in the year under review. In organic terms – i.e. after

adjusting for foreign exchange and acquisitions/divestments

– sales growth came in at 2.9 percent. In 2009, this organic

improvement in sales was due exclusively to higher pricing

levels, while volumes sold underwent a slight decline.

In the regional breakdown, the main increase in sales

achieved was in Europe/Africa/Middle East. We posted

double-digit organic sales growth both in Eastern Europe

and in Africa/Middle East. And sales underwent particu-

larly significant expansion in Russia and Egypt, with our

market positions in those countries further expanding. In

Western Europe, on the other hand, we were unable to quite

reach the sales level of the previous year in volume terms,

although the average revenue generated by our products

rose substantially. The contributory factors in this regard

were the price increases implemented at the end of the

previous year, and new product launches that enabled us

to successfully combat the rise in demand for cheap own

labels. In Latin America, we were able to substantially in-

crease organic sales and expand our market position. Our

sales performance in Asia was affected by our exit from

the Chinese market at the end of 2008. After adjusting for

this exceptional circumstance, sales in Asia underwent a

gratifying increase, with our entry into the South Korean

laundry care market yielding very promising initial results.

In addition to our position as market leader in the supply

of household insecticides, we have also been present in

the South Korean market since the fourth quarter of 2009

with our biggest international laundry brand Persil, which

is already enjoying a high level of retailer acceptance. Our

business in North America remained stable overall. Here we

celebrated a major market success in the form of our innova-

tion Purex Complete 3-in-1. These groundbreaking laundry

volumes in the household cleaners market decreased slightly.

With our detergent brand Purex, we were able to expand our

market position through the launch of new products such

as Purex Complete 3-in-1, providing us with a good position

as competition became increasingly price-driven.

Business activity and strategy

The business sector is globally active in the marketing, sell-

ing and distribution of branded products for the laundry and

home care markets. The Laundry segment includes not only

heavy-duty and specialty detergents but also fabric softeners,

laundry performance enhancers and laundry care products.

The portfolio of our Home Care segment encompasses clean-

ers for bath and WC applications together with household,

glass and specialty cleaners. We also manufacture hand and

machine dishwashing products and have a market presence

in selected regions with air fresheners and insecticides.

Our objective is to further promote profitable growth by

driving the organic expansion of our continuing operations.

To this end, we intend over the medium term to further ex-

pand the share of sales accounted for by our growth regions

from the strong and profitable platform provided by our

positions in Western Europe and North America. Specifi-

cally, our aim is to harness the dynamics of the emerging

economies, increase our market shares in the countries

concerned and raise profitability to the high level of the

more mature regions. We are endeavoring to further extend

our leading market positions in Eastern Europe and North

Africa. In our other growth regions, we intend to further

reduce the gap to the current market leaders.

The year under review demonstrated that successful

innovation can make a significant contribution to profit-

able growth, particularly in economically difficult times.

Consequently, it remains our objective to achieve and main-

tain over the long term a high innovation rate of around

40 percent and to consolidate and expand our innovation

leadership in our markets. With thorough, efficient con-

trol of the entire innovation process, we are able to quickly

identify and harness consumer trends and convert them

into products. We are also continuously reviewing our ex-

isting supply portfolio, responding to changing consumer

needs by adapting our product range. For this, we pursue

a “brand cluster” strategy in which our main focus is on

our major international brands and on promoting their

continuing disproportionate growth versus our portfolio

Group management report » Laundry & Home Care

60 Annual Report 2009

61

Annual Report 2009

to further consolidate our market positions with double-

digit growth rates in many countries. In the market for

machine dishwashing detergents in Western Europe, we

launched Somat 9, once again exemplifying our innova-

tive strengths by extending the integral functions with an

odor neutralizer and an extra-dry effect. In the case of our

WC products, we achieved our highest growth in Eastern

Europe, increasing our market share overall with the aid

of new products such as Bref WC Tornado Gel: once the

gel makes contact with water, a powerful cleaning foam is

produced that extends around the toilet bowl, exerting a

self-acting cleaning effect.

Capital expenditures

Our investments in the year under review were primarily

geared to optimizing and rationalizing our production pro-

cesses. Further capital expenditures were assigned to the

field of plant safety. In total, we invested 151 million euros

in property, plant and equipment, compared to 163 mil-

lion euros in the previous year. This decrease is due to the

completion of a number of special projects in 2008.

Outlook

We expect the laundry and home care markets of relevance

to us to exhibit a slight decline in their growth dynamics in

2010. In North America and Western Europe particularly,

we anticipate that market expansion will be no more than

minor, while competition is expected to remain intense.

The anticipated rise in sales will therefore be generated by

our growth regions.

Within this environment, we intend to expand our

market positions in 2010 and to once again outperform

our relevant markets in terms of organic sales growth. We

also expect a slight increase in adjusted operating profit

compared to prior year.

We see opportunities arising from a revival in demand in

Western Europe and North America, a continuation in the

sales dynamics exhibited by the growth regions, and in the

successful launch of innovations. There is a risk that the pro-

pensity to consume could significantly decline, for example

as a result of a rapid rise in unemployment. We also see risks

arising from increasing competition and promotional pres-

sure in today’s already highly competitive markets. Added

to this is the uncertainty of commodity price developments,

which will depend on the world economic situation.

sheets combine the performance of a laundry detergent and

fabric softener while at the same time preventing the wash

load from becoming charged with static in the drier.

We increased our operating profit (EBIT) by 14.0 percent

to a new record high of 501 million euros. After adjusting

for foreign exchange, the rise was an even more respectable

19.3 percent. Reflected in this result are, in addition to sell-

ing price stability as compared to the end of the previous

year, our successful measures aimed at reducing cost and

enhancing efficiency, plus a decline in our raw material

prices. In order to support our new product launches and

as a contra-cyclic response to the difficult overall economic

situation, we substantially increased our advertising invest-

ments last year. At 12.1 percent, return on sales reached a

new record level, improving by 1.6 percentage points. Return

on capital employed (ROCE) also exhibited a substantial rise

of 2.7 percentage points to 19.6 percent, due in particular

to the improvement in the management of our net work-

ing capital.

Business segments

In the Laundry business segment, the greatest growth mo-

mentum in the year under review came from our heavy-

duty detergents and fabric softeners. In regional terms, the

main boost to growth was from our heavy-duty detergents

in Europe/Africa/Middle East, with double-digit growth rates

having been achieved in a number of countries of Eastern

Europe and the Middle East. We also succeeded in expanding

the market share of our heavy-duty detergents in Western

Europe, with benefits accruing from our successful innova-

tions in this category. We launched new Persil ActicPower

in a number of countries of Western Europe. This product

requires only half the usual detergent dosage and develops

its full laundry power at just 15 degrees Celsius. Our fabric

softeners saw sales increase primarily in Eastern Europe. We

were able to generate additional sales and increase market

share through the launch of Vernel Crystals – innovative

fragrance crystals for the wash – and new fragrance variants

for our Vernel and Silan brands.

The main contributors to the organic sales growth regis-

tered by our Home Care segment were our dishwashing deter-

gents and WC products. While sales in machine dishwashing

products increased particularly in Eastern Europe, hand

dishwashing product sales achieved their highest growth

rates in the Africa/Middle East region. Here, we were able

Group management report » Laundry & Home Care

Group management report » Cosmetics / Toiletries

In 2009, Schwarzkopf – the Henkel brand that generates the company’s highest revenue – celebrated 111 years

of quality, competence and innovation in hair cosmetics. Our experts in colorants are constantly developing

fascinating hair colors for consumers and stylists alike.

From the left:

Nicola delli Venneri Dr. Astrid Kleen Marie-Eve Schroeder Renate Simon-Florek Dr. Mustafa Akram Anett Kaplan

International Production

and Packaging

Development

International Research

and Development –

Colorants

International Marketing –

Colorants, Consumer

Business

International Marketing –

Colorants, Salon Business

International Research

and Development –

Colorants

International Marketing –

Colorants, Consumer

Business

63

Annual Report 2009

Group management report » Cosmetics / Toiletries

Kosmetik /KörperpflegeCosmetics / Toiletries

Key financials1)

in million euros 2008 2009 +/–

Sales 3,016

3,010

–0.2 %

Proportion of Henkel sales 21 %

22

%

1.0 pp

Operating profit (EBIT) 376

387

3.1 %

Adjusted operating

profit (EBIT)

2) 379

387

2.1 %

Return on sales (EBIT) 12.5 %

12.9

%

0.4 pp

Adjusted return on sales (EBIT)

2) 12.6 %

12.9

%

0.3 pp

Return on capital employed

(ROCE)

17.5 %

18.2

%

0.7 pp

EVA®150

164

9.3 %

1) Calculated on the basis of units of 1,000 euros

2) Adjusted for one-time charges/gains and

restructuring charges

pp = percentage points

e

» Organic sales growth of 3.5 percent

» Adjusted operating profit increased to 387 mil-

lion euros

» Adjusted EBIT margin increased by 0.3 percent-

age points to 12.9 percent

Economic environment and market position

The world cosmetics market of relevance to us was valued in

2009 at 135 billion euros, representing a slight decline due

to the world economic situation. The regional developments

observed were very mixed. Our core markets in Western

Europe and North America experienced a decline overall,

particularly with respect to retail hair cosmetics. Neverthe-

less, we succeeded in generating disproportionate growth

and in achieving significant market share increases. We

substantially expanded our already strong market positions

in Western Europe on the back of positive developments in

hair cosmetics and body care. And in North America, we

were able to effectively enhance our position in the core

segments of styling and body care.

The markets in Eastern Europe, the Africa/Middle East

region and Asia-Pacific continued to exhibit above-aver-

age growth, and we were able to generate disproportionate

expansion in these regions, gaining significant market

share.

The hair salon market was heavily impacted worldwide

by the economic crisis, undergoing a substantial decline in

activity. Within this difficult market environment, Schwarz-

kopf Professional was nevertheless able to successfully main-

tain its market share and strengthen its position as the

global number three.

The Cosmetics/Toiletries business sector holds leading

positions in the markets of relevance to us around the world

and was again able to substantially expand its market shares

in the year under review.

Business activity and strategy

The Cosmetics/Toiletries business sector is active both in

the branded consumer goods segments of hair cosmetics,

body care, skin care and oral care, and in the professional

Sales development

in percent 2009

Change versus previous year – 0.2

Organic 3.5

3,000

2,000

1,000

3,010

3,016

2,629

2,864 2,972

2009

2008200720062005

0

Sales

in million euros

Oral care 11 % Hair cosmetics &

salon products 32 %

Skin care 35 %

World market for cosmetics and toiletry products

64 Annual Report 2009

Group management report » Cosmetics / Toiletries

bound environment. In nominal terms, sales decreased by

0.2 percent to 3,010 million euros due to negative foreign

exchange effects and the divestments in North America.

The improvement in organic sales achieved in 2009 was due

not just to higher price levels but also primarily to positive

volume expansion.

The main contributors to organic growth were the suc-

cessful development of our branded consumer goods busi-

ness in Eastern Europe, with good performances also being

posted in the regions of Africa/Middle East, Latin America

and Asia-Pacific. In Western Europe too, we achieved en-

couraging results despite the recessive environment, and

in North America we outperformed the market.

Sales of our hair salon business were below the level of

the previous year, although developments were significantly

better than those of the overall market.

At 387 million euros, operating profit (EBIT) was 3.1 per-

cent above the prior-year level. After adjusting for foreign

exchange, operating profit rose by 6.3 percent compared to

the previous year. Systematic cost reduction measures, selec-

tive price increases and a further reduction in complexity

led to an improvement in our cost structures. Return on

sales rose by 0.4 percentage points compared to the previous

year, attaining a new record level of 12.9 percent.

We increased return on capital employed (ROCE) by

0.7 percentage points to 18.2 percent. This was helped not

only by the increase in profitability but also by the sub-

stantial reduction in capital employed arising from strict

management of our net working capital.

Business segments

In our Hair Cosmetics business, we succeeded in achieving

a significant organic increase in sales to new record levels

accompanied by a corresponding expansion in our market

shares.

We were able to further improve our market position

through the early and successful launch of some top inno-

vations in all segments, aligned to the changing require-

ments of consumers in this time of economic crisis. The

main growth drivers were our Hair Care and Colorants

businesses.

In the case of Hair Care, we saw our market shares reach

new record levels, with the highly successful international

launch of our Syoss brand making a notable contribution.

The Gliss Kur brand further strengthened its European mar-

ket share as a result of the launch of the Asia Straight and

hair salon business. Our strategy to expand our branded

consumer goods operations is focused on strengthening our

market positions in Western Europe and North America, in

Eastern Europe, the Middle East and other specific growth

markets. In the hair salon business, we are continuing to

pursue our globalization strategy and aiming to generate

growth particularly in Asia-Pacific, Latin America and the

Middle East.

The achievement of organic expansion lies at the focus

of our growth strategy, which we are implementing through

the development of innovative products and their rapid

launch. We also aim to complement our organic sales growth

through the acquisition of carefully selected businesses. As

part of our active style of portfolio management, we regu-

larly review our business activities. Hence, for example, we

sold our marginal amenities and chemical products busi-

ness in conjunction with the disposal of our US cosmetics

plant in Aurora, Illinois. And in July 2009, we concluded the

sale of the Agree brand. We also discontinued a number of

further minor brands.

In our branded consumer goods business, our focus is

on the international expansion of our core segments of Hair

Cosmetics, Body Care, Oral Care and Skin Care. The emphasis

of our strategy is on further developing our leading core

brands. With this concentrated portfolio management ap-

proach, our ten top brands again made a disproportionate

contribution to sales in 2009, accounting for more than

87 percent of the business sector’s revenues. And we intend

to follow this dynamic and profitable growth path in the

future through our proactive innovation strategy and dedica-

tion to consistently strengthening our brand equities. Our

current innovation rate lies in the region of 40 percent,

helped by harnessing the additional growth potential avail-

able from strategic partnerships with our customers.

We want to drive forward our hair salon business with

further product innovations, and with efficient sales and

distribution structures. And additionally, we will be looking

to develop new regional potential on a selective basis.

Our aim is to consistently improve our profitability

through the consistent expansion of our core businesses

and core competences.

Sales and profits

With organic sales growth of 3.5 percent, the Cosmetics/

Toiletries business sector was able to continue the very

good growth of the previous years, despite the recession-

65

Annual Report 2009

Group management report » Cosmetics / Toiletries

Despite the difficulties of the market environment, we were

able to further expand the position of our Hair Salon segment

innovation leader, particularly in the core categories of color

and care. The Bonacure relaunch with Amino Cell Rebuild

Technology once again underlined Bonacure’s claim as one

of the fastest growing and most innovative care brands. The

focus in the colorants category was on the launch of Igora

Color 10, the first salon colorant that takes just ten minutes

to apply, and Essensity – the first colorant without ammonia,

fragrance, silicones and preservatives to offer permanent

performance combined with 100 percent gray coverage.

Capital expenditures

The emphasis of our investment activity was on measures

designed to optimize our structures and production pro-

cesses. In all, we spent 40 million euros on property, plant

and equipment compared to 84 million euros in the previous

year. The decrease is due to the completion of a number of

special projects in 2008.

Outlook

With the market environment remaining difficult, we ex-

pect 2010 to bring a further slowdown in the growth dy-

namics of the world cosmetics market of relevance to us.

We expect sales momentum to emanate from the growth

regions of Eastern Europe, Latin America, Africa/Middle

East and Asia-Pacific.

In terms of organic sales growth, our aim is once again

to outperform our relevant markets. We further expect a

slight increase in adjusted operating profit compared to

the previous year.

Our opportunities lie primarily in the further expan-

sion of our market positions in Europe and North America,

driven by the focused pursuit of our innovation offensive,

and in extensively utilizing the potential that lies in our

growth regions. The further expansion of our Schwarzkopf

megabrand is of key importance in this regard.

Risks lie in the possibility of an increasing deterioration

in the consumer climate in the face of rising unemployment.

We expect the intensity of competition to remain persis-

tently high, and that this will be manifested in continuous

promotional pressure and high advertising expenditures.

Further rising raw material and packaging prices may also

increase the pressure on margins.

Hair Active lines. We were also able to strengthen the lead-

ing position of our Schauma brand through the launch of

In the Colorants business, the introduction of, in par-

ticular, the brand Schwarzkopf Essential Color – a perma-

nent colorant without ammonia – generated market share

growth. We were also able to increase the market share

enjoyed by Palette, the market leader in Europe, with Pal-

ette Deluxe and the ten-minute colorant Palette 10. In the

case of our Brillance brand, the focus was on expanding

the range through the introduction of Brillance Intense

Couleur. The colorant Diadem was enriched with the active

ingredient Q10.

Against a background of contracting markets, our Styling

business likewise made significant gains in market share.

We consolidated the growth of Taft, the market leader in

the European styling segment, through the launch of Taft

Ultra with Silk Touch, and also Taft Maxx Power Styling Gel.

And our “young fashion” brand Got2b gained further posi-

tive momentum through the introduction of “superkleber”

[superglue] and “guardian angel.”

The 2009 innovation program was supported by mea-

sures celebrating the 111th anniversary of the Schwarz-

kopf brand, including a raft of special media and customer

events.

The Body Care segment likewise continued to perform

well. The core brands Fa and Dial successfully maintained

their innovation offensive. The launch of the Fa Cream &

Oil series with valuable care oils and the introduction of

the men’s variant Extreme Cool led to an increase in market

shares across Europe. There was a substantial rise in Dial

sales resulting from the launch of Dial Antioxidant with

Cranberry and Dial 3D Odor Defense. Right Guard also made

significant inroads in the US American deodorant market

with Right Guard Fast Break.

In the Skin Care business, the introduction of Diader-

mine’s Dr. Caspari Method Dermo-Ident treatment contrib-

uted to further consolidation of the position enjoyed by

Diadermine in the rapidly growing anti-aging segment. The

Chinese child skin care series Haiermian exhibited double-

digit percentage sales growth as a result of the introduction

of innovative products in that line.

In the Oral Care business, we likewise achieved good re-

sults with the new freshness variant Theramed 2-in-1 Arctic

White.

Group management report » Adhesive Technologies

The worldwide activities of the Packaging, Consumer Goods and Construction Adhesives segment of the Adhesive

Technologies business sector are presented and decided upon in team sessions. Included in these discussions is the

segment’s best selling brand, Dispomelt. Here we see the global management team at a meeting in Bridgewater,

New Jersey, USA.

Sitting, from the left:

Steven Essick Jerry Perkins Jean Chesterfield Jürgen Convent Jean Fayolle Bjoerk Ohlhorst

Head of Finance

Head of North

America

European HR

Key Account Manager

Head of Marketing &

Innovation

Head of Packaging,

Consumer Goods and

Construction Adhesives

Global Purchasing

Key Account Manager –

Adhesive Technologies

Standing, from the left:

Ray Di Muzio Jörg Raichle Thomas Auris Gary Raykovitz Ellen Greenhorn Julio Muñoz Kampff

Head of Global

Operations

Head of Controlling,

Asia-Pacific –

Adhesive Technologies

Head of Asia-Pacific

Head of Global Product

Development

Marketing Head of Adhesive

Technologies,

Latin America

67

Annual Report 2009

Group management report » Adhesive Technologies

Adhesive Technologies

Key financials1)

in million euros 2008 2009 +/–

Sales 6,700

6,224

– 7.1 %

Proportion of Henkel sales 47 %

46

%

–1.0 pp

Operating profit (EBIT) 658

290

– 55.9 %

» Decline in organic sales of 10.2 percent

» Adjusted operating profit of 506 million euros

» Adjusted EBIT margin of 8.1 percent

Economic environment and market position

Fiscal 2009 was characterized by the economic and financial

crisis that gripped the world, exerting a negative impact on

all the sales markets of the Adhesive Technologies business

sector. There was a significant decline in production, particu-

larly in the steel, automotive and electronics industries. The

capital goods sector and the construction industry likewise

registered heavy contraction. Private consumption also suf-

fered from the consequences of the economic crisis, yet as-

sumed the role of economic stabilizer. The effects of the situ-

ation were particularly noticeable in the developed regions

of North America, Western Europe and Japan. The picture

in the growth regions was mixed: although some countries

in Asia and Eastern Europe suffered from the effects of the

crisis, China and India proved to be more robust as the year

unfolded. With the exception of Mexico, Latin America was

also less adversely affected by the market downturn.

In this exceptionally difficult economic climate, the market

of relevance to us for adhesives, sealants and surface treat-

ment technologies exhibited disparate developments. In the

first half of the year particularly, we had to cope with – in

some cases – substantial decreases in sales in individual

market segments, while other segments and regions were

less impacted. Overall, we benefited from the high level of

diversification inherent in our business portfolio. We are

convinced that the megatrends underlying our markets re-

main relevant and intact and will, in future, return to drive

business expansion. Increasing consumption in the growth

regions will also lead to higher adhesives usage in the future;

and the persistent need for energy efficiency and carbon

dioxide reduction will add further growth impetus to the

adhesives markets. The increased usage of lightweight con-

struction materials, and measures to improve the thermal

insulation of buildings will necessarily require the deploy-

ment of modern adhesive systems.

With the unique breadth of our product portfolio, further

enhanced by the acquisition of the adhesives businesses of

National Starch in April 2008, we have assumed a leading po-

sition both on a global scale and in the individual regions.

6,000

6,224

6,700

5,008

5,510 5,711

Sales

in million euros

World market for adhesives, sealants

68 Annual Report 2009

The Packaging, Consumer Goods and Construction Adhesives busi-

ness was reorganized in 2008 following the acquisition of the

National Starch businesses. We have merged the associated

portfolios of both companies within a single organization,

substantially reducing complexity in the process. With this

basis, we can now offer our customers in various sectors even

more persuasive problem solutions with high-performance

products of real quality.

Served by our Electronics business, our customers in the

electronics industry use our range of high-tech adhesives

and soldering pastes in the manufacture of microchips and

printed circuit boards.

The Adhesive Technologies business sector therefore

serves a wide range of customer groupings and industries

around the world. And because we have such a broad spec-

trum of technologies, we can offer tailored services capable

of generating optimum customer benefits. The high level of

diversification in our business portfolio, serving sectors of

differing cyclicality, also proved beneficial under the very

difficult market conditions that prevailed in 2009, cushion-

ing the decline in sales and securing our profitability.

In the case of branded products for private users sold via

the retail trade, particular emphasis is placed on distribution

and brand management, with the associated advertising

and point-of-sale activities. With our leading brands and

often high market shares, we occupy good positions right

across the board.

In the industrial business, it is important to have a

deep insight into different customer requirements and

user expectations in order to create the basis for supply-

ing the tailored systems required. Aside from the products

themselves, such solutions will usually also include major

advisory and training components. Following the assign-

ment of our production activities to the individual strategic

business units in 2009, we are now even better positioned

to offer the flexibility necessary to reliably satisfy customer-

specific demands.

We endeavor to achieve high innovation rates in all our

business segments in order to generate sustainable, profit-

able sales growth. Our current innovation rate lies at around

20 percent. In addition to the development of new solutions

for existing fields of activity, finding and exploiting new ap-

plications for our products constitutes an important aspect

of our strategy.

Business activity and strategy

Following the realignment implemented in the year under

review, the Adhesive Technologies business sector now con-

sists of five strategic business units (SBU). In order to sharpen

our customer focus, we decided in 2009 to define our busi-

nesses more accurately on the basis of the market segments

and the client requirements they serve. By also removing

reporting levels, we not only shortened the decision-making

paths, enabling us to respond more quickly to the require-

ments of our markets, we were able to cut cost as well. The

individual strategic business units were also strengthened

through a higher level of operating responsibility and the

integration of important functions such as production. In

Europe, we no longer manage our businesses on the basis

of national boundaries but rather in accordance with these

newly defined SBUs. There has been a significant improve-

ment in management efficiency, now that the new structure

is in place.

In the Adhesives for Craftsmen, Consumers and Building busi-

ness, our focus is on brandname products for private and

professional users together with products and system so-

lutions for building professionals. For use in the home,

school and office, we offer adhesives under the international

brands of Loctite and Pattex, together with glue and correc-

tion products under the Pritt brand. And for decoration,

renovation and house building or refurbishment work, our

customers can choose from a wide range of adhesives and

sealants including our Pattex power adhesives, Sista sealing

compounds and Metylan decoration products. Under the

Ceresit brand, we market products and systems for tiling,

waterproofing and façade insulation.

The Transport and Metal business has overall responsibility

for our activities involving major international customers

in the automotive and metal processing industries. We of-

fer our clients tailored system solutions and specialized

technical services covering the entire value chain – from

steel coating to final vehicle assembly.

The customers served by our General Industry business are

small and medium-sized manufacturers from a multitude of

industries ranging from household appliance producers to

the wind power sector. Our product portfolio encompasses

Loctite products for industrial maintenance, repair and

overhaul, plus a select range of sealants and system solu-

tions for surface treatment.

Group management report » Adhesive Technologies

69

Annual Report 2009

Operating profit for the year as a whole fell significantly, by

55.9 percent to 290 million euros, as a result of substantial

volume decreases, the corresponding low capacity utiliza-

tion levels and the exceptional charges that had to be rec-

ognized. After adjusting for these one-time items and for

restructuring charges, adjusted operating profit (“adjusted

EBIT”) fell by 25.6 percent to 506 million euros. Compared to

the previous year, return on sales decreased by 5.1 percent-

age points to 4.7 percent; nevertheless, the adjusted figure

only decreased by 2.0 percentage points to 8.1 percent.

Return on capital employed (ROCE) fell by 5.2 percentage

points to 4.8 percent. However, we were able to substantially

decrease working capital through specific measures aligned

to reducing inventories and trade accounts receivable.

Business segments

In the Adhesives for Craftsmen, Consumers and Building business,

performance was affected not only by consumer reluctance

and destocking by our customers but also the continuing

recession affecting the building industry. Even against this

background, we continued to pursue the launch of innova-

tive products such as our new building adhesive under the

Pattex brand. We were able to increase our business with

the building industry overall, due primarily to the particu-

larly gratifying developments encountered in the regions

of Eastern Europe and Africa/Middle East.

The effects of the global economic and financial cri-

sis were particularly noticeable in the Transport and Metal

business. Nevertheless, here too there was a slight recovery

observed during the course of the year, in which we also

successfully participated. In our business activities involving,

in particular, major OEM customers from the automotive

and metal industries, we pursue a policy of maintaining

close cooperation on a partnership basis. As an example,

we were able to implement the first innovative process so-

lutions to involve our Bonderite products for surface treat-

ment on behalf of a major German premium automobile

manufacturer.

The General Industry business suffered from the decline

in industrial production and a low level of propensity to in-

vest, particularly in the case of durable goods. Sales overall

were well below the prior-year levels for this segment. Our

operations involving products for industrial maintenance,

repair and overhaul under the Loctite brand performed

We regularly review all the components of our portfolio

against the long-term objectives of the business sector. As

a consequence of this process, spring 2009 saw the divest-

ment of our adhesive tapes operation under the brands

Duck, Painter’s Mate Green and Easy Liner in the USA and

Canada.

Our business priority going forward is on achieving

profitable organic growth and harnessing the potential

for synergies and economies of scale that lie within our

organization following the successful acquisition of the

National Starch businesses. We intend to utilize the favor-

able positions we enjoy as a supplier in the various market

segments in order to generate further growth while real-

izing in full the planned savings arising from the latest

cost-reducing measures.

Sales and profits

In a heavily contracted overall market, sales of the Adhesive

Technologies business sector decreased in the year under

review by 7.1 percent to 6,224 million euros. Organically –

i.e. after adjusting for foreign exchange and acquisitions/

divestments – the decline was 10.2 percent. In this difficult

environment, sales in the mature markets of Western Europe

and North America in particular were well below the prior-

year levels. In the growth regions, the decreases were less

pronounced; and in Latin America, sales actually increased

compared to the previous year.

Through accelerated realization of synergies arising

from the integration of the National Starch businesses, the

early introduction of our efficiency enhancement program

“Global Excellence” and further substantial efforts to re-

duce cost, we were able to significantly improve our return

on sales in the course of the year. Overall, we considerably

reduced our structural cost levels while maintaining in-

vestments in research and development. In pursuit of our

policy to consolidate our production network, we have closed

30 factories in the last two years, concentrating produc-

tion at our most efficient sites. We have also earmarked

a number of marginal activities for divestment and have

already accounted for the valuation losses necessary in the

event of their sale. In addition, we re-evaluated certain long-

term contracts with suppliers and performed a number of

impairment tests which led to the write-down of identified

intangible assets.

Group management report » Adhesive Technologies

70 Annual Report 2009

Outlook

For 2010 we expect the markets of relevance to us to stabilize

or even undergo a small degree of growth. As in the past, the

growth regions are likely to develop better than the mature

markets. At the moment, we anticipate that Europe and

North America will only experience minor recovery across

major market segments.

We expect the prices for raw materials and packaging

to increase again, due particularly to the capacity adjust-

ments that have occurred in the associated manufacturing

industries.

Following the setbacks of 2009, we intend to return to

the path of profitable growth in 2010. We aim to once again

outperform our relevant markets in terms of organic sales

growth. Given the significant improvement in our cost struc-

ture resulting from the measures introduced in 2009, we

expect adjusted operating profit to undergo a substantial

increase compared to the prior-year figure.

Our opportunities lie primarily in the introduction of

innovations in existing areas of application, the develop-

ment of new applications for adhesives, and the positive

market dynamics of the growth regions.

The primary risks lie in the possibility that the antici-

pated market recovery will not take place, that individual

customers and suppliers might disappear from the markets,

and that raw material prices will again rise significantly.

at a more stable level and even posted a small degree of

growth in the region of North America. We were able once

again to underline our commitment to sustainability with

the expansion of our product range to include halogen-

free adhesives, and threadlock products which, thanks to

new development work, no longer need to be marked with

hazard symbols.

The Packaging, Consumer Goods and Construction Adhesives

business remained somewhat more robust in a market

environment characterized by falling demand for consumer

goods. Although organic sales growth in this SBU declined,

we were able to achieve in part substantial increases in the

growth regions of Eastern Europe, Africa/Middle East and

Latin America. Our adhesives for flexible packaging contin-

ued to perform well. As a result of the integration of the

National Starch businesses, we are able to offer an even more

comprehensive product portfolio. Our customers from the

packaging industry, for example, have given an enthusias-

tic welcome to our integrated solutions comprising both

adhesive and application system.

The Electronics business was heavily affected by devel-

opments in the semiconductor market, with significant

shrinkage during the first half of the year being followed

by a degree of recovery in the second half. However, sales

overall remained substantially below the prior-year level.

In the case of numerous product innovations, as with our

lead-free soldering pastes, sustainability aspects were again

given high priority.

Capital expenditures

2009 saw a continuation of our investment activities pro-

moting the integration of the National Starch businesses.

Due to the difficult economic climate with contracting

production volumes worldwide, we raised the priority of

investments aligned to the consolidation of our produc-

tion capacities. This resulted in a significant decrease in

capital expenditures on property, plant and equipment to

135 million euros in the year under review, compared to

201 million euros in the previous year.

Group management report » Adhesive Technologies

71

Annual Report 2009

Group management report » Risk report

management system, confirming its adequacy and regula-

tory compliance.

The following describes the main features of the internal

control and risk management system in relation to our

accounting processes in accordance with Clause 289 (5)

and Clause 315 (2) no. 5 of the German Commercial Code

[HGB] as amended by the German Accounting Law Reform

Act [BilMoG].

In accordance with the definition of our Risk Manage-

ment System, the objective of our accounting processes

lies in the identification, evaluation and management of

all those risks that jeopardize the regulatorily compliant

preparation of our annual and consolidated financial state-

ments. Consequently, it is the task of the Internal Control

System implemented in order to combat such discrepancies,

to put in place corresponding principles, procedures and

controls that will ensure a regulatorily compliant process

for the preparation of such financial statements.

Within the organization of the Internal Control System,

the Management Board assumes overriding responsibility

at the Group level. The duly coordinated subsystems of the

Internal Control System lie within the spheres of responsi-

bility of the functions Risk Management, Compliance, Cor-

porate Accounting and Financial Operations. Within these

functions, there are a number of integrated monitoring and

control levels, ensuring multi-point stability of the internal

control and risk management system. This is further attested

by regular and comprehensive efficacy reviews performed

by our Internal Audit function.

Of the many and varied control processes incorporated

into the accounting regime, some are worthy of particu-

lar mention. The basis for all our accounting processes is

Risk report

Risk management system

The Risk Management System (RMS) at Henkel is an integral

component of the comprehensive planning, control and re-

porting regime practiced in the individual companies, in our

business sectors and at the corporate level. It encompasses

the systematic identification, evaluation, management,

intelligence and findings are taken into consideration as we

continuously further develop our guidelines and systems. At

Henkel, therefore, risk management is performed on a ho-

listic, integrative basis involving the systematic assessment

of risk exposure. We understand risk as the possibility of a

negative deviation from a financial target or KPI resulting

from an event or change in circumstances.

Our annual risk reporting process begins with iden-

tifying major risks using checklists based on predefined

operating risk categories (e.g. procurement and production)

and predefined functional risk categories (e.g. informa-

tion technology and human resources). We evaluate the

risks in a two-stage process according to occurrence like-

lihood and potential loss. The material limit applied is risk

of a potential loss upward of 1 million euros. We initially

determine the gross risk and then, in a second stage, the

net risk after taking into account our countermeasures.

Initially, risks are recorded on a decentralized basis by our

affiliated companies, coordinated by our regional officers.

The locally collated risks are then analyzed by the experts

in the business sectors and corporate functions, classified

in the appropriate management committees and finally

assigned to a segment-specific risk inventory. Corporate Con-

trolling is responsible for coordinating the overall process

and also the aggregation and analysis of the inventorized

risks. All the risk management processes are supported by

an intranet-resident database which ensures transparent

communication throughout the entire corporation. Within

the framework of its 2009 audit of the financial statements,

the auditor examined the structure and function of our risk

Risk Management System

Regional

officer 1

Adhesive

Tech-

nologies

Cosmetics/

Toiletries

Corporate

functions

(HR, IT ...)

Laundry &

Home Care

72 Annual Report 2009

Group management report » Risk report

ing pressure on prices and conditions, accompanied by an

increase in the market share attributable to own labels.

Our focus therefore is on achieving a steady increase in our

brand equity and developing further innovations. We see

innovative products as enabling us to differentiate ourselves

from the competition, a significant prerequisite for the

continued success of our company.

Procurement market risks: Following the stabilization

of the raw material markets in the course of the year un-

der review, we see further risks in the procurement mar-

kets arising from unplanned price increases with respect

to important raw materials and packaging materials. We

are combating such risks through the proactive manage-

ment of our vendor portfolio and utilization of our glob-

ally engaged, cross-divisional sourcing function. We en-

ter into strategic partnerships with vendors of important

and price-sensitive raw materials in order to minimize the

concomitant price risks. We are also working hard within

interdisciplinary teams (Research and Development, Sup-

ply Chain Management and Purchasing) in order to devise

alternative formulations and different forms of packaging

that will enable us to respond to unforeseen fluctuations

in raw material prices. Due to the risk of non-availability

of important raw materials, we operate a strict policy of

independence from individual vendors so as to better se-

cure the constant supply of the goods and services that

we require. The basis for our successful risk management

approach in this domain is a comprehensive procurement

information system that ensures permanent transparency

of our purchasing volumes.

Production risks: Risks in the field of production arise in

the Henkel case not only from low capacity utilization due

to volume decreases but also in the possibility of operational

interruptions, especially at our so-called single-source sites.

The negative effects of possible production outages can be

offset through flexible production control and appropriate

insurance policies where economically viable. Generally,

risks in the field of production are minimized by ensuring

a high level of employee qualification, establishing clearly

defined safety standards and carrying out regular plant

and equipment maintenance. Decisions relating to capital

expenditures on property, plant and equipment are taken

in accordance with defined, differentiated responsibility

matrices and approval procedures in order to mitigate con-

comitant risk. The procedures implemented incorporate

all the relevant specialist functions and are regulated in

provid

ed by our “Accounting” corporate standard, which

contains detailed accounting instructions covering all

activities and eventualities. It specifies, for example, the

procedure to be adopted in inventory valuation, and how

the transfer prices applicable for intra-group transactions

are to be determined. This corporate standard is binding on

the entire Group and is regularly reviewed and re-released

by the CFO. Further globally binding procedural instruc-

tions affecting our accounting practice are contained in

our corporate standards “Treasury” and “Investments.”

With appropriate organizational measures in conjunc-

tion with restrictive control of access to our information

systems, we ensure the effective separation of responsibili-

ties in our accounting systems between transaction entry

on the one hand and auditing and approval on the other.

Documentation relating to the operational accounting and

closure processes ensures that important tasks – such as

the reconciliation of receivables and payables on the basis

of balance statements and confirmations – are clearly as-

signed. Strict access authorizations also exist with respect

to the approval of contracts, credit notes and similar, and

we practice the double-check security principle right across

the board. This is also stipulated in our Group-wide corpo-

rate standards.

We consider the established systems to be fit for purpose

and functionally efficient. They are regularly reviewed in

order to determine their optimization and further devel-

opment potential. Once identified, such potential is duly

utilized.

Disclosure of major individual risks

The focus of this section is on the primary risks affecting our

operations. We describe the opportunities open to us in the

forecast section starting on page 76 and also in the indi-

vidual business sector summaries starting on page 58.

Economic and sector-specific risks: Given the persis-

tence of the current economic difficulties encountered in

our sales markets, we consider ourselves to still be exposed

to considerable economic risk. The fragile environment in

the industrial sector, and particularly in the automotive

manufacturing and components segments and the metal

processing industry, carries with it risks and may lead to

a decrease in sales volume. In the consumer goods sector,

there is the risk of flattening market growth in conjunction

with increasing competition. In this sector we are seeing

further consolidation in the retail segment with correspond-

73

Annual Report 2009

Group management report » Risk report

credit risks also arise in the case of financial investments

such as cash at bank and the positive fair value of deriva-

tives. However, such exposure is significantly limited by our

Corporate Treasury specialists through selection of banks

of good reputation with at least an A rating, and restriction

of the amounts allocated to individual investments. More

detailed information with respect to our credit risk can be

found in Note 42 starting on page 115.

Risks from pension obligations relate to changes in

interest rates, inflation rates, trends in wages and salaries,

and changes in the statistical life expectancies of pension

beneficiaries. Interest and inflation risks can be reduced by

fully funding the pension obligations with investments in

interest and inflation-sensitive fund assets that mirror the

maturity structure of the pension obligations. Risks relating

to trends in wages and salaries and life expectancies can be

mitigated by inclusion of a return-enhancing portfolio in

the financing mix expected to yield a surplus return over

and above the refinancing costs of the pension obligations.

In order to reduce and better manage risk, therefore, the

pension obligations in the main countries involved are fully

funded and managed on the basis of a twin-track portfolio

approach. The main portion of the portfolio is invested in

fund assets exhibiting the same maturity structure and

similar interest and inflation sensitivities as the pension

obligations (liability-driven investments), reducing the in-

terest rate and inflation risk. In order to cover the risks

arising from trends in wages, salaries and life expectancies,

and to close the potential deficit between fund assets and

pension obligations over the long term, additional invest-

ments are made in a return-enhancing portfolio as an add-on

instrument that contains assets such as equities, private

equity investments, hedge funds, real estate and commod-

ity investments.

The pension fund can be adversely affected in the event

of a downturn in the capital markets. We mitigate this risk

by investing in widely diversified classes of assets and differ-

ent instruments within each asset class. The risks inherent

in the pension fund assets are continuously monitored and

controlled on the basis of risk and return criteria. Risks in

this respect are quantified using sensitivity analyses. Major

pension funds are administered by external fund managers

in Germany, the USA, the UK, Ireland and the Netherlands.

All these countries follow the above-described standard

investment strategy and are centrally monitored. The funds

covering our pension obligations are invested on the basis of

an internal corporate guideline requiring that such invest-

ments be analyzed in advance on the basis of a detailed

risk appraisal. Further auditing and analytical procedures

accompanying projects at the appraisal and implementation

stage provide the basis for successful project management

and effective risk reduction.

Information technology risks: The risks associated with

our IT operations relate primarily to the potential for un-

authorized access and data loss. Appropriate approval pro-

cedures, authorization profiles and defensive technologies

are deployed in order to guard against such eventualities.

Daily data back-up runs are conducted to shadow all critical

databases, and the resultant files are transferred to another

site. We also carry out regular restore tests. External attacks

that took place in 2009 – for example in the form of hack-

ing, spamming or viruses – were successfully repelled by

the security measures implemented and therefore had no

disruptive effect on our business processes. Moreover, Henkel

has put in place a globally binding internal IT guideline to

which our external service-providers are also bound. Major

components of this code include measures for avoiding risk,

and descriptions of escalation processes and best-practice

technologies. Correct implementation is continuously moni-

tored by our globally active Internal Audit unit. In addition,

our safeguards are examined for their efficacy and efficiency

by external specialists.

Personnel risks: The future economic development of

Henkel is essentially dependent upon the commitment and

capabilities of our employees. We respond to the increasing

competition for well qualified technical and managerial staff

by maintaining close contacts with selected universities and

conducting special recruitment campaigns. We combat the

risk of failing to retain valuable employees over the long

term through specifically aligned personnel development

programs. The basis for these is provided by attractive quali-

fication and further training opportunities combined with

performance-related compensation arrangements.

Financial risks: Due to the still tense financial situation,

particularly in the automotive components sector and the

building industry, our credit risk is higher than in the

years prior to the crisis. We mitigate this exposure within

the framework of our global credit policy through standard-

ized procedures, a proactive credit management regime and

the use of guarantees and credit default insurance policies.

Aside from meticulous local vigilance, we also monitor our

key customer relationships at the global level. Default and

74 Annual Report 2009

Henkel of America, Inc. in US dollars has been converted

into fixed-interest instruments through the use of interest

rate swaps. When employing interest rate swaps in order to

fix an interest rate, the net results of the swap are taken to

equity (cash flow hedge accounting). Depending on interest

rate expectations, Henkel also protects itself against short-

term increases by negotiating additional interest rate caps

and concluding forward rate agreements. As a result, the

net interest item derives from a mixed fixed and floating

interest rate structure.

The liquidity risk describes the risk of a company failing

to meet its financial obligations at any given time. At Henkel,

this risk can be regarded as very low due to the fact that we

are able to call upon long-term financing instruments and

additional liquidity reserves in the form of permanently as-

sured credit lines. The basis of our currency, interest rate and

liquidity risk control capability is provided by the treasury

guidelines introduced by the Management Board, which

are binding on the entire corporation. Defined in these are

the targets, principles, accountability and competences of

Corporate Treasury. They describe the fields of responsibil-

ity and establish the distribution of these responsibilities

between the corporate level and our subsidiaries. The Man-

agement Board is regularly and comprehensively informed

of all major risks and of all relevant hedging transactions

and arrangements.

Additional information on risk management with re-

spect to financial instruments can be found in Note 42

on pages 112 to 118.

Legal risks: As a globally active corporation, we are also

exposed in the course of our ordinary business activities to

a range of risks relating to litigations and other proceed-

ings or actions, including those brought by governmental

agencies, in which we are currently involved or may be-

come involved in the future. These include, in particular,

risks arising from the fields of product liability, product

deficiency, laws relating to competition and monopolies,

the infringement of proprietary rights, patent law and tax

law, and environmental protection and land contamination

issues. The possibility cannot be discounted that the deci-

sions taken in some of these litigations and proceedings

will go against us.

We counteract legal risks by issuing corresponding bind-

ing guidelines and codes of conduct and by instituting ap-

propriate training measures. We address current actions and

potential litigation risk by maintaining constant contacts

asset-liability studies aligned to the expected cash flows aris-

ing from the country-specific pension obligations. Further

information on the development of our pension obligations

can be found in Note 28 on pages 103 to 107.

Given the global alignment of our businesses, we are

exposed to two types of currency risk. Transaction risks

arise from exchange rate fluctuations causing changes in

the value of future foreign currency cash flows. Transaction

risks arising from our operating business are avoided primar-

ily by the fact that we largely manufacture our products in

those countries where they are sold. Residual transaction

risks on the operating side are proactively managed by Cor-

porate Treasury. Its remit includes the ongoing assessment

of specific currency risk and the development of appropriate

hedging strategies. Because we strictly limit our potential

losses, any negative impact on profits is restricted. The trans-

action risks arising from major financial receivables and

financial liabilities are extensively hedged. The risks are

predominantly mitigated by forward exchange contracts

and currency swaps. Translation risks, on the other hand,

emanate from changes caused by foreign exchange fluctua-

tions to items on the balance sheet and income statement

of a subsidiary, and the effect these changes have on the

translation of individual company financial statements into

Group currency. The risks arising from the translation of

sales and profits of subsidiaries in foreign currencies and

from net investments in foreign entities are only hedged

in exceptional cases.

The interest rate risk encompasses those potentially

positive or negative influences on profits, shareholders’

equity or cash flow in current or future reporting periods

arising from changes in interest rates. The deployment

of interest-bearing financial instruments with the objec-

tive of optimizing the net interest result for the Henkel

Group constitutes an essential component of our financial

policy. The maturity structure is controlled both by choos-

ing appropriate fixed-interest periods for the underlying

financial assets and financial liabilities affecting liquidity,

and by using interest rate derivatives. The interest rates

on the euro-denominated bonds issued by Henkel have

been converted in full from fixed to floating using interest

rate swaps. As the bonds and interest rate swaps are in a

formally documented hedge accounting relationship, the

measurement of the bonds and the measurement of the

interest rate swaps match in practical terms (fair value hedge

accounting). A large proportion of the financing used for

Group management report » Risk report

75

Annual Report 2009

Group management report » Risk report

between the corporate legal department and local attorneys,

and also through our separate reporting system. For certain

legal risks, we have concluded insurance policies that are

standard for the industry and that we consider to be fit for

purpose. We form provisions for litigations to the extent that

it is likely in our estimation that obligations may arise which

are either excluded from or not fully covered by our insur-

ance policies and where a reasonably accurate estimate of

the potential loss is possible. However, predicting the results

of actions is beset with considerable difficulties, especially

in cases in which the claimant is seeking substantial or

unspecified damages. Given these imponderables, we are

unable to predict what obligations may arise from such

litigations. Consequently, major losses can arise from litiga-

tions and proceedings that are not covered by our insurance

policies or our provisions.

We do not currently foresee risks arising from litigations

or proceedings either pending or threatened that could have

a material influence on our net assets, financial position

or results of operations.

Overall risk

At the time of writing this report, there are no identifiable

risks relating to future developments that could endan-

ger the existence either of the parent company or of the

Group as a going concern. Our risk analysis indicates that

the net assets, financial position and results of operations

of the parent company and of the Group as a whole are

not currently endangered either by individual risks or by

the aggregated exposure arising from all risks combined.

Moreover, such aggregation only takes into account the

risk side of the equation without allowing for the positive

effect that opportunities may bring. The system of risk cat-

egorization undertaken by Henkel clearly indicates that the

most significant exposure currently relates to the impact of

economic uncertainty on sales volumes and revenues, and

the associated financial risks, to which we are responding

with the countermeasures described.

76 Annual Report 2009

Forecast

General economic development

Overview

The world economy is, in our view, likely to return to mod-