1 Chapter 24

CHAPTER 24: Property Insurance

I. Dene Property Damage

A. Modem Fire Coverage Explain that lots and slabs are usually not insured.

B. Endorsements

II. Explain the concerns of a property owner for

Public Liability

III. Discuss Homeowner Policies, and dene Give examples of current area problems such

A. Policy Formats as mold.

B. Properties Covered

C. Perils Covered

D. Tenant’s Policy

E. Condominium Policy

F. Liability Coverage

G. Medical Payments

H. Endorsements

IV. Explain the term “New for Old”

V. Explain how Lender Requirements affect the Discuss the lender’s need for property insurance to

guaran-

need for insurance tee his security. Note that coverage may be only for the

VI. Discuss the advisability of Guaranteed mortgage amount.

Replacement Cost

VII. Explain the need for Flood Insurance under Explain where the Flood Prone Area map may be

obtained

federal law in your community.

VIII. Explain Landlord Policies

IX. Explain Policy Cancellation and policy

suspension

X. Discuss Policy Takeovers

This chapter is available only in Real Estate Principles hard copy text.

If you own real estate, you take the risk that your property may be damaged

due to re or other catastrophe. Additionally, there is the possibility that

someone may be injured while on your property and hold you responsible.

Insurance to cover losses from either of

these occurrences is available.

Chapter 24 2

Page Ref.

Soft Hard

back back Topic Teaching Tips

– 413 Opening Remarks Start this chapter with a general overview of the importance of

having adequate homeowner’s insurance and the requirements

imposed by lenders.

– 413 Modem Fire Coverage Summary: Insured (person buying insurance), insurance premium

(payment), insurer (insurance company).

– 414 Homeowner Policies Local Distinction: Obtain a specimen HO policy (either a blank

one or perhaps your own and “white out” all pertinent informa

tion) as reference material.

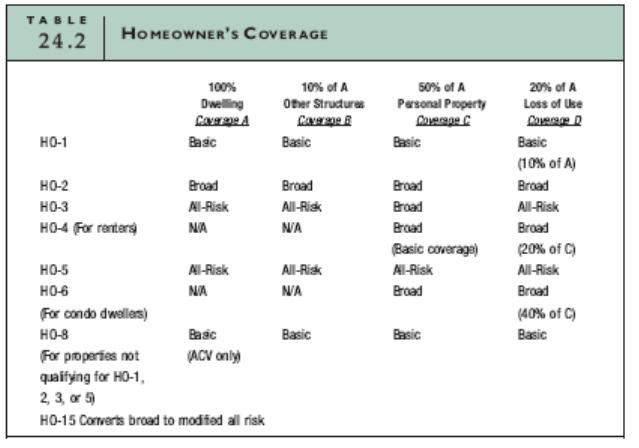

– 414 Policy Formats Summary:

Section I = Property Section II = Liability

Local Distinction: Address the coverage of your specimen policy.

– 415 Perils Covered Expanding the Text: HO-l and HO-2 policies are named peril

policies, i.e., only the perils named in the policy are insured. This

is the opposite of an all-risks policy, such as the HO-5, where all

perils except those listed in the policy are insured.

– 416 Tenant’s Policy Expanding the Text: Point out to students that replacing the

entire contents of an apartment can be expensive.

Should an uninsured tenant cause a fire which destroys several

apartments, tenants of the lost apartments cannot look to the

owner’s insurance on the building for coverage of the tenant’s

personal belongings. Owner’s insurance only covers the building.

Tenants should always carry tenant’s insurance to guard against

losses caused by others.

– 417 New for Old Summary: “Old for old” is actual cash value (new price minus

accumulated depreciation).

“New for old” is replacement cost.

– 419 Flood Insurance Expanding the text: “Rising water” is perceived to be flooding,

and not covered by typical homeowner policies (refer to the

exclusions under Perils Covered, discussed earlier in this chapter).

For instance, after a hurricane, insurance adjusters seek to

determine if the water damage is a result of rain coming into the

house after the roof was blown off, in which case, homeowner’s

insurance covers the damage.

If the damage is a result of flooding (rising water), then the home

owners are protected only if they carry additional flood insurance.

The same principle applies to water damage after an earthquake.

3 Chapter 24

Page Ref.

Soft Hard

back back

– 419

Topic

Policy Cancellation

420 Policy Takeovers

421 Wrap-Up

Teaching Tips

Local Distinction: Some states have enacted legislation which

prohibits short rate cancellation penalties. In other words, the

unused premium on a canceled policy must be refunded pro rata.

Find out in reference to your state.

Stress: The insurance company must accept the insured prior to

his being able to take over the seller’s policy because an insurable

interest must exist.

1. The policy holder is the insured and the insurance company is

the insurer? (True)

2. The terms endorsement, rider, and attachment are

synonymous? (True)

3. Section I of a standard HO policy addresses the property and

Section II addresses the owner’s liability? (True)

4. HO-1 is a basic form policy, and HO-2 is a broad form policy

and both are named peril policies? (True)

5. HO-5 is an all-risk policy? (True)

6. HO-3 provides all-risk coverage on the dwelling and named

peril coverage on content? (True)

7. HO-4 provides coverage for tenants only? (True)

8. Actual cash value is, in effect, “old for old”? (True)

9. Flood insurance is underwritten by the federal government?

(True)

10. When the purchaser of a property takes over (assumes) a seller’s

HO policy, the insurer must determine that he/she has an

insurable interest in the property? (True)

Chapter 24 4