2-11 Describe the cash budget and its three parts. How does a budget deficit differ from a budget

surplus?

2-12 The Gonzales family has prepared their annual cash budget for 2016. They have divided it into 12

monthly budgets. Although only 1 monthly budget balances, they have managed to balance the overall

budget for the year. What remedies are available to the Gonzales family for meeting the monthly budget

deficits?

2-13 Why is it important to analyze actual budget surpluses or deficits at the end of each month?

2-14 Why is it important to use time value of money concepts in setting personal financial goals?

2-15 What is compounding? Explain the rule of 72.

Interest is earned over a given period of time. When interest is compounded, this given period of time is

2-16 When might you use future value? Present value? Give specific examples.

Solutions to Critical Thinking Cases

2.1 The Becker’s Version of Financial Planning

Terry and Evelyn Becker are a married couple in their mid-20s. Terry has a good start as an electrical

engineer and Evelyn works as a sales representative. Since their marriage four years ago, Terry and

Evelyn have been living comfortably. Their income has exceeded their expenses, and they have

accumulated an enviable net worth. This includes $10,000 that they have built up in savings and

investments. Because their income has always been more than enough for them to have the lifestyle they

desire, the Beckers have done no financial planning.

Evelyn has just learned that she’s two months pregnant. She’s concerned about how they’ll make ends

meet if she quits work after their child is born. Each time she and Terry discuss the matter, he tells her

not to worry because “we’ve always managed to pay our bills on time.” Evelyn can’t understand his

attitude because her income will be completely eliminated. To convince Evelyn that there’s no need for

concern, Terry points out that their expenses last year, but for the common stock purchase, were about

equal to his take-home pay. With an anticipated promotion and an expected 10 percent pay raise, his

income next year should exceed this amount. Terry also points out that they can reduce luxuries (trips,

recreation, and entertainment) and can always draw down their savings or sell some of their stock if they

get in a bind. When Evelyn asks about the long-run implications for their finances, Terry says there will

be “no problems” because his boss has assured him that he has a bright future with the engineering firm.

Terry also emphasizes that Evelyn can go back to work in a few years if necessary.

Despite Terry’s arguments, Evelyn feels that they should carefully examine their financial condition in

order to do some serious planning. She has gathered the following financial information for the year

ending December 31, 2016:

Salaries Take-home Pay Gross Salary

Terry $52,500 $76,000

Evelyn 29,200 42,000

Item Amount

Food $ 5,902

Clothing 2,300

Mortgage payments, including property taxes of $1,400 11,028

Travel and entertainment card balances 2,000

Gas, electric, water expenses 1,990

Household furnishings 4,500

Telephone 640

Auto loan balance 4,650

Common stock investments 7,500

Bank credit card balances 675

Federal income taxes 22,472

State income tax 5,040

Social security contributions 9,027

Credit card loan payments 2,210

Cash on hand 85

2012 Nissan Sentra 10,500

Medical expenses (unreimbursed) 600

Homeowner’s insurance premiums paid 1,300

Checking account balance 485

Auto insurance premiums paid 1,600

Transportation 2,800

Cable television 680

Estimated value of home 185,000

Trip to Europe 5,000

Recreation and entertainment 4,000

Auto loan payments 2,150

Money market account balance 2,500

Purchase of common stock 7,500

Addition to money market account 500

Mortgage on home 148,000

Critical Thinking Questions

1. Using this information and Worksheets 2.1 and 2.2, construct the Becker’s balance sheet and

income and expense statement for the year ending December 31, 2016.

Critical Thinking 2–1 part 1

Date

Liquid Assets: Current Libaiblities

Cash on hand 85.00$ Utilities

Cash in checking 485.00 Rent

Savings accounts Insurance premiums

Taxes

2,500.00 Medical/dental bills

Repair bills

Total Liquid Assets 3,070.00$ 675.00

Investments

Stocks 7,500.00$ 2,000.00

Recreational vehicles

Real estate investment

Gas and other credit

Bank line of credit balances

Other

Total Personal Property

15,000.00$ Net Worth 55,245.00$

Total Assets 210,570.00$ Total Liabilities and Net Worth 210,570.00$

Money market funds and deposits

Certificates of deposit <1 yr to

maturity

Balance Sheet

Names(s) Terry and Evelyn Becker

31-Dec–16

Assets

Liabilities and Net Worth

Bank credit card balances

Department store credit

card balances

Travel and entertainment

card balances

Critical Thinking 2-1, Part 1 — Worksheet 2.2

Name(s) Terry and Evelyn Becker

For the Year Ending 31-Dec-16

Income

Wages and salaries Name Terry 76,000.00$

Name Evelyn 42,000.00

Name

Sale of securities

Other

Pensions and annuities

Other income Reimbursements for Travel Exp

Total Income 118,000.00$

Repairs, maintenance, improvements

Utilities Gas, electric, water 1,990.00

Phone 640.00

Doctor, dentist, hospital, medicines 600.00

Clothing Clothes, shoes, and accessories 2,300.00

Insurance Homewoner’s (if not covered by mortgage) 1,300.00

Life (not provided by employer)

Auto 1,600.00

Taxes Income and Social security 36,539.00

Property (if not included in mortgage)

Income and Expense Statement

2. Comment on the Becker’s financial condition regarding (a) solvency, (b) liquidity, (c) savings,

and (d) ability to pay debts promptly. If the Becker’s continue to manage their finances as

described, what do you expect the long-run consequences to be? Discuss.

3. Critically evaluate the Becker’s approach to financial planning. Point out any fallacies in

Terry’s arguments, and be sure to mention (a) implications for the long term, as well as (b) the

potential impact of inflation in general and specifically on their net worth. What procedures

should they use to get their financial house in order? Be sure to discuss the role that long- and

short-term financial plans and budgets might play.

2.2 Brooke Stauffer Learns to Budget

Brooke Stauffer recently graduated from college and moved to Atlanta to take a job as a market research

analyst. She was pleased to be financially independent and was sure that, with her $45,000 salary, she

could cover her living expenses and have plenty of money left over to furnish her studio apartment and

enjoy the wide variety of social and recreational activities available in Atlanta. She opened several

department-store charge accounts and obtained a bank credit card. For a while, Brooke managed pretty

well on her monthly take-home pay of $2,893, but by the end of 2016, she was having trouble fully paying

all his credit card charges each month. Concerned that her spending had gotten out of control and that

she was barely making it from paycheck to paycheck, she decided to list her expenses for the past

calendar year and develop a budget. She hoped not only to reduce her credit card debt but also to begin a

regular savings program.

Brooke prepared the following summary of expenses for 2016:

Item

Annual Expenditure

Rent

$12,000

Auto insurance

1,855

Auto loan payments

3,840

Auto expenses (gas, repairs,

and fees)

1,560

Clothing

3,200

Installment loan for stereo

540

Personal care

424

Phone

600

Cable TV

440

Gas and electricity

1,080

Medical care

120

Dentist

70

Groceries

2,500

Dining out

2,600

Furniture purchases

1,200

Recreation and entertainment

2,900

Other expenses

600

After reviewing his 2016 expenses, Brooke made the following assumptions about her expenses for 2017:

1. All expenses will remain at the same levels, with these exceptions:

a. Auto insurance, auto expenses, gas and electricity, and groceries will increase 5 percent.

b. Clothing purchases will decrease to $2,250.

c. Phone and cable TV will increase $5 per month.

d. Furniture purchases will decrease to $660, most of which is for a new television.

e. She will take a one-week vacation to Colorado in July, at a cost of $2,100.

2. All expenses will be budgeted in equal monthly installments except for the vacation and these items:

a. Auto insurance is paid in two installments due in June and December.

b. She plans to replace the brakes on her car in February, at a cost of $220.

c. Visits to the dentist will be made in March and September.

3. She will eliminate her bank credit card balance by making extra monthly payments of $75 during each

of the first six months.

4. Regarding her income, Brooke has just received a small raise, so her take-home pay will be $3,200 per

month.

Critical Thinking Question

1. a. Prepare a preliminary cash budget for Brooke for the year ending December 31, 2016,

using the format shown in Worksheet 2.3.

b. Compare Brooke’s estimated expenses with his expected income and make

recommendations that will help him balance her budget.

2. Make any necessary adjustments to Brooke’s estimated monthly expenses, and revise her annual

cash budget for the year ending December 31, 2016, using Worksheet 2.3.

3. Analyze the budget and advise Brooke on her financial situation. Suggest some long-term,

intermediate, and short-term financial goals for Brooke, and discuss some steps she can take to

reach them.

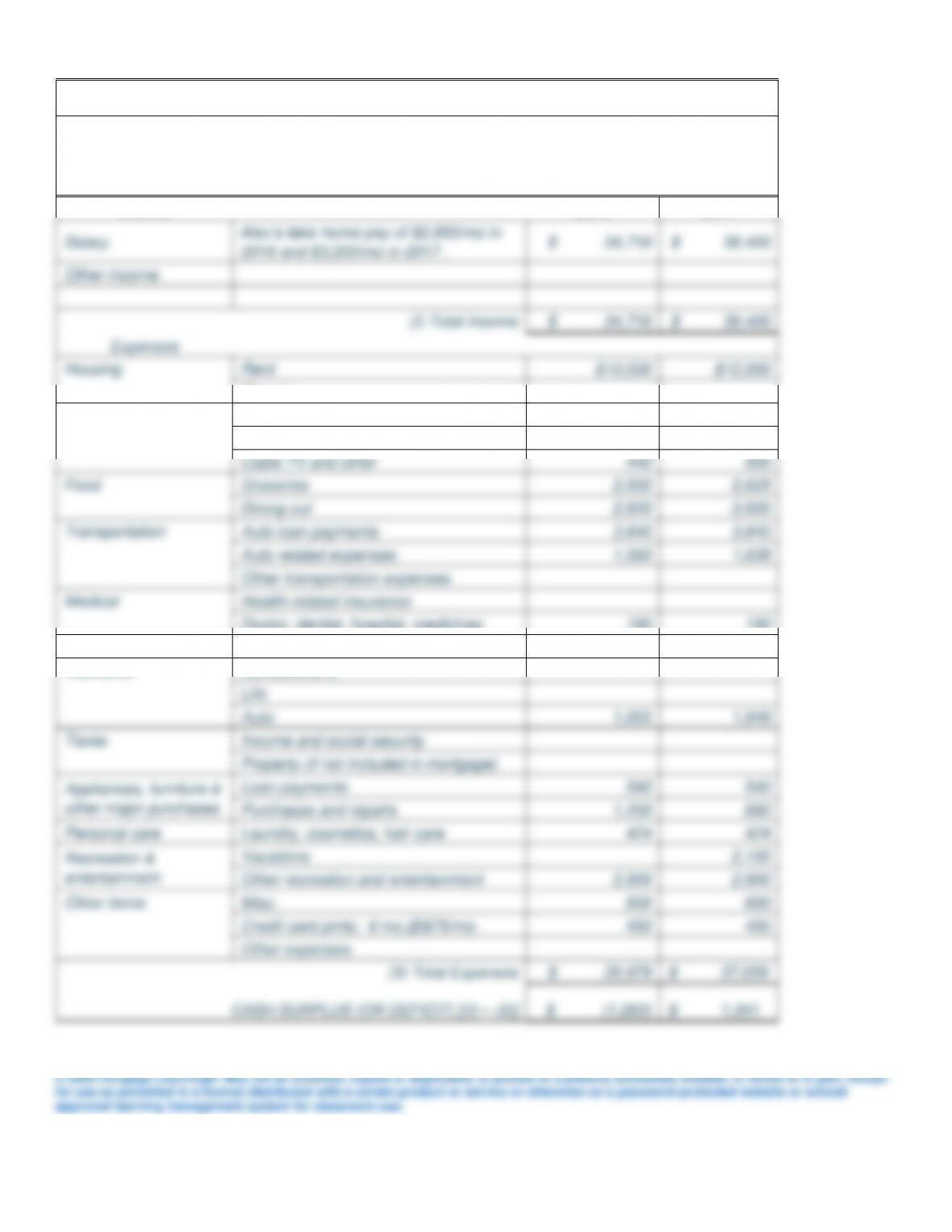

Case 2.2, Problem 1a

Income and Expense Statement

Name:

Brooke Stauffer

For the Year Ending December 31, 2016

Income

2016

2017

Salary

Alex’s take-home pay of $2,893/mo in

2016 and $3,200/mo in 2017 .

$ 34,716

$ 38,400

Other income

(I) Total Income

$ 34,716

$ 38,400

Expenses

Housing

Rent

$12,000

$12,000

Repairs

Utilities

Gas, electric, water

1,080

1,134

Phone

600

660

Cable TV and other

440

500

Food

Groceries

2,500

2,625

Dining out

2,600

2,600

Transportation

Auto loan payments

3,840

3,840

Auto related expenses

1,560

1,638

Other transportation expenses

Medical

Health-related insurance

Doctor, dentist, hospital, medicines

190

190

Clothing

Clothes, shoes, accessories

3,200

2,250

Insurance

Homeowner’s

Life

Auto

1,855

1,948

Taxes

Income and social security

Property (if not included in mortgage)

Appliances, furniture &

other major purchases

Loan payments

540

540

Purchases and repairs

1,200

660

Personal care

Laundry, cosmetics, hair care

424

424

Recreation &

entertainment

Vacations

2,100

Other recreation and entertainment

2,900

2,900

Other items

Misc.

600

600

Credit card pmts: 6 mo.@$75/mo.

450

450

Other expenses

(II) Total Expenses

$ 35,979

$ 37,059

CASH SURPLUS (OR DEFICIT) [(I) – (II)]

$ (1,263)

$ 1,341

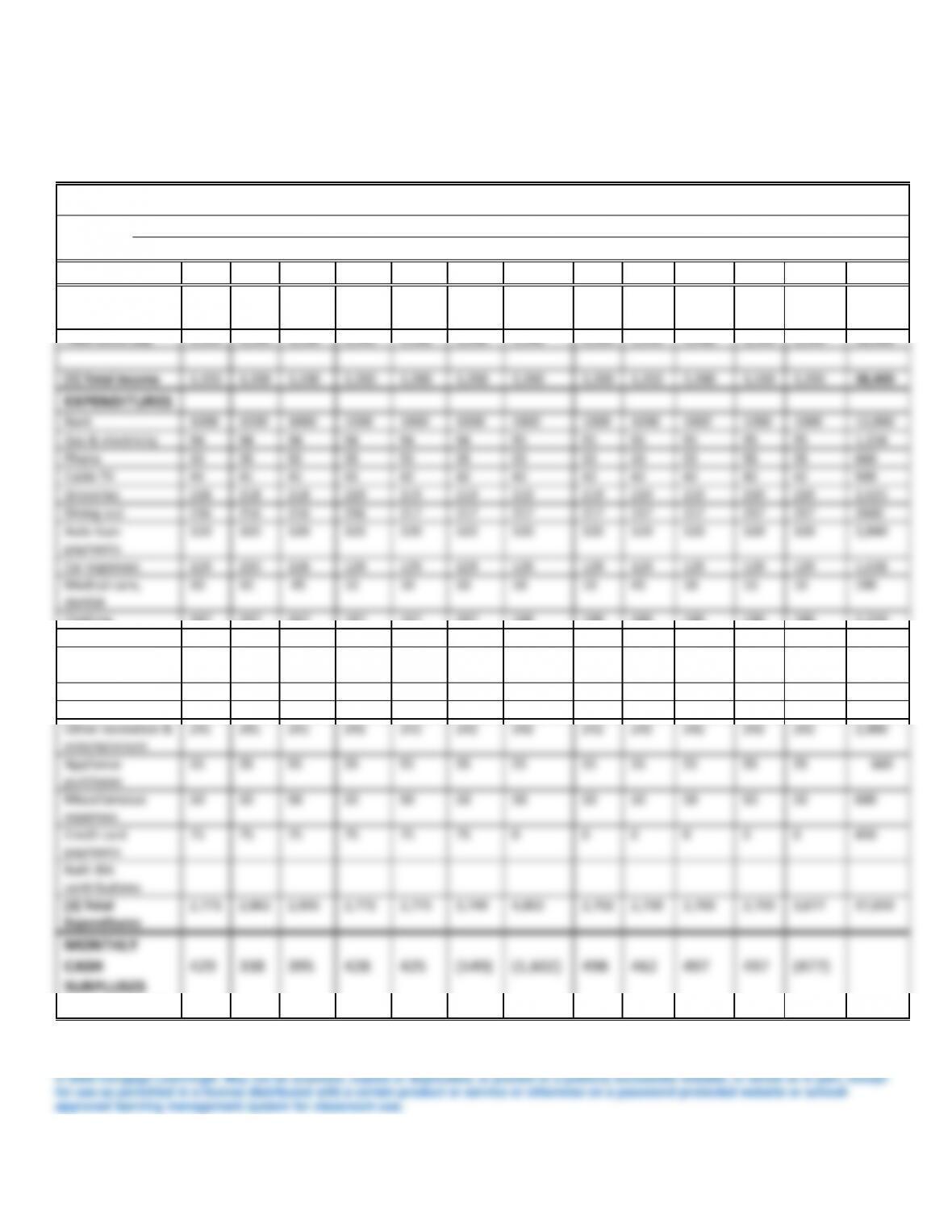

Case 2.2, Problem 2—Worksheet 2.3

ANNUAL CASH BUDGET BY MONTH

Name(s)

Brooke Stauffer

For

the

Year

ending

December 31, 2017

INCOME

Jan.

Feb.

Mar.

Apr.

May

June

July

Aug

.

Sept

.

Oct.

Nov.

Dec.

Total

Take-home pay

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

38,400

[1] Total Income

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

3,200

38,400

EXPENDITURES

Rent

1000

1000

1000

1000

1000

1000

1000

1000

1000

1000

1000

1000

12,000

Gas & electricity

94

94

94

94

94

94

95

95

95

95

95

95

1,134

Phone

55

55

55

55

55

55

55

55

55

55

55

55

660

Cable TV

41

41

41

41

42

42

42

42

42

42

42

42

500

Groceries

218

218

218

219

219

219

219

219

219

219

219

219

2,625

Dining out

216

216

216

216

217

217

217

217

217

217

217

217

2600

Auto loan

payments

320

320

320

320

320

320

320

320

320

320

320

320

3,840

Car expenses

129

220

128

129

129

129

129

129

129

129

129

129

1,638

Medical care,

dentist

10

10

45

10

10

10

10

10

45

10

10

10

190

Clothing

187

187

187

187

187

187

188

188

188

188

188

188

2,250

Auto insurance

0

0

0

0

0

974

0

0

0

0

0

974

1,948

Installment loan

for stereo

45

45

45

45

45

45

45

45

45

45

45

45

540

Personal care

35

35

35

35

35

35

35

35

36

36

36

36

424

Vacation

0

0

0

0

0

0

2,100

0

0

0

0

0

2,100

Other recreation &

entertainment

241

241

241

241

242

242

242

242

242

242

242

242

2,900

Appliance

purchases

55

55

55

55

55

55

55

55

55

55

55

55

660

Miscellaneous

expenses

50

50

50

50

50

50

50

50

50

50

50

50

600

Credit card

payments

75

75

75

75

75

75

0

0

0

0

0

0

450

Roth IRA

contributions

[2] Total

Expenditures

2,771

2,862

2,805

2,772

2,775

3,749

4,802

2,702

2,738

2,703

2,703

3,677

37,059

MONTHLY

CASH

SURPLUSES

(DEFICIT) [1-2]

429

338

395

428

425

(549)

(1,602)

498

462

497

497

(477)

CUMULATIVE

CASH SURPLUS

(DEFICIT)

429

767

1,162

1,590

2,015

1,466

(136)

362

824

1,321

1,818

1,341

1,341

3. Analyze the budget and advise Brooke on her financial situation. Suggest some long-term,

intermediate, and short-term financial goals for Brooke, and discuss some steps she can take to reach

them.

Terms Found in the Chapter

annuity

A fixed sum of money that occurs annually.

assets

Items that one owns.

balance sheet

A financial statement that describes a person’s financial

position at a given point in time.

budget

A detailed financial report that looks forward, based on

expected income and expenses.

budget control

schedule

A summary that shows how actual income and expenses

compare with the various budget categories and where

variances (surpluses or deficits) exist.

budget variance

The difference between the budgeted and actual amount

paid out or received.

cash basis

A method of preparing financial statements in which only

transactions involving actual cash receipts or actual cash

outlays are recorded.

cash budget

A budget that takes into account estimated monthly cash

receipts and cash expenses for the coming year

cash deficit

An excess amount of expenses over income, resulting in

insufficient funds as well as in decreased net worth.

cash surplus

An excess amount of income over expenses that results in

increased net worth.

compounding

When interest earned each year is left in an account and

becomes part of the balance (or principal) on which interest

is earned in subsequent years.

current (short-

term) liability

Any debt due within 1 year of the date of the balance sheet.

debt service ratio

Total monthly loan payments divided by monthly gross

(before-tax) income; provides a measure of the ability to

pay debts promptly.

discounting

The process of finding present value; the inverse of

compounding to find future value.

equity

The actual ownership interest in a specific asset or group of

assets.

expenses

Money spent on living costs and to pay taxes, purchase

assets, or repay debt.

fair market value

The actual value of an asset, or the price for which it can

reasonably be expected to sell in the open market.

financial plans

Describes financial goals and provides the action plans for

their achievement

future value

The value to which an amount today will grow if it earns a

specific rate of interest over a given period.

fixed expenses

Contractual, predetermined expenses involving equal

payments each period.

income and

expense statement

A financial statement that measures financial performance

over time.

income

Earnings received as wages, salaries, bonuses, commissions,

interest and dividends, or proceeds from the sale of assets.

insolvency

The financial state in which net worth is less than zero.

investments

Assets such as stocks, bonds, mutual funds, and real estate

that are acquired in order to earn a return rather than

provide a service.

liabilities

Debts such as credit card charges, loans, and mortgages.

liquid assets

Assets that are held in the form of cash or that can readily

be converted to cash with little or no loss in value.

liquidity ratio

Total liquid assets divided by total current debts; measures

the ability to pay current debts.

long-term liability

Any debt due 1 year or more from the date of the balance

sheet.

net worth

An individual’s or family’s actual wealth; determined by

subtracting total liabilities from total assets.

open account

credit

obligations

Current liabilities that represent the balances outstanding

against established credit lines.

personal financial

statement

Balance sheets and income and expense statements that

serve as essential planning tools for developing and

monitoring personal financial plans

present value

The value today of an amount to be received in the future;

it’s the amount that would have to be invested today at a

given interest rate over a specified time period to

accumulate the future amount.

personal property

Tangible assets that are movable and used in everyday life.

real rate of return

The rate of return earned after adjusting for the effect of

inflation, also referred to as the real interest rate

real property

Tangible assets that are immovable: land and anything fixed

to it, such as a house.

rule of 72

A useful formula for estimating about how long it will take

to double a sum at a given interest rate.

savings ratio

Cash surplus divided by net income (after tax);indicates

relative amount of cash surplus achieved during a given

period.

solvency ratio

Total net worth divided by total assets; measures the degree

of exposure to insolvency.

timeline

A graphical presentation of cash flows.

time value of

money

The concept that a dollar today is worth more than a dollar

received in the future.

variable expenses

Expenses involving payment amounts that change from one

time period to the next.

Chapter Outline

Learning Goals

I. Mapping Out Your Financial Future

A. The Role of Financial Statements in Financial Planning

B. Interlocking Network of Financial Plans and Statements

II. The Balance Sheet: How Much Are You Worth Today?

A. Assets: The Things You Own

B. Liabilities: The Money You Owe

C. Net Worth: A Measure of Your Financial Worth

D. Balance Sheet Format and Preparation

E. A Balance Sheet for Jack and Lily Taylor

III. The Income and Expense Statement: What We Earn and Where It Goes

A. Income: Cash In

B. Expenses: Cash Out

C. Cash Surplus (or Deficit)

D. Preparing the Income and Expense Statement

E. An Income and Expense Statement for Jack and Lily Taylor

IV. Using Your Personal Financial Statements

A. Keeping Good Records

B. Managing Your Financial Records

C. Tracking Financial Progress: Ratio Analysis

D. Balance Sheet Ratios

E. Income and Expense Statement Ratios

V. Cash In and Cash Out: Preparing and Using Budgets

A. The Budgeting Process

B. Forecasting Income

C. Forecasting Expenses

D. Finalizing the Cash Budget

E. Dealing with Deficits

F. A Cash Budget for Jack and Lily Taylor

E. Using Your Budgets

VI. The Time Value of Money: Putting a Dollar Value on Financial Goals

A. Future Value

B. Future Value of a Single Amount

C. Future Value of an Annuity

D. Present Value

1. Present Value of a Single Amount

2. Present Value of an Annuity

3. Other Applications of Present Value

VII. Inflation and Interest Rates

A. Impact of inflation on financial plan

B. Fisher equation

Planning over a Lifetime

Financial Impact of Personal Choices

Financial Planning Exercises