Managing Your Cash and Savings — Chapter 4

Managing Your Cash and Savings

Chapter 4

Learning Objectives

LO1 Understand the role of cash management in the personal financial planning process.

LO2 Describe today’s financial services marketplace, both depository and nondepository

financial institutions.

LO3 Select the checking, savings, electronic banking, and other bank services that meet your

needs.

LO4 Open and use a checking account.

LO5 Calculate the interest earned on your money using compound interest and future value

techniques.

LO6 Develop a cash management strategy that incorporates a variety of savings plans.

Major Topics

This chapter is concerned with cash management, which involves making sure that adequate funds

are available for meeting both planned and unplanned expenditures and that spending patterns are in

line with budgetary guidelines. Cash management is an important aspect of personal financial

planning; it ensures that adequate funds are available for paying bills and that an effective savings

program is established and implemented. This process begins with an understanding of the financial

marketplace, which includes a tremendous variety of institutions providing numerous account and

transaction services. Financial institutions provide checking facilities that allow transactions to be

made safely and efficiently. The methods of accessing accounts vary greatly with the technology

that is available. They also make available numerous savings vehicles that can be used to earn a

return on temporarily idle funds. In addition, a variety of other ways to save are also available from

the government and brokerage firms.

The major topics are included in the Power Point slides available to the instructor and are identified below as they relate

to the learning goals for the chapter.

Managing Your Cash and Savings — Chapter 4

Learning Goals

LG1 Understand the role of cash management in the personal financial planning process.

LG2 Describe today’s financial services marketplace, both depository and nondepository financial

institutions.

LG3 Select the checking, savings, electronic banking, and other bank services that meet your needs.

LG4 Open and use a checking account.

LG5 Calculate the interest earned on your money using compound interest and future value

techniques.

LG6 Develop a cash management strategy that incorporates a variety of savings plans.

Managing Your Cash and Savings — Chapter 4

The ability of the automatic deposit or transfer from checking to savings makes a systematic saving

plan possible. If you never have you hands on the money, you cannot spend it. That’s makes saving

easier. Money market accounts, which pay slightly higher rates than saving accounts, are available

from banks and investment firms.

Financial Facts or Fantasies?

These may be used as “teasers” to get the students on the right page with you. Also, they may be

used as quizzes after you covered the material or as “pre-test questions” to get their attention.

Financial Fact or Fantasy?

1. An asset is considered liquid only if it is held in the form of cash.

2. Today’s financial marketplace offers consumers a full range of financial products and

services, many times all under one roof.

3. Unlike money market mutual funds, money market deposit accounts are federally insured.

Fact: Money market deposit accounts are funds deposited in special, high-paying savings accounts

4. At most banks and other depository institutions, you will be hit with a hefty service charge if

your checking account balance falls even just $1 below the stipulated minimum amount for just one

5. U.S. Series EE and I savings bonds are not a very good way to save.

Fntasy: Investing in Series EE and I savings bonds are excellent ways to save. The bonds are safe

because they are backed by the U.S. government, offer market rates of return, and offer several

attractive features. Series I bonds are particularly attractive to those wanting protection against

inflation.

Managing Your Cash and Savings — Chapter 4

Financial Facts or Fantasies?

These may be used as a quiz or as a pre-test to get the students interested.

1. True False An asset is considered liquid only if it is held in the form of cash.

2. True False Today’s financial marketplace offers consumers a full range of financial

products and services, many times all under one roof.

3. True False Unlike money market mutual funds, money market deposit accounts are

federally insured.

4. True False At most banks and other depository institutions, you will be hit with a

hefty service charge if your checking account balance falls even just $1

below the stipulated minimum amount for just one day out of the month.

5. True False U.S. Series EE and I savings bonds are not a very good way to save.

Rule of 72

The rule says that to find the number of years required to double your money at a given

interest rate, you just divide the interest rate into 72. For example, if you want to know how

long it will take to double your money at eight percent interest, divide 8 into 72 and get 9

years.

Financial Planning Exercises

The following are solutions to the financial planning exercises at the end of the PFIN 7 textbook

chapter.

1. Adapting to a low interest rate environment. A retired couple has expressed concern

about the really low interest rates they’re earning on their savings. They’ve been approached by

an adviser who says he has a “sure–fire” way to get them higher returns. What would you tell this

retired couple about the low-interest-rate environment, and how would you recommend them to

view the adviser’s new prospective investments?

59

Managing Your Cash and Savings — Chapter 4

Monthly check return

No, images of

checks available

online, no fee

Free Checks

No

Overdraft protection

Yes, with fee

ATM and check card

Yes, $2.50 fee for

non-Wells Fargo

3. Choosing a new bank. You’re getting married and believe your present bank is not a good fit.

Discuss how you should go about choosing a new bank and opening an account. Consider the

factors that are important to you in selecting a bank—such as the type and ownership of new

accounts and bank fees and charges.

4. Exposure from stolen ATM card. Suppose that someone stole your ATM card and withdrew

$1,000 from your checking account. How much money could you lose (according to federal

legislation) if you reported the stolen card to the bank:

(a) the day the card was stolen,

(b) 6 days after the theft,

(c) 65 days after receiving your periodic statement?

5. Calculating the net costs of checking accounts. Determine the annual net cost of these

checking accounts:

a. Monthly fee $4, check-processing fee of 20 cents, average of 23 checks written per month

b. Annual interest of 1.5 percent paid if balance exceeds $750, $8 monthly fee if account falls

below minimum balance,

average monthly balance $815, account falls below $750 during four months.

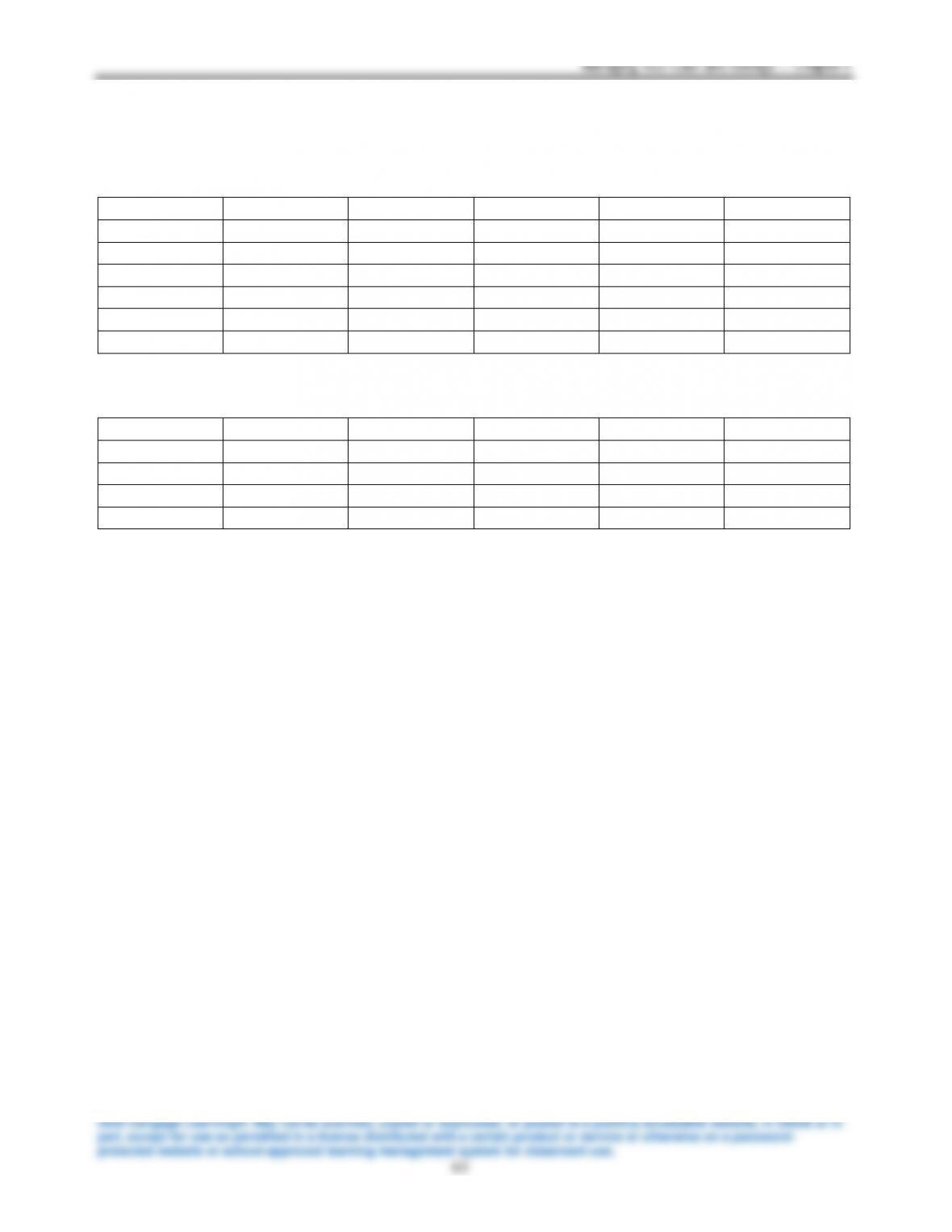

6. Checking account reconciliation. Use Worksheet 4.1. Mateo Gonzalez has an interest-paying

(NOW) checking account at the First State Bank. His checkbook ledger lists the following

checks:

Check Num

Amount

Check Num

Amount

Check Num

Amount

654

206.25

672

24.90

678

38.04

658

55.22

673

32.45

679

97.99

662

103.00

674

44.50

680

486.70

668

99.00

675

30.00

681

43.50

670

6.10

676

30.00

682

75.00

671

50.25

677

111.23

683

98.50

Mateo also made the following withdrawals and deposits at an ATM near his home:

Date

Amount

Transaction

Date

Amount

Transaction

11/1

$50.00

Withdrawal

11/21

$525.60

Deposit

11/2

$525.60

Deposit

11/24

$150.00

Withdrawal

11/6

$100.00

Deposit

11/27

$225.00

Withdrawal

11/14

$75.00

Withdrawal

11/30

$400.00

Deposit

Mateo’s checkbook ledger shows an ending balance of $286.54. He has just received his bank

statement for the month of November. It shows an ending balance of $614.44; it also shows that

he earned interest for November of $3.28, had a check service charge of $8 for the month, and

had another $20 charge for a returned check. His bank statement indicates the following checks

have cleared: 654, 662, 672, 674, 675, 676, 677, 678, 679, and 681. ATM withdrawals on 11/1 and

11/14 and deposits on 11/2 and 11/6 have cleared; no other checks or ATM activities are listed on

his statement, so anything remaining should be treated as outstanding. Use a checking account

reconciliation form like the one in Worksheet 4.1 to reconcile Mateo’s checking account.

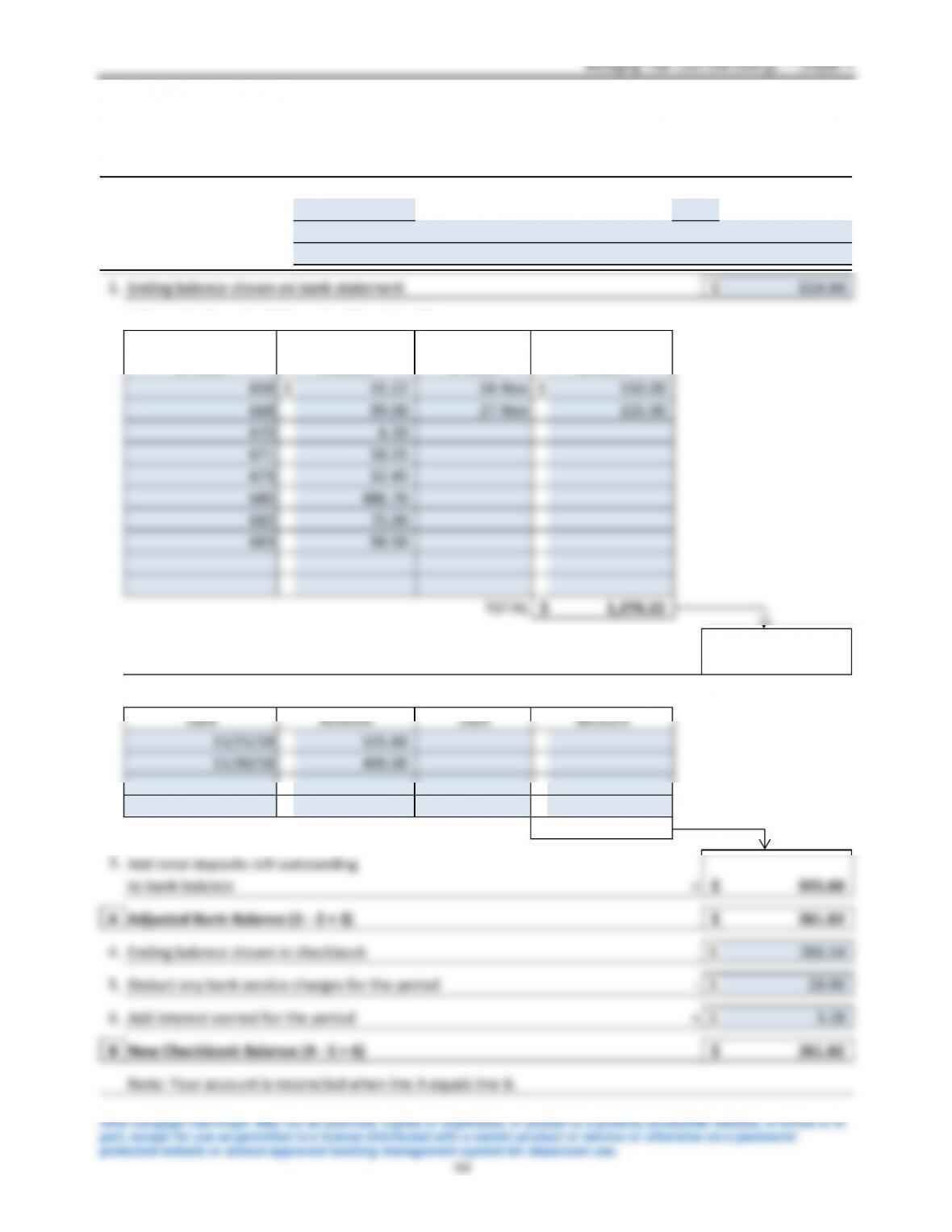

6. Worksheet 4.1 is below.

November , 20

1.

$

614.44

Check Number

or Date

Check Number

or Date

658 $ 55.22 24-Nov $ 150.00

668 99.00 27-Nov 225.00

670 6.10

671 50.25

673 32.45

680 486.70

682 75.00

Add up deposits still outstanding:

11/30/18 400.00

TOTAL

A

4. $ 286.54

5. – $ 28.00

CHECKING ACCOUNT RECONCILIATION

For the month of

Accountholder Name(s)

Mateo Gonzalez

Type of Account

NOW Checking Account

925.60$

Ending balance shown on bank statement

261.82$

Add up checks and withdrawals still outstanding:

Adjusted Bank Balance (1 – 2 + 3)

Amount

Amount

Ending balance shown in checkbook

Deduct any bank service charges for the period

7. Calculating interest earned and future value of savings account. If you put $6,000 in a savings

account that pays interest at the rate of 3 percent, compounded annually, how much will you have

in five years? (Hin Use the future value formula.) How much interest will you earn during the

five years?

If you put $6,000 each year into a savings account that pays interest at the rate of 4 percent a

year, how much would you have after five years?

8. Determining the right amount of short term, liquid investments. Ella and Aaron Martin

together earn approximately $92,000 a year after taxes. Through an inheritance and some wise

investing, they also have an investment portfolio with a value of almost $200,000.

a. How much of their annual income do you recommend the Martins hold in some form of liquid

savings as reserves? Explain.

b. How much of their investment portfolio do you recommend they hold in savings and other

short-term investment vehicles? Explain.

c. How much, in total, should they hold in short-term liquid assets?

9. Short-term investments and inflation. Describe some of the short-term investments that can be

used to manage your cash resources. What factors would you focus on if you were concerned that

inflation will increase significantly in the future?

Managing Your Cash and Savings — Chapter 4

2020 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in

part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-

protected website or school-approved learning management system for classroom use.

67

Additional Questions for Class Discussion

The following are questions and answers may be used for class discussion, for additional homework,

or exam questions.

4-1 What is cash management, and what are its major functions?

4-2 Give two reasons for holding liquid assets. Identify and briefly describe the popular types

of liquid assets.

4-3 Explain the effects that historically low interest rates have on borrowers, lenders, savers,

and retirees.

4-4 Briefly describe the basic operations of—and the products and services offered by—each

of the following financial institutions: (a) commercial bank, (b) savings and loan association,

(c) savings bank, (d) credit union, (e) stock brokerage firm, and (f) mutual fund.

Managing Your Cash and Savings — Chapter 4

Exhibit 4.2 gives a brief description of services offered by commercial banks, savings and loan

associations, savings banks, credit union.

From Exhibit 4.2:

Credit union A nonprofit, member-owned financial cooperative that provides a full range of

financial products and services to its members, who must belong to a common occupation, religious

or fraternal order, or residential area. Generally small institutions when compared with commercial

banks and S&Ls. Offer interest-paying checking accounts—called share draft accounts—and a

variety of saving and lending programs. Because they are run to benefit their members, they pay

higher interest on savings and charge lower rates on loans than do other depository financial

institutions.

4-5 What role does the FDIC play in insuring financial institutions? What other federal

insurance program exists? Explain.

4-6 Would it be possible for an individual to have, say, six or seven checking and savings

accounts at the same bank and still be fully protected under federal deposit insurance?

Explain. Describe how it would be possible for a married couple to obtain as much as

$1,500,000 in federal deposit insurance coverage at a single bank.

4-7 Distinguish between a checking account and a savings account.

4-8 Define and discuss (a) demand deposits, (b) time deposits, (c) interest-paying checking

accounts.

a. Demand deposit refers to an account held at a financial institution from which funds can

be withdrawn (in check or cash) upon demand by the account holder. As long as sufficient

funds are in the account, the bank must immediately pay the amount indicated when