Insuring Your Life

Chapter 8

How Will This Affect Me?

Insurance should be used only to protect against potentially catastrophic losses, not for small risk

exposures. It should cover losses that could derail your family’s future. It balances the relatively

small, certain loss of ongoing premiums against low-probability, high-cost risks. This chapter

focuses on how to go about buying life insurance. Premature death is clearly a catastrophic loss

that could endanger your family’s financial future. We start by explaining how to determine the

amount of life insurance that is right for you. We also consider how to choose among key

insurance products, which include term life, whole life, universal life, variable life, and group

life policies. The key features of life insurance contracts are explained, and frameworks for

choosing an insurance agent and an insurance company are presented. The chapter will help you

prepare to make informed life insurance decisions.

Learning Objectives

8-1 Explain the concept of risk and the basics of insurance underwriting.

8-2 Discuss the primary reasons for life insurance and identify those who need coverage.

8-3 Calculate how much life insurance you need.

8-4 Distinguish among the various types of life insurance policies and describe their advantages

and disadvantages.

8-5 Choose the best life insurance policy for your needs at the lowest cost.

Choosing the best life insurance to fulfill the need is the second primary topic for this chapter.

Most likely term insurance will be the winner. [My bias, as a side note my wife says only buy

8-6 Become familiar with the key features of life insurance policies.

Financial Facts or Fantasies?

These may be used as “teasers” to get the students on the right page with you. Also, they may be

used as quizzes after you covered the material or as “pre–test questions” to get their attention.

• Term insurance provides nothing more than a stipulated amount of death benefits and, as a

result, is considered the purest form of life insurance.

Fact: Term insurance provides a given amount of life insurance (i.e., death benefits) for a

stipulated period of time and nothing more – no investments feature or cash value.

• Selecting an insurance company is the first thing you should do when buying life insurance.

Fantasy: The first thing you should do is determine the amount of life insurance you need and

then select the type of policy that is best for you. Only after you have taken these steps should

Financial Facts or Fantasies?

These may be used as a quiz or as a pre-test to get the students interested. The questions are the

same as above, just in the form of a quiz.

1. True False The best way to figure out how much life insurance you need is to

use a multiple of your earnings.

2. True False Social security survivor’s benefits should be factored into your life

insurance plans if you have a dependent spouse and/or minor

children.

3. True False Term insurance provides nothing more than a stipulated amount of

death benefits and, as a result, is considered the purest form of life

insurance.

4. True False Selecting an insurance company is the first thing you should do

when buying life insurance.

5. True False Because most life insurance policies are largely the same, you need

not concern yourself with differences in specific contract provisions.

Answers:

YOU CAN DO IT NOW

The “You Can Do It Now” cases may be assigned to the students as short cases or problems.

They will help make the topic more real or relevant to the students. In most cases, it will only

take about ten minutes to do, that is, until the student starts looking around at the web site. But

they will learn by doing so.

Shop for a Customized Life Insurance Policy

Let’s make life insurance more concrete and personal. You can easily get an insurance quote

online. Go to the popular Internet site noted in this chapter, http://www.insure.com/life-

insurance/, and provide the requested personal information. Then request a quote for a 20-year,

$200,000 term life insurance policy – you can do it now.

Check Out the Best Life Insurance Companies

The ratings of the best life insurance companies and an overall ranking, known as the Comdex

rank, are provided online at http://toplifeinsurancereviews.com/comdex-ranking-life-

insurance/. Go to the site and jot down the top five life insurance companies. Now you have a

great start when you are ready to shop for life insurance – you can do it now.

Buy term and invest the difference is a frequently stated plan. The “Financial Impact of Personal

Choices” below demonstrates this plan and can be used to discuss buy term and invest the

difference.

Financial Impact of Personal Choices

Amber and Josh Consider “Buying Term and Investing the Rest”

Amber and Josh Peterson have two young children and believe it’s time to buy a life insurance

policy to protect their family. They’ve both heard the life insurance advice to “buy term and

invest the rest.” In order to evaluate this advice, they’ve collected quotes for 20-year term and

whole life policies on Josh, both with a payoff of $250,000. The whole life policy premium is

$347 a month while the term policy premium is only $23 a month. In 20 years the whole life

policy will have a guaranteed cash value of $70,018 but at current rates would be worth

$105,721. The death benefit will have grown to $326,352. If the Petersons buy the term policy

and invest the $324 difference in monthly premiums at 8% for 20 years, they could have a

portfolio worth about $190,843!

The Petersons wonder about the financial consequences of their decision. It looks like buying

term and investing the difference leaves the Petersons better off. Yet the financial consequences

can only be fully evaluated in light of the Peterson’s objectives and attitude towards risk. The

whole life insurance policy provides a guaranteed cash value in 20 years while the invested

difference produces a higher expected but risky, unguaranteed payoff. And the Peterson’s must

consider whether they will have the discipline to keep “investing the difference” over the next 20

years. Once the whole life policy’s cash value builds up, they could stop paying the premium by

accepting some trade-offs in the value of the policy. In 20 years the term life insurance coverage

will go away, which might be fine if the kids are gone and the mortgage is paid off. In contrast,

the Petersons could stop paying the whole life policy premiums then and accept a reduced paid-

up amount of coverage.

The personal financial consequences of “buy term and invest the rest” suggest the advice may

well work for the Petersons. But the best decision depends on their objectives, discipline, and

attitude towards the risks of “investing the rest.”

Source: Adapted from Chris Arnold, “Life Insurance: Is Buying Term and Investing the

Difference Your Best Approach?”

Financial Planning Exercises

Planning Exercises

1. Deciding if additional life insurance is needed and, if so, appropriate type. Use Worksheet

8.1. Harvey Cook, 45, is a recently divorced father of two children, ages 10 and 7. He

currently earns $95,000 a year as an operations manager for a utility company. The divorce

settlement requires him to pay $1,500 a month in child support and $400 a month in

alimony to his ex-wife. She currently earns $35,000 annually as a schoolteacher. Harvey is

now renting an apartment, and the divorce settlement left him with about $100,000 in

savings and retirement benefits. His employer provides a $75,000 life insurance policy.

Harvey’s ex-wife is currently the beneficiary listed on the policy.

What advice would you give to Harvey? What factors should he consider in deciding

whether to buy additional life insurance at this point in his life? If he does need additional

life insurance, what type of policy or policies should he buy? Use Worksheet 8.1 to help

answer these questions for Harvey.

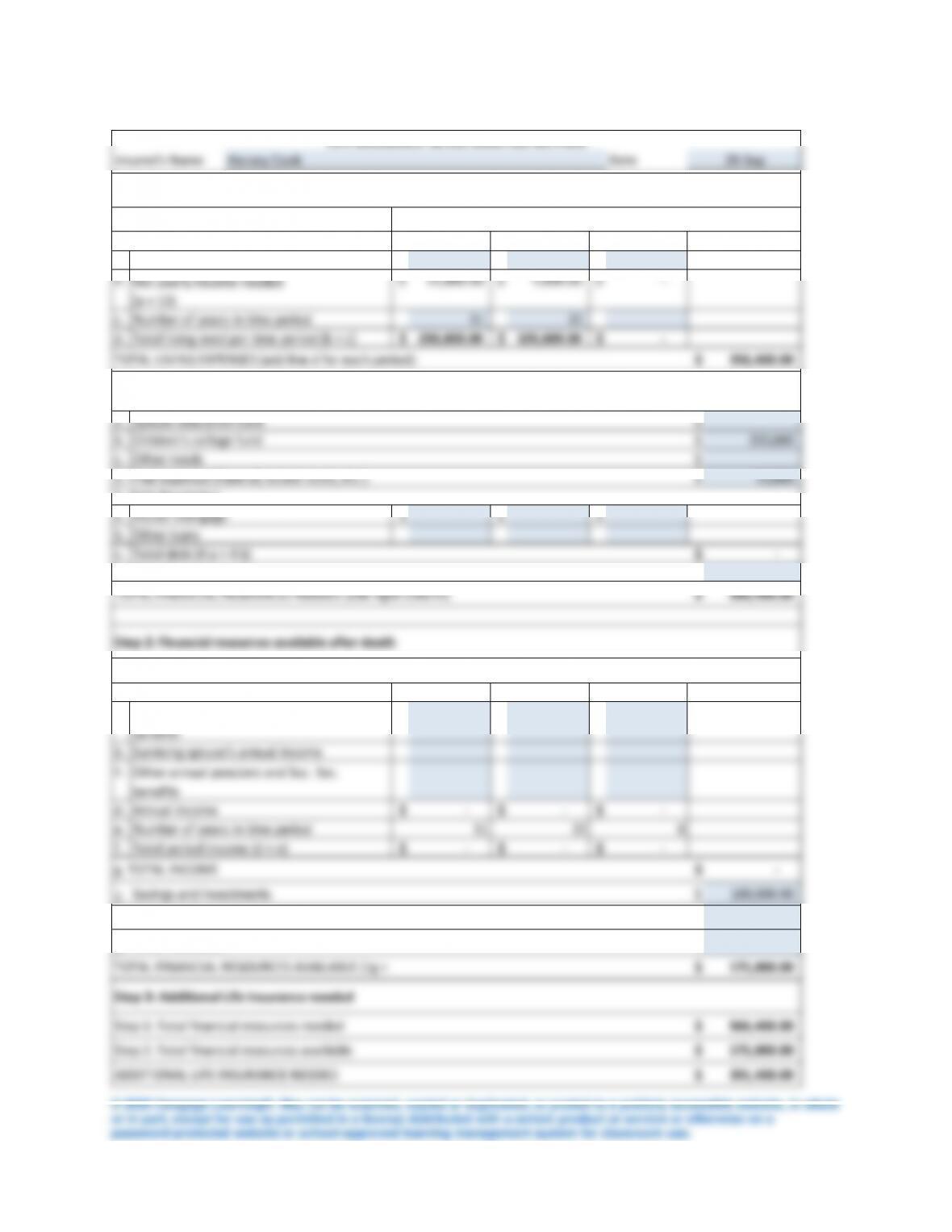

See Worksheet 8.1 below.

In 11 years, both kids will be in college. The funds for college will be available from savings

and not need life insurance. Also, child support payments stop. So when reaches 56 [45 + 11]

Date

a. $ 1,900

$

400 $

b.

c. 11 22

d.

1. Income

TOTAL FINANCIAL RESOURCES NEEDED (add right column)

566,400.00$

Other loans

Total debt (4 a + 4 b)

5. Other financial needs

Children’s college fund

Other needs

3. Final expenses (funeral, estate costs, etc.)

Period 2

Period 3

Period 1

a. $ $

b.

c.

d.

e.

f.

Step 1: Total financial resources needed

Other life insurance

Step 3: Additional Life Insurance needed

566,400.00$

Total period income (d × e)

Step 2: Total financial resources available

ADDITIONAL LIFE INSURANCE NEEDED

g. TOTAL INCOME

391,400.00$

175,000.00$

–$

Annual Social Security survivor’s

benefits

Surviving spouse’s annual income

Other annual pensions and Soc. Sec.

benefits

Annual income

Number of years in time period

Total living need per time period (b × c)

TOTAL LIVING EXPENSES (add line d for each period):

2. Special needs

22,800.00$

250,800.00$

356,400.00$

4,800.00$

105,600.00$

Period 1

Period 2

Net yearly income needed

(a × 12)

Number of years in time period

LIFE INSURANCE NEEDS ANALYSIS METHOD

Insured’s Name

Step 1: Financial resources needed after death

1. Annual living expenses and other needs:

20-Sep

Harvey Cook

–$

Period 3

–$

–$

Monthly living expenses

–$

22

–$

–$

11

–$

0

–$

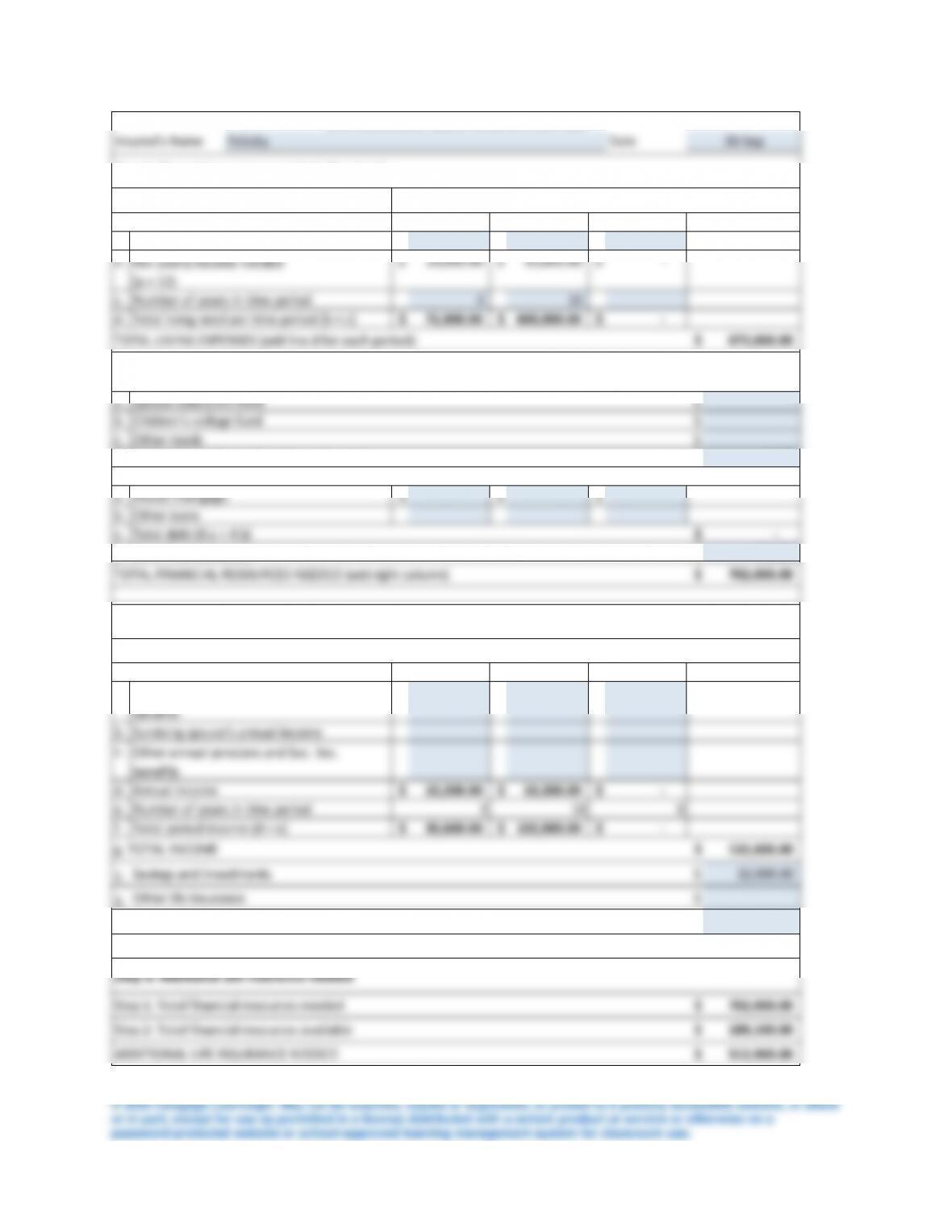

2. Estimating life insurance needs. Use Worksheet 8.1. Sophie Lopez is a 72-year-old widow

who has recently been diagnosed with Alzheimer’s disease. She has limited financial assets

of her own and has been living with her daughter Felicity for two years. Her only income is

$850 a month in Social Security survivor’s benefits. Felicity wants to make sure her mother

will be taken care of if Felicity should die prematurely. Felicity, 40, is single and earns

$55,000 a year as a human resources manager for a small manufacturing firm. She owns a

condo with a current market value of $100,000 and has a $70,000 mortgage. Other debts

include a $5,000 auto loan and $500 in various credit card balances. Her 401(k) plan has a

current balance of $24,500, and she keeps $7,500 in a money market account for

emergencies.

After talking with her mother’s doctor, Felicity believes that her mother will be able to

continue living independently for another two to three years. She estimates that her mother

would need about $2,000 a month to cover her living expenses and medical costs during

this time. After that, Felicity’s mother will probably need nursing home care. Felicity calls

several local nursing homes and finds that it will cost about $5,000 a month when her

mother enters a nursing home. Her mother’s doctor says it is difficult to estimate her

mother’s life expectancy but indicates that with proper care some Alzheimer’s patients can

live 10 or more years after diagnosis. Felicity also estimates that her personal final

expenses would be around $5,000, and she’d like to provide a $25,000 contingency fund

that would be used to pay a trusted friend to supervise her mother’s care if Felicity were no

longer alive.

Use Worksheet 8.1 to calculate Felicity’s total life insurance requirements and recommend

the type of policy that she should buy.

Step 2: Total financial resources available

ADDITIONAL LIFE INSURANCE NEEDED

Other life insurance

Other resources

TOTAL FINANCIAL RESOURCES AVAILABLE (1g + 2

Step 3: Additional Life Insurance needed

189,100.00$

189,100.00$

Date

a. $ 2,000

$

5,000 $

b.

c. 3 10

d.

a. $

b. $

TOTAL FINANCIAL RESOURCES NEEDED (add right column)

House mortgage

Other loans

Total debt (4 a + 4 b)

5. Other financial needs

Other needs

3. Final expenses (funeral, estate costs, etc.)

4. Debt liquidation

Annual Social Security survivor’s

Period 2

Period 3

Period 1

b.

c.

d.

e.

f.

2. $ 32,000.00

Total period income (d × e)

g. TOTAL INCOME

Savings and investments

132,600.00$

benefits

Surviving spouse’s annual income

Other annual pensions and Soc. Sec.

benefits

Annual income

Number of years in time period

1. Income

Step 2: Financial resources available after death

Spouse education fund

Children’s college fund

Total living need per time period (b × c)

TOTAL LIVING EXPENSES (add line d for each period):

2. Special needs

24,000.00$

72,000.00$

672,000.00$

60,000.00$

600,000.00$

Period 1

Period 2

Net yearly income needed

(a × 12)

Number of years in time period

LIFE INSURANCE NEEDS ANALYSIS METHOD

Insured’s Name

Step 1: Financial resources needed after death

1. Annual living expenses and other needs:

20-Sep

Felicity

10,200.00$

Period 3

–$

–$

Monthly living expenses

102,000.00$

10

–$

30,600.00$

3

–$

0

10,200.00$

3. Appropriateness of whole life insurance. Martha and Louis Mitchell are a dual-career

couple who just had their first child. Louis age 30, already has a group life insurance

policy, but Martha’s employer does not offer a life insurance benefit. A financial planner is

recommending that the 27-year-old Martha buy a $250,000 whole life policy with an annual

premium of $1,670 (the policy has an assumed rate of earnings of 5 percent a year). Help

Martha evaluate this advice and decide on an appropriate course of action.

4. Appropriateness of variable life insurance. While at lunch with a group of coworkers,

one of your friends mentions that he plans to buy a variable life insurance policy because it

provides a good annual return and is a good way to build savings for his 5-year-old’s

college education. Another colleague says that she’s adding coverage through the group

plan’s additional insurance option. What advice would you give them?

A variable life insurance policy goes further than whole and universal life policies in

combining death benefits and savings. The policyholder decides how to invest the money in the

5. Choosing among types of life insurance. Camila Rodriguez, a 38-year-old widowed

mother of three children (ages 12,10, and 4), works as a product analyst for a major

consumer products company. Although she’s covered by a group life insurance policy at

work, she feels, based on some rough calculations, that she needs additional protection.

Leon Thompson, an insurance agent from Insurance Advisers, has been trying to persuade

her to buy a $150,000, 25-year, limited payment whole life policy. However, Camila favors

a variable life policy. To further complicate matters, Camila’s father feels that term life

insurance is more suitable to the needs of her young family.

a. Explain to Camila the differences between (i) a whole life policy, (ii) a variable life

policy, and (iii) a term life policy.

(i) Whole life policy: Policy provides insurance and many options such as single premium, paid

b. What are the major advantages and disadvantages of each type of policy?

Exhibit 8-8 lists the major advantages and disadvantages of the various types of life insurance.

Type of Policy

Advantages

Disadvantages

Term

Low initial premiums

Simple, easy to buy

Provides only temporary coverage for a set

period

May have to pay higher premiums when

policy is renewed.

Whole Life

Permanent coverage

Savings vehicle: cash value

builds as premiums are paid

Some tax advantages on

accumulated earnings

Cost: provides less death protection per

premium dollar than term

Often provides lower yields than other

investment vehicles

Sales commissions and marketing expenses

can increase costs of fully loaded policy.

Universal Life

Permanent coverage

Flexible: lets insured adapt

level of protection and cost

of premiums Savings

vehicle: cash value builds at

current rate of interest

Savings and death protection

identified separately

Can be difficult to evaluate true cost at time

of purchase; insurance carrier may levy

costly fees and charges

Interest rate changes may adversely affect

future cash values or expected premium

payments, which may even cause the policy

to lapse

Variable Life

Investment vehicle: insured

decides how cash value will

be invested

Higher risk

c. In what way is a whole life policy superior to either a variable life or term life policy? In

what way is a variable life policy superior? How about term life insurance?

d. Given the limited information in the case, which type of policy would you recommend

for Camila? Explain your recommendation.

6. Life insurance premiums and comparison of types. Using the premium schedules

provided in Exhibits 8.2, 8.3, and 8.5, how much in annual premiums would a 25-year-old

male have to pay for $100,000 of annual renewable term, level premium term, and whole

life insurance? (Assume a five-year term or period of coverage.) How much would a 25-

year-old woman have to pay for the same coverage? Consider a 40-year-old male (or

female): Using annual premiums, compare the cost of 10 years of coverage under annual

renewable and level premium term options and whole life insurance coverage. Relate the

advantages and disadvantages of each policy type to their price differences.

Policy is $100,000, for 10 years

Insured

Annual renewable term

Level premium term

Whole life insurance

25-yr male

$164 * 5 + $167 * 5 =

$1,655

$120* 10 = $1,200

$1,057 * 5 + $1,218 *

5 = $11,375

25-yr female

$143 * 5 + $150 * 5 =

$1,465

$108* 10 = $1,080

$956 * 5 + $1,099 * 5

= $10,275

40-yr male

$188 * 5 + $228 * 5 =

$2,080

$144* 10 = $1,440

$1,749 * 10 =

$17,490

40-yr female

$178 * 5 + $225 * 5 =

$2,015

$135* 10 = $1,350

$1,499 * 10 =

$14,990

7. Using Insurance policy illustrations. Describe the key elements of an insurance policy

illustration and explain what a prospective client should focus on in evaluating an

illustration.

Test Yourself Questions

8-1 Discuss the role that insurance plays in the financial planning process. Why is it

important to have enough life insurance?

8-2 Define (a) risk avoidance, (b) loss prevention, (c) loss control, (d) risk assumption, and (e)

an insurance policy. Explain their interrelationships.

a. risk avoidance — Avoiding an act that would create a risk. Risk avoidance is an attractive

way to deal with risk only when the estimated cost of avoidance is less than the estimated cost of

8-3 Explain the purpose of underwriting. What are some factors that underwriters consider

when evaluating a life insurance application?

8-4 Discuss some benefits of life insurance in addition to protecting family members

financially after the primary wage earner’s death.

8-5 Explain the circumstances under which a single college graduate would or would not

need life insurance. What life-cycle events would change this initial evaluation, and how

might they affect the graduate’s life insurance needs?

8-6 Discuss the two most commonly used ways to determine a person’s life insurance needs.

You can use one of two methods to estimate how much insurance is necessary: the multiple-of–

earnings method and the needs analysis method. The multiple-of-earnings method takes your

1. Estimate the total economic resources needed if the individual were to die.

8-7 Name and explain the most common financial resources needed after the death of a

family breadwinner.