134

© Pearson Education Limited 2008

Risk and Managerial (Real) Options in Capital

Budgeting

“Risk? Risk is our business. That’s what this starship

is all about. That’s why we’re aboard her!”

JAMES T. KIRK,

CAPTAIN OF THE STARSHIP ENTERPRISE

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

135

© Pearson Education Limited 2008

ANSWERS TO QUESTIONS

1. Investment projects with different risks can affect the valuation of the firm by suppliers of

capital. A project that provides a 20 percent expected return may add so much risk as to

2. The

standard deviation is a measure of the absolute dispersion of the probability

(To the extent that a distribution is skewed and a person is concerned with skewness, a

between measure might be the semi-variance. The semivariance is the variance of the

One alternative measure that is easy to use is the coefficient of variation (CV).

Mathematically, it is defined as the ratio of the standard deviation of a distribution to the

3. To standardize the dispersion of a probability distribution, one takes differences from the

expected value (mean) of the distribution and divides them by the standard deviation. The

4. For the riskless project the probability distribution would have no dispersion. It would be a

5. The coefficients of variation for the two projects are:

6. The

initial probabilities are those for outcomes in the first period. Conditional probabilities

are those for outcomes in subsequent periods and conditional on the outcome(s) in the

Chapter 14: Risk and Managerial (Real) Options in Capital Budgeting

136

© Pearson Education Limited 2008

7. The risk-free rate is used to discount future cash flows so as not to double count for risk. If a

premium for risk, particularly a large premium, is included in the discount rate, a risk

8. Simulation gives the analyst an idea of the dispersion of likely returns from a project as well

9. The greater the correlation of net present values among projects, the greater the standard

10. A portfolio of assets dominates another if it has a higher expected return and the same or

11. When a decision maker decides on a portfolio of assets, that determines the acceptance or

12. A managerial option has to do with management’s flexibility to make a decision after a

project is accepted that will alter the project’s subsequent expected cash flows and/or its

13. The present value of a managerial option is determined by the likelihood that it will be

exercised and the magnitude of the resulting cash-flow benefit. The greater the uncertainty

14. Managerial options include (i) the option to expand production in the future if things turn

out well (or to contract if conditions do not turn out well), (ii) the option to abandon a

project, and (iii) the option to postpone a project’s acceptance or launch. Options (i) and (ii)

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

137

© Pearson Education Limited 2008

SOLUTIONS TO PROBLEMS

1. a. Simply by looking, project B looks less risky.

b. E(CFA) = (0.2) ($2,000) + (0.3) ($4,000)

B clearly dominates A since it has lower risk for the same level of return.

2. a.

Project E(NPV) σNPV CVNPV

A $10,000 $20,000 2.00

On the basis of E(NPV) and standard deviation of NPV, …

— C dominates A, B, and D;

— A dominates B and D; and

Chapter 14: Risk and Managerial (Real) Options in Capital Budgeting

138

© Pearson Education Limited 2008

b.

Project Z-score (0 – E(NPV))/σNPV Probability (NPV < 0)

A –0.50 0.3085

3. The general formula to use is:

Z (the Z-score) = (NPV* –

N

PV )/σNPV

4.

Year 1 Year 2 Year 3 Overall

Initial

Prob.

Net Cash

Flow

Cond.

Prob.

Net Cash

Flow

Cond.

Prob.

Net

Cash

Flow

Joint

Prob.

0.4 –$ 300 1.0 $ 0 0.20

NOTE: Initial investment at time 0 = $1,000.

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

139

© Pearson Education Limited 2008

b.

(1)

Cash Flow

Series

(2)

Net Present

Value

(3)

Joint Probability of

Occurrence

(4)

(2) × (3)

1 –$1,272 0.20 –$254.40

c. The expected value of net present value of the project is found by multiplying together

the last two columns above and totaling them. This is found to be $661 (after rounding).

d. The standard deviation is:

[0.20 (–$1,272 – $661)2 + 0.30 (–$1,000 – $661)2

Thus, the dispersion of the probability distribution of possible net present values is very

wide. In addition to the distribution being very wide, there is also a 50 percent

probability of NPV being less than zero.

5. Expected net present value:

1 and 2 = $10,000 + $8,000 = $18,000

Standard deviation of net present value:

1 and 2 = [($4,000)2 + (2) (0.6) ($4,000) ($3,000) + ($3,000)2]0.5 = $6,277

Coefficient of variation of net present value:

1 and 2 = $6,277 / $18,000 = 0.35

Combination of 1 and 2 dominates the other two combinations on the basis of expected net

present value and coefficient of variation of net present value.

Chapter 14: Risk and Managerial (Real) Options in Capital Budgeting

140

© Pearson Education Limited 2008

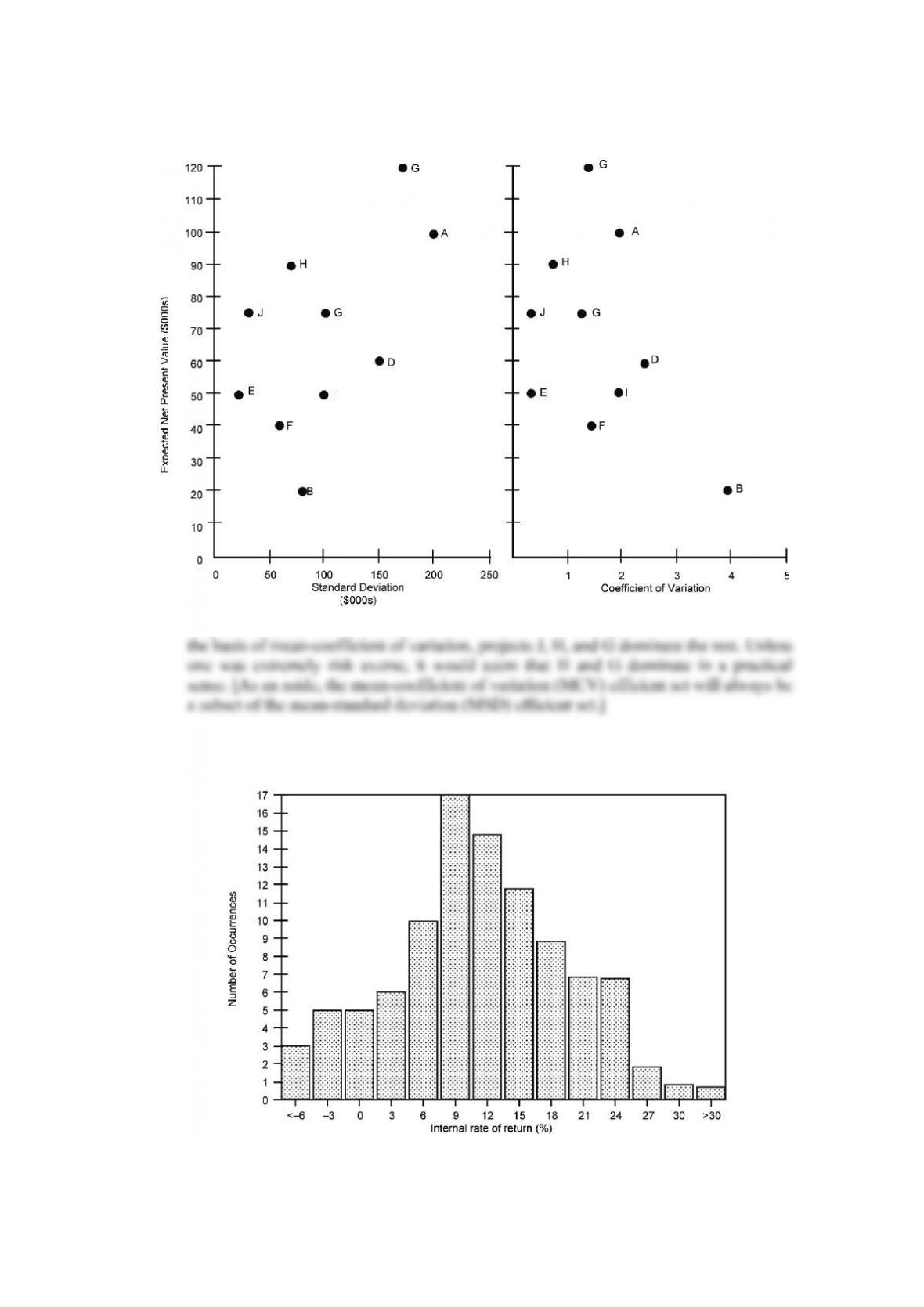

6. a.

b. Projects E, J, H, and G dominate the rest on the basis of mean-standard deviation. On

7. a. Each simulation will differ somewhat, so there is no exact answer to this problem. A

simulation involving 100 runs resulted in the following IRR distribution:

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

141

© Pearson Education Limited 2008

b. The most likely IRR was in the 7 to 9 percent range – a relatively modest return. As can

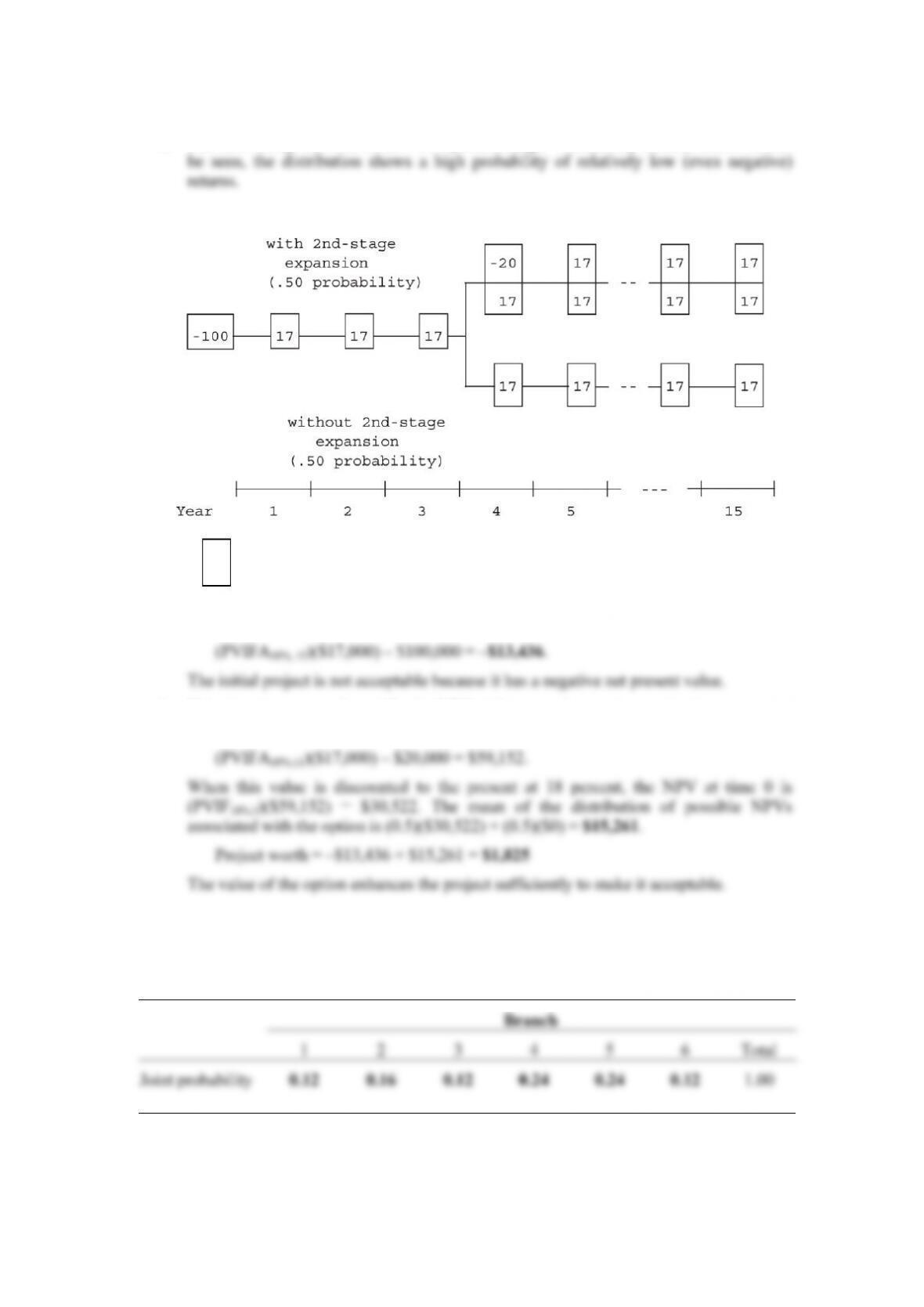

8.

Key: │ │ expected cash flows in $000s

└——┘

a. NPV of initial project at 18 percent required rate of return equals

b. If the location proves favorable, the NPV of the second-stage (expansion) investment at

the end of year 4 will be

SOLUTIONS TO SELF-CORRECTION PROBLEMS

1. a.

Chapter 14: Risk and Managerial (Real) Options in Capital Budgeting

142

© Pearson Education Limited 2008

b. At a risk-free rate of 10 percent (i) the net present value of each of the six complete

Year 0 Year 1 Year 2 Branch NPV

$ 826 1 –$ 810

c. Standardizing the difference from zero, we have –$595/$868 = –0.685. Looking in

2. a. Expected net present value = $16,000 + $20,000 + $10,000 = $46,000

Standard deviation = [($8,000)2 + (2) (0.9) ($8,000) ($7,000) +

b. Expected net present value = $46,000 + $12,000 = $58,000

Standard deviation = [$328,040,000 + ($9,000)2 +

The coefficient of variation for existing projects (/NPV)

σ

= $18,112/$46,000 = 0.39.

The coefficient of variation for existing projects plus puddings = $22,659/$58,000 = 0.39.

While the pudding line has a higher coefficient of variation ($9,000/$12,000 = 0.75) than

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

143

© Pearson Education Limited 2008

3. a.

Year 0 Year 1 Year 2 Branch NPV

$20,000 1 –$17,298

Expected NPV = (0.30) (0.30) (–$17,298) + (0.30) (0.50) (–$8,724) +

b. We should abandon the project at the end of the first year if the cash-flow in that year

turns out to be $60,000. The reason is that given a $60,000 first year cash-flow, the

$29,000 expected value of possible second-year cash flows (i.e., (0.30)($20,000) +

When we allow for abandonment, the original projected cash flows for branches 1, 2,

and 3 are replaced by a single branch having a cash-flow of $105,000 ($60,000 plus

Thus, the expected net present value is increased when the possibility of abandonment

is considered in the evaluation. Part of the downside risk is eliminated because of the

abandonment option.