41

© Pearson Education Limited 2008

Risk and Return

Take calculated risks. That is quite different from being

rash.

GENERAL GEORGE S. PATTON

Chapter 5: Risk and Return

42

© Pearson Education Limited 2008

ANSWERS TO QUESTIONS

1. Virtually none of the concepts presented would hold. Risk would not be a dimension of

concern to the risk-neutral investor. The only concern would be with expected return, and

2. The

characteristic line depicts the expected relationship between excess returns (in excess

3. Beta measures the responsiveness of changes in excess returns for the security involved to

changes in excess returns for the market portfolio. It tells us how attuned fluctuations in

4. Req. (Rj) = Rf + [E(Rm) – Rf] Betaj

Req. (Rj) = required rate of return for security j;

5. No. The security market line (SML) can vary with changes in interest rates, investor

6. a. Lower the market price.

7. If you limit yourself to only common stock, you would seek out defensive stocks — where

8. The undervalued stock would lie above the security market line, thereby providing investors

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

43

© Pearson Education Limited 2008

SOLUTIONS TO PROBLEMS

1. a.

Possible Return, Ri Probability of

Occurrence, Pi (Ri)(Pi) (Ri – R)2(Pi)

–.10 .10 –.10 (–0.10 – 0.11)2 (.10)

b. There is a 30 percent probability that the actual return will be zero (prob. E(R) = 0 is

2. a. For a return that will be zero or less, standardizing the deviation from the expected

value of return we obtain (0% – 20%)/15% = –1.333 standard deviations. Turning to

b. 10 percent:: Standardized deviation = (10% – 20%)/15% = –0.667. Probability of

20 percent:

50 percent probability of return being above 20 percent.

Chapter 5: Risk and Return

44

© Pearson Education Limited 2008

3. As the graph will be drawn by hand with the characteristic line fitted by eye, All of them

4. Req. (RA) = 0.07 + (0.13 – 0.07) (1.5) = 0.16

Req. (RB) = 0.07 + (0.13 – 0.07) (1.0) = 0.13

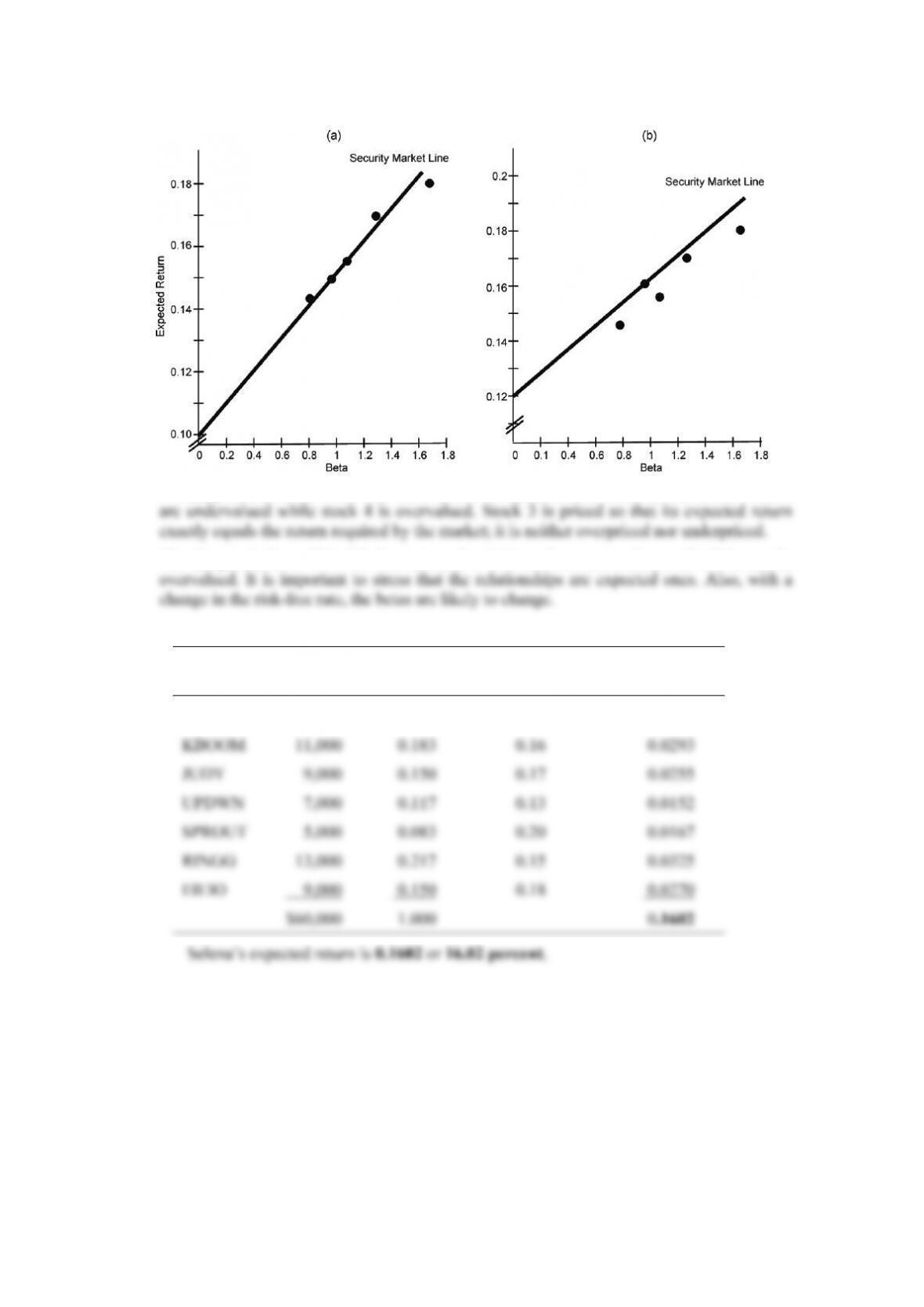

6. Perhaps the best way to visualize the problem is to plot expected returns against beta. This

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

45

© Pearson Education Limited 2008

The (a) panel, for a 10% risk-free rate and a 15% market return, indicates that stocks 1 and 2

The (b) panel, for a 12% risk-free rate and a 16% market return, shows all of the stocks

7. a.

Ticker

Symbol

Amount

Invested

Proportion,

Pi

Expected

Return, Ri

Weighted Return,

(Pi)(Ri)

WOOPS $ 6,000 0.100 0.14 0.0140

Chapter 5: Risk and Return

46

© Pearson Education Limited 2008

b.

Ticker

Symbol

Amount

Invested

Proportion,

Pi

Expected

Return, Ri

Weighted

Return, (Pi)(Ri)

WOOPS $6,000 0.08 0.14 0.0112

KBOOM 11,000 0.147 0.16 0.0235

8. Required return = 0.10 + (0.15 – .10)(1.08)

Assuming that the perpetual dividend growth model is appropriate, we get

9. a. The beta of a portfolio is simply a weighted average of the betas of the individual

securities that make up the portfolio.

Ticker Symbol Beta Proportion Weighted Beta

NBS 1.40 0.2 0.280

Assuming that the constant dividend growth model is appropriate, we get

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

47

© Pearson Education Limited 2008

b. Since the common stock is currently selling for $30 per share in the marketplace, while

Solution to Appendix A Problem:

The standard deviation for the portfolio is found by summing up all the elements in the

following variance-covariance matrix and then taking the sum’s square root.

D E F

Therefore, the standard deviation of the portfolio equals:

SOLUTIONS TO SELF-CORRECTION PROBLEMS

1. a.

Possible

Return, Ri

Probability of

Occurrence, Pi (Ri)(Pi) 2

ii

(R R) (P )−

–0.10 0.10 –0.010 (–0.10 –0.20)2 (0.10)

b. For a return that will be zero or less, standardizing the deviation from the expected

value of return we obtain (0% – 20%)/16.43% = –1.217 standard deviations. Turning to

Chapter 5: Risk and Return

48

© Pearson Education Limited 2008

For a return that will be 10 percent or less, standardizing the deviation we obtain

For a return of 40% or more, standardizing the deviation we obtain (40% –0 20%)/

2. a. R= 8% + (13% – 8%)1.45 = 15.25%

b. If we use the perpetual dividend growth model, we would have

1

0

e

D$2 (1.10)

−−

SOLUTION TO APPENDIX A SELF-CORRECTION PROBLEM

In the above expression, the middle term denotes the covariance (–0.35)(0.05)(0.04) times

the weights of .6 and .4, all of which is counted twice — hence the two in front. For the first

and last terms, the correlation coefficients for these weighted-variance terms are 1.0. This

expression reduces to