Chapter

Using Financial

Statements and Budgets

Chapter 2

How Will This Affect Me?

A recent survey shows that more than half of adult Americans could not cover six months of living expenses or

the cost of medical emergencies. And younger millennials between the ages of 18 to 24 are the least prepared.

This is scary . . . and this chapter explains what you can do to avoid being part of that alarming statistic.

Everyone knows it’s hard to get where you need to go if you don’t know where you are. Financial goals

describe your destination, and financial statements and budgets are the tools that help you determine exactly

where you are in the journey. This chapter helps you define your financial goals and explains how to gauge your

progress carefully over time.

Hopefully most of your students have had a semester of financial accounting. If so, while this chapter will be a

review for them, they may need help understanding the differences between cash and accrual accounting. The

chapter deals with cash accounting; the previous accounting course dealt with accrual accounting. If they have

not had an accounting course, the students may have a hard time. If this material is new to them, it will be

helpful if you go over worksheets (2.1 and 2.2) and then discuss the Financial Planning Exercises 3 (preparing a

personal balance sheet) and 4 (preparing a personal income and expense statement).

The Facts or Fantasies are true false questions designed to create interest in the chapter. They are below and in

the power points for the chapter.

Learning Goals

LG 2-1 Understand the relationship between financial plans and statements.

The statement above “it’s hard to get where you need to go if you don’t know where you are” is very true. The

LG 2-2 Prepare a personal balance sheet.

The Balance Sheet computes the net worth as of a given date. The Balance sheet formula [Total Assets = Total

not. While liquid assets and investments may look the same, their purpose is very different. The liquid assets

LG 2-3 Generate a personal income and expense statement.

While the balance sheet reports financial position as of a given day, the income statement covers a stated period,

typically a month, quarter, or year. A useful exercise is to ask the class “is income gross pay or net pay?” If

LG 2-4 Develop a good record-keeping system and use ratios to evaluate personal financial statements.

Without records, you are flying blind. It like the person who says they can spend money as long as they have a

LG 2-5 Construct a cash budget and use it to monitor and control spending.

The income statement reports the cash surplus or deficit for the period. But is the surplus of $2,000 good or not.

LG 2-6 Apply time value of money concepts to put a monetary value on financial goals.

Financial plans are concerned with what future amounts you will need to be able to provide for your desired

LG 2-7 Understand the relationship between inflation and nominal interest rates and calculate the real interest

rate.

Inflation is arguably the most prominent source of investment risk and is a key driver of interest rates. It is

Financial Facts or Fantasies?

These may be used as “teasers” to get the students on the right page with you. Also, they may be used as

quizzes after you covered the material or as “pre–test questions” to get their attention.

• Because financial statements are used to record actual results, they’re really not that important in personal

financial planning.

• A leased car should be listed as an asset on your personal balance sheet.

• Only the principal portion of a loan should be recorded on the liability side of a balance sheet.

• Generating a cash surplus is desirable, because it adds to your net worth.

Fact: You can only increase your net worth by generating a cash surplus, someone giving you additional

assets, or through increases in market values. The only one of the three you control is generating cash surplus.

Financial Facts or Fantasies?

These may be used as a quiz or as a pre-test to get the students interested.

1. True False Whereas the balance sheet summarizes your financial condition at a given point in time, the

income and expense statement reports on your financial performance over time.

2. True False Because financial statements are used to record actual results, they’re really not that important in

personal financial planning.

3. True False A leased car should be listed as an asset on your personal balance sheet.

4. True False Only the principal portion of a loan should be recorded on the liability side of a balance sheet.

5. True False Generating a cash surplus is desirable, because it adds to your net worth.

6. True False When evaluating your income and expenses statement, primary attention should be given to the

top line: income received.

YOU CAN DO IT NOW

The “You Can Do It Now” cases may be assigned to the students as short cases or problems. They will help

make the topic more real or relevant to the students. In most cases, it will only take about ten minutes to do,

that is, until the student starts looking around at the web site. But they will learn by doing so.

Track Your Expenses

It’s easy for spending to become so automatic that we’re not aware we’re doing it. So where does your money

go? The only way to find out is to keep track of it. Writing down what you spend in a paper journal or using an

app like Expensify (www.expensify.com) is simple and will make you more aware of where your money goes.

Knowing where you are will probably make you feel better too – so do it now.

Save Automatically

We all know we should save regularly. One way to create a savings “habit” is to literally make it automatic.

Open a savings account apart from your checking account. This will separate your savings from what you have

available to spend. And then set up an automatic deposit or transfer from your checking account to your savings

account each month. This sets your “habit.” You can do it now.

Financial Impact of Personal Choices

Read and think about the choices being made. Do you agree or not? Ask the students to discuss the choices

being made.

No Budget, No Plan: Tyler Bought a Boat!

Tyler is 28 and has a good job as a sales rep. He’s always found budgeting boring and has been intending to start

a financial plan for years.

Recently Tyler went out with some friends on a rented boat to fish. He had a great time and saw a boat for sale

on his way home. Before he knew it, the salesman convinced Tyler that the deal was just too good to pass up.

So Tyler bought a $10,000 boat and financed 80 percent of the cost for the next 5 years. Sean now finds himself

relying more on his credit card to get by each month.

What if Tyler had kept track of his money, used a budget, and had a set of financial goals? Knowing where his

money went and having a financial plan would have increased the chance that Tyler would make more

deliberate, informed financial decisions.

Solutions to Financial Planning Exercises

1. Financial plans v statements: Describe and distinguish financial plans and statements.

2. Preparing Financial Statements: Hugo Garcia is preparing his balance sheet and income and

expense statement for the year ending December 31, 2020. He is having difficulty classifying seven

items and asks for your help. Which, if any, of the following transactions are assets, liabilities,

income, or expense items?

a. Hugo rents a house for $1,350 a month.

b. On June 21, 2020, Hugo bought diamond earrings for his wife and charged them using his Visa

card. The earrings cost $900, but he hasn’t yet received the bill.

c. Hugo borrowed $3,500 from his parents last fall, but so far, he has made no payments to them.

d. Hugo makes monthly payments of $225 on an installment loan; about half of it is interest, and the

balance is repayment of principal. He has 20 payments left, totaling $4,500.

e. Hugo paid $3,800 in taxes during the year and is due a tax refund of $650, which he hasn’t yet

received.

f. Hugo invested $2,300 in a mutual fund.

g. Hugo’s Aunt Lydia gave him a birthday gift of $300.

The gift increases his cash account and he has no obligation to repay. So, the amount is reported on his

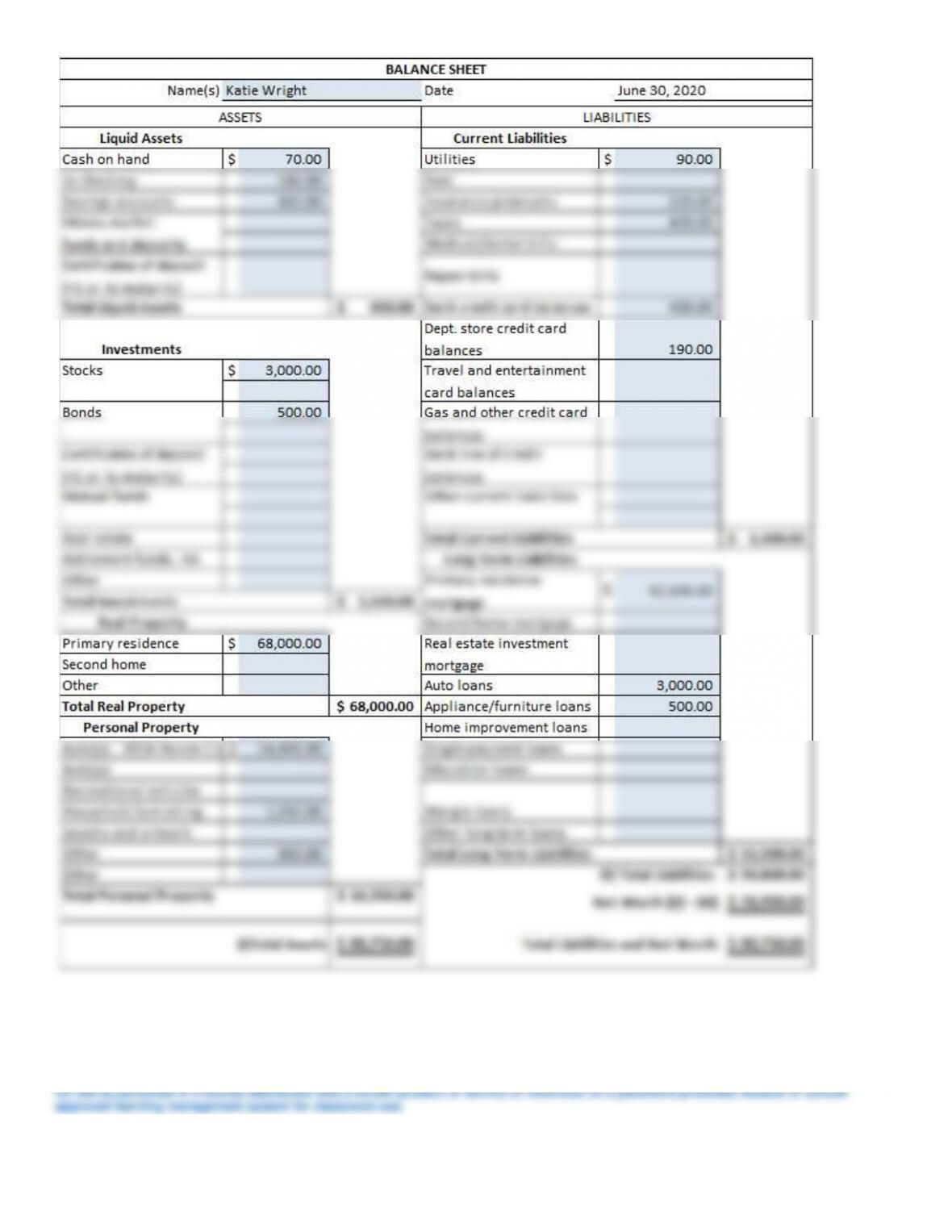

3. Preparing Personal Balance Sheet: Use Worksheet 2.1 Katie Wright’s banker has asked her to submit

a personal balance sheet as of June 30, 2020, in support of an application for a $6,000 home improvement

loan. She comes to you for help in preparing it. So far, she has made the following list of her assets and

liabilities as of June 30, 2016:

Cash on hand $ 70

Balance in checking account 180

Balance in money market deposit account with

Southwest Savings 650

Bills outstanding:

Telephone $ 20

Electricity 70

Charge account balance 190

Visa 180

MasterCard 220

Taxes 400

Insurance 220 1,300

Condo and property 68,000

Condo mortgage loan 52,000

Automobile: 2016 Honda Civic 14,400

Installment loan balances:

Auto loans 3,000

Furniture loan 500 3,500

Personal property:

Furniture 1,050

Clothing 900 1,950

Investments:

U.S. government savings bonds 500

Apple Stock 3,000 3,500

From the data given, prepare Katie Wright’s balance sheet, dated June 30, 2020 (follow the balance sheet

form shown in Worksheet 2.1). Then evaluate her balance sheet relative to the following factors: (a)

solvency, (b) liquidity, and (c) equity in her dominant asset.

See following page for Worksheet 2.1 for Denise Fisher.

© 2020 Cengage Learning®. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part, except

3-a. Solvency Ratio: This term refers to having a positive net worth. The calculation for her solvency

ratio is as follows:

Total Current Debts $1,700

This means she can cover only about 53% of her current debt with her liquid assets. Rule of thumb, the

liquidity ration should be at least 1.

If we assume that her installment loan payments for the year are about $2,000 (half the auto loan

balance and all of the furniture loan balance) and add them to the bills outstanding, the liquidity ratio at

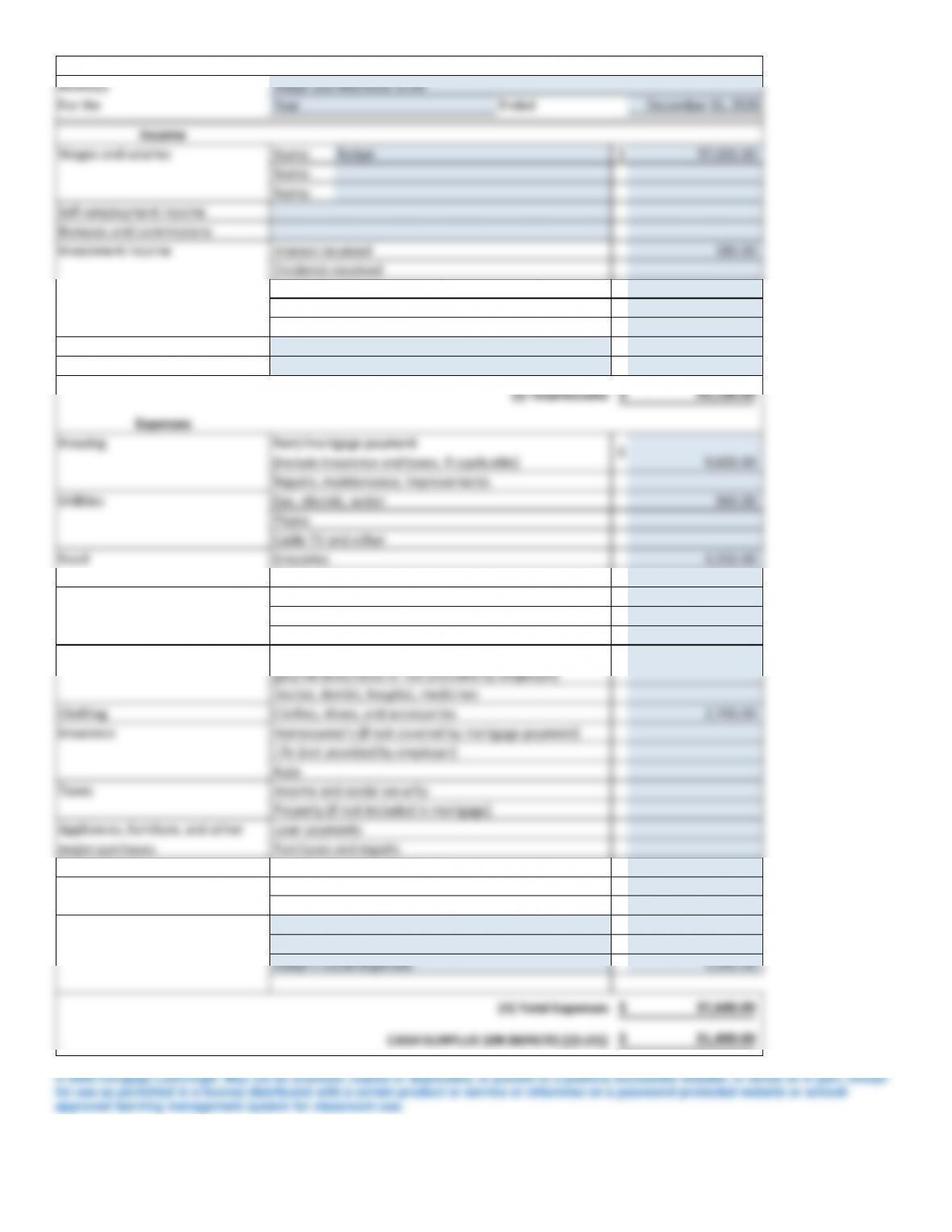

4. Preparing Income and Expense Statement: Use Worksheet 2.2. Robyn and Matthew Scott are about to

construct their income and expense statement for the year ending December 31, 2020. They have put

together the following income and expense information for 2020:

Robyn’s salary $57,000

Reimbursement for travel expenses 1,950

Interest on:

Savings account 110

Bonds of Alpha Corporation 70

Groceries 4,150

Rent 9,600

Utilities 960

Gas and auto expenses 650

Matthew’s tuition, books, and supplies 13,300

Books, magazines, and periodicals 280

Clothing and other miscellaneous expenses 2,700

Cost of photographic equipment

purchased with charge card 2,200

Amount paid to date on photographic equipment 1,600

Robyn’s travel expenses 1,950

Purchase of a used car (cost) 9,750

Outstanding loan balance on car 7,300

Purchase of bonds in Verizon Communication Inc 4,900

Using the information provided, prepare an income and expense statement for the Scotts for the year

ending December 31, 2020 (follow the form shown in Worksheet 2.2).

See worksheet on following page.

Issues: Purchase of bonds is a balance sheet transaction, a non-recurring conversion of cash to investment in

bonds. There is no expense; there is no impact on net worth. The payment of the auto loan could be left off the

expense statement since it is a reduction of an asset and a liability. However, the loan payment is a recurring

item and reporting it as an expense helps explain the change in cash. The determining factor is the recurring

nature and impact on net worth. The goal of all financial statements is to provide information. If the reader of

the statement needs to know about a transaction, that transaction should be on the financial statement.

Robyn’s travel expenses are off set by the reimbursement. There is no impact on net worth. However, it is a

recurring transaction and reporting it helps explain the change in the cash account. Reporting the expense may

also remind Robyn of an item that has not been reimbursed.

Name(s)

For the Ended December 31, 2020

Income

Name: $ 57,000.00

Name:

Name:

Self-employment income

Bonuses and commissions

180.00

Dividends received

Rents received

Sale of securities — Gain or Loss

Other: Reimbursement of Robyn‘s travel expenses

960.00

4,150.00

Medical

Health, major medical, disability insurance

(payroll deductions or not provided by employer)

Doctor, dentist, hospital, medicines

Clothes, shoes, and accessories

Transportation

Auto loan payments

License plates, fees, etc.

Gas, oil, repairs, tires, maintenance

Personal care

280.00

13,300.00

1,600.00

1,950.00

(II) Total Expenses

CASH SURPLUS (OR DEFICIT) [(I)–(II)]

Laundry, cosmetics, hair care

Vacations

37,640.00$

21,490.00$

$

9,600.00

Appliances, furniture, and other

major purchases

Loan payments

Purchases and repairs

Other recreation and entertainment

Other items

Matthew’s books, tuition, and supplies

Photographic equipment — amount paid

Robyn‘s travel expenses

Life (not provided by employer)

Auto

Taxes

Income and social security

Property (if not included in mortgage)

Food

Groceries

Dining out

Utilities

Gas, electric, water

Phone

Cable TV and other

Rent/mortgage payment

(include insurance and taxes, if applicable)

Repairs, maintenance, improvements

Investment income

Interest received

Housing

INCOME AND EXPENSE STATEMENT

Robyn and Matthew Scott

Year

Wages and salaries

Robyn

5. Preparing Cash Budget: Theo and Sophia Martinez are preparing their 2021 cash budget. Help the

Martinez family reconcile the following differences, giving reasons to support your answers.

a. Their only source of income is Theo’s salary, which amounts to $5,000 a month before taxes.

Sophia wants to show the $5,000 as their monthly income, whereas Theo argues that his take-

home pay of $3,917 is the correct value to show.

Like many questions it depends. If the taxes and other payroll deductions are considered out of their

b. Sophia wants to make a provision for fun money, an idea that Theo cannot understand.

He asks, “Why do we need fun money when everything is provided for in the budget?”

By having an allowance for “fun money,” the Martinez family have specifically set aside a certain

PLEASE NOTE: Problems 6 through 8 deal with time value of money, and solutions using both the tables and

6. Calculating present and future values: Use future or present value techniques to solve the following

problems.

a. If you inherited $45,000 today and invested all of it in a security that paid a 7 percent rate of

return, how much would you have in 25 years?

FV

=

PV x FV factor 7%, 25 yrs. (1+i)n

45000

+/–

PV

=

$45,000 x 5.427

7

I

=

$244,215

25

N

FV

$244,234.47

b. If the average new home costs $275,000 today, how much will it cost in 10 years if the price

increases by 5 percent each year?

FV

=

PV x FV factor 5%, 10 yrs. (1+.05)10

275000

+/–

PV

=

$275,000 x 1.629

5

I

=

$447,975

10

N

FV

$447,946.02

c. You forecast that in 15 years, it will cost $190,000 to provide your child with a 4-year college

education. Will you have enough if you take $75,000 today and invest it for the next 15 years at 4

percent?

No, you will have $135,071, which is less than your $190,000 goal.

FV

=

PV x FV factor 4%, 15 yrs.

75000

+/–

PV

=

$75,000 x 1.801

4

I

=

$135,071

15

N

FV

$135,070.76

d. If you can earn 4 percent, how much will you have to save each year if you want to retire in 35

years with $1 million?

c. To achieve his annual withdrawal goal of $35,000 calculated in part b., how much more than the

amount in part a. must Austin deposit today in an investment earning 4 percent annual interest.

8. Inflation and Interest Rates: Jessica Adams is 21 years old and has just graduated from college. In

considering the retirement investing options available at her new job, she is thinking about the long-term

effects of inflation. Help her by answering the following related questions.

a. Explain the effect of long-term inflation on meeting retirement financial planning goals.

b. If long-term inflation is expected to average 4 percent per year and you expect a long-term investment

return of 7 percent per year, what is your long-term expected real rate of return (adjusted for inflation)?

Be sure to consider the important impact of compounding.

2-1 What are the two types of personal financial statements? What is a budget, and how does it differ from

personal financial statements? What role do these reports play in a financial plan?

Personal financial statements provide important information needed in the personal financial planning process.

2-2 Describe the balance sheet, its components, and how you would use it in personal financial planning.

Differentiate between investments and real and personal property.

The balance sheet summarizes your financial position by showing your assets (what you own listed at fair

2-3 What is the balance sheet equation? Explain when a family may be viewed as technically insolvent.

2-4 Explain two ways in which net worth could increase (or decrease) from one period to the next.

There are basically two ways to achieve an increase in net worth. First, one could prepare a budget for

the pending period to specifically provide for an increase in net worth by acquiring more assets and/or

2-5 What is an income and expense statement? What role does it serve in personal financial planning?

2-6 Explain what cash basis means in this statement: “An income and expense statement

should be prepared on a cash basis.” How and where are credit purchases shown when statements are

prepared on a cash basis?

2-7 Distinguish between fixed and variable expenses, and give examples of each.

2-8 Is it possible to have a cash deficit on an income and expense statement? If so, how?

2-9 How can accurate records and control procedures be used to ensure the effectiveness of the personal

financial planning process?

2-10 Describe some of the areas or items you would consider when evaluating your balance sheet and

income and expense statement. Cite several ratios that could help in this effort.