213

© Pearson Education Limited 2008

Term Loans and Leases

Rough winds do shake the darling buds of May. And

summer’s lease hath all too short a date…

WILLIAM SHAKESPEARE, SONNET XVIII

Chapter 21: Term Loans and Leases

214

© Pearson Education Limited 2008

ANSWERS TO QUESTIONS

1. The demand for intermediate-term loans arises from the needs of many firms to finance

assets with relatively short and uncertain life expectancies.

a. These assets are financed with intermediate debt rather than long-term funds because

the firm is uncertain that the assets represent a permanent funds requirement, because it

b. The use of short-term debt is also undesirable if the firm is unable to generate cash

2. Because of the long-term nature and stability of their liabilities, insurance companies prefer

to invest in assets of like maturity. This reduces the problem of reinvestment of income cash

3. Protective covenants are designed to safeguard the borrower’s ability to repay the loan with

4. A

revolving credit agreement is a legal agreement whereby the lender must loan the

company money upon proper notice. An upper limit is set and the number of years for

5. The lender wishes to preserve the liquidity of a borrower but at the same time does not want

to be so restrictive as to seriously affect the borrower’s profitability. The two restrictions

6. The borrower will wish to negotiate hard on those covenants that may be binding and not so

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

215

© Pearson Education Limited 2008

7. Commercial banks are perhaps the most important source of intermediate-term financing.

8. A

chattel mortgage is a lien against a borrower’s equipment. With a conditional sales

9. If the investment decision and the financing decision cannot be separated, decisions may be

made that are not optimal. By coupling the decision to use leasing with a highly profitable

10. A financial lease is longer term than an operating lease. The financial lease is also

noncancellable with lease payments being required until the lease’s expiration. The

11. In a sale-and-leaseback, the asset is sold and leased back by the company. The company

12. The capitalized value of a financial lease is shown on the balance sheet as an asset and the

associated liability is shown on the right-hand side of the balance sheet. The amortization of

13. a. Higher liquidity ratios.

Chapter 21: Term Loans and Leases

216

© Pearson Education Limited 2008

14. This argument is illogical. On financial leases, for example, the lessor will receive the

15. a. The tax rate increase would be neutral in the sense that each tax deductible dollar under

b. Faster accelerated depreciation should favor borrowing as a larger tax shield would

c. This would tend to favor borrowing, especially if the market value of the asset financed

e. If the interest rate rise affected both lessor and lender equally, the effect would tend to

SOLUTIONS TO PROBLEMS

Schedule of debt payments

(a) (b) (c)

End of

Year

Loan

Payment

Principal Amount

Owing At End of

Year (b)t–1 – (a) + (c)

Annual Interest

(b)t–1 × (0.14)

0 $ 0 $600,000 $ 0

* Difference due to rounding and the fact that the discount factor is only four places to the right

of the decimal point.

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

217

© Pearson Education Limited 2008

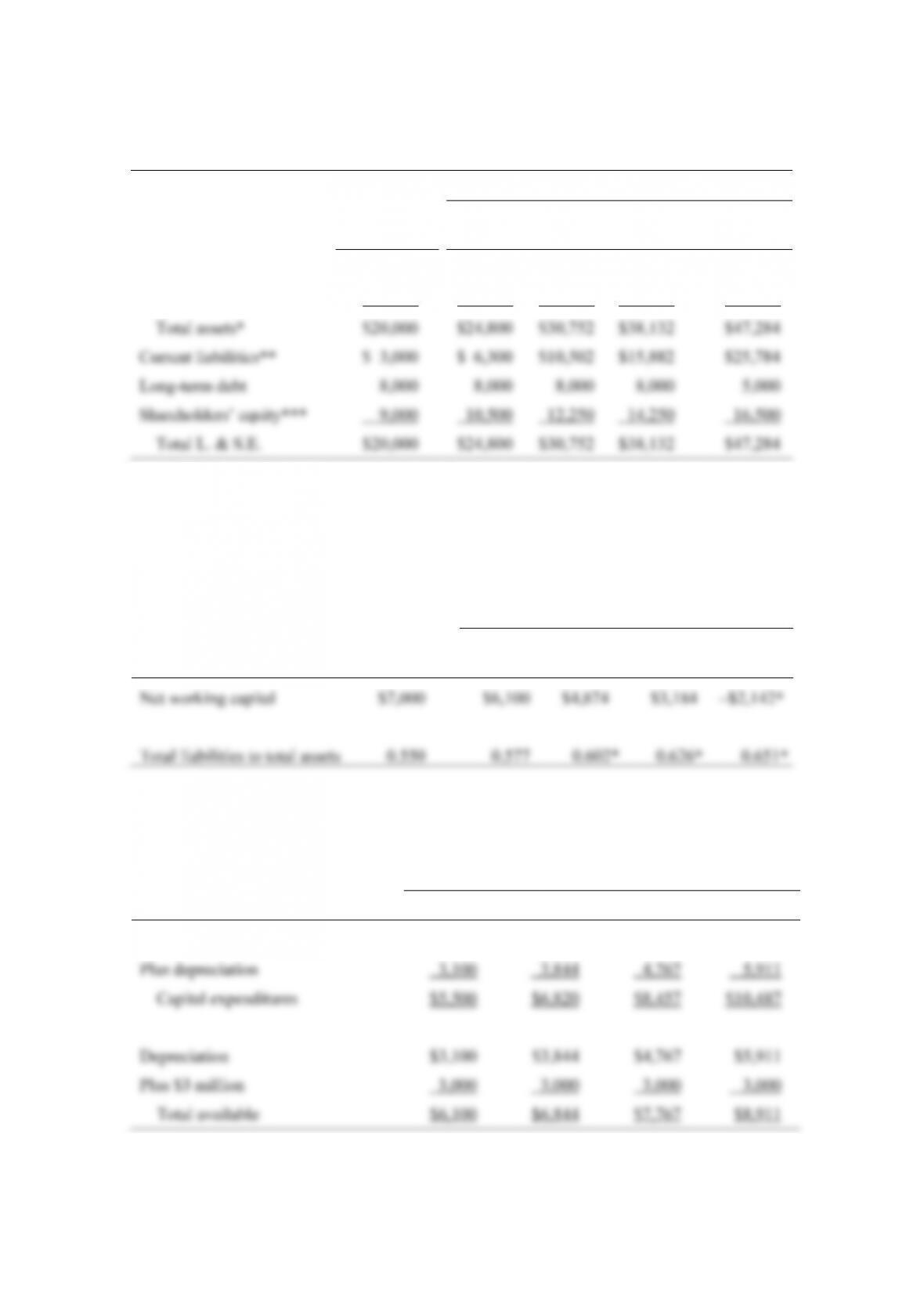

2. Balance Sheet Under Growth Assumptions (000s omitted)

Years in Future (at December 31)

Now

(after financing) 1 2 3 4

Current assets* $10,000 $12,400 $15,376 $19,066 $23,642

Fixed assets* 10,000 12,400 15,376 19,066 23,642

* Will show a 24 percent growth rate starting in year 1.

** The current liabilities row is a residual and is found by subtracting long-term debt and

shareholders equity from total assets. In the 4th year, the term loan becomes a current

liability.

*** Increased by the amount of expected profits.

Years in Future (at December 31)

Protective Covenant

Now (after

financing) 1 2 3 4

* In violation of covenant.

Long-term debt does not increase. All growth is financed with short-term liabilities and retained

earnings.

Years in Future (at December 31)

1 2 3 4

Net addition to fixed assets $2,400 $2,976 $3,690 $ 4,576

Chapter 21: Term Loans and Leases

218

© Pearson Education Limited 2008

The company will breach the total-liabilities-to-total-assets ratio restriction in the second,

third, and fourth year, the capital expenditures restriction in the third and fourth year, and

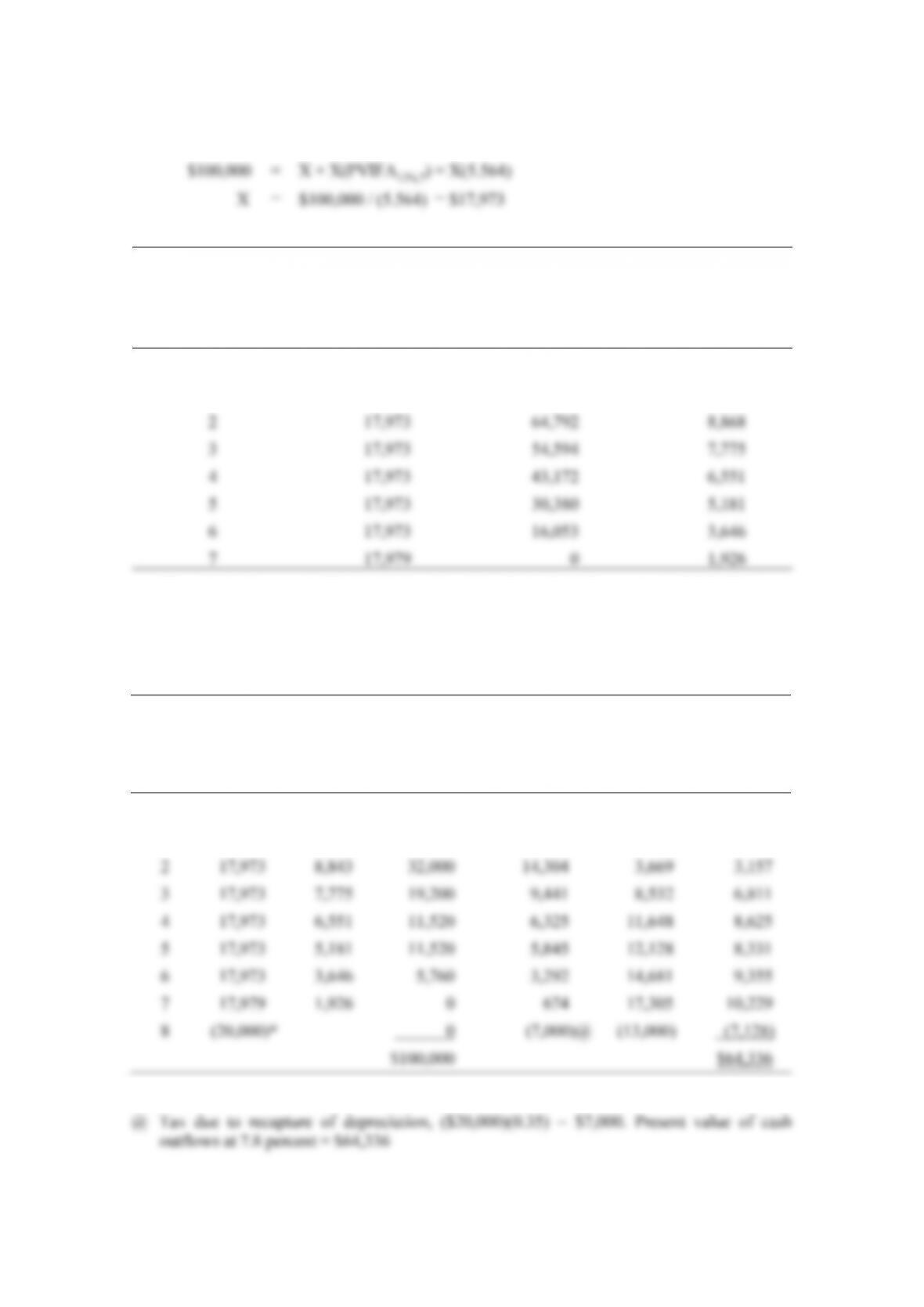

4. a. $18,600 = X + (PVIFA12%,7)X = X + (4.564)X

5. Schedule of cash flows for the leasing alternative

(a) (b) (c) (d)

End of Year

Lease

Payment

Tax-Shield

Benefits

(a)t–1 × (0.35)

Cash Outflow

After Taxes

(a) – (b)

Present Value

of Cash

Outflows

(at 7.8%)

0 $16,000 $ 0 $16,000 $16,000

* Total for years 1–7.

The discount rate of 7.8 percent is the product of the cost of borrowing of 12 percent times

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

219

© Pearson Education Limited 2008

Annual debt payments are found using a generalized version of Eq. (21.2):

Schedule of debt payments

(a) (b) (c)

End of Year

Loan

Payment

Principal Amount

Owing At End of

Year (b)t–1 – (a) + (c)

Annual Interest

(b)t–1 × (0.12)

0 $17,973 $82,027 $ 0

1 17,973 73,897 9,843

The principal amount of $100,000 is reduced by the initial debt payment of $17,973 to get

the principal amount owing at time 0 of $82,027. Interest on this amount in year 1 is found

by multiplying it by 12 percent. The debt payment in the last year is slightly larger due to

previous rounding.

Schedule of cash flows for the debt alternative

(a) (b) (c) (d) (e) (f)

End of

Year

Debt

Payment

Annual

Interest

Annual

Depreciation

Tax-Shield

Benefits

(b+c)0.35

After-Tax

Cash Flow

(a)–(d)

PV of

Cash Flows

(at 7.8%)

0 $17,973 $ 0 $ 0 $ 0 $17,973 $17,973

1 17,973 9,843 20,000 10,445 7,528 6,983

* Salvage value.

Chapter 21: Term Loans and Leases

220

© Pearson Education Limited 2008

Because the present value of debt payments, $64,336, is less than the present value of lease

payments, $67,448, the debt alternative is preferred. However, some would argue that we

6. Schedule of cash flows for the leasing alternative

(a) (b) (c) (d)

End of

Year

Lease

Payment

Tax-Shield

Benefits

(a)t–1 × (0.30)

Cash Outflow

After Taxes

(a) – (b)

Present Value

of Cash

Outflows

(at 7%)

0 $17,000 — $17,000 $17,000

* Total for years 1–4.

The discount rate of 7 percent is the product of the cost of borrowing (10%) times one

minus the tax rate of 30 percent. The present value of cash outflows is $53,672.

Annual debt payments are found using a generalized version of Eq. (21.2):

Schedule of debt payments

(a) (b) (c)

End of Year Loan Payment

Principal Amount

Owing At End of

Year (b)t–1 – (a) + (c)

Annual Interest

(b)t–1 × (0.10)

0 $19,185 $60,815 $ 0

1 In order for the present value of cash outflows for the leasing alternative ($67,448) to be less

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

221

© Pearson Education Limited 2008

Schedule of cash flows for the debt alternative

(a) (b) (c) (d) (e) (f)

End of

Year

Debt

payment

Annual

Interest

Annual

Depreciation

Tax-Shield

Benefits

(b + c) .30

After-Tax

Cash Flow

(a)–(d)

PV of

Cash

Flows

(at 7%)

0 $19,185 $ 0 $ 0 $ 0 $19,185 $ 19,185

* Residual value.

Solution to Appendix Problem:

7. a. After the initial lease payment, there are five remaining payments. The lower cost

b. Principal amount during the first year for accounting purposes = $110,877

1 In order for the present value of cash outflows for the leasing alternative ($53,672) to be less

Chapter 21: Term Loans and Leases

222

© Pearson Education Limited 2008

SOLUTIONS TO SELF-CORRECTION PROBLEMS

1. a. b. (in thousands)

YEAR

Revolving Credit Term Loan

1 2 3 4 5 6

Amount borrowed during year $ 1,400 $ 3,000 $ 3,000 $ 3,000 $ 2,000 $ 1,000

2. A generalized version of Eq. (21.2) as the formula is used throughout.

a. $46,000 = X + X(PVIFA11%,5)

b. $210,000 = $47,030 / (1 + PVIFAX,5)

Subtracting 1 from this gives 5.759. Looking in Table IV in the 10% column, we find

that 5.759 corresponds to the 9-period row. Therefore, the lease period is 9 + 1, or 10

years.

3. Schedule of cash flows for the leasing alternative

(a) (b) (c) (d)

End of Year Lease Payment

Tax-Shield

Benefits

(a)t–1 × (0.40)

Cash Outflow

After Taxes

(a) – (b)

Present Value of

Cash Outflows

(at 8.4%)

0 $16,000 – – $16,000 $16,000

* Total for years 1–7.

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

223

© Pearson Education Limited 2008

The discount rate is the before-tax cost of borrowing times 1 minus the tax rate, or

(14 percent) (1 – 0.40) = 8.4%.

Annual debt payment:

Schedule of debt payments

(a) (b) (c)

End of

Year

Loan

Payment

Principal Amount Owing At

End of Year (b)t–1 – (a) + (c)

Annual Interest

(b)t–1 × (0.14)

0 $18,910 $81,090 $ 0

1 18,910 73,533 11,353

* The last payment is slightly lower due to rounding throughout.

Schedule of cash flows for the debt alternative

(a) (b) (c) (d) (e) (f)

End of

Year

Debt

Payment

Annual

Interest

Annual

Depreciation

Tax-Shield

Benefits

(b+c).40

After-Tax

Cash Flow

(a)–(d)

PV of Cash

Flows

(at 8.4%)

0 $18,910 $ 0 $ 0 $ 0 $18,910 $18,910

1 18,910 11,353 20,000 12,541 6,369 5,875

* Salvage value.

** Tax due to recapture of depreciation, ($24,000)(0.40) = $9,600.

Chapter 21: Term Loans and Leases

224

© Pearson Education Limited 2008

As the debt alternative has the lower present value of cash outflows, it is preferred.

However, some would argue that we should apply a discount rate higher than the lessee’s

1 In order for the present value of cash outflows for the leasing alternative ($61,948) to be less

than the present value of cash outflows for the debt alternative ([$60,309 + $7,553] –

[$14,400 / (1 + X)8]), the discount rate (X) must be roughly 11.8 percent or more.