144

© Pearson Education Limited 2008

Required Returns and the Cost

of Capital

To guess is cheap. To guess wrong is expensive.

CHINESE PROVERB.

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

145

© Pearson Education Limited 2008

ANSWERS TO QUESTIONS

1. If the weights used in the calculations do not correspond to the proportions of financing the

2. The principal qualification to its use is that existing as well as new investment proposals are

alike with respect to risk. In other words, the proposal being judged should not alter the risk

3. Yes, these funds have a cost. In most cases, however, the cost is ignored because these

4. The tax shield associated with the use of debt funds would be lost, at least until profits were

restored. As a result, we would no longer multiply the before-tax cost of debt by one minus

5. Dividends per share are estimated out into the future, preferably out to infinity. The

discount rate necessary to equate the present value of the expected future stream of

6. The critical assumption is that capital markets are perfect and that only the systematic risk

of the firm is important. With market imperfections, such as bankruptcy costs, the total risk

7. The firm’s before-tax cost of debt is used as a base to which a risk premium is added. The

risk premium is the difference in required return between stocks and bonds. For companies

8. Proxy companies are used in place of the project or group of projects under consideration.

The idea is to find a group of proxy companies that closely parallel the business represented

Chapter 15: Required Returns and the Cost of Capital

146

© Pearson Education Limited 2008

9. A project-specific required return refers to the hurdle rate for a specific project as derived

10. Management determines the acceptability of the project on the basis of the project’s

expected return in relation to the probability distribution of possible returns. The usual

11. The RADR approach to project selection calls for “adjusting” the required return, or

discount rate, upward (downward) from the firm’s overall cost of capital for projects or

12. For a group of projects, the correlation between returns of the various projects must be

13. Empirically, companies in the same industry tend to have similar betas and required rates of

return. However, there are many exceptions. It depends on how similar the industry

14. No. Eventually the equity base will need to be rebuilt and this will require retained earnings

15. An increase in bankruptcy costs would increase the required rate of return for companies.

The change should make companies more conscious of avoiding bankruptcy and analyzing

16. If the divisions have significantly different risks, a company should use different costs of

capital for them. One approach is the capital-asset pricing model context using outside

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

147

© Pearson Education Limited 2008

17. Value is created when projects are accepted, whose expected returns exceed the required

18. Through investment in assets, value is created by industry attractiveness and competitive

SOLUTIONS TO PROBLEMS

1. (1) (2) (1) × (2)

Cost Proportion of Total Financing Weighted Cost

Bonds ki B/(B+S) ki[B/(B+S)]

Thus, ko = ki[B/(B+S)] + ke[S/(B+S)]

or alternatively written

ie

o

k(B)+k(S)

k(B + S)

=

$7,000,000 += +=

ko = ki[B/(B+S)] + ke[S/(B+S)]

Chapter 15: Required Returns and the Cost of Capital

148

© Pearson Education Limited 2008

3. (January 20X1)

1

0

D$3

P$300

(January 20X2)

1

0

D$3.45

P = = = $57.50

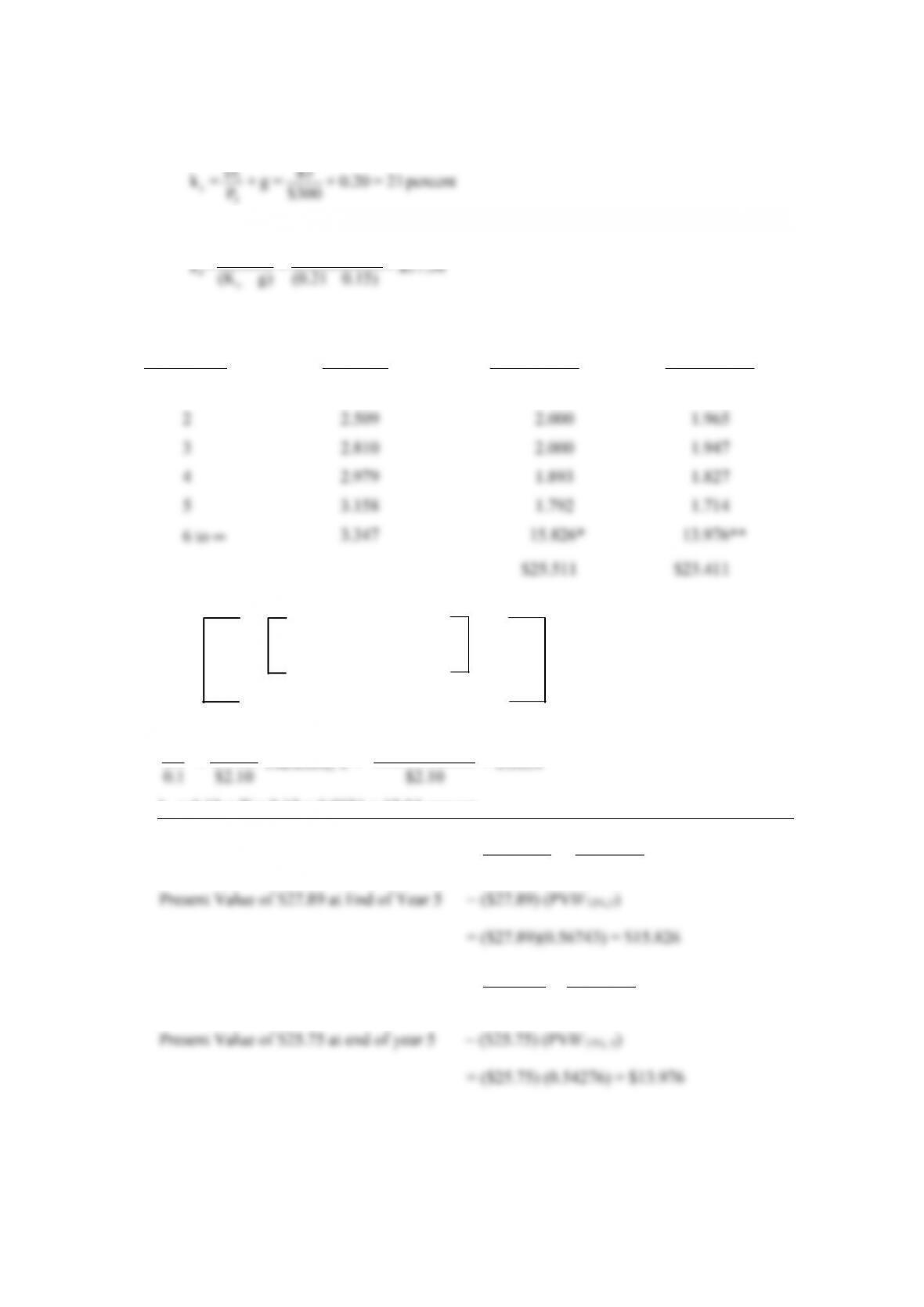

4.

End of Year

Dividend

Per Share

Present Value

at 12 Percent

Present Value

at 13 Percent

1 $ 2.240 $ 2.000 $ 1.982

0.12 $25.511

X $0.511

k

e $25

0.01

0.13 $23.411

$2.10

x $0.511 (0.01)($0.511)

= Therefore, x = = 0.0024

ke = 0.12 + X = 0.12 + 0.0024 = 12.24 percent

* Implied Value of Stock at End of Year 5 = D$3.347

6= = $27.89

(0.12 – g) (0.12 – g)

**Implied Value of Stock at End of Year 5 = $3.347

D6

(0.13–g) (0.13 – 0)

= = $25.75

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

149

© Pearson Education Limited 2008

5.

(1)

After-tax Cost

(2)

Proportion of Total Financing

(1) × (2)

Weighted Cost

$90,000

.145 −−=−

The proposal should be rejected. Without flotation costs, however, the net present value

would have been positive and the proposal acceptable.

7. a. Cost of equity = 0.12 + (0.18 – 0.12) 1.28 = 19.68 percent

b. The approach assumes that unsystematic risk is not a factor of importance, which may

8. a. Required Return = 0.10 + (0.15 – 0.10)(1.10) = 15.5 percent

c. Required Return

Required Return

Expected value of required rate of return

Chapter 15: Required Returns and the Cost of Capital

150

© Pearson Education Limited 2008

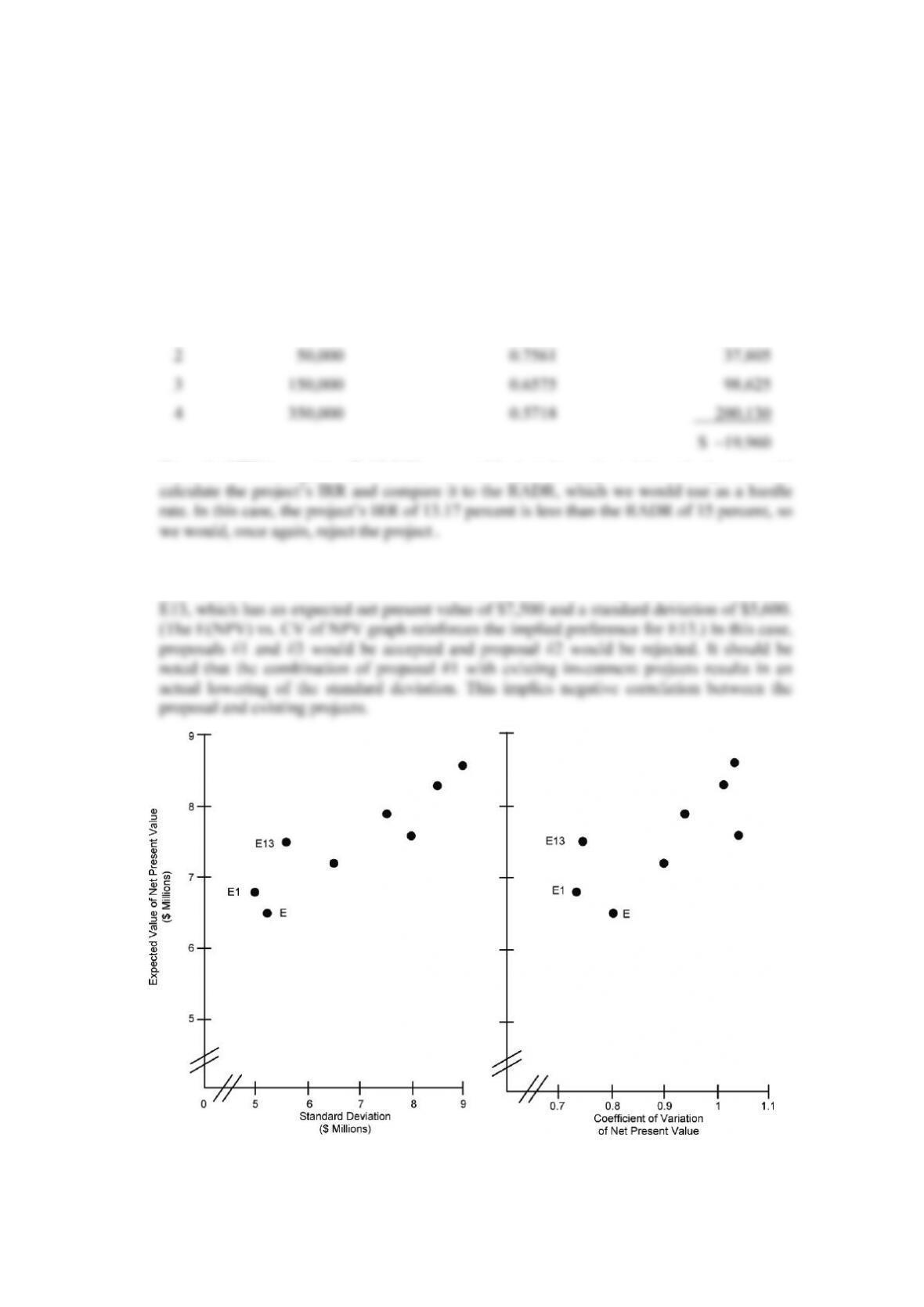

9. Using the RADR approach we would calculate the project’s net present value at the

management-determined risk-adjusted discount rate:

Year

————

(1)

——————————

Expected Cash Flow

——————————

(2)

————————————

Discount Factor at 15%

————————————

(1) × (2)

———————

Present Value

———————

0 $–400,000 1.0000 $–400,000

1 50,000 0.8695 43,480

Since the NPV is negative ($–19,960), we would reject the project. Alternatively, we could

10. The selection will depend on the risk preferences of the individual. Graphs of the plots are

shown below. For the reasonable risk averter, the selection will probably be combination

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

151

© Pearson Education Limited 2008

Solution to Appendix A Problem:

11. a.

c)]

β

Peerless unlevered beta = [1+(B/S) (1 T

j

–

1.15 1.15 1.00

===

An adjusted beta of 1.45 is appropriate for the new venture if the assumptions of the

capital-asset pricing model hold, except for corporate taxes.

b. ki = kd(1 – Tc) = 0.15(1 – 0.4) = 0.09

ke = Rf + ( m

R– Rf)ß = 0.13 + (0.17 – 0.13)1.45 = 0.188

Chapter 15: Required Returns and the Cost of Capital

152

© Pearson Education Limited 2008

Solution to Appendix B Problem:

12. a.

Schedule for determining the present value of the interest tax-shield benefits related to

the new snow plow truck

End of

Year

(1)

Debt Owed

At Year End

(1)t–1 – $3,000

(2)

Annual Interest

(1)t–1 × 0.12

(3)

Tax-Shield

Benefits

(2) × 0.30

(4)

PV of Benefits

at 12%

0 $18,000 – – – – – –

1 15,000 $2,160 $648 $ 579

To an all-equity financed firm, the net present value of the project’s after-tax operating cash

flows would be,

t

while the adjusted present value would be,

The project is acceptable.

b. If the cash flows are $8,000 per year instead of $10,000, the net present value of the

project’s after-tax operating cash flows becomes –$520, while the adjusted present

value becomes,

The project is still acceptable – but, barely.

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

153

© Pearson Education Limited 2008

SOLUTIONS TO SELF-CORRECTION PROBLEMS

1. a. ke = D1/P0 + g D1 = D0(1.12) = $1(1.12) = $1.12

b. Through the trial-and-error approach illustrated in Chapters 3 and 4, one ends up

determining that the discount rate necessary to discount the cash dividend stream to $20

must fall somewhere between 18 and 19 percent as follows:

End of Year Dividend Per Share Present Value At 18% Present Value At 19%

1 $1.20 $1.02 $1.01

Year 6 dividend = $2.49 (1.10) = $2.74

Market prices at the end of year 5 using a constant growth dividend

valuation model: P5 = D6/(ke – g)

Present value at time 0 for amounts received at end of year 5:

Chapter 15: Required Returns and the Cost of Capital

154

© Pearson Education Limited 2008

18% 19%

Present value of years 1 – 5 $ 5.26 $ 5.13

Therefore, the discount rate is closer to 18 percent than it is to 19 percent. Interpolating,

we get

and ke = 0.18 + X = 0.18 + 0.0010 = 18.10 percent, which is the estimated return on equity

that the market requires.

2.

Situation Equation: Rf + ( m

R– Rf)ß Return Required

1 10% + (15% – 10%) 1.00 15.0%

The greater the risk-free rate, the greater the expected return on the market portfolio, and the

greater the beta, the greater will be the required return on equity, all other things being the

same. In addition, the greater the market risk premium mf

(R R )–, the greater the required

return, all other things being the same.

3. Cost of debt = 15%(1 – 0.4) = 9%

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

155

© Pearson Education Limited 2008

As mentioned in the text, a conceptual case can be made for adjusting the nonequity costs of

financing the two divisions for differences in systematic risks. However, we have not

done so.

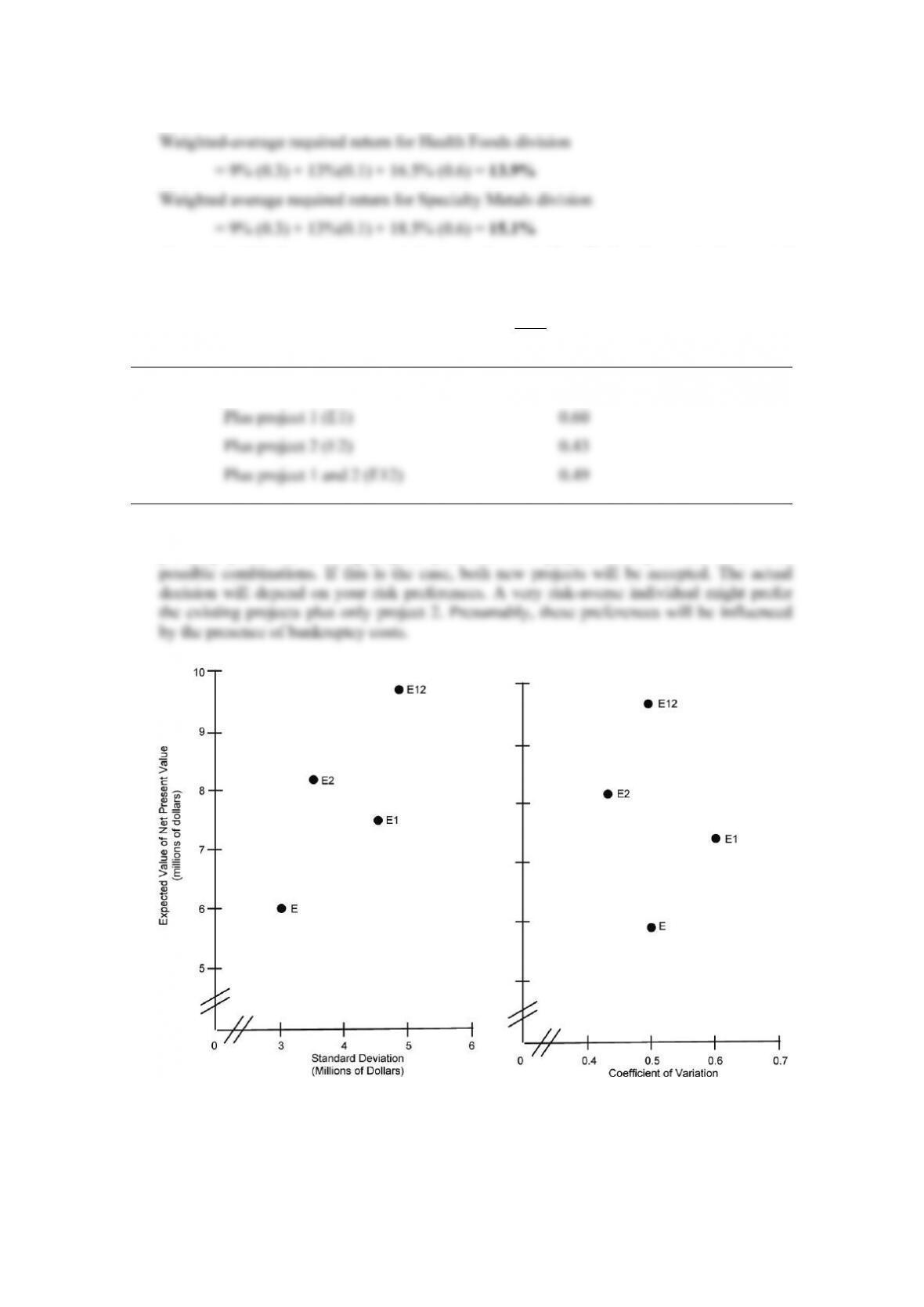

4. a. The coefficients of variation (standard deviation/

N

PV ) for the alternatives are as follows:

Existing projects (E) 0.50

Graphs of risk versus return are shown below. A moderately risk-averse decision maker will

probably prefer the existing projects plus both new projects to any of the other three

Chapter 15: Required Returns and the Cost of Capital

156

© Pearson Education Limited 2008

b. If the CAPM approach leads to a different decision, the key to deciding would be the

importance of market imperfections. As indicated earlier, if a company’s stock is traded