5-5 In addition to single-family homes, what other forms of housing are available in the

United States? Briefly describe each of them.

Single-family homes: They can be stand-alone homes on their own legally defined lots or row

5-6 What type of housing would you choose for yourself now, and why? Why might you

choose to rent instead of buy?

5-7 Why is it important to have a written lease? What should a rental contract include?

5-8 Briefly describe the various benefits of owning a home. Which one is most important to

you? Which is least important?

5-9 What does the loan-to-value ratio on a home represent? Is the down payment on a home

related to its loan-to-value ratio? Explain.

5-10 What are mortgage points? How much would a home buyer have to pay if the lender

wanted to charge 2.5 points on a $250,000 mortgage? When would this amount have to be

paid? What effect do points have on the mortgage’s rate of interest?

5-11 What are closing costs, and what items do they include? Who pays these costs, and

when?

Closing costs are all other expenses besides the down payment that borrowers ordinarily pay at

5-12 What are the most common guidelines used to determine the monthly mortgage

payment one can afford?

5-13 Why is it advisable for the prospective home buyer to investigate property taxes?

5-14 Describe some of the steps home buyers can take to improve the home-buying process

and increase their overall satisfaction with their purchases.

5-15 What role does a real estate agent play in the purchase of a house? What is the benefit

of the MLS? How is the real estate agent compensated, and by whom?

Most home buyers rely on real estate agents because they’re professionals who are in daily

contact with the housing market. Once you describe your needs to an agent, he or she can begin

5-16 Describe a real estate short sales transaction. What are the potential benefits and costs

from the perspective of the homeowner?

5-17 Why should you investigate mortgage loans and prequalify for a mortgage early in the

home-buying process?

5-18 What information is normally included in a real estate sales contract? What is an

earnest money deposit? What is a contingency clause?

State laws generally specify that, to be enforceable in court, real estate buy–sell agreements must

5-19 Describe the steps involved in closing the purchase of a home.

5-20 Describe the various sources of mortgage loans. What role might a mortgage broker

play in obtaining mortgage financing?

5-21 Briefly describe the two basic types of mortgage loans. Which has the lowest initial

rate of interest? What is negative amortization, and which type of mortgage can experience

it? Discuss the advantages and disadvantages of each mortgage type.

The fixed-rate mortgage still accounts for a large portion of all home mortgages. Both the rate

5-22 Differentiate among conventional, insured, and guaranteed mortgage loans.

Critical Thinking Problems

5.1 The Newtons New Car Decision: Lease versus Purchase

Farrah and Same Newton, a dual-income couple in their late 20s, want to replace their

seven-year-old car, which has 90,000 miles on it and needs some expensive repairs. After

reviewing their budget, the Newtons conclude that they can afford auto payments of not

more than $350 per month and a down payment of $2,000. They enthusiastically decide to

visit a local dealer after reading its newspaper ad offering a closed-end lease on a new car

for a monthly payment of $245. After visiting with the dealer, test-driving the car, and

discussing the lease terms with the salesperson, they remain excited about leasing the car

but decide to wait until the following day to finalize the deal. Later that day, the Newtons

begin to question their approach to the new car acquisition process and decide to

reevaluate their decision carefully.

Critical Thinking Questions

1. What are some basic purchasing guidelines that the Newtons should consider when

choosing which new car to buy or lease? How can they find the information they need?

2. How would you advise the Newtons to research the lease-versus-purchase decision before

visiting the dealer? What are the advantages and disadvantages of each alternative?

3. Assume that the Newtons can get the following terms on a lease or a bank loan for the

car, which they could buy for $17,000. This amount includes tax, title, and license fees.

• Lease: 48 months, $245 monthly payment, 1 month’s payment required as a security

deposit,

$350 end-of-lease charges; a residual value of $6,775 is the purchase option price at the end

of the lease.

• Loan: $2,000 down payment, $15,000, 48-month loan at 5 percent interest requiring a

monthly payment of $345.44; assume that the car’s value at the end of 48 months will be

the same as the residual value and that sales tax is 6 percent.

The Newtons can currently earn interest of 3 percent annually on their savings. They

expect to drive about the same number of miles per year as they do now.

a. Use the format given in Worksheet 5.1 to determine which deal is best for the Newtons.

b. What other costs and terms of the lease option might affect their decision?

c. Based on the available information, should the Newtons lease or purchase the car? Why?

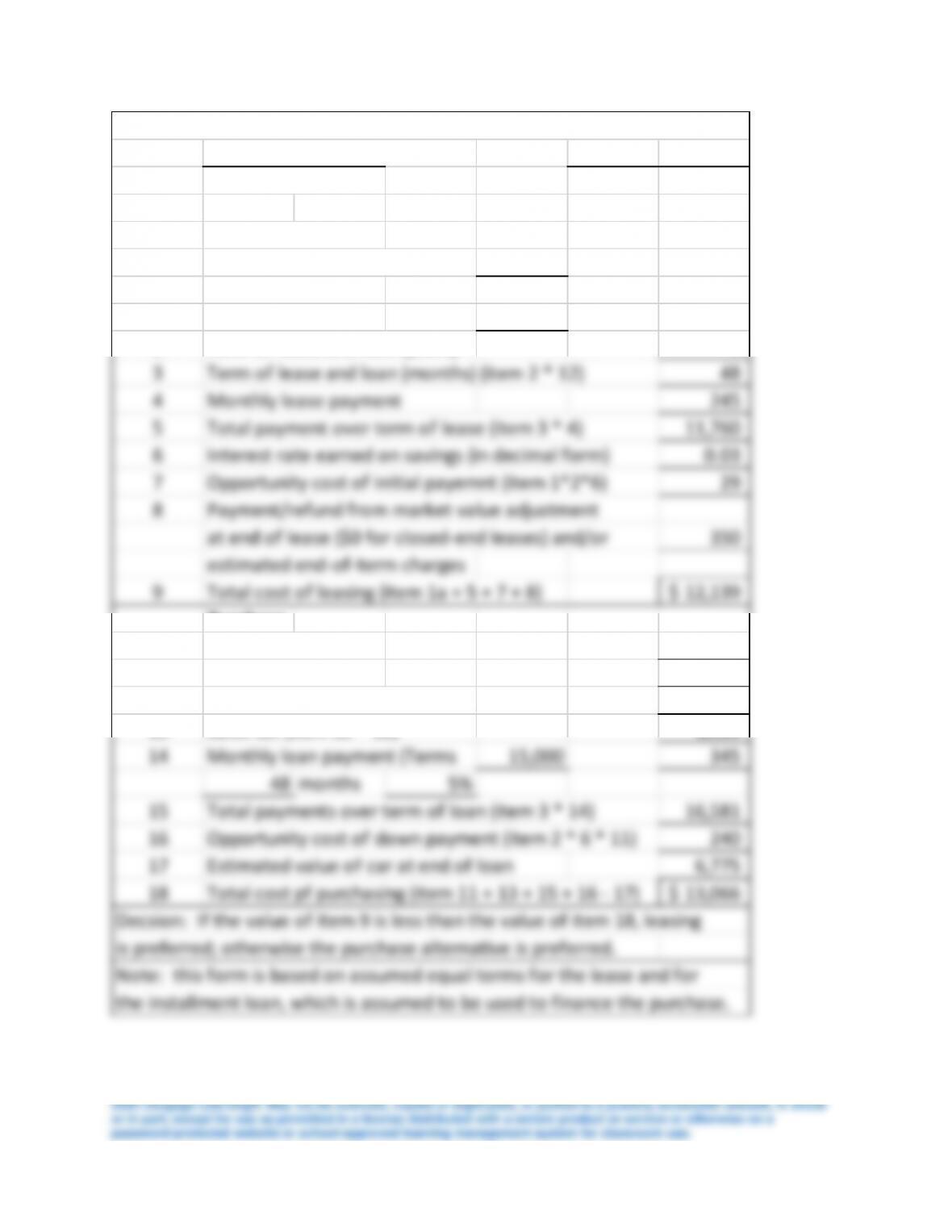

Name Farrah and Same Newton Date 4-May-16

Item Description Amount

Lease

1 Initial payment:

a. Down payment (capital

cost reduction)

b. Security deposit: 245

2 Term of lease and loan (years) 4

3 Term of lease and loan (months) (item 2 * 12) 48

4 Monthly lease payment 245

5 Total payment over term of lease (item 3 * 4) 11,760

6 Interest rate earned on savings (in decimal form) 0.03

7 Opportunity cost of initial payemnt (item 1*2*6) 29

8 Payment/refund from market value adjustment

at end of lease ($0 for closed–end leases) and/or 350

estimated end-of–term charges

16 Opportunity cost of down payment (item 2 * 6 * 11) 240

17 Estimated value of car at end of loan 6,775

18 Total cost pf purchasing (item 11 + 13 + 15 + 16 – 17) 13,066$

Decsion: If the value of item 9 is less than the value of item 18, leasing

is preferred; otherwise the purchase alternative is preferred.

Automobile Lease Versus Purchase Analysis

5.2 Evaluating a Mortgage Loan for the Gerrards

Ben and Marie Gerrard, both in their mid-20s, have been married for four years and have

two preschool-age children. Ben has an accounting degree and is employed as a cost

accountant at an annual salary of $62,000. They’re now renting a duplex but wish to buy a

home in the suburbs of their rapidly developing city. They’ve decided they can afford a

$215,000 house and hope to find one with the features they desire in a good neighborhood.

The insurance costs on such a home are expected to be $800 per year, taxes are expected to

be $2,500 per year, and annual utility bills are estimated at $1,440—an increase of $500

over those they pay in the duplex. The Gerrards are considering financing their home with

a fixed-rate, 30-year, 6 percent mortgage. The lender charges 2 points on mortgages with

20 percent down and 3 points if less than 20 percent is put down (the commercial bank that

the Gerrards will deal with requires a minimum of 10 percent down). Other closing costs

are estimated at 5 percent of the home’s purchase price. Because of their excellent credit

record, the bank will probably be willing to let the Gerrards’ monthly mortgage payments

(principal and interest portions) equal as much as 28 percent of their monthly gross

income. Since getting married, the Gerrards have been saving for the purchase of a home

and now have $44,000 in their savings account.

Critical Thinking Questions

1. How much would the Gerrards have to put down if the lender required a minimum 20

percent down payment? Could they afford it?

2. Given that the Gerrards want to put only $25,000 down, how much would their closing

costs be?

Considering only principal and interest, how much would their monthly mortgage

payments be?

Would they qualify for a loan using a 28 percent affordability ratio?

3. Using a $25,000 down payment on a $215,000 home, what would the Gerrards’ loan–to–

value ratio be? Calculate the monthly mortgage payments on a PITI basis.

4. What recommendations would you make to the Gerrards? Explain.

5.3 Julie’s Rent-or-Buy Decision

Julie Brown is a single woman in her late 20s. She is renting an apartment in the

fashionable part of town for $1,200 a month. After much thought, she’s seriously

considering buying a condominium for $175,000. She intends to put 20 percent down and

expects that closing costs will amount to another $5,000; a commercial bank has agreed to

lend her money at the fixed rate of 6 percent on a 15-year mortgage. Julie would have to

pay an annual condominium owner’s insurance premium of $600 and property taxes of

$1,200 a year (she’s now paying renter’s insurance of $550 per year). In addition, she

estimates that annual maintenance expenses will be about 0.5 percent of the price of the

condo (which includes a $30 monthly fee to the property owners’ association). Julie’s

income puts her in the 25 percent tax bracket (she itemizes her deductions on her tax

returns), and she earns an after-tax rate of return on her investments of around 4 percent.

Critical Thinking Questions

1. Given the information provided, use Worksheet 5.2 to evaluate and compare Julie’s

alternatives of remaining in the apartment or purchasing the condo.

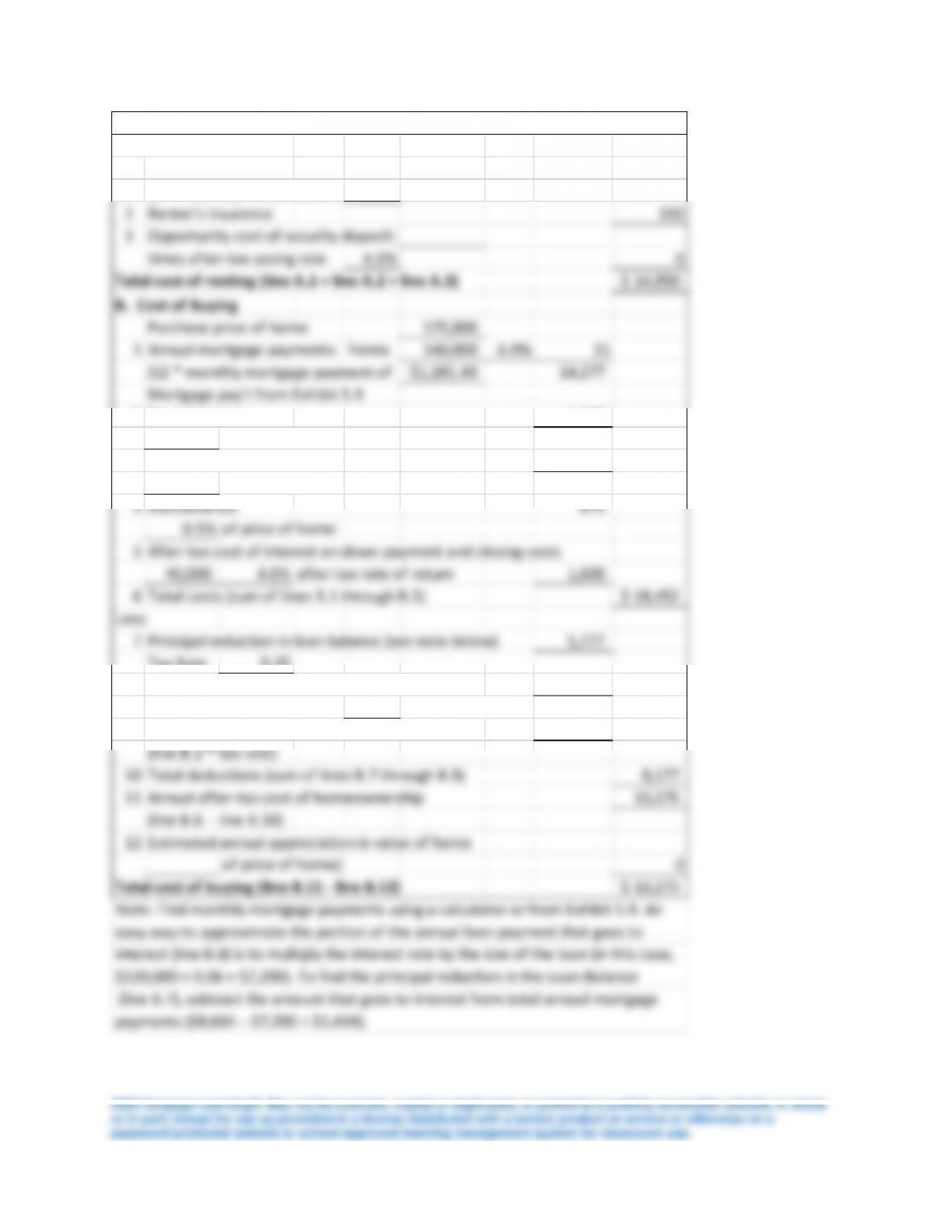

A. Cost of Renting

1 Annual rental costs 14400

(12 * monthly rental rate of 1200

2Renter’s insurance 550

3 Opportunity cost of security deposit:

times after-tax saving rate 4.0% 0

Total cost of renting (line A.1 + line A.2 + line A.3) 14,950$

B. Cost of Buying

Purchase price of home 175,000

1

Annual mortgage payments:

Terms 140,000 6.0% 15

(12 * monthly mortgage payment of $1,181.40 14,177

Mortgage pay’t from Exhibit 5.9

Less:

7 Principal reduction in loan balance (see note below) 5,777

Tax Rate 0.25

8 Tax savings due to interest deductions* 2,100

of price of home) 0

Total cost of buying (line B.11 – line B.12) 10,275$

RENT–OR–BUY ANALYSIS — Julie Brown

Note: Find monthly mortgage payments using a calculator or from Exhibit 5.9. An

easy way to approximate the portion of the annual loan payment that goes to

2. Working with a friend who is a realtor, Julie has learned that condos like the one that

she’s thinking of buying are appreciating in value at the rate of 3.5 percent a year and are

expected to continue doing so. Would such information affect the rent-or-buy decision

made in Question 1?

Explain.

3. Discuss any other factors that should be considered when making a rent-or-buy decision.

Location is important and must be considered. For example, the rental unit may be on a public

4. Which alternative would you recommend for Julie in light of your analysis?

Terms Found in the Chapter

adjustable-rate

mortgage (ARM)

A mortgage on which the rate of interest, and therefore the size of the

monthly payment, is adjusted based on market interest rate

movements.

adjustment period

On an adjustable-rate mortgage, the period of time between rate or

payment changes.

anchoring

A behavioral bias in which an individual tends to allow an initial

estimate (of value or price) to dominate one’s subsequent assessment

(of value or price) regardless of new information to the contrary.

balloon-payment

mortgage

A mortgage with a single large principal payment due at a specified

future date

biweekly mortgage

A loan on which payments equal to half the regular monthly payment

are made every two weeks.

buydown

Financing made available by a builder or seller to a potential new-

home buyer at well below market interest rates, often only for a short

period.

capitalized cost

The price of a car that is being leased.

closed-end lease

The most popular form of automobile lease; often called a walk-away

lease, because at the end of its term, the lessee simply turns in the car

(assuming the preset mileage limit has not been exceeded and the car

hasn’t been abused).

closing costs

All expenses (including mortgage points) that borrowers ordinarily

pay when a mortgage loan is closed and they receive title to the

purchased property.

condominium

(condo)

A form of direct ownership of an individual unit in a multiunit project

in which lobbies, swimming pools, and other common areas and

facilities are jointly owned by all property owners in the project.

contingency clause

A clause in a real estate sales contract that makes the agreement

conditional on such factors as the availability of financing, property

inspections, or obtaining expert advice.

conventional

mortgage

A mortgage offered by a lender who assumes all the risk of loss;

typically requires a down payment of at least 20 percent of the value

of the mortgaged property.

convertible ARM

An adjustable-rate mortgage loan that allows borrowers to convert

from an adjustable-rate to a fixed rate loan, usually at any time

between the 13th and the 60th month.

cooperative

apartment (co-op)

An apartment in a building in which each tenant owns a share of the

nonprofit corporation that owns the building.

depreciation

The loss in the value of an asset, such as an automobile, that occurs

over its period of ownership; calculated as the difference between the

price initially paid and the subsequent sale price.

down payment

A portion of the full purchase price provided by the purchaser when a

house or other major asset is purchased; often called equity.

earnest money

deposit

Money pledged by a buyer to show good faith when making an offer

to buy a home.

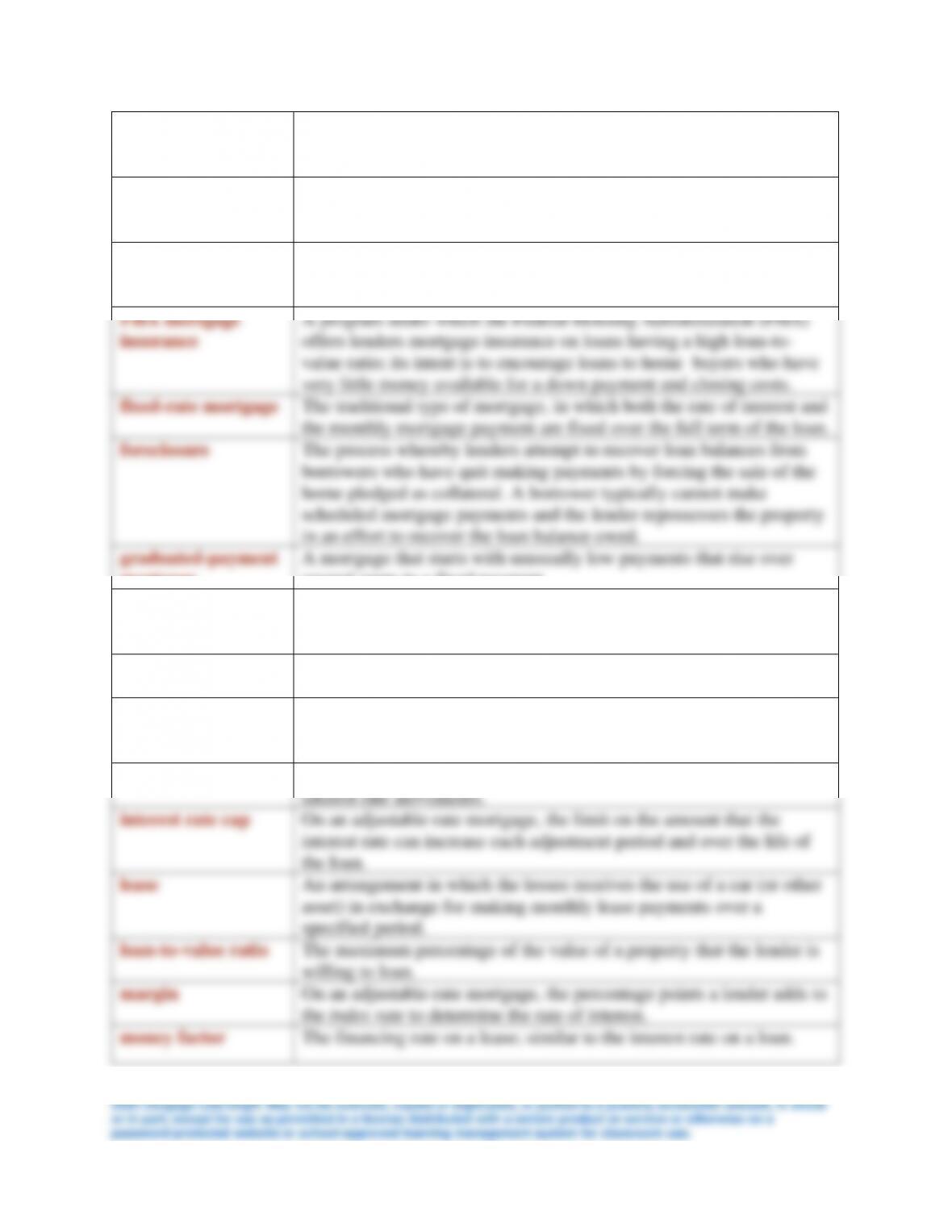

FHA mortgage

insurance

A program under which the Federal Housing Administration (FHA)

offers lenders mortgage insurance on loans having a high loan-to–

value ratio; its intent is to encourage loans to home buyers who have

very little money available for a down payment and closing costs.

fixed-rate mortgage

The traditional type of mortgage, in which both the rate of interest and

the monthly mortgage payment are fixed over the full term of the loan.

foreclosure

The process whereby lenders attempt to recover loan balances from

borrowers who have quit making payments by forcing the sale of the

home pledged as collateral. A borrower typically cannot make

scheduled mortgage payments and the lender repossesses the property

in an effort to recover the loan balance owed.

graduated-payment

mortgage

A mortgage that starts with unusually low payments that rise over

several years to a fixed payment.

growing-equity

mortgage

Fixed-rate mortgage with payments that increase over a specific

period. Extra funds are applied

to the principal so that the loan is paid off more quickly.

homeowner’s

insurance

Insurance that is required by mortgage lenders and covers the

replacement value of a home and its contents.

interest-only

mortgage

.

A mortgage that requires the borrower to pay only interest; typically

used to finance the purchase of more expensive properties

index rate

On an adjustable-rate mortgage, the baseline index rate that captures

interest rate movements.

interest rate cap

On an adjustable-rate mortgage, the limit on the amount that the

interest rate can increase each adjustment period and over the life of

the loan.

lease

An arrangement in which the lessee receives the use of a car (or other

asset) in exchange for making monthly lease payments over a

specified period.

loan-to-value ratio

The maximum percentage of the value of a property that the lender is

willing to loan.

margin

On an adjustable-rate mortgage, the percentage points a lender adds to

the index rate to determine the rate of interest.

money factor

The financing rate on a lease; similar to the interest rate on a loan.

mortgage banker

A firm that solicits borrowers, originates primarily government-

insured and government- guaranteed loans, and places them with

mortgage lenders; often uses its own money to initially fund

mortgages that it later resells.

mortgage broker

A firm that solicits borrowers, originates primarily conventional loans,

and places them with mortgage lenders; the broker merely takes loan

applications and then finds lenders willing to grant the mortgage loans

under the desired terms.

mortgage loan

A loan secured by the property: If the borrower defaults, the lender

has the legal right to liquidate the property to recover the funds it is

owed.

mortgage points

Fees (one point equals 1 percent of the amount borrowed) charged by

lenders at the time they grant a mortgage loan; they are related to the

lender’s supply of loanable funds and the demand for mortgages.

Multiple Listing

Service (MLS)

A comprehensive listing, updated daily, of properties for sale in a

given community or metropolitan area; includes a brief description of

each property with a photo and its asking price but can be accessed

only by realtors who work for an MLS member.

negative

amortization

When the principal balance on a mortgage loan increases because the

monthly loan payment is lower than the amount of monthly interest

being charged; some ARMs are subject to this undesirable condition.

open-end (finance)

lease

An automobile lease under which the estimated residual value of the

car is used to determine lease payments; if the car is actually worth

less than this value at the end of the lease, the lessee must pay the

difference.

payment cap

On an adjustable-rate mortgage, the limit on the monthly payment

increase that may result from a rate adjustment.

PITI

Acronym that refers to a mortgage payment including stipulated

portions of principal, interest, property taxes, and homeowner’s

insurance.

prequalification

The process of arranging with a mortgage lender, in advance of

buying a home, to obtain the amount of mortgage financing the

lender deems affordable to the home buyer.

private mortgage

insurance (PMI)

An insurance policy that protects the mortgage lender from loss in the

event the borrower defaults on the loan; typically required by lenders

when the down payment is less than 20 percent.

property taxes

Taxes levied by local governments on the assessed value of real estate

for the purpose of funding schools, law enforcement, and other local

services.

purchase option

A price specified in a lease at which the lessee can buy the car at the

end of the lease term.

Real Estate

Settlement

Procedures Act

(RESPA)

A federal law requiring mortgage lenders to give potential borrowers a

government publication describing the closing process and providing

clear, advance disclosure of all closing costs to home buyers.

real estate short

sale

Sale of real estate property in which the proceeds are less than the

balance owed on a loan secured by the property sold.

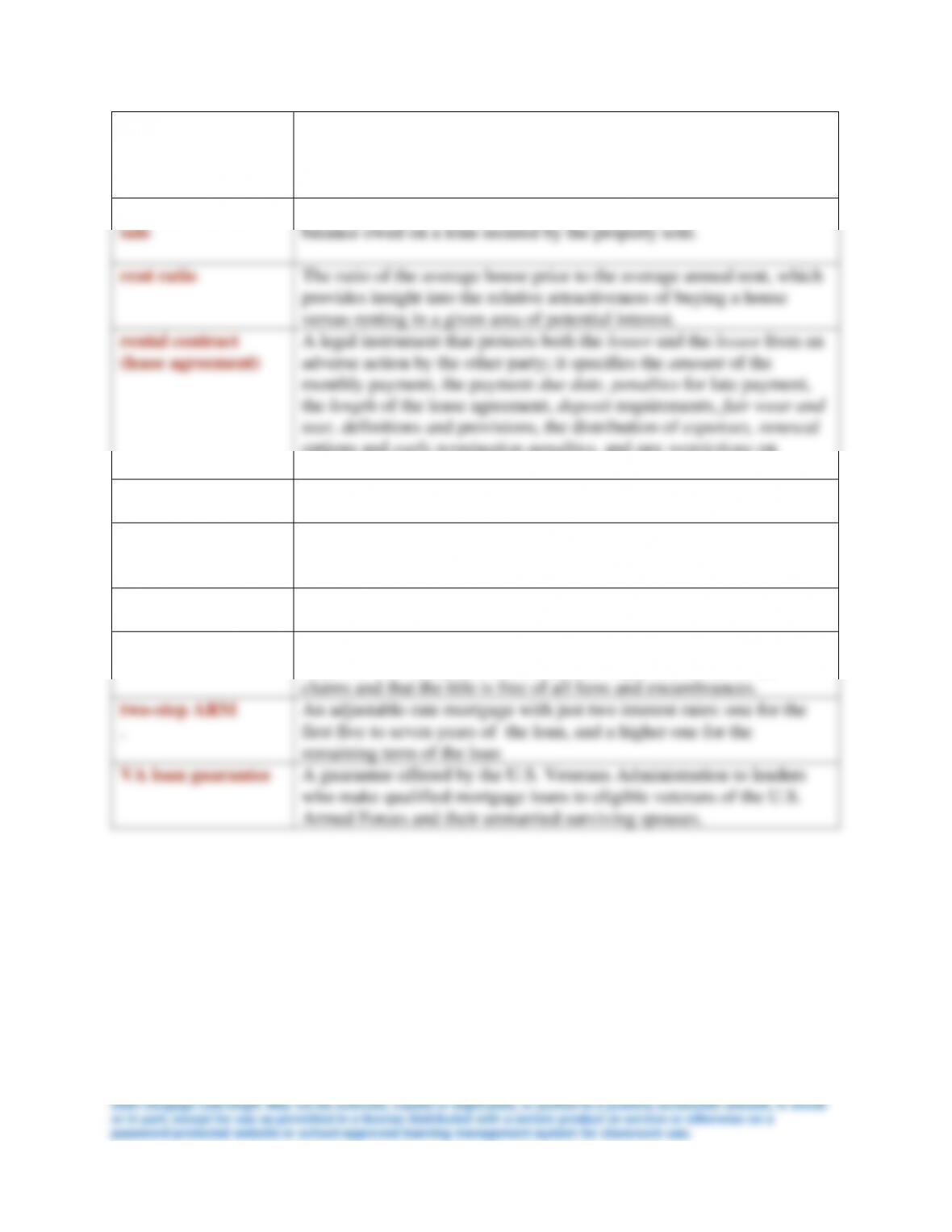

rent ratio

The ratio of the average house price to the average annual rent, which

provides insight into the relative attractiveness of buying a house

versus renting in a given area of potential interest.

rental contract

(lease agreement)

A legal instrument that protects both the lessor and the lessee from an

adverse action by the other party; it specifies the amount of the

monthly payment, the payment due date, penalties for late payment,

the length of the lease agreement, deposit requirements, fair wear and

tear, definitions and provisions, the distribution of expenses, renewal

options and early termination penalties, and any restrictions on

children, pets, subleasing or using the facilities.

residual value

The remaining value of a leased car at the end of the lease term.

sales contract

An agreement to purchase an automobile that states the offering price

and all conditions of the offer; when signed by the buyer and seller,

the contract legally binds them to its terms.

shared-appreciation

mortgage

A loan that allows a lender or other party to share in the appreciated

value when the home is sold.

title check

The research of legal documents and courthouse records to verify that

the seller conveying title actually has the legal interest he or she

claims and that the title is free of all liens and encumbrances.

two-step ARM

.

An adjustable-rate mortgage with just two interest rates: one for the

first five to seven years of the loan, and a higher one for the

remaining term of the loan

VA loan guarantee

A guarantee offered by the U.S. Veterans Administration to lenders

who make qualified mortgage loans to eligible veterans of the U.S.

Armed Forces and their unmarried surviving spouses.

Chapter 5

Making Automobile

and Housing Decisions

Learning Goals

How Will This Affect Me?

I. Buying an Automobile

A. Choosing a Car

B. Affordability

C. Operating Costs

D. Gas, Diesel, or Hybrid?

E. New, Used, or “Nearly New”?

F. Size, Body Style, and Features

II. The Purchase Transaction

A. Negotiating Price

B. Closing the Deal

III. Leasing Your Car

A. The Leasing Process

B. Lease versus Purchase Analysis

C. When the Lease Ends

IV. Meeting Housing Needs: Buy or Rent?

A. Housing Prices and the Financial Crisis 2008-2009

B. What Type of Housing Meets Your Needs?

C. Analyzing the Rent-or-Buy Decision

V. How Much Housing Can You Afford?

A. Benefits of Owning a Home

B. The Cost of Homeownership

C. The Down Payment

D. Points and Closing Costs

E. Mortgage Payments

F. Affordability Ratios

G. Property Taxes and Insurance

H. Maintenance and Operating Expenses

I. Performing a Home Affordability Analysis

VI. The Home-Buying Process

A. Shop the Market First

B. Real Estate Short Sales

C. Using an Agent

D. Prequalifying and Applying for a Mortgage

E. The Real Estate Sales Contract

F. Closing the Deal

VI. Financing the Transaction

A. Sources of Mortgage Loans

B. Types of Mortgage Loans

C. Fixed-Rate Mortgages

D. Adjustable-Rate Mortgages (ARMs)

a. Features of ARMs

b. Beware of Negative Amortization

E. Fixed Rate or Adjustable Rate?