61

© Pearson Education Limited 2008

Funds Analysis, Cash-Flow Analysis, and

Financial Planning

Forecasting is very difficult, especially if it is about the

future.

ANONYMOUS

Chapter 7: Funds Analysis, Cash-Flow Analysis, and Financial Planning

62

© Pearson Education Limited 2008

ANSWERS TO QUESTIONS

1. Flow of funds (sources and uses) statements provide the analyst with information generally

being about year-to-year changes in assets and how these changes are financed. It is

2. A

statement of cash flows reports a firm’s cash inflows and outflows during a period of time

segregated into three categories: operating, investing, and financing activities. When used

3. The variable that most directly affects the cash budget is sales since the cash inflow is

4. Cash budgeting can lower the cost of borrowing for two reasons. By knowing ahead of time

7. The purpose of accounting statements is to provide information to creditors and investors so

that they may make a correct assessment of the risk and return characteristics of the firm.

The statement of cash flows may provide insights not apparent in studying either the income

8. Some managers prefer the flow of funds statement over the more complex cash-flow

9. Whether or not depreciation is a source of funds has been debated for many years by

accountants and financial analysts. Accountants argue that depreciation is an accounting

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

63

© Pearson Education Limited 2008

11. a. Source/Investing

b. Use/Financing

12. The cash budget deals with inflows and outflows of cash and not necessarily accounting

13. The financial manager should concentrate on accurate projections of sales as well as the

14. Probably the cash budget is a better measure of liquidity. The current ratio and quick ratio

15. Virtually everything in the cash budget depends on sales: receivables, production costs,

16. Forecast statements are projections of expected future income statements and balance

While both the cash budget and the forecast income statement are forecasts of the future, the

17. The two principal ways by which to prepare forecast statements are through a cash budget

Answers to Appendix Questions:

18. A sustainable growth rate (SGR) is the maximum percentage growth in sales that can occur

consistent with target operating, debt, and dividend ratios. With sustainable growth

Chapter 7: Funds Analysis, Cash-Flow Analysis, and Financial Planning

64

© Pearson Education Limited 2008

19. Steady-state modeling assumes that balance sheet and performance ratios do not change

20. The input variables are beginning sales and beginning equity. Target variables are the ratio

SOLUTIONS TO PROBLEMS

1. Source: – $ 100 Cash

Use: + $ 700 Accounts receivable

2. a.

Svoboda Corporation

Sources and uses of funds statement

for December 31, 20X1 to December 31, 20X2 (in millions)

Sources Uses

Funds provided by operations:

Net profit $ 7 Dividends $ 3

Depreciation 5 Additions to fixed assets 10

Decrease, other assets 3 Increase,

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

65

© Pearson Education Limited 2008

b.

Svoboda Corporation Statement of cash flows

for the year ended December 31, 20X2 (in millions)

CASH FLOW FROM OPERATING ACTIVITIES:

Net income ……………………………………………………………………………… $ 7

Depreciation …………………………………………………………………………… 5

Cash provided (used) by current assets and

CASH FLOW FROM INVESTING ACTIVITIES:

Additions to fixed assets ……………………………………………………………. $ (10)

CASH FLOW FROM FINANCING ACTIVITIES:

Decrease in short-term bank borrowings ……………………………………… $ (20)

*Note: Taxes paid = Taxes (from income statement) minus increase in accrued taxes (from

comparative balance sheets) — $2 = $4 – $2.

Chapter 7: Funds Analysis, Cash-Flow Analysis, and Financial Planning

66

© Pearson Education Limited 2008

3. a.

Begalla Corporation

Sources and uses of funds statement

for December 31, 20X1 to December 31, 20X2 (in millions)

Sources Uses

Funds provided by operations:

Net profit $15 Dividends $10

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

67

© Pearson Education Limited 2008

b.

Begalla Corporation

Statement of cash flows

for the year ended December 31, 20X2 (in millions)

CASH FLOW FROM OPERATING ACTIVITIES:

Net income ………………………………………………………………………………………… $ 15

Depreciation ………………………………………………………………………………………. 3

CASH FLOW FROM INVESTING ACTIVITIES:

Additions to fixed assets ……………………………………………………………………… $ (3)

CASH FLOW FROM FINANCING ACTIVITIES:

_______________________________________________________________

*Note: Taxes paid = Taxes (from income statement) plus decrease in accrued taxes (from

comparative balance sheets) — $11 = $10 + $1.

Chapter 7: Funds Analysis, Cash-Flow Analysis, and Financial Planning

68

© Pearson Education Limited 2008

4.

Schedules of projected sales and collections

for May to July (in thousands)

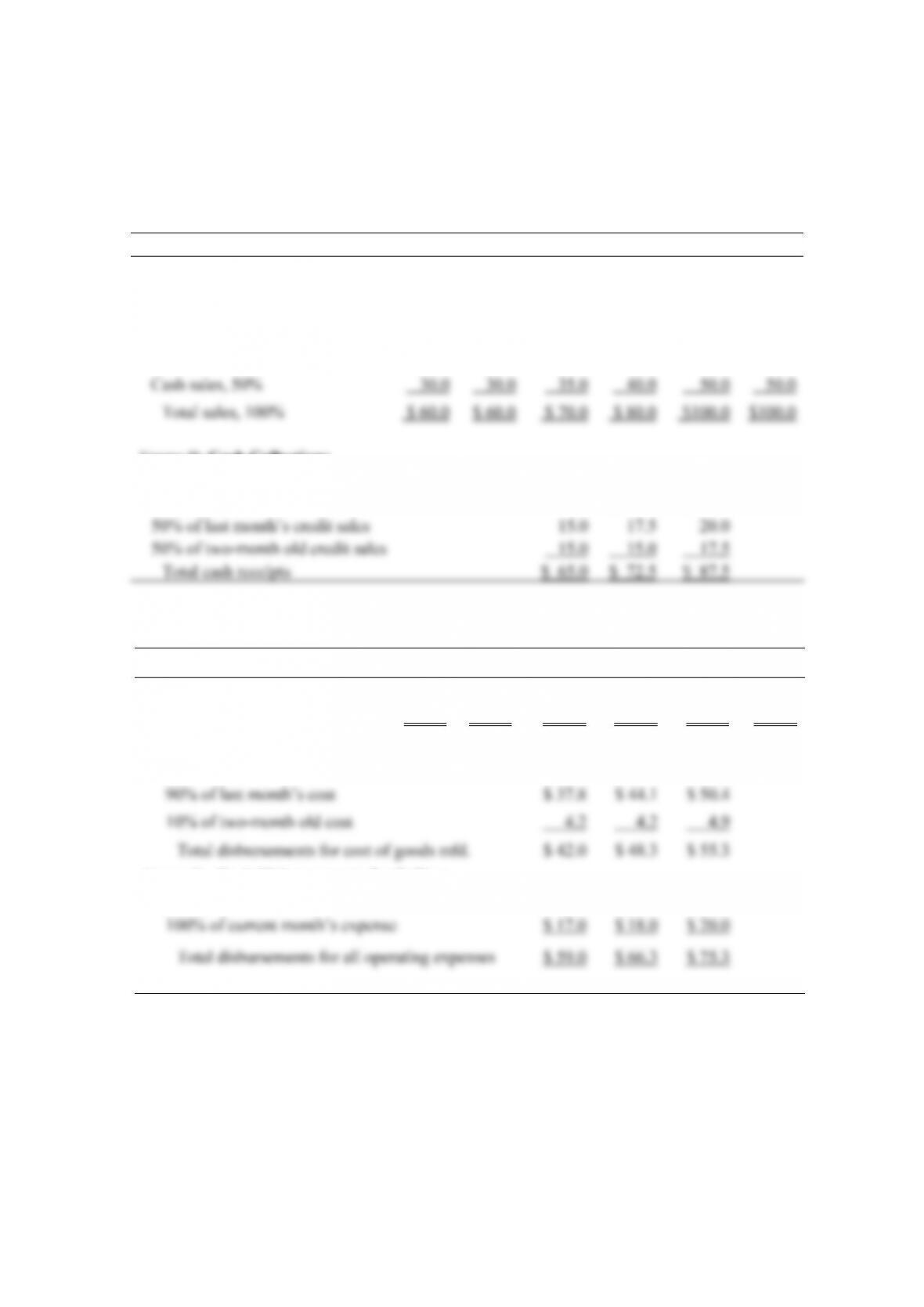

Mar. Apr. May June July Aug.

Frame A: Sales

Credit sales, 50% $ 30.0 $ 30.0 $ 35.0 $ 40.0 $ 50.0 $ 50.0

Frame B: Cash Collections

Cash sales, this month $ 35.0 $ 40.0 $ 50.0

Schedule of projected disbursements for operating expenses for May to July (in thousands)

Mar. Apr. May June July Aug.

Frame A: Cost of

Goods Mfd. $ 42.0 $ 42.0 $ 49.0 $ 56.0 $ 70.0 $ 70.0

Frame B: Cash Disbursements for

Cost of Goods Mfd.

Frame C: Cash Disbursements for Selling,

General, and Administrative Expenses

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

69

© Pearson Education Limited 2008

Schedule of projected total cash disbursements for May to July (in thousands)

May June July

Total disbursements for all operating expenses $ 59.0 $ 66.3 $ 75.3

Interest payment 9.0

________________________________________________________________

Schedule of projected net cash flows and cash balances for May to July (in thousands)

May June July

Beginning cash balance, without additional financing $ 20.0 $ 26.0 $ (7.8)

Total cash receipts 65.0 72.5 87.5

Chapter 7: Funds Analysis, Cash-Flow Analysis, and Financial Planning

70

© Pearson Education Limited 2008

5.

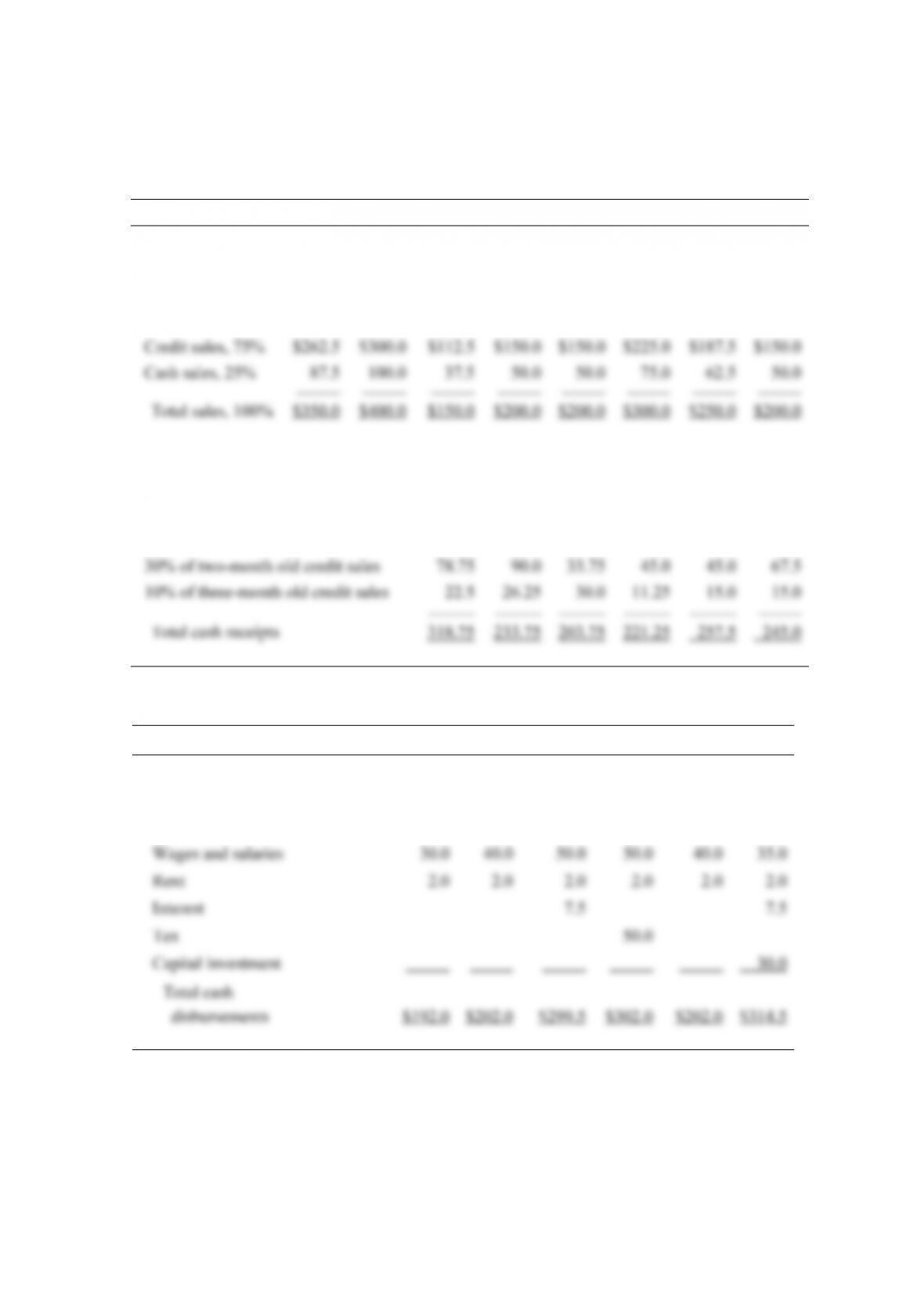

Schedules of projected sales and collections for January to June (in thousands)

Nov. Dec. Jan. Feb. Mar. Apr. May June

Frame A: Sales

Frame B: Cash Collections

Cash sales, this month $ 37.5 $ 50.0 $ 50.0 $ 75.0 $ 62.5 $ 50.0

60% of last month’s credit sales 180.0 67.5 90.0 90.0 135.0 112.5

Schedule of projected total cash disbursements for January to June (in thousands)

Jan. Feb. Mar. Apr. May June

Cash payments for:

Purchases $160.0 $160.0 $240.0 $200.0 $160.0 $240.0

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

71

© Pearson Education Limited 2008

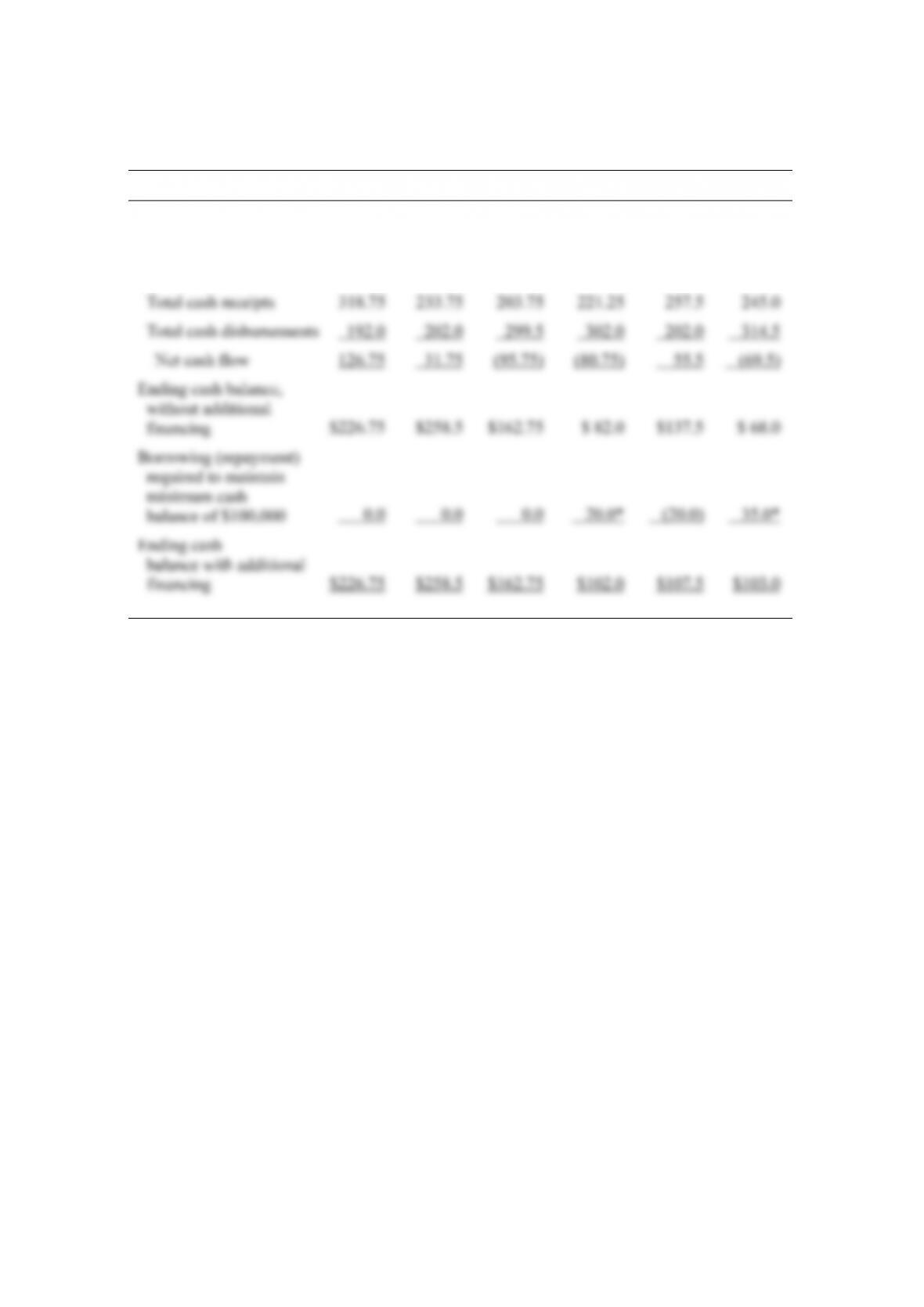

Schedule of projected net cash flows and cash balances for January to June (in thousands)

Jan. Feb. Mar. Apr. May June

Beginning cash

balance, without

additional financing

$100.0

$226.75

$258.5

$162.75

$ 82.0

$137.5

*Funds can be borrowed in $5,000 multiples.