Preparing Your Taxes

Chapter 3

How Will This Affect Me?

There’s an old joke that people who complain about taxes can be divided into two groups: men

and women. This chapter helps you pursue the tax-planning goal of maximizing the money that

you get to keep by legally minimizing the taxes you have to pay. Income, various adjustments to

income, deductions, and credits are considered in computing taxes. The chapter walks through

the steps in completing representative tax returns. The impact of Social Security taxes and tax

shelters are considered. And a framework for choosing a professional tax preparer or tax

preparation software is provided. After reading this chapter you should be able to prepare your

own taxes or to better understand and evaluate how your taxes are prepared by software or a tax

professional.

The one continuing characteristic of the federal income tax is change. Congress feels compelled

to “improve” the tax law, frequently doing so in December of the tax year at issue. Thus, any

summary of the tax law will be out of date whenever it is written. This chapter is based upon the

law in effect November, 2018. The tax rates and other numeric items for 2019 are included for

your information. The tax forms used are drafts of 2018 forms that were available in October,

2018. The final forms for 2018 were not available in time to include in these materials. The

forms will be available at irs.gov, forms and publications.

The student who is serious about personal financial planning needs to take an individual tax

course. While only about half of all people pay income tax [that half pays a lot of FICA taxes

and state sales taxes] the people who ask for help with their financial planning are in the top 20%

and they do pay income taxes. Minimizing that tax is a concern to the clients of financial

planners.

There are several dollar limits or deductions that are annually adjusted for inflation. The

numbers in the text are the numbers for 2018. The adjusted numbers are published in a revenue

procedure issued by the IRS in mid-November of each year. The adjusted numbers for 2019 are

included here for information. For planning purposes, the exact adjusted number is not

necessary. Whether the standard deduction for a joint return is $24,000 [the amount for 2018] or

$24,400 [the amount for 2019], the impact on financial planning is the same.

Learning Goals

LG1 Discuss the basic principles of income taxes and determine your filing status.

All taxes have a tax base and a tax rate, thus tax = base * rate. The name of the tax indicates the

tax base, thus, the tax base for the income tax is income; for the sales tax, the base is sales; and

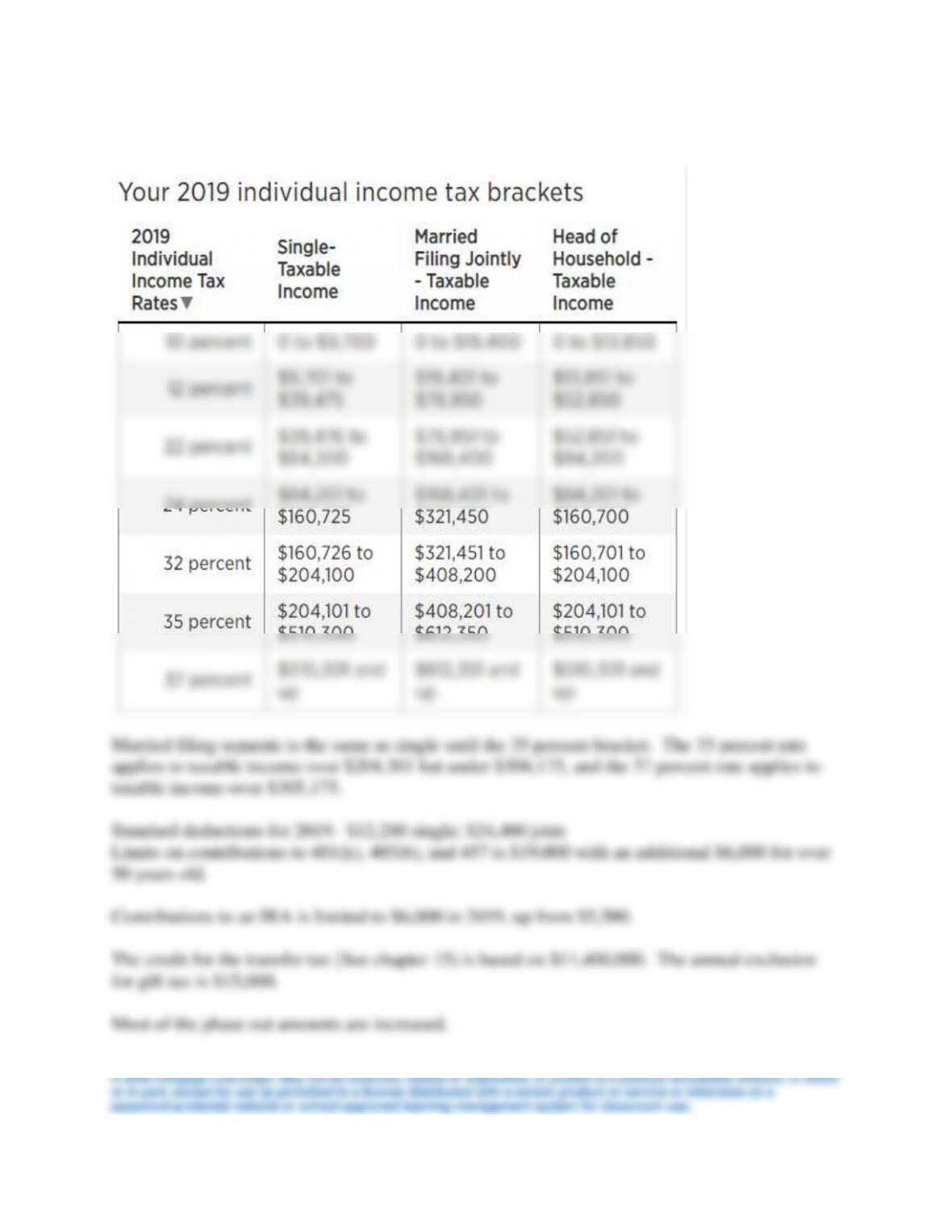

There are four sets of rates – Single, Joint, Married filing separately, and Head of households.

The 2018 rates are in the textbook. The 2019 rates are below. The chapter has several examples

of computing the tax. You can build the tax by computing the tax on each bracket of income or

2019 Tax Rates

LG2 Describe the sources of gross income and adjustments to income, differentiate between

standard and itemized deductions and exemptions, and calculate taxable income.

Exhibit 3.1 gives the steps to compute taxable income and the related tax liability. It will be

good to go over these steps.

The standard deduction varies by taxpayer’s age and filing status. Most common are the single

status which has a standard deduction of $12,000 in 2018 and $12,200 in 2019, and the married

filing joint status which has a standard deduction of $24,000 in 2018 and $24,400 in 2019. They

change every year as the Consumer Price Index changes. If the taxpayer’s itemized deductions

LG3 Prepare a basic tax return using the appropriate tax forms and rate schedules.

All taxpayers file Form 1040. Previously there were less complicated versions of the Form 1040

but for 2018 these have been eliminated. There are special versions for the 1040 for non-

amount of the credit, thus the value of a $2,000 child tax credit to a 22% marginal rate taxpayer

is $2,000.

Worksheet 3.1 is an example of a form 2014.

LG4 Explain who needs to pay estimated taxes, when to file or amend your return, and how to

handle an audit.

LG5 Know where to get help with your taxes and how software can make tax return preparation

easier.

LG6 Implement an effective tax planning strategy.

There are two strategies to tax planning:

Financial Facts or Fantasies?

These may be used as “teasers” to get the students on the right page with you. Also, they may be

used as quizzes after you covered the material or as “pre–test questions” to get their attention.

Are the following statements Financial Facts (true) or Fantasies (false)? Consider the answers to

the questions below as you read through this chapter.

• Tax credits, and deductions reduce your taxable income by comparable amounts.

Fantasy: Tax credits are far more valuable than comparable dollar amounts of deductions

because they directly reduce, dollar for dollar, the amount of taxes due.

Financial Facts or Fantasies?

These may be used as a quiz or as a pre-test to get the students interested.

1. True False Every individual or married couple is required to file a federal income tax

return regardless of the amount of income earned.

2. True False The amount of federal income tax withheld depends on both your level of

earnings and the number of withholding allowances claimed.

3. True False Federal income taxes are levied against the total amount of money earned.

4. True False Gains on the sale of investments such as stocks, bonds, and real estate are

taxed at the lower capital gains tax rate.

5. True False Tax credits and deductions reduce your taxable income by comparable

amounts.

6. True False An easy way to earn tax-deferred income is to invest in Series EE savings

bonds.

Answers:

YOU CAN DO IT NOW

The “You Can Do It Now” cases may be assigned to the students as short cases or problems.

They will help make the topic more real or relevant to the students. In most cases, it will only

take about ten minutes to do, that is, until the student starts looking around at the web site. But

they will learn by doing so.

Tax Planning

Solutions to Financial Planning Exercises

1. Calculating marginal tax rates. Lacey Hansen is single and received the following items

and amounts of income during 2018, as shown below. Determine the marginal tax rate

applicable to each item. Note that if the item is not taxable, the marginal rate is 0.

2. Estimating taxable income, tax liability, and potential refund. Anabella Cunningham is 24

years old and single, lives in an apartment, and has no dependents. Last year she earned

$55,000 as a sales representative for Planning Associates; $3,910 of her wages were

withheld for federal income taxes. In addition, she had interest income of $142. She takes

the standard deduction. Calculate her taxable income, tax liability, and tax refund or tax

owed for 2018.

3. Calculating Taxes on security transactions. If Julia Diaz is single and in the 24 percent

tax bracket, calculate the tax associated with each of the following transactions. (Use the

IRS regulations for capital gains in effect in 2018.) Treat each of the following cases as

independent of the others.

a. She sold stock for $1,200 that she purchased for $1,000 5 months earlier.

b. She sold bonds for $4,000 that she purchased for $3,000 3 years earlier.

c. She sold stock for $1,000 that she purchased for $1,500 15 months earlier.

© 2020 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole

or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a

password-protected website or school-approved learning management system for classroom use.

4. Education Tax Credits. Mason is married and has two sons. The older son, Harrison, is

a graduate student working on his MBA. He paid $15,000 in tuition, $2,000 for textbooks

and supplies, and incurred $20,000 in living expenses for the year. The younger son,

Alexander, is a sophomore in college. Alexander’s tuition was $12,000, textbooks and

supplies were $1,500, and Alexander’s living expenses were $18,000. While Mason’s

younger son, Alexander, is claimed as a dependent on his return, his older son, Harrison, is

not claimed as a dependent.

Determine the amount of education credits or deductions Mason can take on his tax return

for these education expenses.

The available educations credits and deductions are:

In summary, total credits of $4,500 and a $4,000 deduction for tuition and fees.

5. Calculating taxable income for a married couple filing jointly. Freya and Sebastian Hunter

are married and have one child. Sebastian is putting together some figures so that he can

prepare the Hunter’s joint 2018 tax return. So far, he’s been able to determine the

following concerning income and possible deductions:

Total unreimbursed medical expenses incurred $ 1,155

Gross wages and commissions earned 50,770

IRA contribution 5,000

Mortgage interest paid 5,200

Capital gains realized on assets held less than 12 months 1,450

Income from limited partnership 200

Interest paid on credit cards 380

Qualified Dividend income earned 610

Sales taxes paid 2,470

Charitable contributions made 1,200

Capital losses realized 3,475

Interest paid on a car loan 570

Social Security taxes paid 2,750

Property taxes paid 700

State income taxes paid 1,700

Given this information, determine the amount of the available itemized deductions. How

much taxable income will the Compton’s have in 2018? (Note: Assume that Sebastian is not

covered by a pension plan where he works, his child qualifies for the child tax credit, and

the standard deduction of $24,000 for married filing jointly applies.

Income

Gross wages

$50,770

Income from Limited Partnership

200

Capital gains-short term

$1,450

Capital Losses

(3,475)

Net capital loss

(2,025)

Qualified Dividends

610

Total income

$49,555

Adjustments to income

IRA Contribution

$5,000

Adjusted Gross Income

$44,555

Less: Standard Deduction

$24,000

Taxable Income

$20,555

Less Qualified dividends

(610)

Ordinary taxable income

$19,945

Ordinary income tax

1,905 + [(19,945 – 19,050) * 12%]

$2, 012.40

Tax on qualified dividends @0%

0

Less Child Tax Credit

(2,000.00)

Income Tax Liability

$12.40

Notes: The qualified dividends are subject to the alternative tax of 0% since the ordinary tax rate

is 12%.

Total Itemized Deductions: The total of the itemized deductions is $9,570, which is less than

the standard deduction of $24,000. Thus, the standard deduction is used. The itemized

deductions are:

Total unreimbursed medical

expenses incurred

$ 1,155 less 7.5% of AGI, thus 0 deductible

(10% in 2019 and beyond)

Mortgage interest paid

5,200

Sales taxes paid

2,470 [Since Sales tax is greater than state

income tax paid (1,700), deduct sales tax]

Property taxes paid

700

Charitable contributions made

1,200

Total itemized deductions

$9,570

Nondeductible items: Interest paid on credit cards, Interest paid on a car loan, and Social

Security taxes paid are personal items and are not deductible.

The Hunters would qualify for the earned income credit. The credit would be $101 for adjusted

gross income for $44,555 with one child. This computation is beyond the scope of the text and is

given only for your information.

6. Choosing and Preparing an individual tax form. Liam McKenzie is single, graduated

from college in 2018 and began work as a systems analyst in July of that year. He is

preparing to file his income tax return for 2018 and has collected the following financial

information for that calendar year. A blank Form 1040 and Schedule 1 may be obtained at

www.irs.gov.

Scholarship used to pay Tuition $ 5,750

Scholarship used to pay room, and board 1,850

Salary 55,000

Interest income 185

Itemized Deductions 3,000

Income taxes withheld 2,600

a. Prepare Liam’s 2018 tax return, using a $12,000 standard deduction and the tax rates

given in Exhibit 3.3.

b. Prepare Liam’s 2018 tax return using the data in part a, along with the following

information:

IRA contribution $5,000

Cash dividends received 150

7. Effect of tax credit v tax deduction. Explain and calculate the differences resulting from a

$1,000 tax credit versus a $1,000 tax deduction for a single taxpayer with $40,000 of pre-tax

income.

8. Preparing for a tax audit. Paige and Landon Diamond have been notified that they are

being audited. What should they do to prepare for the audit?

9. Getting help with tax form preparation. Noah King’s job doesn’t leave him much spare

time. Consequently, he would like some help preparing his federal tax forms. What advice

would you give Noah?