Part Two

Important Conceptual Tools

Part Two Includes

Chapter 4 Return and Risk

Chapter 5 Modern Portfolio Concepts

Chapter 4

Return and Risk

◼ Outline

Learning Goals

I. The Concept of Return

A. Components of Return

1. Income

2. Capital Gains (or Losses)

B. Why Return Is Important

1. Historical Performance

2. Expected Return

C. Level of Return

1. Internal Characteristics

2. External Forces

D. Historical Returns

II. The Time Value of Money and Returns

A. Computational Aids for the Use of Time Value Calculations

B. Determining a Satisfactory Investment

Concepts in Review

III. Measuring Return

A. Real, Risk-Free, and Required Returns

B. Holding Period Return

1. Understanding Return Components

2. Computing the Holding Period Return (HPR)

3. Using the HPR in Investment Decisions

C. Yield: The Internal Rate of Return

1. Yield for a Single Cash Flow

a. Calculator Use

b. Spreadsheet Use

Chapter 4 Return and Risk 51

◼ Key Concepts

1. The concept of return, its component parts, and the forces that affect the level of return realized by an

investor; historical returns reviewed

2. Interest income and the concept of time value, its underlying future and present value computations,

and its use in the investment decision-making process

3. Usage of financial calculators, computers, and spreadsheets in measuring risk and return

4. Real, risk-free, and required returns on investments

5. The computation and use of the holding period return and the internal rate of return, and the role yield

can play in the investment decision

6. The sources and basic types of risk, the concept of risk, its positive relationship to return, and its role

in investment decision-making

7. The basic steps involved in evaluating the risk-return characteristics of an investment

◼ Overview

The concepts of return and risk are developed in this chapter. This chapter is conceptually more

demanding than the preceding one, so the instructor should plan to spend more class time on it.

1. Returns are rewards for investing. The components of total return are income and capital gains (or

losses). Income is cash received for holding an investment, whereas capital gains refers to income

that is attributed to an increase—realized or unrealized—in the value of the investment.

2. Expected return motivates a person to invest in a particular vehicle. Expectations of returns are based

on the past returns of that vehicle. Measuring the historical return of a particular investment reveals

its average return as well as the trend of its returns.

3. The level of returns for a particular investment vehicle depends on internal characteristics, such

4. A satisfactory investment is one in which the present value (PV) of benefits (discounted at the

5. The required return of an investment is the rate that compensates the investor for its risk. It is

6. The holding period return (HPR), defined next, is useful in making investment decisions. The

instructor may show the class how HPR is computed, stressing that the HPR from identical periods

should be used when comparing two investments.

Chapter 4 Return and Risk 53

History tells us that stock market returns have averaged well above the interest rates payable on

3. Ignoring risk, a satisfactory investment is one for which the present value of benefits (discounted)

4. (a) The real rate of return is the return earned in a certain, risk-free world. It would equal the

nominal rate of return on a risk-free security less inflation. Historically, it has been relatively

The required rate of return equals the real rate of return plus the expected inflation premium

5. The holding period is simply the period of time over which the investor wishes to measure the return

on an investment. In comparing alternative investments, it is essential to use equal-length holding

6. The yield, or IRR, is the annual rate of return earned by a long-term investment. It is also defined as

Chapter 4 Return and Risk 55

©2011 Pearson Education, Inc. Publishing as Prentice Hall

(g) Event risk is the risk that comes from a largely or totally unexpected event that has a significant

and usually immediate effect on the underlying value of an investment. The effect of this risk

seems to be isolated in most cases, affecting only certain companies and properties.

(h) Market risk is the risk of changes in investment returns caused by factors independent of the

given investment vehicle. It results from factors such as political, economic, and social events, or

changes in investor tastes and preferences.

11. Standard deviation is the most common measure of an asset’s risk. It measures the dispersion of

12. Investors’ attitudes toward risk or their risk-return trade-offs may be classified as one of the following:

Risk-indifferent investors do not require a greater return in exchange for each unit of additional risk.

13. The investment process can be summarized in four steps:

(1) Estimate the expected return over a given holding period using historical data or projected return

data, or both. The time value of these returns must be considered for long-term investments.

◼ Suggested Answers to Discussion Questions

Answers will vary according to student’s selections, tastes, and preferences.

◼ Solutions to Problems

©2011 Pearson Education, Inc. Publishing as Prentice Hall

58 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

(i)

(ii)

Forecasts

for:

Based on

Arithmetic Average

Based on

Average HPR

2012

$4.37

($45.00)* .128 = $5.76

2013

$4.37

($49.00)** .128 = $6.27

End of 2005 price gain in original data

For lack of information, we are assuming the 2006 return is $4.00 from capital

gains and $1.76 from income.

(c) Students should be made aware of the fact that many other forecasts are possible. Other factors

may be relevant here: Will the pattern of two good years followed by a bad one continue? Do

future prospects seem bright? (We will discuss forecasting returns on specific investments in

later chapters.)

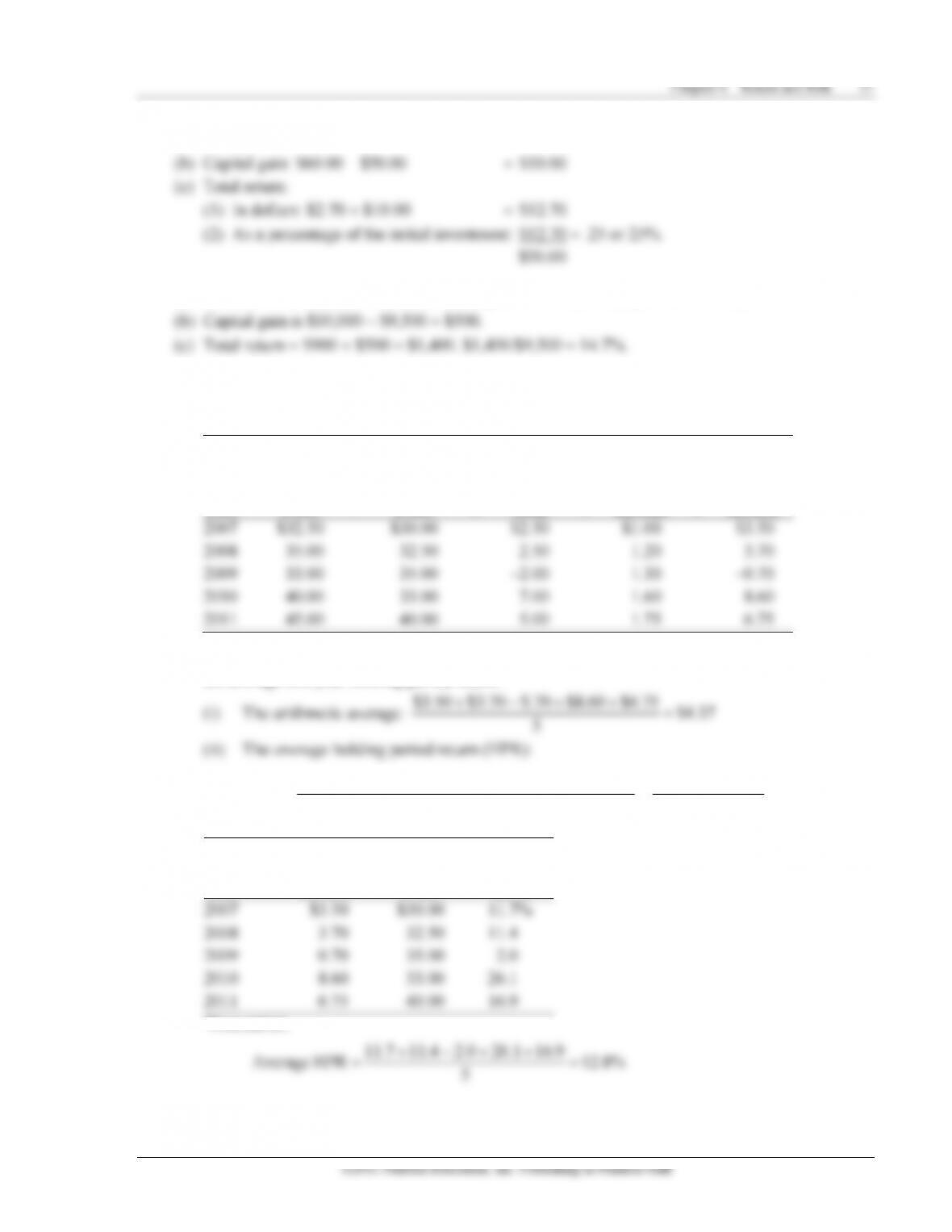

6. Total return = Income plus capital gains

7. (a) Using the notation given in the chapter, the risk-free rate of interest for both investments is:

=+

=

F* IP

8%

Rr

(b) The required returns for each investment are calculated as follows:

r1 =

*r

*r

+ IP + RPi or RF + RPi

8. The risk-free rate = Real rate + Expected inflation premium. If the expected inflation premium

increases by 1%, then the risk-free rate will increase by 1% to 8%.

9. Holding period return (HPR) =

Current income Ending price Beginning price

Beginning price

+−

+ + + + −

==

=

+ + + + −

==

=

X

Y

$1.00 $1.20 $0 $2.30 $29.00 $30.00 $3.50

HPR $30.00 $30.00

11.67%

$0 $0 $0 $2.00 $56.00 $50.00 $8.00

HPR 50.00 $50.00

16%

Chapter 4 Return and Risk 59

If the investments are held beyond a year, the capital gain (or loss) component would not be realized

and would likely change. Assuming they are of equal risk, Investment Y would be preferred since it

offers the higher return (16.00% for Y versus 11.67% for X).

10. HPR = (Income over the period + Capital gains)/Beginning investment value

The first investment provides the higher annualized return.

12. The present value is $5,000. The value in 10 years will be $9,000.

(a) Using present value, the yield is calculated as:

=

=

=

x%, 10 yrs.

x%, 10 yrs.

$9,000 PVIF $5,000

$5,000

PVIF $9,000

0.556

From Table A.3, Appendix A, at 10 years the PVIF of 6% is 0.558, which is very close to 0.556.

The yield, then, is estimated to be 6%. (Calculator solution is 6.05%).

(b) If a minimum return of 9% is required, this investment would not be recommended because it

only yields about 6%.

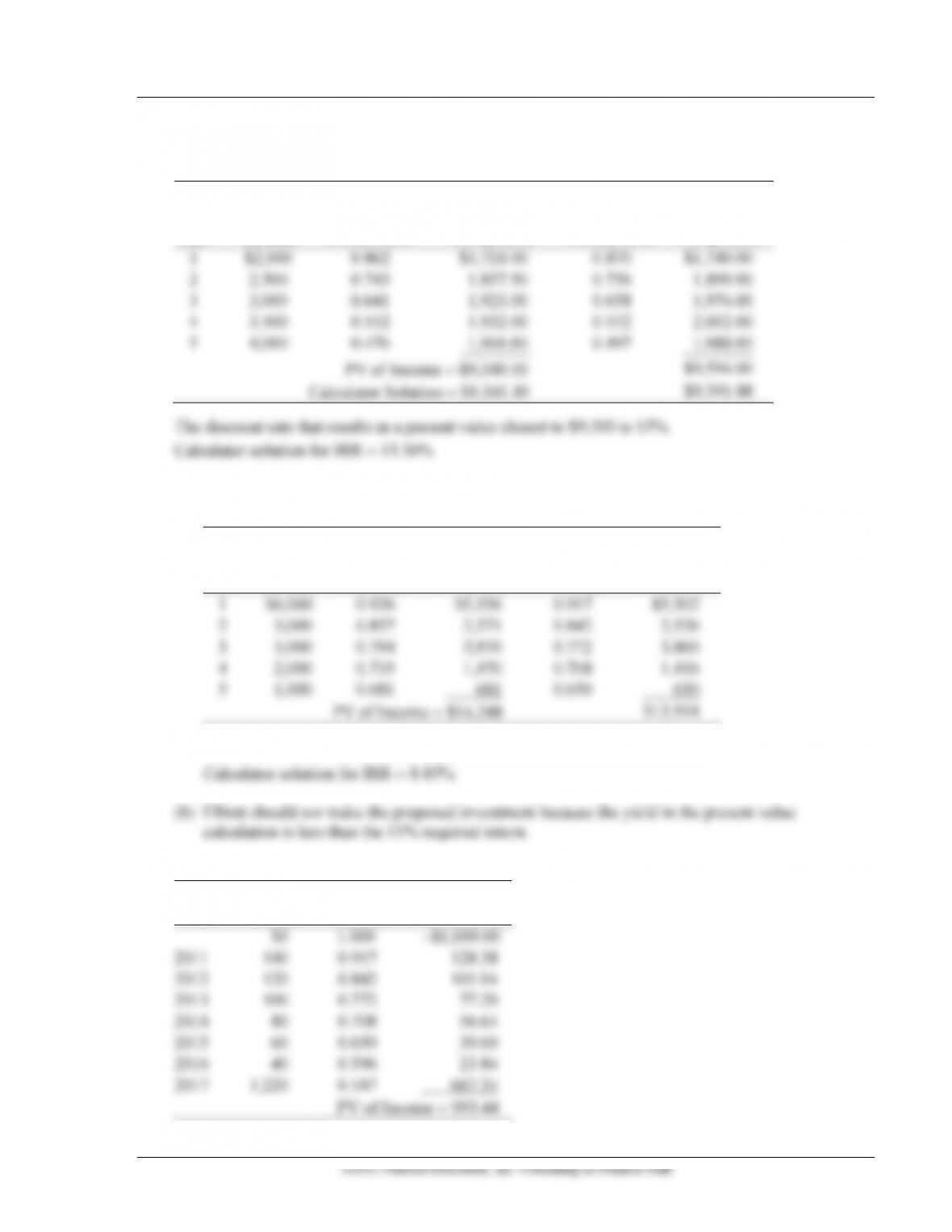

13. Using a present value interest factor of 4%:

$65 .962 = $62.53

$70 .925 = $64.75

$70 .889 = $62.23

$7,965 .855 = $6,810.08

$6,999.59

14. Interest on the investment in year 5:

Chapter 4 Return and Risk 61

The closest interest rate to 3.167 in Table A.4, Appendix A, is 17%. Because the larger cash flows are

received in the later years, 16% is a good starting point.

(1)

(2)

(3)

(4)

(5)

(1) (4)

Year

Income

PVIF, 16%

PV at 16%

PVIF, 15%

PV at 15%

1

$2,000

0.862

$1,724.00

0.870

$1,740.00

2

2,500

0.743

1,857.50

0.756

1,890.00

3

3,000

0.641

1,923.00

0.658

1,974.00

4

3,500

0.552

1,932.00

0.572

2,002.00

5

4,000

0.476

1,904.00

0.497

1,988.00

PV of Income = $9,340.50

$9,594.00

Calculator Solution = $9,341.49

$9,591.88

The discount rate that results in a present value closest to $9,500 is 15%.

Calculator solution for IRR = 15.36%

18. (a) Using the same technique as shown in the prior question, we find that 7% is a possible discount

rate. Because the larger cash flows occur in the early years, 8% is a good starting point.

(1)

(2)

(3)

(4)

(5)

(1) (2)

(1) (4)

Year

Income

8% PVIF

PV at 8%

9% PVIF

PV at 9%

1

$6,000

0.926

$5,556

0.917

$5,502

2

3,000

0.857

2,571

0.842

2,526

3

5,000

0.794

3,970

0.772

3,860

4

2,000

0.735

1,470

0.708

1,416

5

1,000

0.681

681

0.650

650

PV of Income = $14,248

$13,954

The discount rate that results in a present value closest to $14,000 is 9%.

19.

End of

(1)

(2)

(3)

Year

Income

9% PVIF

PV at 9%

$0

1.000

–$1,000.00

2011

140

0.917

128.38

2012

120

0.842

101.04

2013

100

0.772

77.20

2014

80

0.708

56.64

2015

60

0.650

39.00

2016

40

0.596

23.84

2017

1,220

0.547

667.34

PV of Income = $93.44

62 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

The yield is very close to 11% on this investment.

Since the yield of 11% is greater than the minimum required return of 9%, the investment is

recommended. This project would result in positive net present value to the investor.

20. Growth rates are calculated using the present value formula: PV = FVn PVIFk,n.

Investment

A

n = 2008 – 2004 = 4

PV = FV4 PVIFk, 4 yrs.

$5 = $8 PVIFk, 4 yrs.

.625 = PVIFk, 4 yrs.

12% < k < 13%

Calculator solution = 12.47%

B

n = 2008 – 1999 = 9

PV = FV9 PVIFk, 9 yrs.

$1.50 = $2.28 PVIFk, 9 yrs.

.658 = PVIFk, 9 yrs.

4% < k < 5%

Calculator solution = 4.76%

C

n = 2008 – 2002 = 6

PV = FV6 PVIFk, 6 yrs.

$2.50 = $2.90 PVIFk, 6 yrs.

.862 = PVIFk, 6 yrs.

2% < k < 3%

Calculator solution = 2.50%

21. 2010 – 2003 = 7 years

22. 2010 – 2006 = 4 years

23. (a) Investment A, with returns that vary widely—from 1% to 26%—appears to be more risky than

(b)

2

1

()

n

i

s r r

=

=−

Standard deviation

©2011 Pearson Education, Inc. Publishing as Prentice Hall

(1)

(2)

(3)

(4)

Return

Average

(1) – (2)

(3)2

Year

r I

Return, r

ri – r

(ri – r)2

2006

19%

12%

7%

49%

2007

1

12

–11

121

2008

10

12

–2

4

2009

26

12

14

196

2010

4

12

–8

64

434

= = =

−

==

A

434

S 108.5 10.42%

10.42%

CV .87

12.00%

Investment B:

(1)

(2)

(3)

(4)

Year

Return

Average

(1) – (2)

(3)2

r i

Return, r

ri – r

(ri – r)2

2006

8%

12%

–4%

16%

2007

10

12

–2

4

2008

12

12

0

0

2009

14

12

2

4

2010

16

12

4

16

40

= = =

−

==

A

40

S 10 3.16%

3.16%

CV .26

12.00%

(c) Investment A, with a standard deviation of 10.42, is considerably more risky than Investment B,

◼ Solutions to Case Problems

Case 4.1 Coates’ Decision

This case introduces the student to the concepts of opportunity cost and required rate of return. It further

64 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

(a) Using the present value technique for the equally risky projects, we select the one with the highest

=+

=

$799.20 $370.30

$1,169.50

Present value of B: This is the present value of a mixed stream, so we use the present-value interest

factors for one dollar from Table A.3.

(1)

(2)

(3)

(1) (2)

Year

Benefit

12% PVIF

Present Value

2011

$100

0.893

$89.30

2012

150

0.797

119.55

2013

200

0.712

142.40

2014

250

0.636

159.00

2015

300

0.567

170.10

2016

350

0.507

177.45

2017

300

0.452

135.60

2018

250

0.404

101.00

2019

200

0.361

72.20

2020

150

0.322

48.30

Total PV = $1,214.90

Each investment is acceptable because its present value is greater than its initial cost of $1,050.

(b) For projects of unequal risk, we must evaluate each at its required rate of return (adjusted for its level

of risk). Using a 16% interest factor (from Table A.3, Appendix A), the present value of Investment B is:

(1)

(2)

(3)

(1) (2)

Year

Benefit

16% PVIF

Present Value

2011

$100

0.862

$86.20

2012

150

0.743

111.45

2013

200

0.641

128.20

2014

250

0.552

138.00

2015

300

0.476

142.80

2016

350

0.410

143.50

2017

300

0.354

106.20

2018

250

0.305

76.25