174

© Pearson Education Limited 2008

Capital Structure Determination

When you have eliminated the impossible, whatever

remains, however improbable, must be the truth.

SHERLOCK HOLMES

IN THE SIGN OF THE FOUR

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

175

© Pearson Education Limited 2008

ANSWERS TO QUESTIONS

1. The net operating income (NOI) approach and the Modigliani-Miller (M&M) approach, in

the absence of taxes, are identical in form. The only difference is that M&M specify the

2. The optimal capital structure would differ from one industry to another because each

industry has a different level of business risk. The higher the level of business risk, the

3. Many factors influence the interest rate a firm must pay for debt funds. Some factors are

external to the firm. For example, the expected inflation rate, the Federal Reserve’s activity

4. The

total-value principle states that a corporation is valued on the basis of its earnings’

potential and its business risk. The total “pie” of value stays the same regardless of how it is

5. Arbitrage implies that an identical product cannot sell for different prices in different

markets. If it does, arbitragers will buy in one market and sell in another to earn an arbitrage

profit with no risk to them. These actions will cause the price of one asset to rise and the

6. Without financial-market imperfections, variation in capital structure would have no impact

on share price. Capital structure decisions would be irrelevant, as suggested by Modigliani-

Miller. Market imperfections take us away from a frictionless world and reduce the

7. Bankruptcy costs include out-of-pocket expenses to lawyers, accountants, appraisers,

Chapter 17: Capital Structure Determination

176

© Pearson Education Limited 2008

8. For reasons of prudence as well as legal reasons, institutional investors will not lend money

to a company that has excessive financial leverage. Both the investors, under state

9. Without the payment of taxes, the corporate tax-shield due to debt, disappears and so too

10. Debt financing would decrease on a relative basis, all other things being the same. The tax

11. The tax effect associated with debt and equity financing would be the same, as opposed to

12. If there is asymmetric information between management and investors, the former might

signal via capital structure. The implication is that management would not bind itself to the

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

177

© Pearson Education Limited 2008

SOLUTIONS TO PROBLEMS

1. a.

O Net operating income $10,000,000

I Interest on debt 1,400,000

b.

O Net operating income $10,000,000

k

o Overall capitalization rate ÷ 0.1126126

Chapter 17: Capital Structure Determination

178

© Pearson Education Limited 2008

2. a. (i) Sell your Gottahave stock for $22,500.

Your net dollar return, $3,600, is the same as it was for your investment in

b. When there is no further opportunity for employing fewer funds and achieving the same

3. a. $400,000 in debt. The market price per share of common stock is highest at this amount

of financial leverage.

b. (000s omitted)

# shares B EBIT I EBT EAT

100 $ 0 $250 $ 0.0 $250.0 $125.00

ki EPS P ke = EPS/P S = (# shares) × P V = B + S

— $1.25 $10.00 12.5% $1,000.0 $1000.0

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

179

© Pearson Education Limited 2008

ki(B/V) + ke(S/V) = ko

(12.5%)($1,000/$1,000.0) = 12.50%

(5.00%)($100/$1,000.0) + (13.3%)($900.0/$1,000.0) = 12.47

c. Yes. The optimal capital structure – the one possessing the lowest overall cost of capital

– involves $400,000 in debt.

4. a.

All-equity Debt and Equity

Chapter 17: Capital Structure Determination

180

© Pearson Education Limited 2008

5.

(in millions)

(1)

Debt

(2)

Value of Unlevered

Firm

(3)

PV of tax- shield

benefits

(1) × 0.22

(4)

PV of

Bankruptcy

Costs

(5)

Value of

Levered Firm

(2) + (3) – (4)

$0 $10 $0.00 $0.00 $10.00

1 10 0.22 0.00 10.22

*The optimal amount of debt would be $5 million.

6. a. without bankruptcy costs

[ki × (B/V)] + [ke × (S/V)] = ko

(10.00%) (1.00) = 10.000%

(4.00%) (0.10) + (10.50%) (0.90) = 9.850%

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

181

© Pearson Education Limited 2008

b. with bankruptcy costs

[ki × (B/V)] + [ke × (S/V)] = ko

(10.00%)(1.00) = 10.000%

(4.00%)(0.10) + (10.50%)(0.90) = 9.850%

With bankruptcy costs, the optimal capital structure is 40 percent debt in contrast to 60

percent bankruptcy costs.

7. According to the notion of asymmetric information between management and investors, the

company should issue the overvalued security, or at least the one that is not undervalued in

In contrast, if the common stock were believed to be overvalued, management would want

Chapter 17: Capital Structure Determination

182

© Pearson Education Limited 2008

SOLUTIONS TO SELF-CORRECTION PROBLEMS

1. a. Qwert Typewriter Company:

O Net operating income $ 360,000

k

o Overall capitalization rate ÷ 0.18

b. Yuiop Typewriters, Inc.:

O Net operating income $ 360,000

k

o Overall capitalization rate ÷ 0.18

Yuiop has a lower equity capitalization rate than Qwert, because Yuiop uses less debt in

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

183

© Pearson Education Limited 2008

2. Value of firm if unlevered:

Earnings before interest and taxes $ 3,000,000

Value with $4 million in debt:

Value of

levered firm = Value of firm

if unlevered + Present value of

tax-shield benefits of debt

Value with $7 million in debt:

Due to the tax subsidy, the firm is able to increase its value in a linear manner with more

debt.

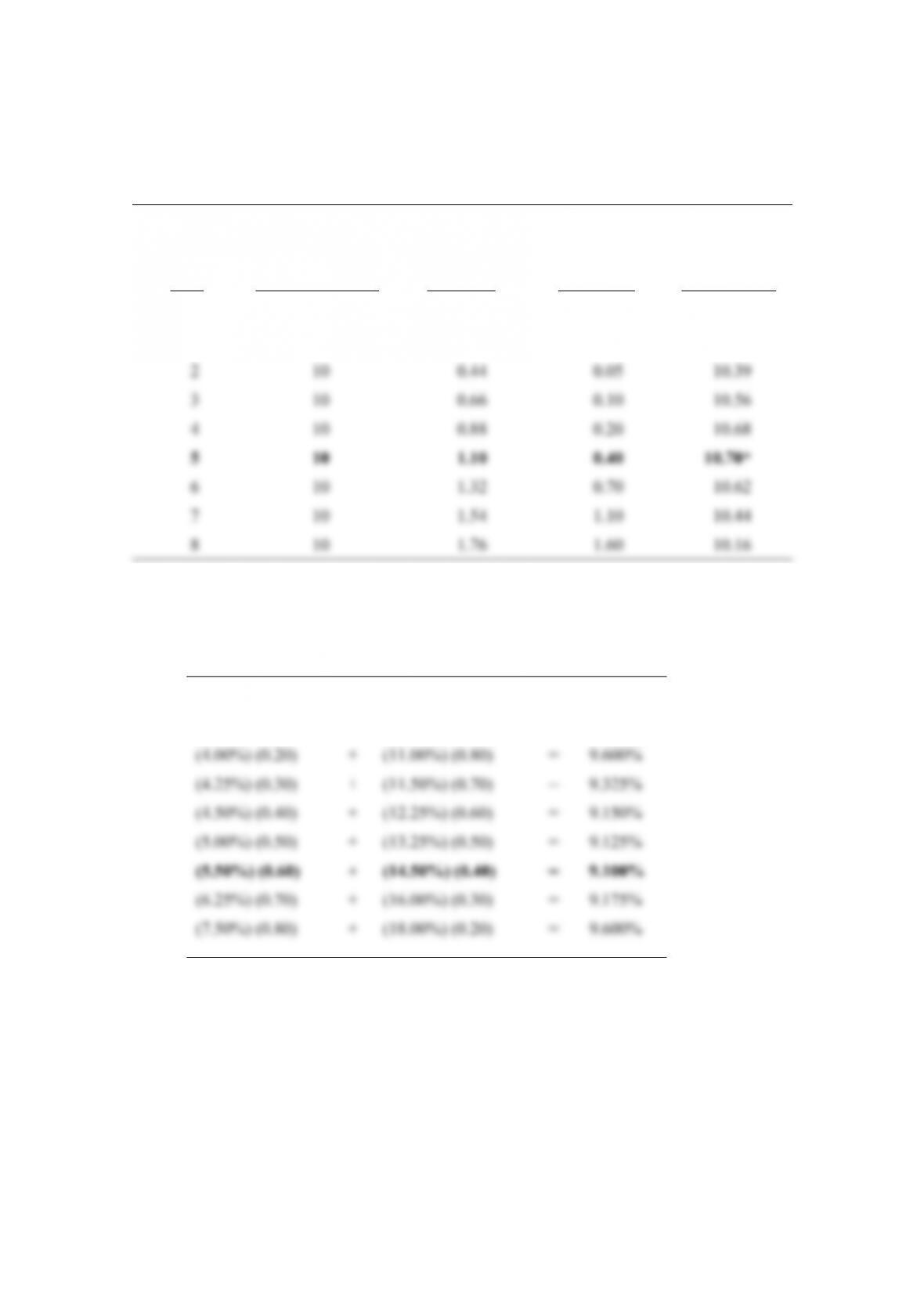

3. (In millions):

(1)

Level

of

Debt

(2)

Firm

Value

Unlevered

(3)

PV of Tax-Shield

Benefits Of Debt

(1) × 0.20

(4)

PV of Bankruptcy,

Agency & Increased

Interest Costs

Value of Firm

(2)+(3)–(4)

$ 0 $15 $0 $0.0 $15.0

5 15 1 0.0 16.0

*The market value of the firm is maximized with $20 million in debt.