93

© Pearson Education Limited 2008

Accounts Receivable and Inventory Management

IN GOD WE TRUST. All others must pay cash.

ANONYMOUS

Chapter 10: Accounts Receivable and Inventory Management

94

© Pearson Education Limited 2008

ANSWERS TO QUESTIONS

1. No. Only if the added profitability of the additional sales to the “deadbeats” (less bad-debt

loss and other costs) does not exceed the required return on the additional (and prolonged)

2. a. Sales unaffected; profits decreased. This policy suggests that the firm has a poor

b. Sales increased; profitability probably reduced. This policy suggests a lax collection

c. Sales decreased, profits decreased. Credit standards are probably too strict. Customers

d. Sales decreased, profits decreased. Credit standards are probably too strict. Customers

4. To analyze a credit applicant, one might turn to financial statements provided by the

applicant, credit ratings and reports, a check with the applicant’s bank (particularly if a loan

8. A

line of credit establishes the maximum amount of credit, that an account can have

outstanding at one time. The advantage of this arrangement is that it is automatic. An order

9. Aging accounts receivable represents an effort to determine the age composition of

receivables. A similar approach for inventory could involve determining the inventory

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

95

© Pearson Education Limited 2008

10. The greater the ordering costs, the more inventory that will be maintained, all other things

11. Efficient inventory management implies the elimination of redundant inventory and

selecting a level of inventory that provides the risk-profitability trade-off desired by

investors. Eliminating redundant inventory does not involve increasing risk. The

12. The firm could lower its investment in inventories by

a. shortening the lead time on purchases;

b. improving sales forecasts;

Increased costs include

a. higher prices from suppliers;

13. With no variation in product demand, the firm would be able to minimize costs by

maintaining a level production schedule and eliminating inventory safety stocks. With

14. From the standpoint of dollars committed, the two are the same. However, inventories

15. Usually a company will use the same required rate of return for both. However, if one type

Chapter 10: Accounts Receivable and Inventory Management

96

© Pearson Education Limited 2008

SOLUTIONS TO PROBLEMS

1.

Credit Policy A B C D

a. Incremental sales $2,800,000 $1,800,000 $1,200,000 $600,000

b. Incremental profitability1 280,000 180,000 120,000 60,000

1(10% contribution margin) × (incremental sales)

The company should adopt credit policy C because incremental profitability exceeds the

increased carrying costs for policies A, B, and C, but not for policy D.

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

97

© Pearson Education Limited 2008

2.

Credit Policy A B C D

a. Incremental sales $2,800,000 $1,800,000 $1,200,000 $600,000

b. Percent default 3% 6% 10% 15%

Adopt credit policy A. It is the only one where incremental profitability exceeds opportunity

costs plus bad-debt losses.

Chapter 10: Accounts Receivable and Inventory Management

98

© Pearson Education Limited 2008

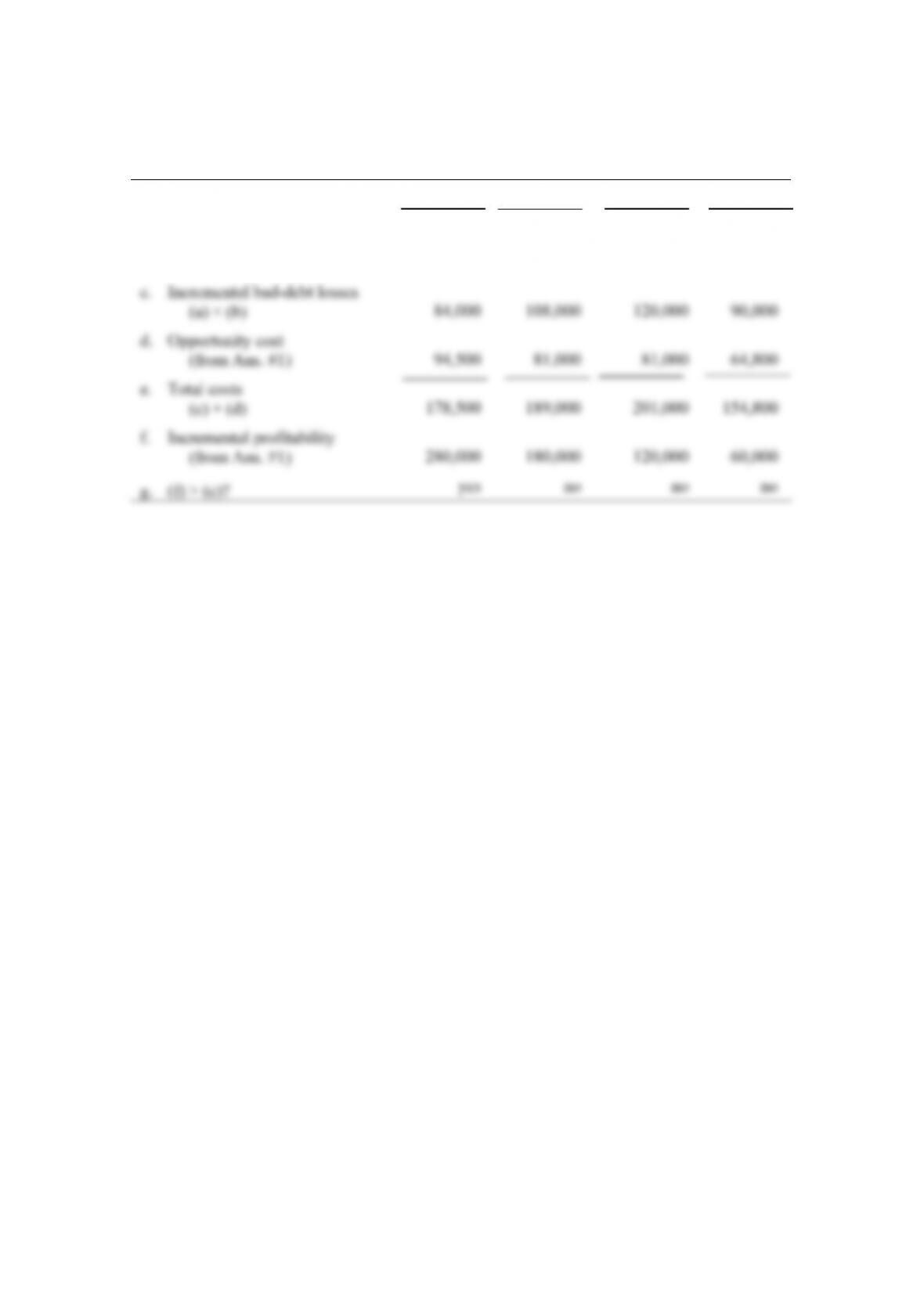

3.

Credit Policy A B C D

a. Incremental sales $2,800,000 $1,800,000 $1,200,000 $600,000

b. Percent default 1.5% 3% 5% 7.5%

Credit policy B now would be best. Any more liberal credit policy beyond this point

would only result in more incremental costs than benefits.

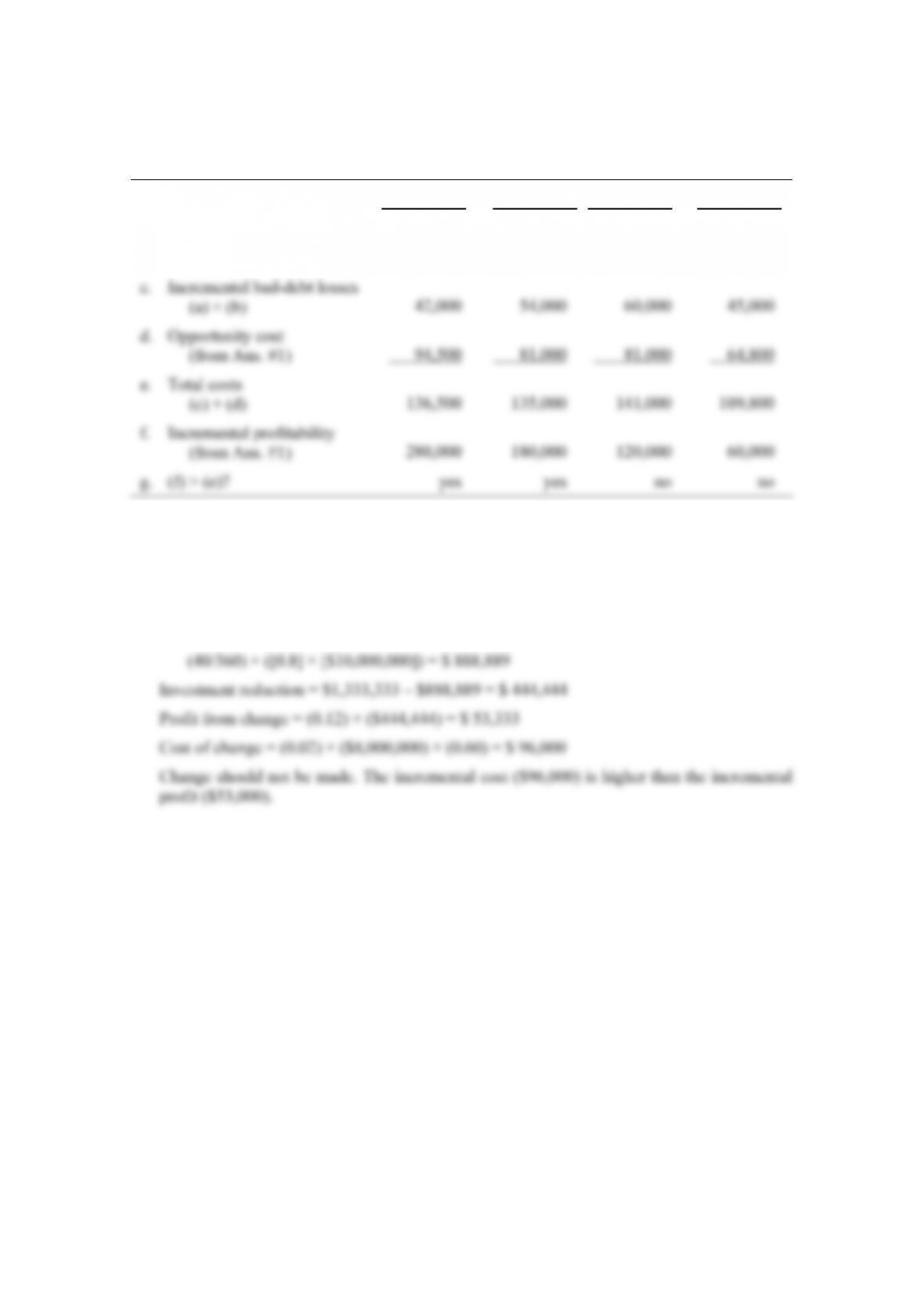

4. Current investment in accounts receivable =

(60/360) × ([0.8] × [$10,000,000]) = $1,333,333

New policy investment in accounts receivable =

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

99

© Pearson Education Limited 2008

5.

Present

Program

New Program Assuming

20% Opportunity Cost

New Program Assuming

10% Opportunity Cost

a. Annual sales $12 million $12 million $12 million

b. Receivable

turnover (RT)

(360 days/RTD) 4.8 6 6

As the sum of the return on the reduction in receivables with a 20 percent opportunity

cost plus, the reduction in bad-debt losses exceeds the increased collection expense of

Chapter 10: Accounts Receivable and Inventory Management

100

© Pearson Education Limited 2008

6. Positive factors:

a. The firm has maintained a reasonably good cash position over the period.

b. The firm has reduced by 50 percent its outstanding long-term debt.

7. a. C(Q/2) + O(S/Q) = TC

(1×): $1(5,000/2) + $100(5,000/5,000) = $2,600

c. It is assumed that sales are made at a steady rate, which may not be correct for

8. a. Total number of dints required = 150,000 × 12 = 1,800,000

b. TC = C(Q/2) + O(S/Q)

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

101

© Pearson Education Limited 2008

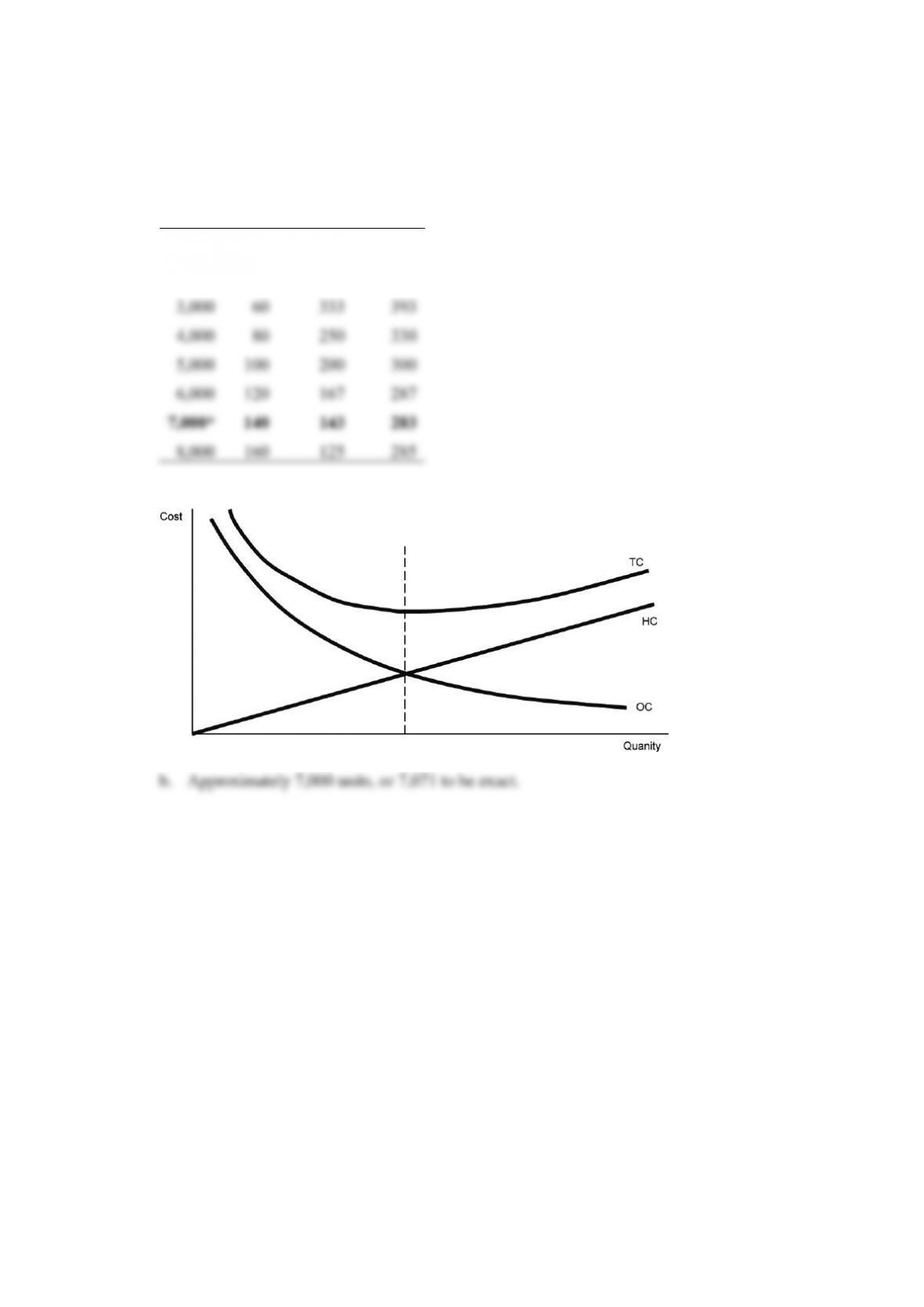

9. a. TC = C (Q / 2) + O (S / Q)

= ($0.04) (Q / 2) + ($200) (5,000 / Q)

Q HC OC TC

1,000 $ 20 $1,000 $1,020

2,000 40 500 540

Chapter 10: Accounts Receivable and Inventory Management

102

© Pearson Education Limited 2008

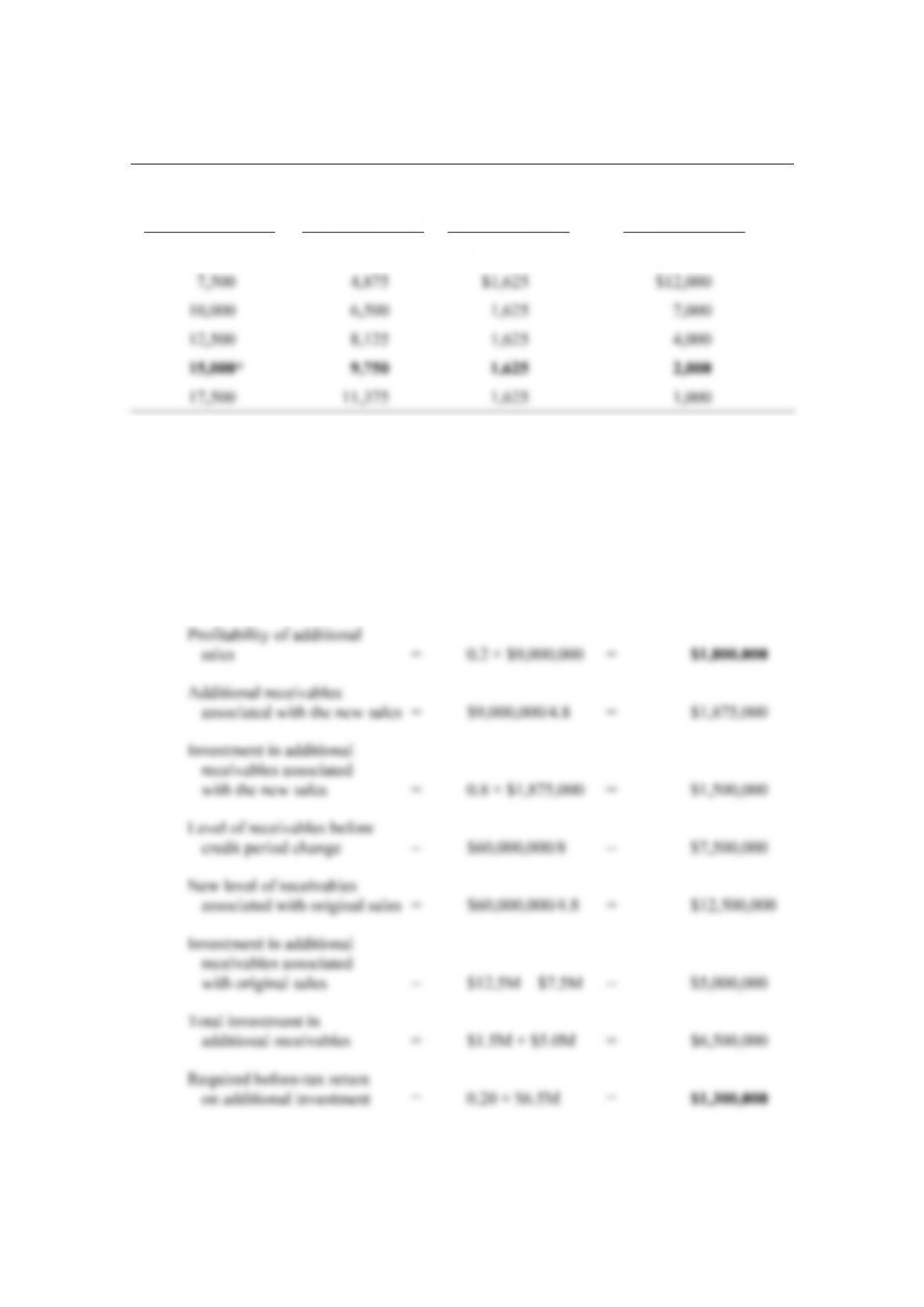

10.

Level of Safety

Stock (In Gallons)

Cost of Carrying

Safety Stock

Incremental

Cost

Incremental

Stockout

Cost Savings

5,000 $ 3,250 – – – –

The level of safety stock should be increased to 15,000 gallons from 5,000 gallons.

Beyond that point incremental costs are larger than incremental benefits.

SOLUTIONS TO SELF-CORRECTION PROBLEMS

1. Old receivable turnover = 360/45 = 8 times

New receivable turnover = 360/75 = 4.8 times

Van Horne and Wachowicz, Fundamentals of Financial Management, 13th edition, Instructor’s Manual

103

© Pearson Education Limited 2008

As the profitability on additional sales, $1,800,000, exceeds the required return on the

2. As the bad-debt loss ratio for the high-risk category exceeds the profit margin of 22 percent,

it would be desirable to reject orders from this risk class if such orders could be identified.

However, the cost of credit information as a percentage of the average order is $4/$50 = 8

An example can better illustrate the solution. Suppose that new orders were $100,000, the

following would then hold:

ORDER CATEGORY

Low

Risk

Medium

Risk

High

Risk

To save $4,800 in bad-debt losses by identifying the high-risk category of new orders,

the company must spend $8,000. Therefore, it should not undertake the credit analysis of

new orders. This is a case where the size of order is too small to justify credit analysis. After

a new order is accepted, the company will gain experience and can reject subsequent orders

if its experience is bad.

3. a.

b.

c.

The lower the order cost, the more important carrying costs become relatively, and the

smaller the optimal order size.

Chapter 10: Accounts Receivable and Inventory Management

104

© Pearson Education Limited 2008

4. Inventories after change = $48 million/6 = $8 million