37

Annual Report 2009

Group management report » Value-based management and control system

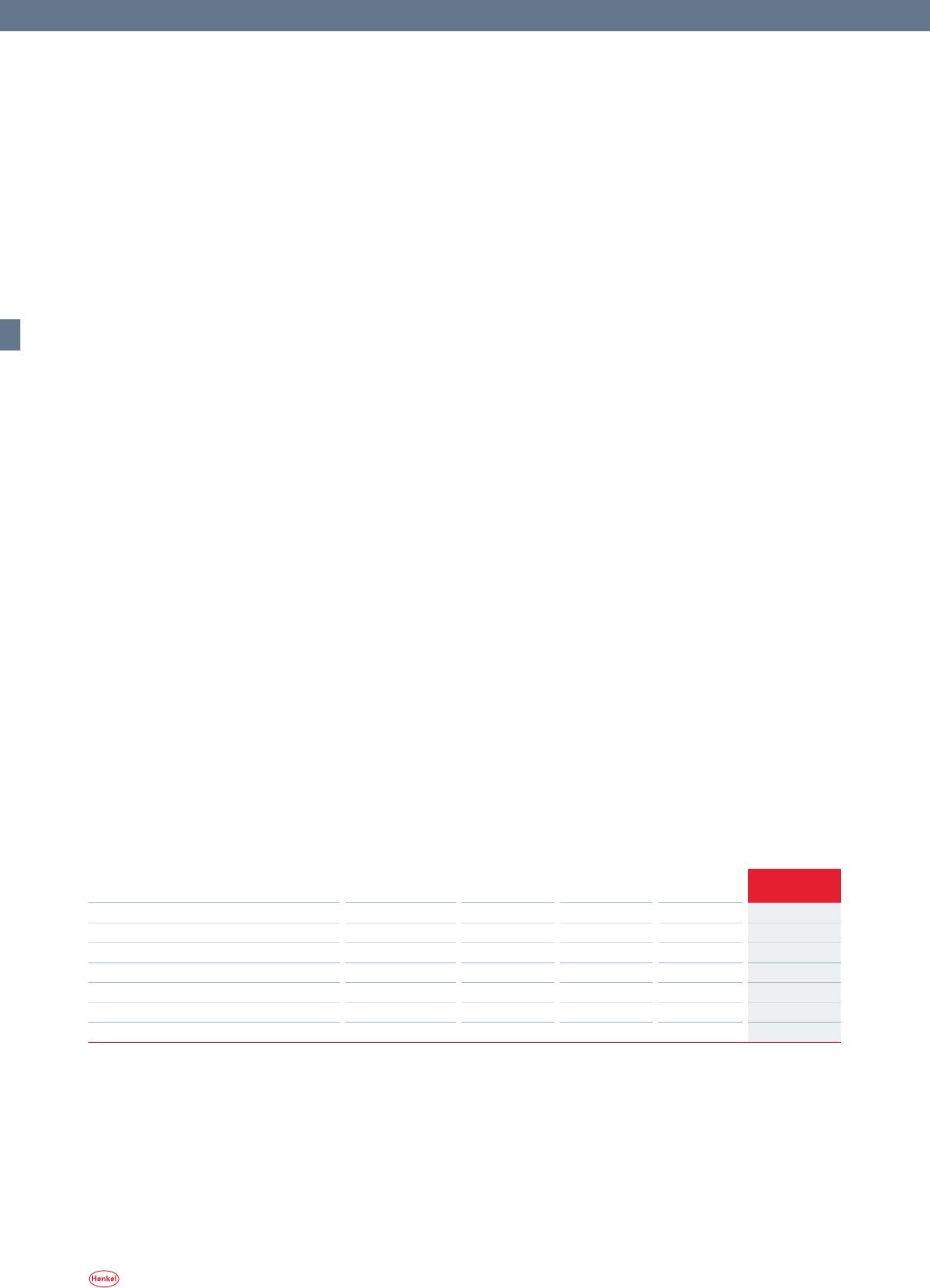

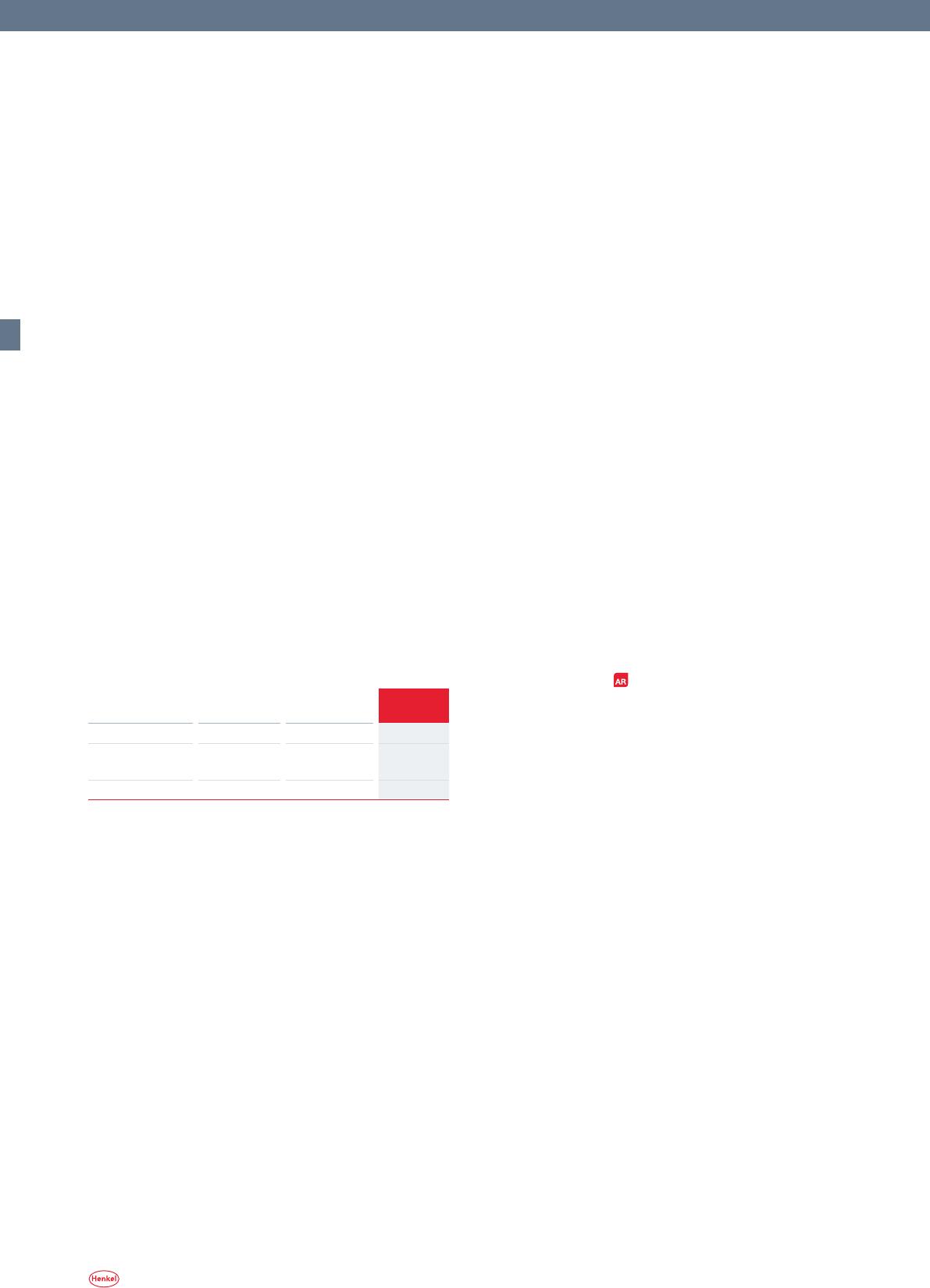

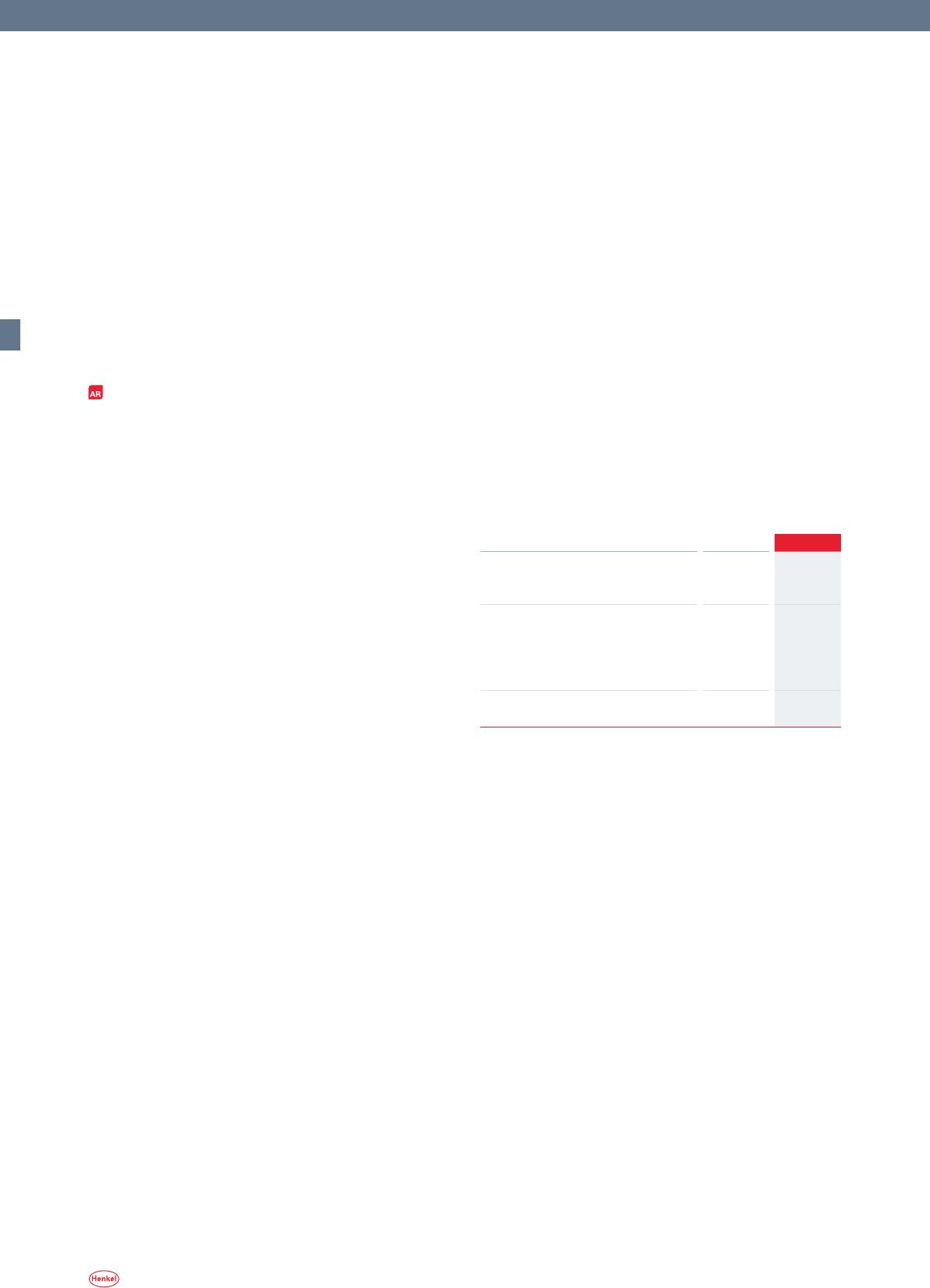

Weighted average cost of capital (WACC)

2009 from 2010

Risk-free interest rate 4.8 % 4.3 %

Market risk premium 4.5 % 4.5 %

Beta factor 1.00 0.80

Cost of equity after tax 9.4

% 8.0

%

Cost of debt capital before tax 5.3 % 5.0 %

Tax shield (30 %) –1.6 % –1.5 %

Cost of debt capital after tax 3.7

% 3.5

%

Share of equity

1) (target structure) 75 % 75 %

Share of debt capital

1) (target structure) 25 % 25 %

WACC after tax

2) 8.0

% 7.0

%

Tax rate 30 % 30 %

WACC before tax

2) 11.5

% 10.0

%

1) At market values

2) Rounded

WACC before tax by business sector

2009 from 2010

Laundry & Home Care 10.5 % 10.0 %

Cosmetics/Toiletries 10.5 % 10.0 %

Adhesive Technologies 12.5 % 11.5 %

EVA® and ROCE

EVA® serves to promote value-added decisions and profitable

growth in all our business sectors. Operations exhibiting neg–

ative value contributions with no prospect of positive EVA®

in the future are divested or otherwise discontinued.

At Henkel, EVA® is calculated as follows:

EVA® = EBIT

2) – (Capital Employed x WACC).

In order to be better able to compare business units of vary–

ing size, we additionally apply return on capital employed,

calculated as follows:

ROCE = EBIT

2) / Capital Employed.

ROCE represents the return on average capital employed. We

create value where this metric exceeds the cost of capital.

In fiscal 2009, the Henkel Group generated a negative

economic value added (EVA®) of –201 million euros. This

represents an improvement of 265 million euros compared

to the previous year. The business sectors Laundry & Home

Care and Cosmetics/Toiletries each generated a positive

EVA®. At 164 million euros, the contribution made by Cos-

metics/Toiletries was some 10 percent above the prior-year

level; and with 232 million euros, Laundry & Home Care

was able to significantly outstrip the figure of 166 million

Value-based management and control system

To make achievement of our growth targets measurable, we

have adopted a modern system of metrics with which we

calculate value-added and return ratios in line with capital

market practice.

We use economic value added (EVA®)

1)

to assess growth to

date and to appraise future plans. EVA® is a measure of the

additional financial value created by a company in a given

reporting period. A company creates economic value added

if its operating profit exceeds its cost of capital, the latter

being defined as the return on capital employed expected

by the capital market.

Operational business performance is measured on the

basis of operating profit (EBIT adjusted for any goodwill

impairment losses). The capital employed figure is calculated

from the assets side of the balance sheet. A reconciliation

of the year-end figures in the balance sheet to the average

values used in determining capital employed can be found

on page 123.

The cost of capital employed is calculated as a weighted

average of the cost of capital (WACC) comprising both equity

and debt. In fiscal 2009, we applied a WACC after tax of

8.0 percent. Before tax, the figure was 11.5 percent. We regu–

larly review our cost of capital in order to reflect changing

market conditions. Starting fiscal 2010, therefore, we have

adopted a WACC of 10.0 percent before tax and 7.0 percent

after tax.

We further apply different WACC rates depending on the

business sector involved. This is based on sector-specific beta

factors taken from a peer group benchmark. In fiscal 2009,

this resulted in a WACC before tax of 10.5 percent (7.5 per-

cent after tax) for both Laundry & Home Care and Cosmetics/

Toiletries, and of 12.5 percent before tax (8.5 percent after

tax) for Adhesive Technologies. In 2010 we are applying a

WACC of 10.0 percent before tax (7.0 percent after tax) for

the business sectors Laundry & Home Care and Cosmetics/

Toiletries, and 11.5 percent before tax (8.0 percent after tax)

for Adhesive Technologies.

1) EVA® is a registered trademark of Stern Stewart & Co. 2) Before goodwill impairment

38 Annual Report 2009

Group management report » Value-based management and control system

ties and other plant and equipment are likewise governed by

framework rules and regulations – including those relating

to the decontamination of soil.

Product-specific regulations of relevance to us relate in

particular to ingredients and input materials, safety of man–

ufacture, the handling of products and their constituents,

and the packaging and marketing of these items. The control

mechanisms include statutory material-related regulations,

usage prohibitions or restrictions, procedural requirements

(test and inspection, identification marking, provision of

warning labels, etc.), and product liability law.

Our internal standards are geared to ensuring compli–

ance with statutory regulations and the safety of our manu–

facturing facilities and products. The associated require–

ments have been incorporated within and implemented

through our management systems, and are subject to a

regular audit and review regime. This includes monitoring

and evaluating relevant statutory and regulatory require–

ments and changes.

One example of a material change in the statutory en-

vironment is the European regulation on the registration,

evaluation, authorization and restriction of chemicals –

Regulation (EC) No. 1907/2006, abbreviation: REACH. This

regulation primarily affects Henkel as a user of chemical

materials; however, it also affects us as an importer and

manufacturer. In order to ensure the efficient implementa–

tion of the associated requirements, we have established a

central REACH management team for handling and control–

ling the main REACH processes.

euros for the previous year, thanks to its strong operat–

ing profit. By contrast, the EVA® of Adhesive Technologies

came in at –543 million euros. This is primarily due to the

operating profit decrease emanating from the economic

crisis; however, this figure also reflects substantial one-

time and restructuring charges. We achieved a significant

improvement in the Corporate segment with –77 million

euros compared to –692 million euros for the previous year.

This substantial increase resulted from the absence of the

burden on operating profit from the previous year arising

from the restructuring charges pertaining to the “Global

Excellence” program and the integration of the National

Starch businesses.

ROCE increased from 6.9 percent to 9.8 percent. This is

again essentially due to the upturn in operating profit ema–

nating from the absence of the high restructuring charges

from the previous year.

Statutory and regulatory situation

Our business is governed by national rules and regulations

and – within the European Union (EU) – increasingly by

harmonized pan-European laws. In addition, some of our

operations are subject to rules and regulations derived from

approvals, licenses, certificates or permits.

Our product manufacturing operations are bound by

rules and regulations with respect to the usage, storage,

transportation and handling of certain substances and also

in relation to emissions, wastewater, effluent and other

waste. The construction and operation of production facili–

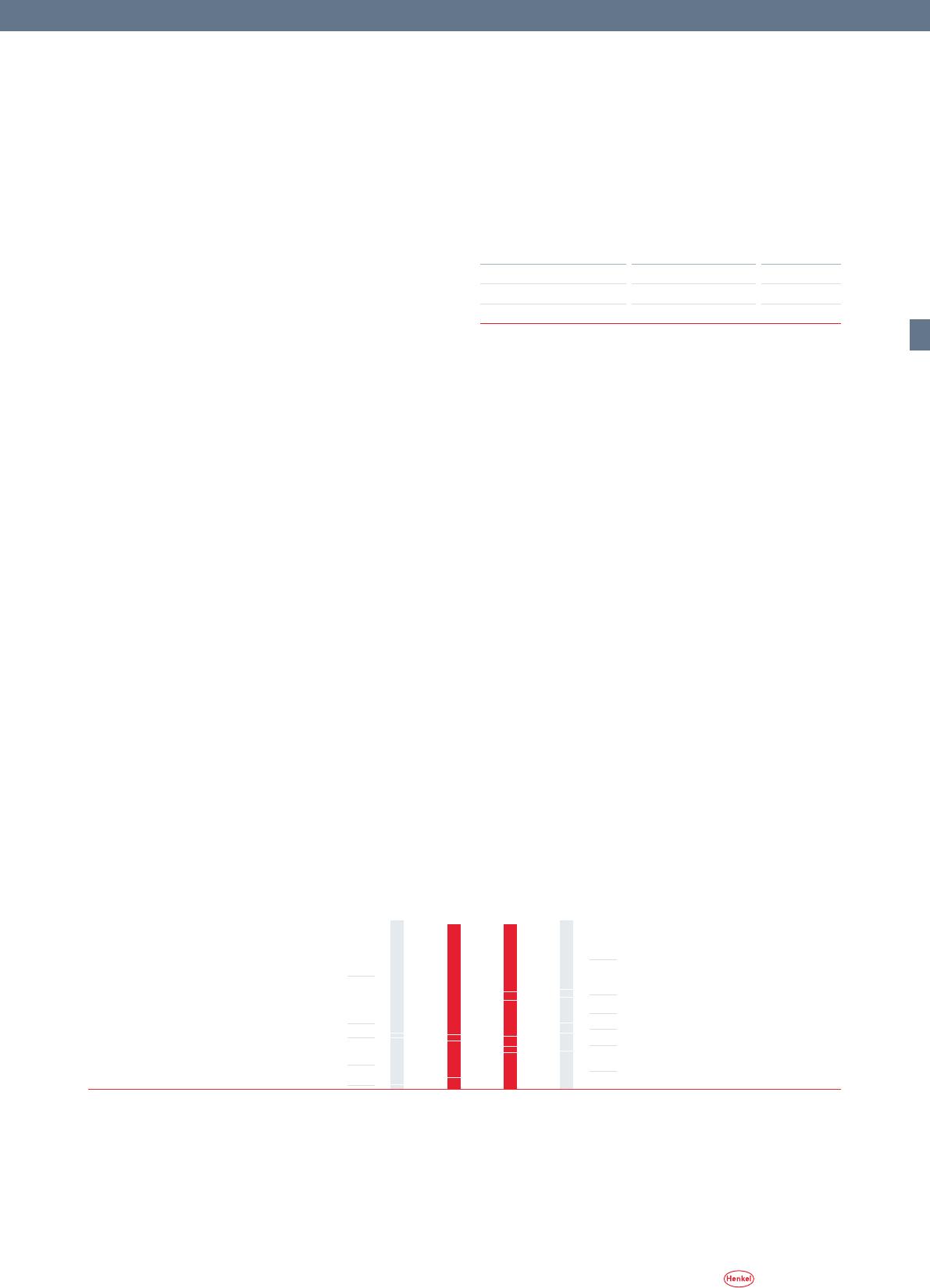

EVA® and ROCE1)

in million euros Laundry &

Home Care

Cosmetics/

Toiletries

Adhesive

Technologies

Corporate Henkel

EBIT 501 387 336

5) – 98

1,126

5)

Capital employed 2,562 2,125 7,035 –181

11,541

WACC2) 269 223 879 – 21 1,327

3)

EVA

®

2009 232 164 – 543 – 77 – 2013)

EVA® 2008 166 150 –132 – 692

– 466

4)

ROCE 2009 19.6 % 18.2 % 4.8 % – 9.8 %

ROCE 2008

16.9 % 17.5 % 10.0 % –

6.9

%

1) Calculated on the basis of units of 1,000 euros

2) Calculated on the basis of the different sector-specific WACC rates applied

3) Calculated on the basis of the WACC rate of 11.5 percent for the Henkel Group

4) Calculated on the basis of the WACC rate of 11.0 percent for the Henkel Group

5) EBIT plus 46 million euros in goodwill impairment losses

39

Annual Report 2009

Group management report » Business performance

The growth countries – with exceptions such as Mexico and

Russia – began to stabilize earlier than the mature markets,

with Asia, and particularly China, leading the way.

Raw material prices

The cost of raw materials such as crude oil, ethylene, pro–

pylene, palm kernel oil, metals and paper increased signifi–

cantly with the first signs of stabilization and then recovery

of the world economy as of the beginning of the second

quarter. This is particularly evident in the price of crude

oil which rose from 45 US dollars per barrel in the first

quarter to 79 US dollars per barrel in the fourth quarter.

However, average raw material prices remained below the

level of the previous year.

Currencies

In the first quarter of 2009, the foreign exchange markets

very much reflected the repercussions of the financial cri–

sis. While the US dollar was regarded as a safe haven and

appreciated substantially, the currencies of the growth

regions in particular lost value. As 2009 developed, the dol–

lar experienced a steady decline versus the euro. And while

the Eastern European currencies of particular importance

for Henkel recovered from their March low points, the ex-

change rates remained below the average levels prevailing

in 2008.

Inflation

There were noticeable reductions in inflation rates world-

wide. Many countries in the developed regions registered

stable or even falling prices.

Unemployment

Unemployment increased with the recession but generally

remained lower than had been expected in view of the depth

of the economic crisis.

Private consumption and developments by sector

While the consumer climate clouded in 2009 compared to

the longer view, consumers only restricted their spend to a

small extent worldwide. This at least cushioned the effects

of the crisis. In the course of the year, the consumer climate

began to brighten again with the gradual end to the general

crisis of confidence.

Business performance

World economy

Overview

The world economy was hit in 2009 by the heaviest reces–

sion of the post-war period. According to current estimates,

economic activity measured on the basis of gross domestic

product worldwide fell by around 2 percent. The extent of

the crisis can be explained by a coincidence of numerous

negative factors which, to some extent, also resulted in a

degree of mutual reinforcement: the financial and real

estate market crisis, the general crisis in confidence among

corporates and consumers, the slump in world trade and the

significant decline in industrial demand and production.

Developments in 2009

Nevertheless, the patterns exhibited in the individual quar–

ters differed quite considerably. The year began with a sharp

decline, followed in many regions by a still relatively weak

second quarter. In the following quarters, there was a degree

of recovery. Compared to the respective prior-year quarters,

however, the decrease in gross domestic product continued,

albeit at a slower pace.

Industry and consumption

The industrial sectors were considerably more heavily im–

pacted by the recession than private consumption. In most

regions, industrial production contracted substantially.

Some sectors, particularly export-dependent capital goods

industries, underwent double-digit declines compared to the

previous year. Nevertheless, a relatively stable level of private

consumption served to ease the decline in total economic

output in many countries, including Germany.

Regions

The crisis was substantially more noticeable in the developed

regions of North America and Western Europe than in the

growth regions. Asia (excluding Japan) proved to be the

most robust region. Eastern Europe was heavily hit, while

Latin America – with the exception of Mexico – managed

the crisis relatively well. The effects of the crisis were like-

wise noticeable in Africa and the Middle East. Instead of the

strong growth of the previous years, we saw gross domestic

product in these regions only slightly increase.

40 Annual Report 2009

Group management report » Business performance

decreased appreciably. Only China and India were able to

achieve expansion in 2009.

Further details on developments with respect to specific

segments and regions can be found in the individual busi-

ness sector reports starting on page 58.

Management Board review of business performance

Henkel’s business performance was characterized by the

above-described significant deterioration in the underlying

economic conditions compared to fiscal 2008. With the slump

in market growth at the beginning of the year, particularly in

the segments served by the Adhesive Technologies business

sector, the ensuing pattern was one of successive signs of

recovery. Our organic sales growth in the second half of the

year again experienced an improvement compared to the first

six months. Organic sales development at the Henkel Group

for the year as a whole underwent a decline of 3.5 percent.

The tense situation on the procurement markets that

characterized the trading environment of 2008 dissipated

in fiscal 2009. In the second and third quarters particularly,

we experienced a significant boost to our gross margin as

a result of declining raw material prices.

The process of stabilization in our markets toward the

end of the year and successful savings arising from our

structural and cost realignment programs were also re–

flected in the results achieved. We generated an adjusted1)

operating profit of 1,364 million euros. The implementation

of our “Global Excellence” program, introduced in order to

strengthen the profitability and competitiveness of Henkel

over the long term, turned in better results during the year

under review than was originally planned, as did the inte-

gration of the National Starch businesses.

The Adhesive Technologies business sector aligned its

activities more strictly to the needs of its customers, reor–

ganizing its internal structures to this end.

A further major event in 2009 was the successful sale of

our consumer adhesives brands Duck, Painter’s Mate Green

and Easy Liner in the USA and Canada. This divestment con–

tributed to the further consolidation of our portfolio.

Thanks to strong cash flows from our operating activi-

ties, we were able to substantially reduce our net debt. The

senior bond issued in March 2009 in the amount of 1.0 bil-

lion euros served to significantly strengthen the long-term

financing of the Henkel Group.

In the developed regions, consumption fell slightly com–

pared to 2008. In the growth regions, average consumption

stagnated. Developments in Eastern Europe were substan–

tially less favorable, with consumers significantly limiting

their expenditure following several boom years.

The retail trade performed poorly in 2009, although the

decline in activity was minor compared to that suffered by

the industrial sector.

Fiscal 2009 was a year characterized by a major industrial

downturn that exceeded the decline in total economic out–

put. Around the world, industrial production fell by almost a

tenth. And many sectors such as the transport industry had

to cope with production decreases in the high teens.

All the developed countries were affected by the heavy

industrial decline. Among the growth regions, Latin America

– with the exception of Mexico – was able to keep the minus

rates within limits. Developments in Asia were mixed: while

Japan’s industrial production declined by more than a fifth,

China was able in the crisis year of 2009 to almost repeat

the double-digit plus rates of previous years.

The region of Eastern Europe was more heavily hit by

the crisis. In most countries here, the decline in output

in the manufacturing industries was in the double-digit

percentage range.

The automotive industry began 2009 with substantial

falls in production and demand. It suffered from a reluc–

tance both among private households to buy and among

companies to invest. In the course of the year came a degree

of recovery from a low base, due primarily to state stimulus

measures such as the “scrappage premium” in Germany.

Compared to the previous year, the contraction in produc-

tion was considerable.

The electronics industry also belonged to the sectors par–

ticularly hard hit by the crisis. Here too there was a degree

of recovery during the second half of the year. Equivalent

in its magnitude was the crisis in the metals industry. Only

toward the end of the year did this sector see a gradual

revival in activity. A more substantial decline in produc–

tion was avoided in the packaging industry thanks to the

consumer-related food and semi-luxuries segment remain-

ing relatively robust.

The crisis in the building industry accelerated in 2009

with home-building being especially impacted. Most re–

gions, headed by the USA, recorded significant declines in

building output. In Eastern Europe too, building volumes

1) Adjusted for one-time charges/gains and restructuring charges

41

Annual Report 2009

Group management report » Business performance

In the regional breakdown too, the worsening economic

environment predominantly led to sales declines:

At 8,335 million euros, sales of the Europe/Africa/Middle

East region decreased organically by 1.9 percent compared

to prior year. While the consumer businesses achieved a

gratifying increase in organic sales, Adhesive Technologies

posted a decline in the double-digit percentage range. Sales

in Western Europe decreased, while in Eastern Europe we

achieved a single-digit increase in organic sales, and the

Africa/Middle East subregion once again posted a double-

digit growth rate. Overall, the share of sales of the region

fell from 63 percent to 61 percent.

Sales in the North America region decreased organically

by 8.6 percent to 2,546 million euros. All our business sec-

tors suffered considerably from the underlying economic

conditions, particularly during the first half of the year. The

share of sales accounted for by the North America region

remained constant at 19 percent.

The Latin America region continued to perform very

encouragingly, posting an organic sales growth of 5.0 per–

cent to 825 million euros, with all our business sectors con–

tributing. The share of sales attributable to Latin America

increased from 5 to 6 percent.

Like Europe and North America, the Asia-Pacific region

felt the effects of the economic crisis, with sales declin–

ing organically by 5.8 percent. Reported sales amounted to

1,657 million euros. An increase in sales posted by Cosmetics/

Toiletries was offset by a decline in Laundry & Home Care

which resulted from the discontinuation of operations in

China at the end of 2008. The organic sales performance of

the Adhesive Technologies business sector likewise under-

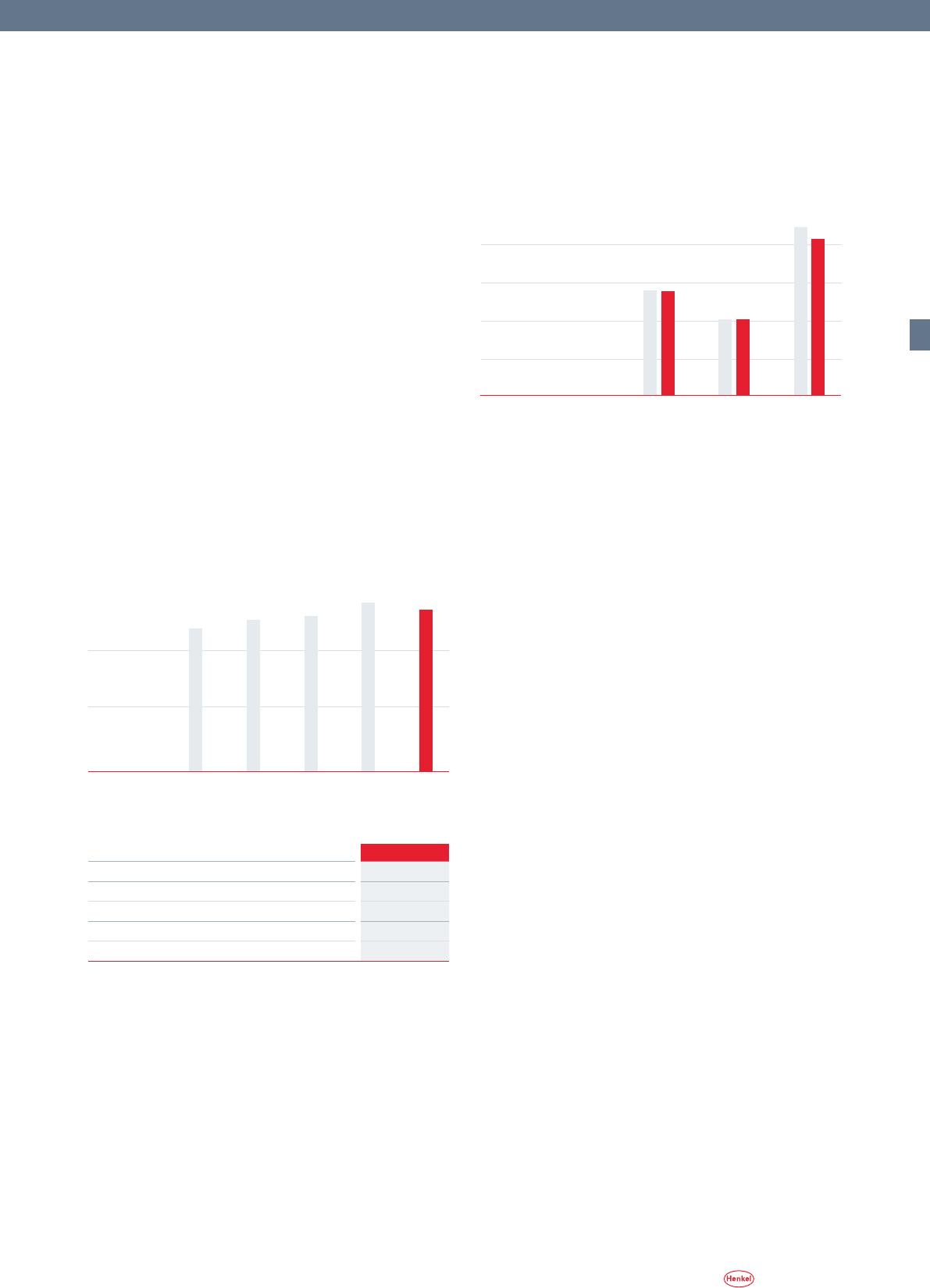

Sales and profits

Henkel Group sales in 2009 amounted to 13,573 million

euros, a fall of 3.9 percent compared to prior year. After

adjusting for foreign exchange, the decline in sales was

1.5 percent. Due to the difficult market environment in

2009, organic sales development (i.e. sales adjusted for for-

eign exchange and acquisitions/divestments) declined by

3.5 percent. Positive pricing was more than offset by vol–

ume decreases, particularly in the Adhesive Technologies

business sector.

After a first quarter heavily impacted by the econom–

ic crisis, the subsequent quarters were characterized by

a gradual recovery. With a decline of 1.0 percent overall,

organic sales performance in the second half of the year

was an improvement on developments during the first six

months, which saw a 6.1 percent decrease.

Sales development

1)

in percent 2009

Change versus previous year – 3.9

Foreign exchange

– 2.4

After adjusting for foreign exchange –1.5

Acquisitions/Divestments

2.0

Organic – 3.5

1) Calculated on the basis of units of 1,000 euros

The performance of our business sectors varied consider–

ably: while the consumer businesses Laundry & Home Care

and Cosmetics/Toiletries continued to perform well during

fiscal 2009 with organic growth rates of 2.9 percent and

3.5 percent respectively, sales of the Adhesive Technolo–

gies business sector decreased organically by 10.2 percent

due to the globally difficult situation being experienced by

important customer industries.

Sales

in million euros

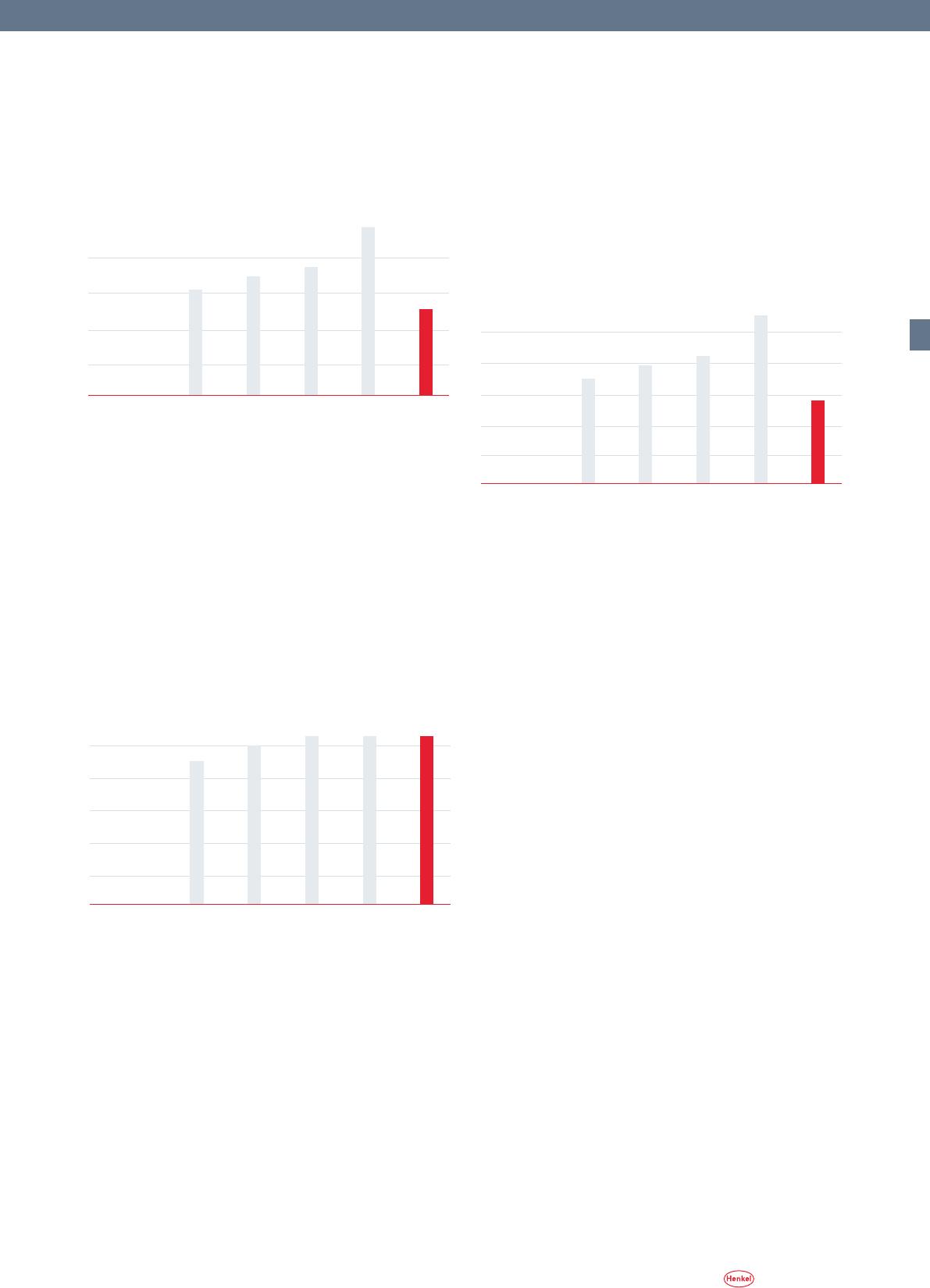

5,000

0

2009

2008200720062005

10,000

13,573

14,131

11,974 12,740 13,074

1) Excluding Corporate

Sales by business sector1)

in million euros

1,500

0

200920092009 200820082008

Laundry &

Home Care

Cosmetics/

Toiletries

Adhesive

Technologies

3,000

4,500

6,000 6,224

3,010

4,129

4,172

3,016

6,700

42 Annual Report 2009

Group management report » Business performance

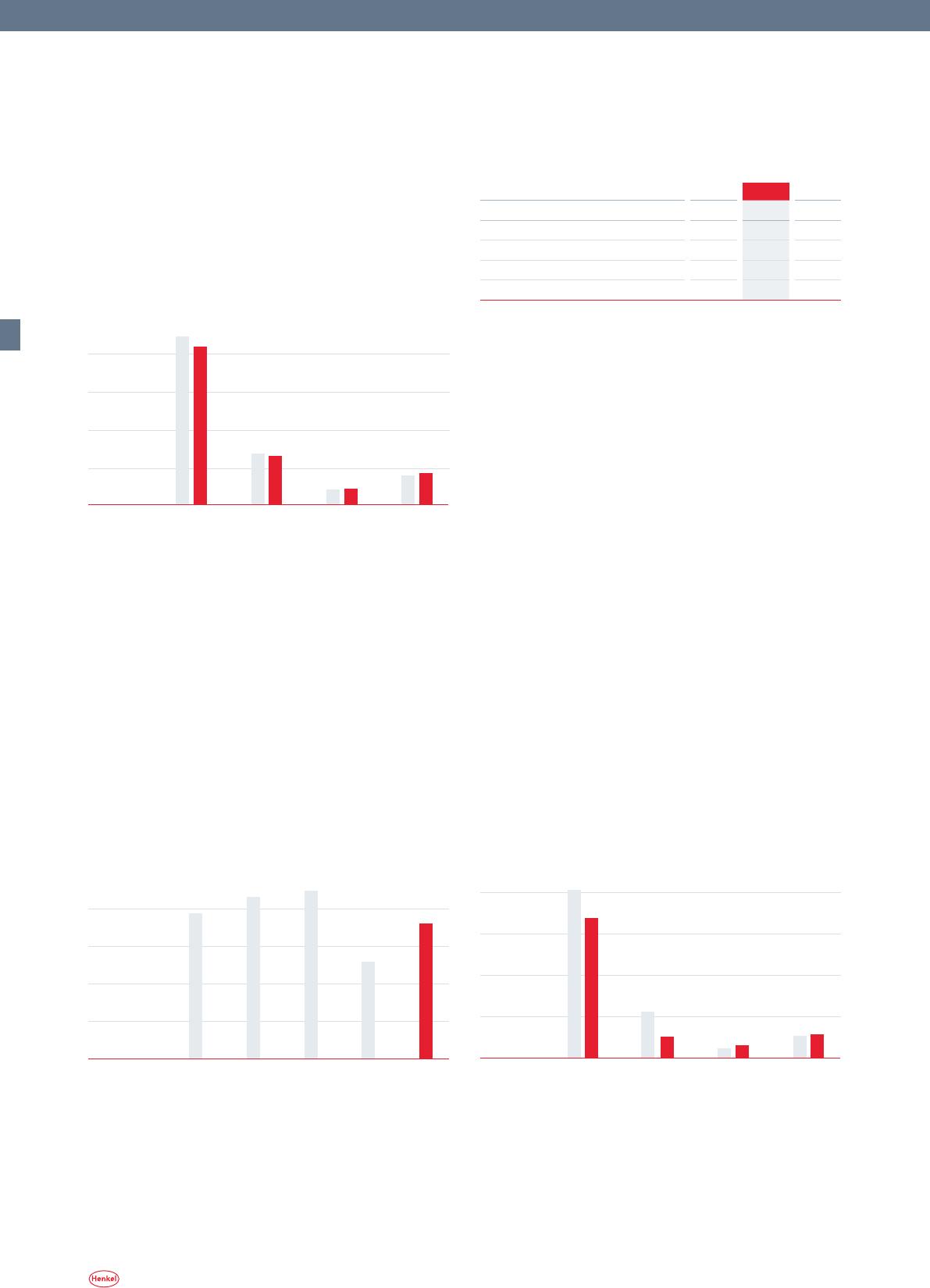

Adjusted EBIT

in million euros 2008 2009 %

EBIT (as reported) 779 1,080 38.6

One-time gains – 30

– 9

One-time charges 48

134

Restructuring charges 663

159

Adjusted EBIT 1,460 1,364 – 6.6

At 1,364 million euros, adjusted operating profit (“adjusted

EBIT”) fell below the prior-year figure of 1,460 million euros

due to the decline suffered by the Adhesive Technologies

business sector. However, we succeeded in avoiding a greater

decrease thanks to the savings generated from our “Global

Excellence” program and the integration of the National

Starch businesses. Adjusted return on sales fell by 0.3 per-

centage points to 10.0 percent due to the margin decline at

Adhesive Technologies from 10.1 percent to 8.1 percent. The

consumer businesses Laundry & Home Care and Cosmetics/

Toiletries were able to increase their adjusted return on

sales figures to an encouraging 12.8 percent (previous year:

10.8 percent) and 12.9 percent (previous year: 12.6 percent)

respectively.

The difficult market conditions also affected the profit

performance of our regions:

In Europe/Africa/Middle East, operating profit decreased

by 16.7 percent (–9.8 percent after adjusting for foreign ex-

change). While the consumer businesses saw their currency-

adjusted EBIT rise, there was a significant decline at Adhesive

Technologies. At 10.1 percent, the region’s return on sales

was below the prior-year level of 11.4 percent.

went a downturn, although there was already a return to

positive growth in the second half of the year. The share of

sales accounted for by Asia-Pacific increased to 12 percent

compared to 11 percent in the previous year.

Sales of our growth regions Eastern Europe, Africa/Middle

East, Latin America and Asia (excluding Japan) fell by 1.0 per–

cent to 5,114 million euros. Organic growth amounted to

3.7 percent, with continuous recovery in the course of the

year following a weak start. The consumer businesses made

a particularly important contribution to this improvement,

registering growth rates close to the double-digit percent–

age mark, while developments at Adhesive Technologies

remained slightly regressive. The share of sales of the growth

regions increased from 37 to 38 percent.

The following is a discussion of our operating perfor–

mance without one-time charges/gains and restructuring

charges:

1) Excluding Corporate

Sales by region1)

in million euros

0

2009200920092009 2008200820082008

North AmericaEurope/Africa/

Middle East

Latin America Asia-Pacific

2,000

4,000

6,000

8,000

1,657

825

2,546

8,335

2,700

8,863

780

1,545

1) Excluding Corporate. Effective 2009, we assign the centrally incurred cost of our

regional business management activities to the individual regions; the figures for

2008 have been adjusted accordingly

EBIT by region1)

in million euros

250

0

2009200920092009 2008200820082008

North AmericaEurope/Africa/

Middle East

Latin America Asia-Pacific

500

750

1,000

139

74

127

838

1,006

59

132

276

EBIT

in million euros

2009

2008200720062005

1,200

900

600

300

1,080

779

1,162

1,298 1,344

0

43

Annual Report 2009

Group management report » Business performance

shared services. The early implementation of the efficiency

enhancement measures resulted in benefits already accruing

in 2009, despite the difficult market environment.

One major aspect of the “Global Excellence” program

has been the consolidation of our liquid detergents manu-

facturing operation in Europe, initiated in 2008. However,

we avoided closure of the production facility in Genthin,

selling it instead to a third party with the majority of jobs

there being retained. Liquid detergent production has now

been transferred to Düsseldorf.

National Starch:

Integration of operational activities

Through the integration of the National Starch businesses,

we have been able to significantly improve Henkel’s product

and service portfolio for both existing and potential cus–

tomers in the global adhesives market. The integration of

customer relationships, our extended know-how in research

and development and a combination of the capabilities of

our two internationally successful organizations have cre-

ated an excellent basis for sustainable, profitable growth.

We accelerated the process of integrating the acquired

businesses in 2009. For 2011, we expect at least to achieve

the planned total synergies of 250 million euros.

Production consolidation, information technology and

revenue synergies constituted the focal areas of the 2009

integration program. By combining the product portfolios,

we have been able to expand our business with existing and

new customers, leveraging the potential available around

the world in the form of specific customer-related projects.

We have also succeeded in completing a number of major

production relocation projects. The implementation of the

measures still remaining is either running according to

schedule or has been expedited. Since the middle of 2009,

the IT systems of Henkel and those of the seller have been

operating independently. The rapid merger of the two orga–

nizations has facilitated simplification and acceleration of

the internal processes within the new organization. Looking

to the future, we intend to continue our systematic approach

in pursuing all synergy projects aligned to increasing sales

and profits.

Our integration work and focus in 2010 will be aligned

to further production relocations and revenue synergies.

The projects are due for completion in 2011, marking a

In North America, operating profit fell by 54.1 percent

(–56.2 percent after adjusting for foreign exchange). Due

to the difficult market environment, there was a substan–

tial decrease in profits at Adhesive Technologies, while the

consumer businesses Laundry & Home Care and Cosmetics/

Toiletries suffered only a slight decline. The return on sales de–

creased correspondingly, from 10.2 percent to 5.0 percent.

Operating profit in the Latin America region improved

by 25.1 percent. After adjusting for foreign exchange, profits

rose by 37.1 percent, with the encouraging results of Laundry

& Home Care and Adhesive Technologies making a major

contribution. Return on sales increased by 1.4 percentage

points to 9.0 percent.

The operating profit of the Asia-Pacific region rose by

5.6 percent (–0.9 percent after adjusting for foreign ex–

change). This is primarily due to the discontinuation of the

detergents business in China. The region’s return on sales

decreased slightly from 8.5 percent to 8.4 percent.

Further details relating to our business performance

can also be found in the reports dealing with the individual

business sectors starting on page 58.

“Global Excellence” restructuring program

In February 2008, Henkel announced the main framework

of a worldwide efficiency enhancement program under the

heading “Global Excellence.” This initiative had become nec–

essary due to changing market conditions, an increasingly

tough competitive environment and rising cost pressures.

“Global Excellence” encompasses a wide range of indi-

vidual measures in all our business sectors, regions and

functions around the world. In view of the economic crisis

of 2009, we accelerated the implementation of the program

so that, utilizing the entire volume of provisions made in

2008 in the amount of 504 million euros, we were able to

successfully complete “Global Excellence” before the end

of 2009.

While the original plan was to generate annual savings

of around 150 million euros from 2011, we now expect – as

a result of said accelerated implementation of the program

– to achieve this figure and possibly exceed it from 2010.

We introduced “Global Excellence” in order to strengthen

the long-term profitability and competitiveness of Henkel.

This initiative has enabled us to respond to changes in our

markets, improve our production network and expand our

44 Annual Report 2009

Group management report » Business performance

Other operating income and charges

The balance of other operating income and charges fell by

110 million euros. Income from the reversal of operating

provisions decreased compared to the previous year by 6 mil–

lion euros. Moreover, the income figure for the previous year

included gains from the sale of our water treatment business

amounting to 8 million euros. Reflected in the rise in other

operating charges are valuation adjustments with respect to

individual activities in the Adhesive Technologies business

sector. Planned closures or divestments of product lines led

to goodwill impairment losses of 46 million euros.

Financial result

The financial result for 2008 reflects a gain of 1,042 million

euros arising from the sale of our participating interest in

Ecolab Inc. Overall, the 2009 financial result decreased sig–

nificantly due to this one-time effect to –195 million euros.

Net interest improved by 84 million euros to –191 million

euros. Due to the rise in cash flow and the lack of major

acquisitions, we were able to substantially reduce our net

debt. Together with the lower interest rate levels prevailing,

this made a significant contribution to the improvement

in our net interest result.

Net earnings

Earnings before tax decreased by 45.6 percent to 885 million

euros due to the gain recognized in the previous year from

the sale of our Ecolab stake. Taxes on income amounted to

257 million euros. The tax rate was 29.0 percent. The lower

tax rate of 24.2 percent that applied in the previous year

was due in part to the lower rate payable on the at-equity

income from our Ecolab investment, and to the subsequent

sale of said investment.

Net earnings for the year decreased by 605 million euros

to 628 million euros. After deducting minority interests of

26 million euros, net earnings totaled 602 million euros.

Adjusted net earnings after minority interests, i.e. the figure

after allowing for one-time charges/gains and restructur–

ing charges, declined by 123 million euros to 822 million

euros.

The annual financial statements of the parent company

of Henkel AG & Co. KGaA are summarized on page 131.

further milestone as we consolidate our position as a world

leader in adhesives.

Expense items

The cost of sales for the year under review decreased by

9.5 percent, coming in at 7,411 million euros. Gross profit

increased to 6,162 million euros, which meant gross mar–

gin improved by 3.4 percentage points to 45.4 percent. It

was positively influenced by, in particular, the fall in raw

material prices, while a reduction in capacity utilization in

the Adhesive Technologies business sector compared to the

prior year had a burdening effect. Restructuring charges

arising from the efficiency enhancement measures and the

integration of the National Starch businesses were incurred

in both the year under review and in the previous year, and

these need to be taken into account in any comparison. The

allocation of the restructuring charges between the various

items of the income statement is explained on page 80.

After adjusting for restructuring charges, gross margin

amounted to 45.9 percent, 1.2 percentage points above the

adjusted prior-year figure.

The expense items discussed in the following were also

affected by the restructuring charges. It should also be noted

that the National Starch businesses acquired in the previous

year were not consolidated until April 2008.

At 3,926 million euros, marketing, selling and distribu–

tion expenses fell by 1.7 percent below the figure for the

previous year. After adjusting for restructuring charges, this

item remained roughly at the prior-year level.

Our research and development expenses totaled 396 mil–

lion euros, with the R&D ratio (i.e. research and develop–

ment expenses expressed as a proportion of sales) falling

0.1 percentage points below the prior-year figure of 3.0 per–

cent. After allowing for restructuring charges, the adjusted

R&D ratio rose compared to prior year by 0.1 percentage

points.

Administrative expenses decreased by 10.9 percent to

735 million euros. After adjusting for allocated restructur-

ing charges, administrative expenses increased slightly by

1.9 percentage points.

45

Annual Report 2009

Group management report » Business performance / Assets and financial analysis

The Stock Incentive Plan introduced in 2000 resulted in no

dilution of earnings per ordinary or preferred share as of

December 31, 2009.

Assets and financial analysis

Acquisitions and divestments

The Laundry&HomeCare business sector acquired the

remaining minority shares in a Tunisian joint venture for

a total of around 8 million euros.

As part of its ongoing portfolio streamlining operation,

the Cosmetics/Toiletries business sector disposed of a num–

ber of minor brands in the USA.

The AdhesiveTechnologies business sector increased

its shareholding in joint venture companies in Turkey and

China, expending a total of around 19 million euros. Its

major disposal in the year under review was of the North

American consumer adhesives business operated under the

Duck brand. The proceeds of the sale amounted to around

87 million euros.

Capital expenditures

Capital expenditures (excluding financial assets) amounted

to 415 million euros in the year under review. Investments

in property, plant and equipment for our continuing opera–

tions totaled 344 million euros, 129 million euros below the

level of the previous year. A major portion of these fixed asset

investments relates to the integration of the production and

IT facilities of the acquired National Starch sites (Adhesive

Technologies). A further portion of the expenditure went on

establishing and expanding production capacities and on

Dividends and distribution policy

The level of dividend distribution is primarily aligned to

earnings after deducting minority interests and exception–

al items. The payout ratio should be around 25 percent.

We intend to propose to the Annual General Meeting that

the dividends payable on both classes of share remain un-

changed. This will yield payouts of 0.53 euros per preferred

share and 0.51 euros per ordinary share, giving a payout

ratio of 27.6 percent.

Earnings per share (EPS)

Basic earnings per share are calculated by dividing earnings

after minority interests by the weighted average number of

shares outstanding during the reporting period. Earnings

per preferred share decreased from 2.83 euros to 1.40 euros

and earnings per ordinary share fell from 2.81 euros to

1.38 euros. Adjusted earnings per preferred share amounted

to 1.91 euros (previous year: 2.19 euros).

Net earnings

in million euros

0

2009

2008200720062005

250

500

750

1,000

628

1,233

770

871

941

Preferred share dividends1)

in euros

0.10

0

2009

2008200720062005

0.20

0.30

0.40

0.50

0.53

2)

0.50

0.53 0.53

0.45

1) Basis: share split (1:3) of June 18, 2007

2) Proposal

Earnings per preferred share1)

in euros

0.50

0

2009

2008200720062005

1.00

1.50

2.00

2.50

1.40

2.83

1.77

1.99 2.14

1) Basis: share split (1:3) of June 18, 2007

46 Annual Report 2009

Group management report » Assets and financial analysis

344 million euros, offset by depreciation of 377 million euros

and disposals with a book value of 63 million euros. Other

financial assets rose compared to the end of 2008 due pri-

marily to the positive fair values of interest rate derivatives

transacted in order to hedge our long-term borrowings.

Under current assets, there was a substantial decrease of

390 million euros in the combined totals of inventories and

trade accounts receivable, supported by our continuing strict

management of net working capital. Other current financial

assets fell by a total of 361 million euros, due primarily

to the cash pool settlement by the seller in respect of the

acquired National Starch businesses, and a decrease in the

fair values of financial derivatives. Conversely, liquid funds

increased by a substantial 772 million euros to 1,110 million

euros as a result of the strong cash flows generated by our

operating activities. Due to continuing uncertainties in the

financial markets, our focus in the year under review was

again on securing our liquidity. Assets held for sale decreased

substantially following the disposal of certain consumer

adhesive brands in the USA and Canada.

At 6,544 million euros, shareholders’ equity includ–

ing minority interests remained roughly at the prior-year

level. The changes are shown in detail in the statement of

changes in equity on page 83. The equity ratio increased

compared to the previous year by 1.1 percentage points to

41.4 percent.

Non-current liabilities rose overall by 914 million euros.

The increase is primarily due to the senior bond for 1.0 bil-

lion euros issued in March 2009. The funds generated were

used to repay short-term borrowings and to increase our

liquid funds.

Under current liabilities, there was a decrease in tax pro–

visions from 343 million euros to 224 million euros. This is

predominantly due to tax payments arising from the sale of

our Ecolab stake in November 2008. Short-term borrowings

decreased substantially from around 1.8 billion euros to 0.7

billion euros as a result of the financing measures indicated

above and also repayment of the remaining balance of the

bridge loan facility used to acquire the National Starch busi–

nesses. There was a countervailing rise of 207 million euros

in trade accounts payable as a further component of our

net working capital.

structural improvements such as the merger of our admin–

istrative and production sites. Among the major individual

projects of 2009 were the following:

» Expansion of capacity for construction-related prod–

ucts in Eastern Europe (Ukraine and Russia; Adhesive

Technologies).

» Completion of the new production and administrative site

in South Korea (Adhesive Technologies).

» Consolidation and concentration of our liquid detergent

manufacturing operation in Western Europe. In Germany,

relocation of production from Genthin to Düsseldorf, and

in Spain from Malgrat to Montornès (Laundry & Home

Care).

» Launch of the new detergent generation Purex Complete

3-in-1 in the USA (Laundry & Home Care).

» New production plant for the manufacture of bar and liq–

uid soaps in West Hazleton, Pennsylvania, USA (Cosmetics/

Toiletries).

» Commissioning of a new factory for liquid detergents in

Toluca, Mexico (Laundry & Home Care).

» Completion of the new main administrative center in

Greece (Cosmetics/Toiletries, Adhesive Technologies).

Capital expenditures 2009

in million euros Continuing

operations

Acquisitions Total

Intangible assets 28 40

68

Property, plant

and equipment 344 3

347

Total 372 43 415

In regional terms, the emphasis of our capital expenditures

in 2009 lay in North America and Europe.

Net assets

At 15.8 billion euros, the balance sheet total in 2009 was

slightly below that of the previous year. On the assets side,

a decline in intangible assets resulted from currency trans–

lation effects based on a lower US dollar exchange rate,

and the remeasurement of individual assets attributable

to the Adhesive Technologies business sector. Within the

also slightly lower property, plant and equipment total are

included capital expenditures in continuing operations of

47

Annual Report 2009

Group management report » Assets and financial analysis

“A3/P2” (Moody’s). The ratings are thus one notch lower

than at the end of 2008.

Credit ratings

Standard & Poor’s Moody’s

Long-term A– A3

Outlook Stable Stable

Short-term A–2 P2

At December 31, 2009

Our financial strategy is aligned to the single-A rating cat-

egory as a means of maintaining our financial flexibility.

We are endeavoring to upgrade our long-term credit rating

by one notch to A (Standard & Poor’s) and A2 (Moody’s). Cash

flows from operating activities and from divestments are

used to reduce our net debt exposure.

Essentially, we pursue a conservative borrowing policy,

again aligned to flexibility, within a balanced financial

portfolio. This is based on a core platform of syndicated

credit facilities and a multi-currency commercial paper

program.

At December 31, 2009, our long-term borrowings

amounted to 3.4 billion euros. Included in this figure are

the hybrid bond issued in November 2005 with a nominal

value of 1.3 billion euros, and the fixed-interest bonds is–

sued in May 2003 and March 2009, each with a volume of

1.0 billion euros.

Our short-term borrowings – i.e. those with maturities

of less than 12 months – amounted to 0.7 billion euros as of

the balance sheet date. These essentially comprise interest-

bearing loans and overdrafts from banks.

We considerably reduced net debt in the course of the fi–

nancial year, finishing at 2,799 million euros, a decrease of

993 million euros compared to the level of the previous year.

We define net debt as borrowings less liquid funds and – com–

mencing with the 2009 financial year – minus any positive

or plus any negative fair values of hedging contracts covering

those borrowings, providing that the underlying borrowings

are themselves subject to mark-to-market accounting.

Financing

The finances of the Group are, to a large extent, centrally

managed by Henkel AG & Co. KGaA. Financial funds consti–

tute a global resource and are, as a rule, centrally procured

and then allocated within the Group. The primary goals

of financial management are to secure the liquidity and

creditworthiness of the Group and to achieve a sustainable

increase in shareholder value. Our capital needs and capital

procurement activities are coordinated to ensure that the

requirements with respect to yield, liquidity, security and

independence are taken into account and appropriately bal–

anced. The cash flows not required for capital expenditures,

dividends and interest payments are used to reduce our

net debt. We cover our short-term financing requirement

primarily with commercial papers and bank loans. Our

bonds outstanding serve to cover our long-term financing

requirements.

Our creditworthiness is regularly checked by indepen-

dent rating agencies. Both Standard & Poor’s and Moody’s

currently categorize Henkel in the best possible category,

the Investment Grade Segment, with “A–/A–2” (S&P) and

Property, plant and equipment/Intangible assets

Financial assets

Other non-current assets

Liquid funds/Marketable securities

Shareholders’ equity

of which in % of which in %

Pension provisions

Other non-current liabilities

Short-term borrowings

Other current liabilities

1) Including assets held for sale 2008 2009 2009 2008

Balance sheet structure

in million euros Assets Shareholders’ equity and liabilities

15,818 16,173

15,818

16,173

Current assets1)

Long-term borrowings

66

67

41 41

0

0

55

5

3

22 15

22

28

6

6

7

2

411

22 22

48 Annual Report 2009

Group management report » Assets and financial analysis / Employees

We have used the inflowing funds arising from the increase

in long-term borrowings in order to repay short-term bor–

rowings and to increase our liquid funds.

The hybrid bond is treated by Moody’s as 75 percent

equity and by Standard & Poor’s as 50 percent equity. This

reduces the rating-specific borrowing ratios of the Group

(see adjacent key financial ratios table).

For further information on our financial steward–

ship and our financial instruments, please refer to Notes

41 and 42 to the consolidated financial statements on

pages 112 to 118.

Financial position

Cashflowfromoperatingactivities in 2009 amounted

to 1,919 million euros, an increase of 754 million euros

above the level of the previous year. Income tax payments

decreased due to a fall in advance tax payments. Positive

developments in net working capital, primarily during the

second half of 2009 with improvements in inventories, trade

accounts receivable and trade accounts payable, made a

significant contribution to the substantial increase in cash

inflow. With regard to other liabilities and provisions, the

main burden derived from payments in respect of restruc-

turing measures.

Cashflowfrominvestingactivities/acquisitions was

influenced by a reduction in capital expenditures on prop–

erty, plant and equipment compared to the previous year.

Further, the previous year had been characterized by high

cash outflows arising from the acquisition of the National

Starch businesses on the one hand, and proceeds from the

sale of our Ecolab stake on the other. The cash pool settle–

ment relating to the acquisition of the National Starch busi–

ness resulted in a cash inflow of 103 million euros in the

year under review.

Our cashflowfromfinancingactivities shows lower

and thus less burdensome outflows in the form of interest

payments, together with payments to reduce short-term

borrowings and higher pension fund contributions.

Liquidfunds/marketablesecurities increased as a re–

sult of the higher cash flow from operating activities, by

772 million euros to 1,110 million euros.

At 1,462 million euros, freecashflow is 1,005 mil–

lion euros above the comparable prior-year level, having

increased primarily due to the strong inflow of cash from

the management of our net working capital, reduced in–

vestments in property, plant and equipment, and lower

interest payments.

Key financial ratios

The interest coverage ratio, i.e. EBITDA divided by our net

interest expense, improved due to the twin effects of lower

interest outgoings and higher earnings before interest, tax,

depreciation and amortization. In the previous year, this

metric was burdened by charges arising from the efficiency

enhancement and integration measures and also – follow-

ing the acquisition of the National Starch businesses – an

increase in our interest expense.

The significant reduction in our net debt in 2009 has had

a beneficial effect on the debt coverage ratio. In the previ-

ous year, this metric was additionally boosted by the gain

from the sale of our Ecolab stake. The slightly higher equity

ratio is a reflection of the strengthening of our financing

structure in the year under review.

Key financial ratios

2008

2) 2009

Interest coverage ratio

(EBITDA/Net interest expense including

interest element of pension provisions)

4.8

8.7

Debt coverage ratio

(Net earnings + Amortization and

depreciation + Interest element of pension

provisions/Net borrowings and

pension provisions)1)

45.1 %

41.8 %

Equity ratio

(Equity/Total assets)

40.3 %

41.4 %

1) Hybrid bond included on 50 percent equity basis

2) Prior-year figures adjusted on the basis of the new definition of net borrowings

Employees

The number of people employed by Henkel at the end of the

reporting period was 49,262. In the course of the year, head–

count decreased by 5,880. Per capita sales increased further

to 264,300 euros. Henkel Group payroll costs decreased by

54 million euros to 2,382 million euros. The decrease in the

number of employees is due both to the “Global Excellence”

program and the synergies arising from the integration of

the National Starch businesses, with economic develop–

ments also exerting an influence. We responded to the latter

with specific countermeasures, for example with a highly

selective hiring policy and organizational adjustments. The

reductions in personnel in 2009 affected all our regions and

hierarchical levels; and as ever, they were implemented in

a socially responsible manner.

With the “Global Excellence” program introduced at the

beginning of 2008, Henkel responded very quickly to the ad–

vent of economic change. The resultant efficiency enhance–

ments and process optimizations already began to take effect

49

Annual Report 2009

Group management report » Employees

in this respect through the inclusion of dual studies as of

the start of the 2009 academic year. Here, students are able

to combine a course leading to a diploma granted by the

Chamber of Trade and Industry, with a bachelor degree at a

university, allowing them to obtain academic qualifications

combined with practical professional training.

One of the most important tasks undertaken by our

managers is that of developing our employees. Again in

2009, we focused specifically on the identification of high

potentials and ensuring their effective development. The

“Talent Management Process” introduced for senior man–

agement candidates in 2008 was extended in the year un–

der review to cover all managerial levels worldwide. This

involves groups of managers attending so-called “Develop-

ment Round Tables” chaired by their own line manager to

discuss the performance and potential of their employees on

the basis of global standards, and to decide on appropriate

further development measures. The managers pass on to

their employees the results of this evaluation in feedback

meetings, and together the two parties prepare individual

development plans which are then implemented on a joint

responsibility basis. An international training initiative was

carried out in order to prepare managers for these feedback

meetings.

2009 saw us significantly improve our performance-re-

lated compensation structure – i.e. the linkage between per–

sonal contribution and individual remuneration. We intend

to take this process forward in 2010 by providing regular

feedback on employee performance and target achievement,

in 2009. Regarding the integration of the National Starch

businesses, the main activities in 2009 involved the forma-

tion of a uniform and high-caliber organization exhibiting

a strong customer focus. All the employees incorporated as

a result of the acquisition have now been completely inte-

grated within our corporation and our compensation, per-

formance appraisal and personnel development systems.

In order to attract the best young talents, we maintain

a program of close collaboration with universities and fac-

ulty chairs. Our offerings in the form of workshops, case

studies and lectures are readily received and have resulted

in ever more applications from graduates with outstanding

qualifications. 2009 also saw the third of our innovation

competitions for students – the “Henkel Innovation Chal–

lenge” – successfully launched in twelve European countries.

This enabled us to gain extensive online and print media

coverage, positioning Henkel as an “employer of choice”

within the international environment.

A review of our hiring process, which has now been

extensively transferred to an online platform, led to more

internal efficiency and a more convenient application pro–

cess for candidates.

In Germany, Henkel offers apprenticeships and initial

qualifications at ten locations covering more than 20 profes–

sions. In all, we engaged 167 apprentices at Henkel’s German

sites in 2009. The number of applications rose considerably

compared to the previous year, indicating the level of attrac–

tiveness assigned to an apprenticeship and similar training

opportunities at Henkel. We extended our range of offerings

Employees by function

Marketing, selling

and distribution 32 %

Production and

engineering 49 %

Research and development 5 %

Administration 14 %

Employees by business sector

Adhesive

Technologies 49 %

Laundry & Home Care 23 %

Cosmetics/

Toiletries 15 %

Corporate 13 %

Group management report » Employees

Since 2005, an international team has been working on a Henkel-wide personnel data system. Today it already

provides the basis for standardized procedures in HR management. Each year, between 15 and 20 projects have

had to be managed concurrently on a worldwide basis. Whether in airports, the office, in a hotel or in a taxi,

telephone conferences across various time zones with local colleagues throughout the world were a permanent

feature of the everyday work of this young team from HR management and information technology.

From the left:

AndreasBender MarthaPereiras TianshuDeng FabricediFiore InaSchreckenberger JörgHeinen

Project Manager –

Europe and

North America

Change Manager and

Project Manager

Project Manager –

Europe/Africa/

Middle East

Program Manager –

Information Technology

Program Manager –

HR Management

Program Manager –

Information Technology

51

Annual Report 2009

Group management report » Employees / Procurement

were among the first signatories of their respective national

diversity charters, which constitute a public commitment

to diversity and inclusion. And our “Women in Leadership”

network has also laid the ground for a global mentoring

program at Henkel, due to be launched in 2010.

Procurement

Fiscal 2009 was again characterized by severe price volatility

in the procurement markets. Following the fall in the prices

of raw materials such as crude oil, ethylene, propylene,

palm kernel oil, metals and paper in the first quarter as a

consequence of the global economic crisis, the prices of, in

particular, petrochemical derivatives began to rise again by

the start of the second quarter. The average price level for

raw materials for the year as a whole was, however, below

that of the previous year. With a natural time lag, this also

had a beneficial effect on the costs of the raw materials and

packaging purchased by Henkel.

Our expenditures on direct materials (raw materials,

packaging, purchased goods and services) in the year under

review amounted to 5.9 billion euros, a fall of around 0.7 bil–

lion euros compared to the previous year. This is largely due

to lower production volumes coupled with the decrease in

prices for raw materials and packaging. 2009 was the first

full financial year to contain the procurement expenditures

of the National Starch businesses.

Aside from our ongoing efforts to negotiate new, com-

petitive contractual conditions, our global program aligned

to reducing overall procurement cost is a major factor in

the success of our sourcing strategy. We are permanently

engaged in reducing product complexity, optimizing our raw

material mix and promoting the further standardization of

packaging and raw materials. This gives us strong negotiat–

and by further developing the monetary reward systems in

place, taking into account aspects of differentiation and

competitiveness.

The development of our global team is a strategic priority

of Henkel and is therefore regarded as an important manage–

ment duty. Consequently, not only technical expertise but

also managerial competence are significant aspects in the

selection process applied to our managers. These undergo

regular training using our “Henkel Global Academy” re–

source with value-adding courses provided in collaboration

with international business schools. In 2009, we reviewed

the curriculum and now offer high-quality training events

covering general management requirements, together with

specific managerial and technical expertise. In developing

our managerial staff, we also make use of international as-

sessment centers that match the current competence profile

of the manager with future requirements, defining specific

measures for the further advancement of the personnel

concerned. As in the past, we endeavor to develop and pro-

mote managerial talent primarily from within. With a strict

selection process, we ensure that every candidate appointed

to a post satisfies our high quality criteria.

In 2009, the Management Board introduced a global

directive on Diversity & Inclusion, providing us with a uni-

form definition of both terms and a number of associated

implementation priorities. An international team of di–

versity ambassadors was also formed within the company.

Their task is to instigate and implement local projects and

initiatives on this theme. In 2009, activities included a Di-

versity Day in the USA and a cross-generation mentoring

program in Belgium. Our subsidiaries in Italy and Spain

Management structure

Senior executive personnel

Female 15 %

Expenditures by type

Raw materials 61 %

Contract manufacturing

and traded goods 19 %

52 Annual Report 2009

Group management report » Procurement / Production

Production

Henkel operates 203 production sites in 57 countries. Our

biggest site is located in Düsseldorf, Germany. Here we manu–

facture not only detergents and household cleaners but also

adhesives for consumers and craftsmen, and products for

our industrial customers.

Our Düsseldorf plant is also the largest production site of

the Laundry & Home Care business sector. Here we predomi–

nantly manufacture powder and liquid detergents, fabric

softeners and liquid cleaning products. To enable transfer

of production from Genthin to Düsseldorf, we substantially

expanded our capacity in the course of 2009 through the

construction of a modern liquid detergent manufacturing

facility. We reduced the number of production sites around

the world to 33 last year. Through concentrating our deter–

gent production on just a few high-performing factories, we

have been able to generate substantial cost advantages.

Our biggest plant for manufacturing products for the

Cosmetics/Toiletries business sector is located in Wasser–

trüdingen, Germany. In addition to body and hair care prod–

ucts for consumers, we also manufacture products for the

salon business here. With the sale of a production facility

in the USA and one in India, and closure of two factories

in China, the business sector is efficiently structured with

eight factories worldwide. We expect further efficiency en–

hancements through the expansion of production sites with

a more regional responsibility – our “regional hubs” – in

Columbia and Thailand.

The two largest sites for Adhesive Technologies are like–

wise located in Germany: in Düsseldorf – with a portfolio of

high-quality specialty adhesives for industry and consumers

– and in Heidelberg where we manufacture a wide range of

adhesives and sealants. In the course of our “Global Excel–

lence” program and the integration of the National Starch

businesses, we have over the last two years significantly

consolidated our production network, closing 30 factories,

therefore reducing the number to 162. In 2010, we intend

to continue the optimization of our global manufacturing

capability and to undertake further production transfers

to more efficient locations.

We have improved our production network throughout

the Group as part of the efficiency enhancement programs

respect to manufacturing, logistics, quality and innovation.

We support this program with individual target agreements

involving our strategically important suppliers.

Against the background of persistently high price vola-

tility in the procurement and financial markets and the

tense economic situation, one important element of our

sourcing strategy is that of expanding our integrated and

all-encompassing risk management capability. As part of

our active price management approach, we establish strate–

gies for safeguarding prices over the longer term both on a

contractual basis and – where appropriate and possible – by

means of financial hedging instruments. We also systemati–

cally analyze the effects of currency fluctuations on procure–

ment costs and introduce corresponding countermeasures

to reduce foreign exchange risks. We constantly monitor our

vendor portfolio in order to minimize the risks of financial

failure among our suppliers. If a vendor is considered to be

in a critical state, we systematically prepare back-up plans

in order to ensure consistency of supply.

Our five most important raw material groups are surfac–

tants, raw materials for polyurethane-based adhesives, raw

materials for aqueous adhesive systems, raw materials for

use in hotmelt adhesives, and inorganic raw materials for

use e.g. in detergents and surface treatment products. These

account for around 30 percent of our total direct materials

expenditure. Our five largest suppliers account for around

11 percent of our cost of direct materials.

Our annual expenditure on indirect materials and ser–

vices, plus logistics, amounts to some 3.4 billion euros, or

around one third of total procurement expenditures at

Henkel. Here we have been able to reduce procurement

prices in all areas compared to the previous year through the

introduction of savings measures. These have been initiated

both regionally and globally in all the relevant categories

on the basis of procurement strategies extending across the

entire corporation.

Expenditures by business sector

Laundry & Home Care 32 %

Adhesive Technologies 47 %

Group management report » Production / Research and development

As an annual average, the number of employees working

in research and development at our sites around the world

was 2,743 compared to 2,942 in 2008. The main reasons

for this decline lay in the “Global Excellence” efficiency

enhancement program initiated in 2008 and the associated

dissolution of our Corporate Research division, coupled with

the integration of the National Starch businesses.

We have stepped up our drive toward open innovation

– i.e. the increased inclusion of universities, institutes, sup–

pliers and customers within our innovation process – as part

of our worldwide research and development strategy. To this

end, we have also increased the funds available for collabora–

tion with external partners. Three examples indicate the kind

of successes that can be achieved with this approach:

In cooperation with the Fraunhofer Institute for Manu-

facturing Technology and Applied Materials Research in

Bremen, Germany, and a leading automobile manufacturer,

our Adhesive Technologies business sector has developed a

new generation of energy-absorbing structural adhesives

for composite materials.

In conjunction with the launch of our automatic dish-

washing detergent Somat 9, we together with Cognis gar–

nered the 2009 Best Innovation Contributor Award for the

development of a unique surfactant for improved dishwasher

drying performance. In addition, Symrise AG has provided

a completely new fragrance technology for Somat 9 to neu–

tralize unpleasant odors.

nological platform for the relaunch of Bonacure, our biggest

salon hair care brand for professional hairdressers.

complexity within the overall value chain with respect to

both production and logistics, adding simplicity in product

manufacturing and in our vendor selection processes. As a

result, we have been able to substantially increase efficiency

and reduce cost.

Our optimization activities are also aligned to making

our manufacturing operations ever more environmentally

reducing our carbon footprint. For further details relating

to the development of our environmental parameters, please

refer to the sustainability/corporate social responsibility

section on page 56.

The current and planned measures are expected to con–

tribute equally to cost optimization and improved sustain-

ability. The main priorities are to achieve additional savings

in resources with respect to raw materials and packaging,

to introduce further improvements in the supply chain and

to make greater use and improve the technology of our IT

capability for planning and control.

Research and development

Expenditures on research and development at Henkel

amounted to 396 million euros in the year under review,

compared to 429 million euros in 2008. After adjusting for

restructuring charges, the 2009 figure was 383 million euros

compared to 377 million euros in the previous year. The R&D

share of sales was 2.9 percent (adjusted: 2.8 percent) following

3.0 percent in 2008 (adjusted: 2.7 percent). This demonstrates

that, even in this difficult economic environment, we man–

aged to maintain our expenditures on research and develop–

ment at a high level, conscious of the fact that innovations

are an important driver of profitable growth.

R&D expenditures by business sector

Laundry & Home Care 26 %

R&D expenditures

in million euros

200

300

400 3961)

4291)

324 340 350

54 Annual Report 2009

Group management report » Research and development

» Further development of TecTalis, a new high-performance

generation of pretreatment products free of heavy metals

for the automotive industry

All the new developments and products exhibit an improved

sustainability profile, particularly in the form of lower en-

ergy consumption, the increased use of renewable raw ma–

terials and/or a reduced waste footprint.

Each year we select a number of outstanding develop–

ments for our Fritz Henkel Award for Innovation. In 2009,

this accolade went to three interdisciplinary project teams

in recognition of their efforts in the realization and com–

mercialization of the following concepts:

» PurexComplete3-in-1LaundrySheets: Setting a com–

pletely new set of performance standards, Purex Complete

3-in-1 laundry sheets offer an innovative combination of a

laundry detergent – significantly more concentrated than

the market standard – with a fabric softener and an anti-

static compound to prevent the build-up of charge in the

drier. This unique product concept is a further successful

example of the strategy adopted by our Laundry & Home

Care business sector of offering consumers outstanding,

innovative product performance accompanied by high

environmental compatibility – Quality & Responsibility.

» Ammonia-freePermanentColorantsSchwarzkopfEs–

sentialColorandEssensity: With Essential Color (for

consumers) and Essensity (for the salon sector), the ex–

perts from Schwarzkopf have succeeded for the first time

in developing a permanent colorant with no ammonia

whatsoever, offering optimum hair care with a maximum

of natural-derived raw materials. Essential Color, our first

100 percent permanent hair colorant without ammonia

and with nature-based ingredients such as lychee and white

tea, offers an intensively radiant color with long-lasting

gray coverage. And, for the professional hairdresser, Es–

sensity is the first colorant without ammonia, fragrance,

silicones or preservatives capable of ensuring a permanent

effect with 100 percent gray coverage. Essensity – 100 per–

cent performance, 0 percent compromise.

» TechnomeltSupraCool130: A newly developed hotmelt

adhesive for packaging that combines the best of both

After ten years of successful research collaboration, we have

allowed our contract with Henkel Kindai Laboratories in

Japan to expire, and have instead launched a number of

special projects with Japan’s top universities.

Following the successful integration of the National

Starch businesses, the Adhesive Technologies business sector

has restructured its research portfolio with the intention to

concentrate on larger projects and thereby increase both its

innovation rate and the number of breakthrough innova–

tions available to the business sector.

Our scientists have made valuable contributions to our

corporate success in the following areas:

» Development of ammonia-free permanent hair colorants

with certain natural-based ingredients for home and salon

applications

» Joint development of “Dermo-Ident” technology with

the beauty expert Dr. Caspari for innovative anti-aging

cosmetics

» Development of Dial Anti-Ox, a new body wash with

cran berry extract and vitamin E pearls as an active anti-

oxidative complex – the USA’s most successful launch in

this category in 2009

» Development of an innovative capsule technology for the

optimum release of fragrances, particularly for laundry

detergent additives

» Development of a new surfactant with a substantially

improved drying effect for use particularly in machine

dishwasher detergents

» Development of Purex Complete 3-in-1, a product com–

prised of laundry detergent, fabric softener and an anti-

static compound

» Development of halogen-free structural adhesives for mo–

bile devices

» Development of Pattex No More Nails Invisible – a high-

performance adhesive that dries to a transparent finish

Major R&D sites

Düsseldorf, Germany

Dublin, Ireland

Shanghai, China

Hamburg, Germany

Rocky Hill, USA

Irvine, USA

Vienna, Austria

55

Annual Report 2009

Group management report » Research and development / Marketing and distribution

and technical advice in the salons. As an additional service,

we also offer specialist seminars and training courses in our

50-plus Schwarzkopf academies worldwide.

Our Adhesive Technologies business sector serves a wide

range of clientèle from large, internationally active corpo-

rations to small and medium-sized industrial businesses,

craftsmen, do-it-yourselfers and private home consumers,

all with specific needs and applications.

For the most part, our customers are addressed by our

own sales personnel. Our direct customers are industrial

clients and retail companies; these latter are able to meet

demand from private users and craftsmen more efficiently

than is possible through direct sales. While the grocery

retailers, DIY stores and specialist retailers are of great

importance for the private user, craftsmen purchase our

products primarily from specialist wholesalers. Due to our

unique global position, we are able to support internation–

ally active customers such as automobile manufacturers or

large retail chains effectively and comprehensively with key

account management teams. As many of our products are

characterized by their high technical complexity, our Tech–

nical Customer Services and the training of users also have

an important role to play. Our Technical Customer Services

people have detailed knowledge both of the properties of

our products and of their application, and can therefore

assist our customers in everything from the choice of the

right product and its usage to fine adjustment of their pro–

duction processes.

The close contact maintained by our employees with our

customers and users is also an important source of input

for innovation and development, enabling us to meet exist–

ing requirements even more effectively and develop new

applications for our adhesives.

For us, communication with end users is of central im-

portance. While we develop our marketing strategy at the