12-4 What is interest on interest, and why is it such an important element of return?

Note that because the bond was originally bought at par ($1,000), you start off with a 4 percent

12-5 What is the desired rate of return, and how would it be used to make an investment

decision?

The value of any investment depends on the amount of return that it’s expected to provide

12-6 From a tax perspective, would it make any difference to an investor whether the

return on a stock took the form of dividends or capital gains? Explain.

Historically yes it mattered. However, for tax years beginning after 2012, qualified dividends

12-7 What’s the difference between a cash dividend and a stock dividend? Which would

you rather receive?

Cash dividends are paid to the stockholder in cash and are taxable at the capital gains rate. Stock

12-8 Define and briefly discuss each of these common stock measures: (a) book value, (b)

ROE, (c) EPS, (d) P/E ratio, and (e) beta.

The amount of stockholders’ equity [assets minus liabilities minus preferred stock] in a firm is

measured by book value. Book value indicates the amount of stockholder funds used to finance

the firm.

12-9 Briefly discuss some of the different types of common stock. Which types would be

most appealing to you, and why?

1. blue-chip stock A stock generally issued by companies expected to provide an uninterrupted

12-10 Summarize the evidence on the potential cost of being out of the stock market during

its best months.

A common myth: During volatile markets, it makes sense to sell your stocks and wait for

12-11 What are DRPs, and how do they fit into a stock investment program?

12-12 Go to the asset allocation tool provided at the following internet site:

http://www.ipers.org/calcs/AssetAllocator.html. Enter assumptions that fit your current

and anticipated situation and produce an asset allocation recommendation. Then add 20

years to your age and redo the calculations. Finally, redo the calculations assuming

minimal risk tolerance. Explain the results of changing these key assumptions.

12-13 What’s the difference between a secured bond and an unsecured bond?

12-14 Are junk bonds and zero coupon bonds the same? Explain. What are the basic tax

features of a tax-exempt municipal bond?

Zero coupon bonds, as the name implies, are bonds issued without coupons. To compensate for

12-15 What is a convertible bond, and why do investors buy convertible securities?

12-16 Describe the conversion privilege on a convertible security. Explain how the market

price of the underlying common stock affects the market price of a convertible bond.

12-17 Explain the system of bond ratings used by Moody’s and Standard & Poor’s. Why

would it make sense to ever buy junk bonds?

12-18 Explain the difference between dirty (full) and clean bond prices? What is the

significance of the difference in the prices for a bond buyer?

12-19 What effects do market interest rates have on the price behavior of outstanding

bonds?

Criterial Thinking Cases

12.1 The Madsen’s Problem: What to Do with All That Money?

A couple in their early 30s, Rodney and Carly Madsen recently inherited $90,000 from a

relative. Charles earns a comfortable income as a sales manager for System Analytics, Inc.,

and Carly does equally well as an attorney with a major law firm. Because they have no

children and don’t need the money, they’ve decided to invest all of the inheritance in

stocks, bonds, and perhaps even some money market instruments. However, because

they’re not very familiar with the market, they turn to you for help.

Critical Thinking Questions

1. What kind of investment approach do you think the Madsen should adopt—that is,

should they be conservative with their money or aggressive? Explain.

The Madsens do not have a specific goal that they are investing to reach. Also, they do not

2. What kind of stocks do you think the Madsen should invest in? How important is

current income (i.e., dividends or interest income) to them? Should they be putting any of

their money into bonds? Explain.

3. Construct an investment portfolio that you feel would be right for the Madsen and invest

the full $90,000. Put actual stocks, bonds, and/or convertible securities in the portfolio; you

may also put up to one-third of the money into short-term securities such as CDs, Treasury

bills, money funds, or MMDAs. Select any securities you want, so long as you feel they’d be

suitable for the Madsen. Make sure that the portfolio consists of six or more different

securities, and use the latest issue of The Wall Street Journal or an online source such as

http://finance.yahoo.com to determine the market prices of the securities you select. Show

the amount invested in each security along with the amount of current income (from

dividends and/or interest) that will be generated from the investments. Briefly explain why

you selected these particular securities for the Madsen’ portfolio.

12.2 Natasha Explores Investing

Natasha Cormier is a 28-year-old management trainee at a large chemical company. She is

single, has an annual salary of $34,000 (placing her in the 15 percent tax bracket), and her

monthly expenditures come to approximately $1,500. During the past year or so, Natasha

has managed to save around $8,000, and she expects to continue saving at least that amount

each year for the foreseeable future. Her company pays the premium on her $35,000 life

insurance policy. Because Natasha’s entire education was financed by scholarships, she was

able to save money from the summer and part-time jobs she held as a student. Altogether,

she has a nest egg of nearly $18,000, out of which she’d like to invest about $15,000. She’ll

keep the remaining $3,000 in a bank CD that pays 3 percent interest and will use this

money only in an emergency. Natasha can afford to take more risks than someone with

family obligations can, but she doesn’t wish to be a speculator; she simply wants to earn an

attractive rate of return on her investments.

Critical Thinking Questions

1. What investment options are open to Natasha?

2. What chance does she have of earning a satisfactory return if she invests her $15,000 in

(a) bluechip stocks, (b) growth stocks, (c) speculative stocks, (d) corporate bonds, or (e)

municipal bonds?

3. Discuss the factors you would consider when analyzing these alternate investment

vehicles.

4. What recommendation would you make to Natasha regarding her available investment

alternatives? Explain.

Terms Found in the Chapter

accrued interest

The amount of interest that’s been earned since the last coupon

payment date by the bond holder/seller, but which will be received by

the new owner/buyer of the bond at the next regularly scheduled

coupon payment date.

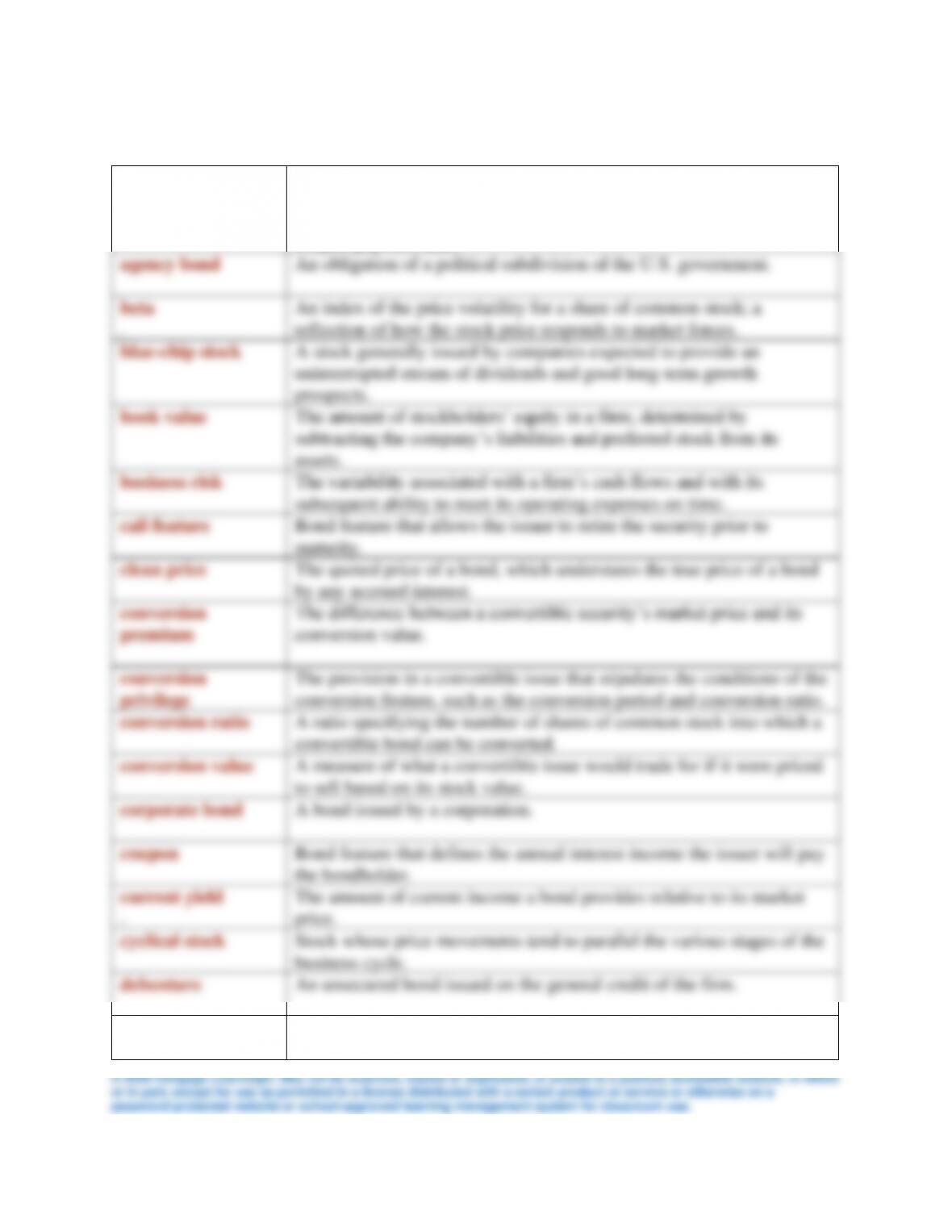

agency bond

An obligation of a political subdivision of the U.S. government.

beta

.

An index of the price volatility for a share of common stock; a

reflection of how the stock price responds to market forces.

blue-chip stock

A stock generally issued by companies expected to provide an

uninterrupted stream of dividends and good long-term growth

prospects.

book value

The amount of stockholders’ equity in a firm; determined by

subtracting the company’s liabilities and preferred stock from its

assets.

business risk

The variability associated with a firm’s cash flows and with its

subsequent ability to meet its operating expenses on time.

call feature

Bond feature that allows the issuer to retire the security prior to

maturity.

clean price

The quoted price of a bond, which understates the true price of a bond

by any accrued interest.

conversion

premium

The difference between a convertible security’s market price and its

conversion value.

conversion

privilege

The provision in a convertible issue that stipulates the conditions of the

conversion feature, such as the conversion period and conversion ratio.

conversion ratio

A ratio specifying the number of shares of common stock into which a

convertible bond can be converted.

conversion value

A measure of what a convertible issue would trade for if it were priced

to sell based on its stock value.

corporate bond

A bond issued by a corporation.

coupon

Bond feature that defines the annual interest income the issuer will pay

the bondholder.

current yield

.

The amount of current income a bond provides relative to its market

price.

cyclical stock

Stock whose price movements tend to parallel the various stages of the

business cycle.

debenture

An unsecured bond issued on the general credit of the firm.

defensive stock

Stock whose price movements are usually contrary to movements in

the business cycle.

discount bond

A bond whose market value is lower than par.

dirty (full) price

The quoted price of a bond plus accrued interest, the total of which is

the relevant price to be paid by a bond buyer.

dividend

reinvestment

plan (DRP)

A program whereby stockholders can choose to take their cash

dividends in the form of more shares of the company’s stock.

dividend yield

The percentage return provided by the dividends paid on common

stock.

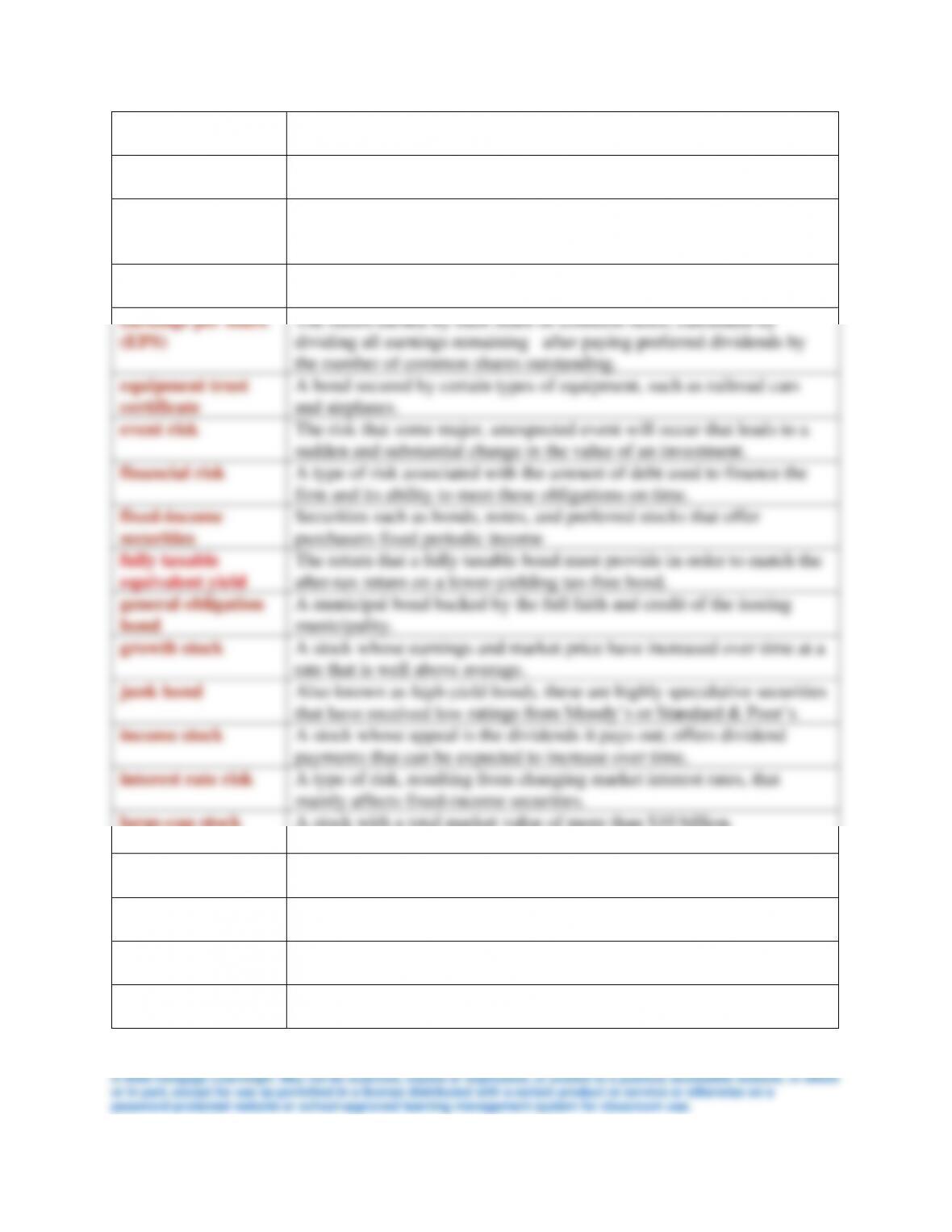

earnings per share

(EPS)

The return earned by each share of common stock; calculated by

dividing all earnings remaining after paying preferred dividends by

the number of common shares outstanding.

equipment trust

certificate

A bond secured by certain types of equipment, such as railroad cars

and airplanes.

event risk

The risk that some major, unexpected event will occur that leads to a

sudden and substantial change in the value of an investment.

financial risk

A type of risk associated with the amount of debt used to finance the

firm and its ability to meet these obligations on time.

fixed-income

securities

Securities such as bonds, notes, and preferred stocks that offer

purchasers fixed periodic income

fully taxable

equivalent yield

The return that a fully taxable bond must provide in order to match the

after-tax return on a lower-yielding tax-free bond.

general obligation

bond

A municipal bond backed by the full faith and credit of the issuing

municipality.

growth stock

A stock whose earnings and market price have increased over time at a

rate that is well above average.

junk bond

Also known as high-yield bonds, these are highly speculative securities

that have received low ratings from Moody’s or Standard & Poor’s.

income stock

A stock whose appeal is the dividends it pays out; offers dividend

payments that can be expected to increase over time.

interest rate risk

A type of risk, resulting from changing market interest rates, that

mainly affects fixed-income securities.

large-cap stock

A stock with a total market value of more than $10 billion.

liquidity risk

A type of risk associated with the inability to liquidate an investment

conveniently and at a reasonable price.

market risk

A type of risk associated with the price volatility of a security.

mid-cap stock

A stock whose total market value falls somewhere between $2 billion

and $10 billion.

mortgage-backed

securities

Securities that are a claim on the cash flows generated by mortgage

loans; bonds backed by mortgages as collateral.

municipal bond

A bond issued by state or local governments; interest income is usually

exempt from federal taxes.

mortgage bond

A bond secured by a claim on real assets, such as a manufacturing

plant.

net profit margin

A key measure of profitability that relates a firm’s net profits to its

sales; shows the rate of return the company is earning on its sales.

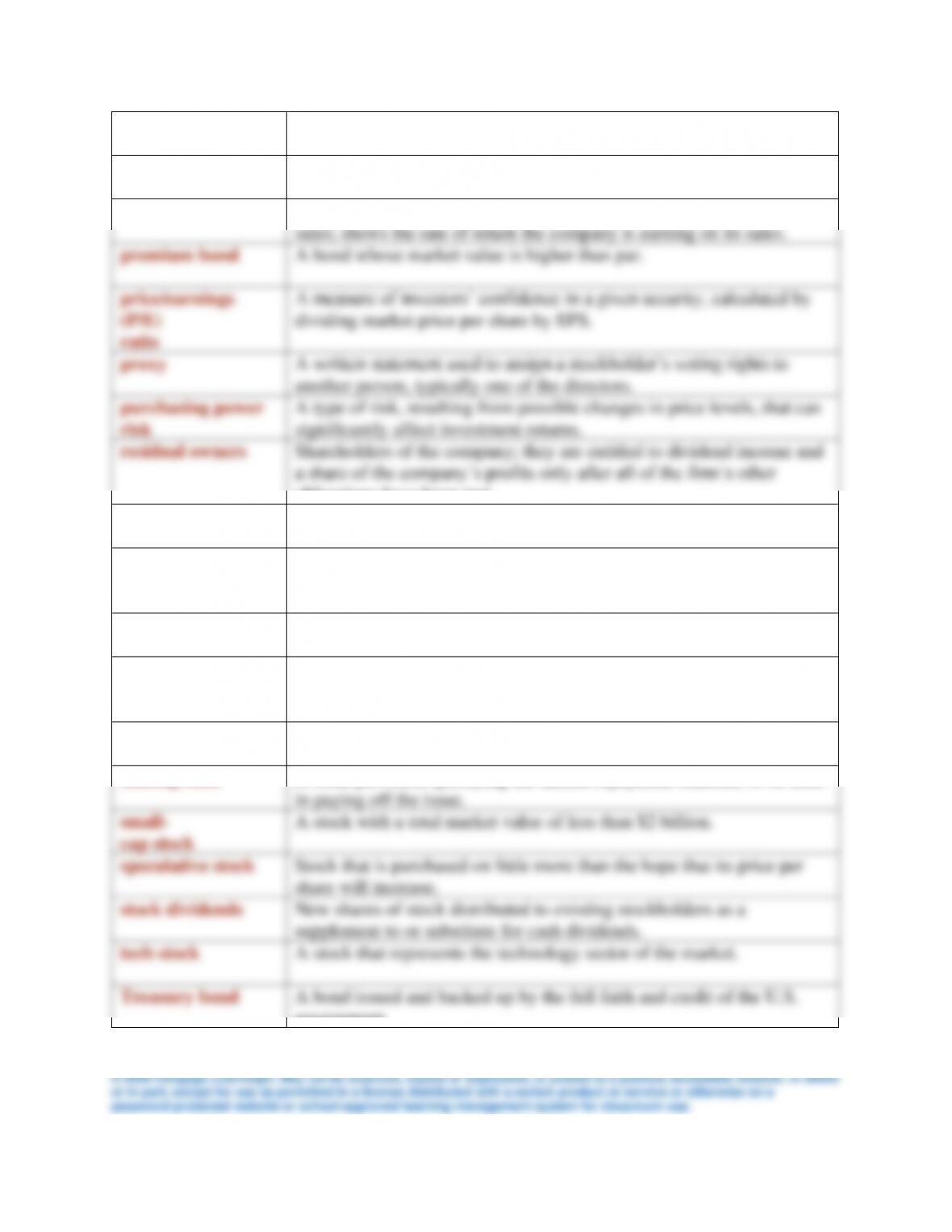

premium bond

A bond whose market value is higher than par.

price/earnings

(P/E)

ratio

A measure of investors’ confidence in a given security; calculated by

dividing market price per share by EPS.

proxy

A written statement used to assign a stockholder’s voting rights to

another person, typically one of the directors.

purchasing power

risk

A type of risk, resulting from possible changes in price levels, that can

significantly affect investment returns.

residual owners

Shareholders of the company; they are entitled to dividend income and

a share of the company’s profits only after all of the firm’s other

obligations have been met.

return on equity

(ROE)

A measure that captures the firm’s overall profitability; it is important

because of its impact on the firm’s growth, profits, and dividends.

required rate

of return

The minimum rate of return an investor feels should be earned in

compensation for the amount

revenue bond

.

A municipal bond serviced from the income generated by a specific

project

risk-free rate

of return

The rate of return on short-term government securities, such as

Treasury bills, that is free from any type of risk.

serial obligation

An issue that is broken down into a series of smaller bonds, each with

its own maturity date and coupon rate.

sinking fund

A bond provision specifying the annual repayment schedule to be used

in paying off the issue.

small-

cap stock

A stock with a total market value of less than $2 billion.

speculative stock

Stock that is purchased on little more than the hope that its price per

share will increase.

stock dividends

New shares of stock distributed to existing stockholders as a

supplement to or substitute for cash dividends.

tech stock

A stock that represents the technology sector of the market.

Treasury bond

A bond issued and backed up by the full faith and credit of the U.S.

government.

Treasury inflation-

indexed bond

A bond, issued by the U.S. government, whose principal payments are

adjusted to provide protection again inflation as measured by the

Consumer Price Index (CPI).

yield to maturity

The fully compounded rate of return that a bond would yield if it were

held to maturity.

zero coupon bond

A bond that pays no annual interest but sells at a deep discount to its

par value.

Investing in Stocks and Bonds

Chapter Outline

Learning Objectives

I. The Risks and Rewards of Investing

A. The Risks of Investing

1. Business Risk

2. Financial Risk

3. Market Risk

4. Purchasing Power Risk

5. Interest Rate Risk

6. Liquidity Risk

7. Event Risk

B. The Returns from Investing

1. Current Income

2. Capital Gains

3. Earning Interest on Interest: Another Source of Return

C. The Risk-Return Trade-off

D. What Makes a Good Investment?

1. Future Return

2. Approximate Yield

II. Investing in Common Stock

A. Common Stocks as a Form of Investing

1. Issuers of Common Stock

2. Voting Rights

3. Basic Tax Considerations

B. Dividends

C. Some Key Measures of Performance

1. Book Value

2. Net Profit Margin

3. Return on Equity

4. Earnings per Share

5. Price/Earnings Ratio

6. Beta

D. Types of Common Stock

1. Blue-Chip Stocks

2. Growth Stocks

3. Tech Stocks

4. Income Stocks versus Speculative Stocks

5. Cyclical Stocks or Defensive Stocks

6. Large-Caps, Mid-Caps, and Small-Caps

E. Market Globalization and Foreign Stocks

F. Investing in Common Stock

1. Advantages and Disadvantages of Stock Ownership

G. Making the Investment Decision

1. Putting a Value on Stock

2. Timing Your Investments

3. Be Sure to Plow Back Your Earnings

III. Investing in Bonds

A. Why Invest in Bonds?

B. Bonds versus Stocks

C, Basic Issue Characteristics

1. Types of Issues

2. Sinking Fund

3. Call Feature

D. The Bond Market

1. Treasury Bonds

2. Agency and Mortgage-Backed Bonds

3. Municipal Bonds

4. Corporate Bonds

5. The Special Appeal of Zero Coupon Bonds

6. Convertible Bonds

E. Bond Ratings Exhibit 12.6

F. Pricing a Bond

1. Bond Prices and Accrued Interest

2. Bond Prices and Yields

3. Current Yield and Yield to Maturity

Financial Impact of Personal Choices: Lucy and Ted Richardson

Personal Choices