Using Consumer Loans

Chapter 7

How Will This Affect Me?

Learning Objectives

6-1 Know when to use consumer loans and be able to differentiate between the major types.

6-2 Identify the various sources of consumer loans.

6-3 Choose the best loans by comparing finance charges, maturity, collateral and other loan

terms.

6-4 Describe the features of, and calculate the finance charges on, single-payment loans.

6-5 Evaluate the benefits of an installment loan.

6-6 Determine the costs of installment loans and analyze whether it is better to pay cash or take

out a loan.

Financial Facts or Fantasies?

These may be used as “teasers” to get the students on the right page with you. Also, they may be

used as quizzes after you covered the material or as “pre–test questions” to get their attention.

• An S&L is the only type of financial institution that is prohibited from making consumer loans.

Fantasy: Financial deregulation opened up the consumer loan market to S&Ls and they are an

important source of such credit.

• Single-payment loans are often secured with some type of collateral and are usually relatively

short-term in duration (maturities of one year or less).

Fact: Because these loans require only one payment at maturity, banks and other lenders

generally keep them fairly short-term and often require some type of collateral.

Financial Facts or Fantasies?

These true/false questions may be used as quizzes or as pretest to get the students’ attention.

1. True False Buying a new car is the major reason that people borrow money through

consumer loans.

2. True False Consumer loans can be set up with fixed rates of interest or with variable

loan rates.

3. True False An S&L is the only type of financial institution that is prohibited from

making consumer loans.

4. True False Single-payment loans are often secured with some type of collateral and

are usually relatively short-term in duration (maturities of one year or

less).

5. True False Using the discount method to figure interest is one way of lowering the

effective cost of a consumer loan.

6. True False The Rule of 78 is a regulation that grew out of the Consumer Credit

Enhancement Act of 1978 and mandates how installment loans will be set

up.

Answers:

YOU CAN DO IT NOW

The “You Can Do It Now” cases may be assigned to the students as short cases or problems.

They will help make the topic more real or relevant to the students. In most cases, it will only

take about ten minutes to do, that is, until the student starts looking around at the web site. But

they will learn by doing so.

Current Auto Loan Rates

Financial Impact of Personal Choices

Read and think about the choices being made. Do you agree or not? Ask the students to discuss

the choices being made.

Ann and Ezra Calculate their Auto Loan Backwards

Financial Planning Exercises

1. Student loan options. Scarlett Hill is a sophomore at State College and is running out of

money. Wanting to continue her education, Scarlett is considering a student loan. Explain

her options. How can she minimize her borrowing costs and maximize her flexibility?

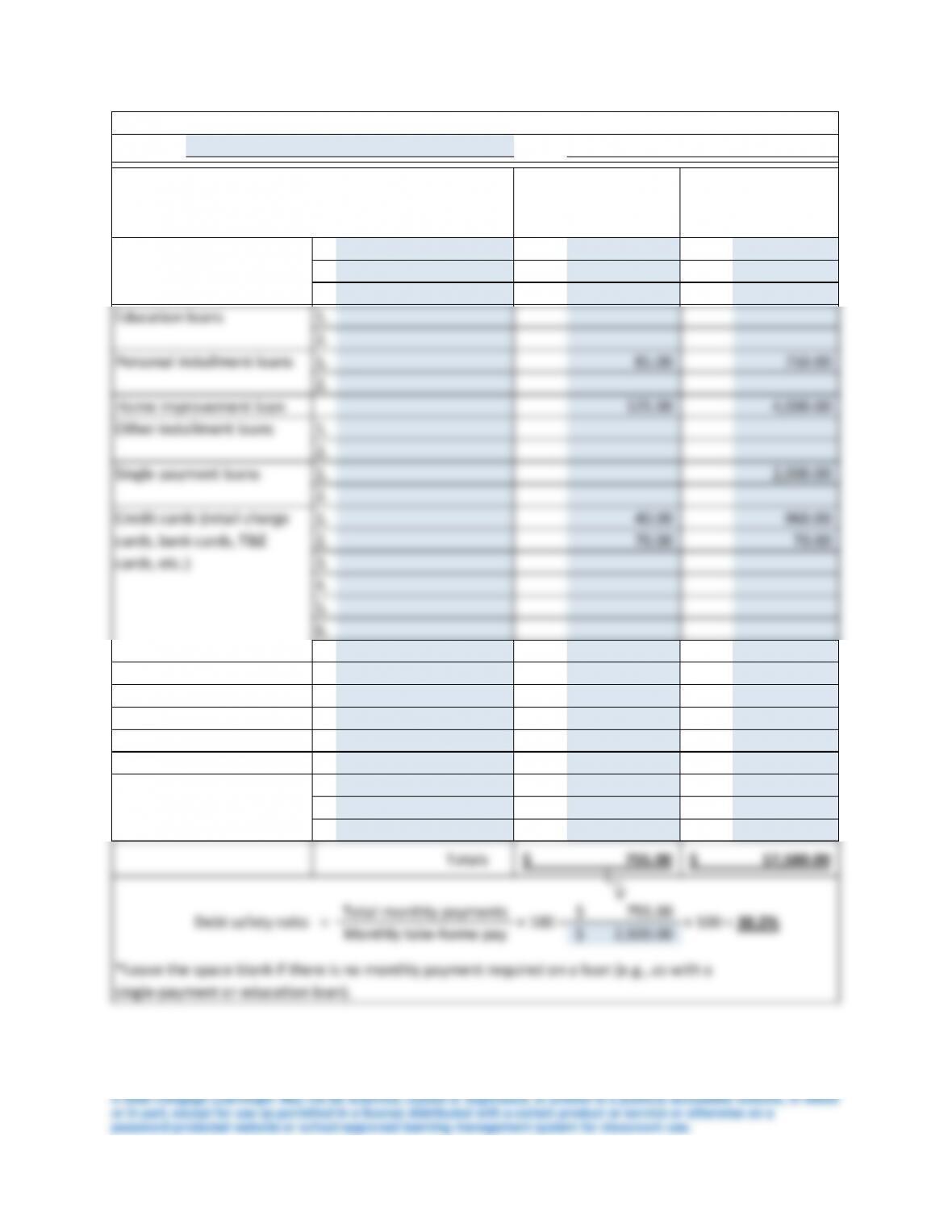

2. Calculating debt safety ratio. Use Worksheet 7.1. Every six months, Leo Perez takes an

inventory of the consumer debts that he has outstanding. His latest tally shows that he still

owes $4,000 on a home improvement loan (monthly payments of $125); he is making $85

monthly payments on a personal loan with a remaining balance of $750; he has a $2,000,

secured, single-payment loan that’s due late next year; he has a $70,000 home mortgage on

which he’s making $750 monthly payments; he still owes $8,600 on a new car loan

(monthly payments of $375); and he has a $960 balance on his MasterCard (minimum

payment of $40), a $70 balance on his Shell credit card (balance due in 30 days), and a

$1,200 balance on a personal line of credit ($60 monthly payments).

Use Worksheet 7.1 to prepare an inventory of Leo’s consumer debt. Find his debt safety

ratio given that his take-home pay is $2,500 per month. Would you consider this ratio to be

good or bad? Explain.

Name Date

1. $ 375.00 $ 8,600.00

2.

3.

1.

2.

1. 85.00 750.00

2.

125.00 4,000.00

1.

2.

1. 2,000.00

2.

1. 40.00 960.00

2. 70.00 70.00

cards, etc.)

Overdraft protection line

Personal line of credit

Loan on life insurance

Margin loan from broker

Other loans

Total monthly payments 755.00$

Monthly take-home pay 2,500.00$

*Leave the space blank if there is no monthly payment required on a loan (e.g., as with a

single-payment or education loan).

Type of Consumer Debt

Creditor

Current

Monthly

Payment*

Latest

Balance

Due

Debt safety ratio

=

× 100 =

× 100 =

30.2%

Auto loans

Education loans

Personal installment loans

Home improvement loan

Other installment loans

AN INVENTORY OF CONSUMER DEBT

September 13, 2018

Leo Perez

Single-payment loans

Credit cards (retail charge

cards, bank cards, T&E

3. Evaluating finance packages. Assume that you’ve been shopping for a new car and

intend to finance part of it through an installment loan. The car you’re looking for has a

sticker price of $18,000. Custom Vehicles has offered to sell it to you for $3,000 down and

finance the balance with a loan that will require 48 monthly payments of $333.67.

However, a competing dealer will sell you the exact same vehicle for $3,500 down, plus a

60-month loan for the balance, with monthly payments of $265.02.

Which of these two finance packages is the better deal? Explain.

4. Calculating single payment loan amount due at maturity. Stanley Price plans to borrow

$8,000 for five years. The loan will be repaid with a single payment after five years, and the

interest on the loan will be computed using the simple interest method at an annual rate of

6 percent. How much will Jim have to pay in five years? How much will he have to pay at

maturity if he’s required to make annual interest payments at the end of each year?

5. Calculating the APR on simple interest and discount loans. Find the finance charges on a

6.5 percent, 18-month, single-payment loan when interest is computed using the simple

interest method. Find the finance charges on the same loan when interest is computed using

the discount method. Determine the APR in each case.

6. Calculating monthly installment loan payments. Using the simple interest method, find

the monthly payments on a $3,000 installment loan if the funds are borrowed for 24

months at an annual interest rate of 6 percent

Computation of the monthly payment amount:

7. Calculating interest and APR of installment loan. Assuming that interest is the only

finance charge, how much interest would be paid on a $5,000 installment loan to be repaid

in 36 monthly installments of $166.10? What is the APR on this loan?

8. Calculating payments, interest, and APR on auto loan. After careful comparison

shopping, Isabella Green decides to buy a new Toyota Camry. With some options added,

the car has a price of $23,558—including plates and taxes. Because she can’t afford to pay

cash for the car, she will use some savings and her old car as a trade-in to put down $8,500.

She plans to finance the rest with a $15,058, 60-month loan at a simple interest rate of 4

percent.

a. What will her monthly payments be?

b. How much total interest will Isabella pay in the first year of the loan?

c. How much interest will Isabella pay over the full (60-month) life of the loan?

d. What is the APR on this loan?

Loan Amortization Schedule

Pay’t num Beg Bal Interest Payment End Bal

1 15,058.00$ 50.19 $277.32 $14,830.88

2 14,830.88$ 49.44 277.32 $14,602.99

3 14,602.99$ 48.68 277.32 $14,374.35

4 14,374.35$ 47.91 277.32 $14,144.94

5 14,144.94$ 47.15 277.32 $13,914.77

6 13,914.77$ 46.38 277.32 $13,683.84

7 13,683.84$ 45.61 277.32 $13,452.13

8 13,452.13$ 44.84 277.32 $13,219.65

9 13,219.65$ 44.07 277.32 $12,986.40

10 12,986.40$ 43.29 277.32 $12,752.36

11 12,752.36$ 42.51 277.32 $12,517.55

12 12,517.55$ 41.73 277.32 $12,281.96

Total Interest for year 551.79$

55 1,644.61$ 5.48 $277.32 $1,372.77

56 1,372.77$ 4.58 $277.32 $1,100.03

57 1,100.03$ 3.67 $277.32 $826.38

58 826.38$ 2.75 $277.32 $551.82

59 551.82$ 1.84 $277.32 $276.35

60 276.35$ 0.92 $277.32 ($0.05)

Total interest for 60 month

1,580.95

9. Calculating and comparing add-on and simple interest loans. Eli Nelson is borrowing

$10,000 for five years at 7 percent. Payments, which are made on a monthly basis, are

determined using the add-on method.

a. How much total interest will Chris pay on the loan if it is held for the full five-year term?

b. What are Chris’s monthly payments?

c. How much higher are the monthly payments under the add-on method than under the

simple interest method?

10. Comparing payments and APRs of financing alternatives. Because of a job change, Finn

McBryde has just relocated to the southeastern United States. He sold his furniture before

he moved, so he’s now shopping for new furnishings. At a local furniture store, he’s found

an assortment of couches, chairs, tables, and beds that he thinks would look great in his

new two-bedroom apartment; the total cost for everything is $6,400.

Because of moving costs, Ben is a bit short of cash right now, so he’s decided to take out an

installment loan for $6,400 to pay for the furniture. The furniture store offers to lend him

the money for 48 months at an add-on interest rate of 6.5 percent. The credit union at

Finn’s firm also offers to lend him the money—they’ll give him the loan at an interest rate

of 6 percent simple, but only for a term of 24 months.

a. Compute the monthly payments for both of the loan offers.

b. Determine the APR for both loans.

c. Which is more important: low payments or a low APR? Explain.

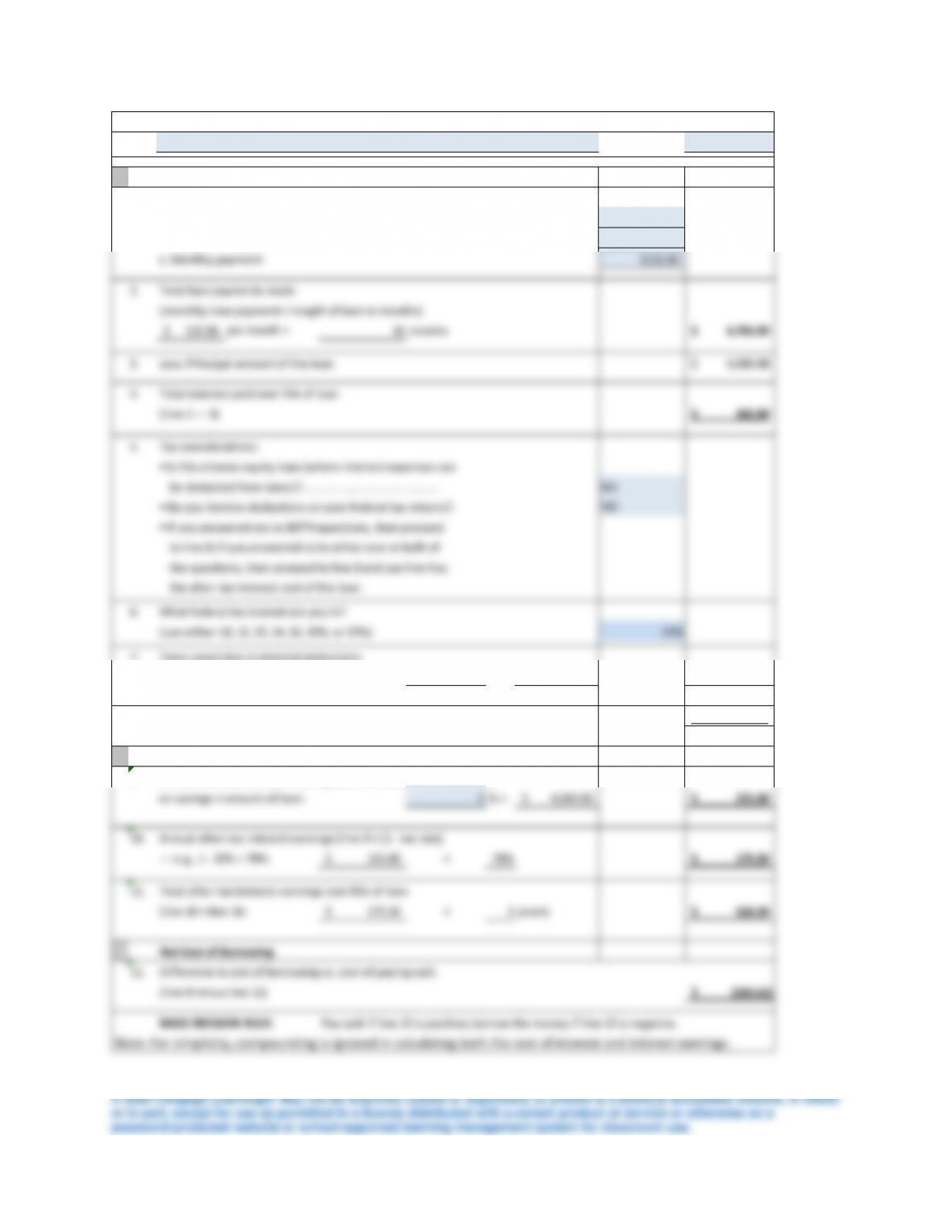

11. Deciding whether to pay cash or finance a purchase. Use Worksheet 7.2. Matilda

Edwards wants to buy a home entertainment center. Complete with a big-screen TV, DVD,

and sound system, the unit would cost $4,500. Matilda has over $15,000 in a money fund, so

she can easily afford to pay cash for the whole thing (the fund is currently paying 5 percent

interest, and Matilda expects that yield to hold for the foreseeable future). To stimulate

sales, the dealer is offering to finance the full cost of the unit with a 36-month installment

loan at 4 percent, simple. Matilda wants to know: Should she pay cash for this home

entertainment center or buy it on time? (Note: Assume Matilda is in the 22 percent tax

bracket and that she itemizes deductions on her tax returns.) Briefly explain your answer.

a. Should she pay cash for the entertainment center?

(line 8 minus line 11)

Pay cash if line 12 is positive; borrow the money if line 12 is negative.

BASIC DECISION RULE:

Date 11/5/2018

1. 0.04

4,500.00$

3

$132.86

2.

132.86$

per month ×36 months 4,782.89$

3. 4,500.00$

4.

282.89

$

(use either 10, 12, 22, 24, 32, 35%, or 37%)

Taxes saved due to interest deductions

Total after-tax interest cost on the loan (line 4 – line 7)

Cost of Paying Cash

Tax considerations:

• Is this a home equity loan (where interest expenses can

be deducted from taxes)? . . . . . . . . . . . . . . . . . . . . . . .

• Do you itemize deductions on your federal tax returns?.

• If you answered yes to BOTH questions, then proceed

to line 6; if you answered no to either one or both of

the questions, then proceed to line 8 and use line 4 as

the after-tax interest cost of the loan.

What federal tax bracket are you in?

Annual interest earned on savings (annual rate of interest earned

on savings × amount of loan:

10.

225.00$ ×78% 175.50

$

11.

175.50$ ×3 years) 526.50

$

12.

Less: Principal amount of the loan

BUY ON TIME OR PAY CASH

Name

Matilda Edwards

Terms of the loan Rate

Cost of Borrowing

a. Amount of the loan

b. Length of the loan (in years)

c. Monthly payment

Total loan payments made

(monthly loan payment × length of loan in months)

Total interest paid over life of loan

(line 2 — 3)

Annual after-tax interest earnings (line 9 × [1 – tax rate]

— e.g., 1 – 22% = 78%:

Total after-tax interest earnings over life of loan

(line 10 × line 1b:

Net Cost of Borrowing

Difference in cost of borrowing vs. cost of paying cash

Making the Payments!

A project to help understand how loan payments are determined

For many of us, new cars can be so appealing! We get bitten by the “new car bug” and think how

great it would be to have a new car. Then we tell ourselves that we really need a new car because

our old one is just a piece of junk waiting to fall apart in the middle of the road. Of course, we

don’t have the money to purchase a new car outright, so we’ll have to get a loan. That means car

payments. The trouble is, car payments often turn out to be a lot less affordable after we actually

get the loan than we thought they would be before we signed on the dotted line. And they last

way beyond the time the new car aura wears off. This project will help you understand how loan

payments are determined, as well as the obligation that they place on you as the borrower. Let’s