Web Chapter 18

Real Estate and Other Tangible Investments

◼ Chapter Outline

Learning Goals

I. Investing in Real Estate

A. Investor Objectives

1. Investment Characteristics

2. Constraints and Goals

2. Supply

3. The Property

a. Restrictions on Use

b. Location

c. Site

d. Improvements

e. Property Management

4. Property Transfer Process

Concepts in Review

II. Real Estate Valuation

A. Estimating Market Value

2. The Comparative Sales Approach

3. The Income Approach

4. Using an Expert

B. Performing Investment Analysis

1. Market Value versus Investment Analysis

a. Retrospective versus Prospective

b. Impersonal versus Personal

c. Unleveraged versus Leveraged

d. NOI versus After-Tax Cash Flows

©2011 Pearson Education, Inc. Publishing as Prentice Hall

3. Calculating Yield

Concepts in Review

III. An Example of Real Estate Valuation

A. Set Investor Objectives

B. Analyze Important Features of the Property

C. Collecting Data on Determinants of Value

1. Demand

2. Supply

3. The Property

4. The Property Transfer Process

D. Perform Valuation of Investment Analysis

1. The Numbers

2. Cash Flow of Analysis

3. Proceeds from Sale

4. Discounted Cash Flow

5. Yield

E. Synthesize and Interpret Results of Analysis

Concepts in Review

IV. Real Estate Investment Securities

A. Real Estate Investment Trusts (REITs)

1. Basic Structure

2. Investing in REITs

B. Other Forms of Real Estate Investment

Concepts in Review

V. Other Tangible Investments

A. Tangibles as Investment Outlets

1. Investment Merits

B. Investing in Tangibles

1. Gold and Other Precious Metals

2. Gemstones

3. Collectibles

Concepts in Review

Web Chapter 18 Real Estate and Other Tangible Investments 329

Summary

Key Terms

Discussion Questions

Problems

Case Problems

18.1 Gary Sofer’s Appraisal of the Wabash Oaks Apartments

18.2 Analyzing Dr. Davis’s Proposed Real Estate Investment

◼ Key Concepts

1. Investing in real estate and setting investment objectives

2. Analysis of important features of real estate investments

3. Determinants of real estate value and the property transfer process

4. Techniques used to estimate market value

5. Considerations and procedures used to perform investment analysis

6. Demonstration of a complete real estate investment analysis of a small apartment building

7. Forms of real estate investment securities, including real estate investment trusts (REITs)

8. The investment characteristics and suitability of gold and other tangible assets, such as silver,

gemstones, and collectibles

◼ Overview

The role of real estate as an investment vehicle and the use of appropriate real estate investment analysis

techniques are the subjects of this chapter.

1. A real estate investor must consider how the investment characteristics of real estate differ and

establish appropriate investment constraints and goals.

2. To meaningfully evaluate the investment potential of real estate, the investor must analyze the

property’s important features. This analysis should include: (1) identification of the physical

property, (2) definition of the applicable property rights, (3) the time horizon for the investment,

and (4) the delineation of a geographic area.

3. The investor should ask a number of questions relative to determining a property’s value. Answering

these questions intelligently requires evaluation of four major determinants of value: demand, supply,

the property, and the property transfer process.

332 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

©2011 Pearson Education, Inc. Publishing as Prentice Hall

(d) Improvements. Improvements—man-made additions to a site—should be accurately measured

and appropriately built in terms of traffic flow and accessibility. Also, amenities, style, and

construction quality are important in determining a property’s competitive edge.

(e) Property management. Investors should find the optimal level of management benefits for a

property at the lowest cost.

7. Real estate markets are not efficient because there is no good system for complete information

exchange among buyers and sellers, and among tenants and lessors. Also, real estate returns are

partially controlled by the property owners themselves. Profits and cash flows depend on how well

8. Market value is the prevailing price of a property, indicating how the market as a whole has assessed

the property’s worth. A real estate appraisal is the estimate of a property’s current market value based

9. The three valuation approaches commonly used by real estate appraisers are:

(1) Cost approach. Value based on the notion that an investor should not pay more for a property

10. Real estate investment analysis considers not only what similar properties have sold for, but also

Web Chapter 18 Real Estate and Other Tangible Investments 337

(b) One financial constraint is the risk-return relationship that is unique to each investor. Another

(c) The investor must decide the relevant time horizon. For a short-term investor, the quick drop in

2–4. Answers will vary according to student choices.

5. (a) Gold coins. Little or no collector value; quality and amount of gold in the coins are most critical

(b) Comparative grid:

Costs

Ease of

Purchase/Sale

Commissions

Potential

Returns

Coins

Fluctuate with

sellers; storage

involved

Relatively

difficult to find

No limit

Uncertain

Stocks

Negotiable

Relatively easy

Depends on size

of trade

Depends on the

price of gold

Futures

Fixed commission

Commodity

exchanges make

it easy

Fixed

Depends on the

price of gold

Certificates

No storage

Very convenient

Depends on size

of trade

Depends on the

price of gold

(c) Certificates would probably be the least risky way to invest in gold. In every case except coins,

(d) Collectives such as coins, stamps, posters, and cars have value because of their attractiveness to

338 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

◼ Solutions to Problems

1.

Alternative

X Y

(I) $7,500 Appreciation

Initial Cash Outlay: $50,000 $50,000 .20 = $10,000

Value after 1 Year: $57,500 $57,500

(II) $7,500 Depreciation

Value after 1 Year: $42,500 $42,500

If the purchase is leveraged, gains are magnified but so are losses. There is obviously more risk

2. (a) Net operating income (NOI) = Gross rental income − Vacancy and collection losses − Property

operating expenses, including property taxes and insurance

(b) Year’s Income-Tax Computation

(1) (2) (3)

NOI $9,000 $9,540 $10,112.40

Web Chapter 18 Real Estate and Other Tangible Investments 339

Year’s After-Tax Cash Flow (ATCF) Computation

(1) (2) (3)

NOI $9,000 $9,540 $10,112.40

3. (a) Original Cost: $200,000 Annual Appreciation: 6%

Year Value

Forecast Sale Price: $252,495.39

Capital Gain

Recaptured Depreciation

(b) (Outstanding Mortgage Balance: $155,000)

4. (a)

3 4 R4 0

12

1 2 3 4

CF CF CF I

CF CF

NPV (1 ) (1 ) (1 ) (1 )r r r r

+−

= + + +

+ + + +

0

I

= $55,000 n = 4 r = 14% = 0.14

1 2 3 4

$6,200 $8,000 $8,300 $8,500 $59,000 $55,000

NPV (1 14) (1 14) (1 14) (1 14)

[$5,439 $6,156 $5,602 $39,965] $55,000

$57,162 $55,000

$2,162

+−

= + + +

+ + + +

= + + + −

=−

=

340 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

(b)

Year 1 Year 2 Year 3 Year 4

(c) At a required rate of return of 14%, the net present value of the expected cash flows would equal

$2,162. Another way of looking at this value is that the present value of the forecast cash flows

◼ Solutions to Case Problems

Case 18.1 Gary Sofer’s Appraisal of the Wabash Oaks Apartments

This case gives the student the opportunity to discuss various factors involved in analyzing a prospective

real estate investment and to apply the analysis to an investment decision.

(a) First, Mr. Sofer must establish and/or assure conformance with his financial and nonfinancial

objectives when pursuing investment property. Second, he must be sure that the Wabash Oaks

Web Chapter 18 Real Estate and Other Tangible Investments 341

(b) Demand relates to the population segment that will rent an apartment in the complex. It relates to the

people who will want and use the facility. Gary must look at the tenants and determine who are the

(c) Gary should be aware that although the owner is probably not criminal or fraudulent, he or she is

trying to sell the apartment and, accordingly, will put his or her best foot forward to make the sale.

(d) Using the NOI from the owner’s income statement, Gary’s estimated capitalization rate of 9.62%,

and the income approach for determining market value, the estimated market value of the Wabash

Oaks Apartments would be:

Annual net operating income (NOI)

Market value (V) Market capitalization rate (R)

NOI $24,330 $18,380 *

$42,710

=

=+

=

*Mortgage payments are not considered an operating expense when calculating NOI.

R 9.62%

NOI $42,710

V $443,971

R .0962

=

= = =

342 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

(e) To answer this question, adjust the owner’s income statement to reflect certain financial expectations.

Estimated rents will be $437.50 per month for one-bedroom units and $525 per month for two-

Reconstructed Income Statement (2007)

Gross Potential Income* $69,300

Less: Vacancy & Collection Losses at 4% 2,772

*[(6 $437.50) + (6 $525)] 12 months

R .0962

If Gary can purchase the apartments for $10,000 less than the original estimated market value, the

Case 18.2 Analyzing Dr. Davis’s Proposed Real Estate Investment

This case provides the student with an opportunity to use quantitative methodology to evaluate a real

estate investment.

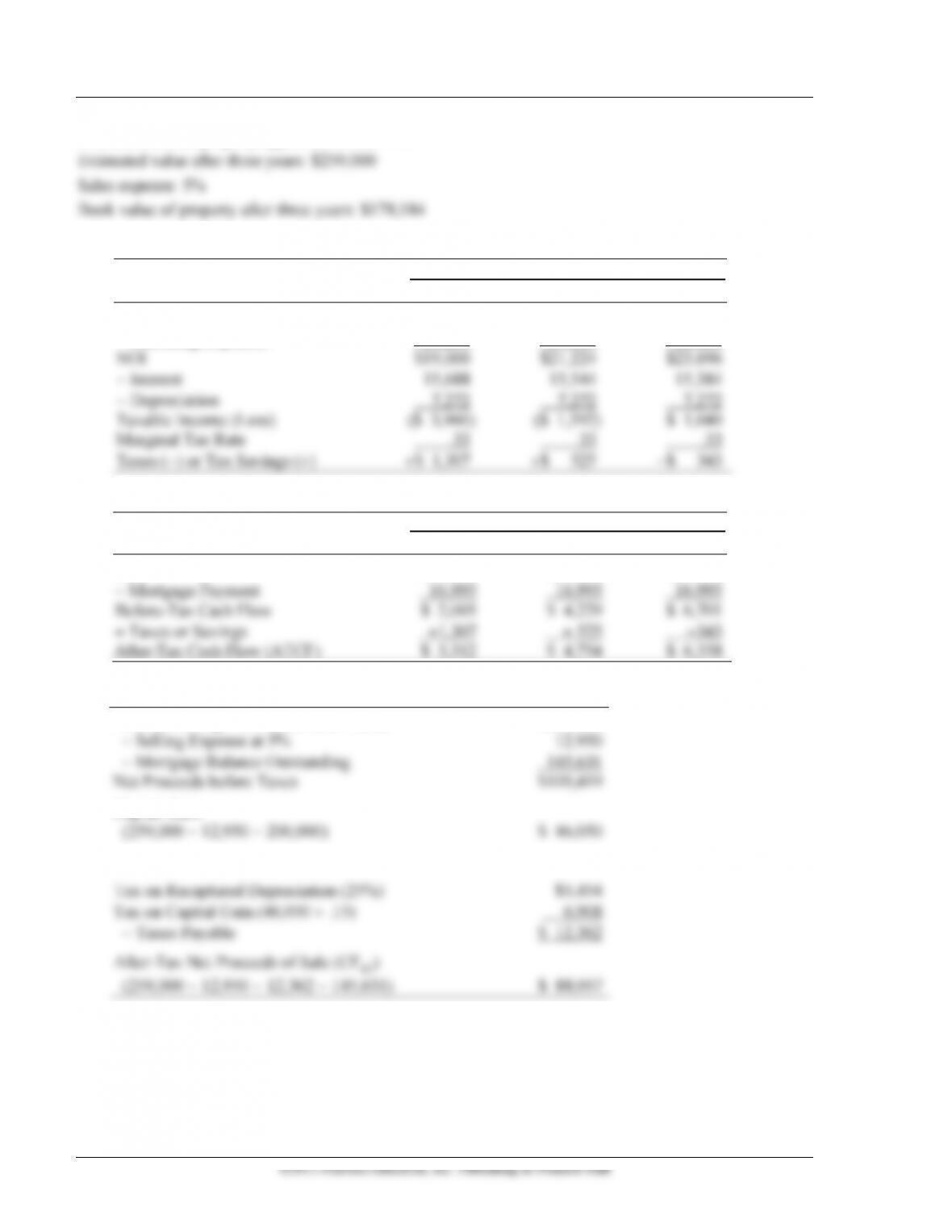

Summary of Key Facts:

Tax bracket: 33%

Web Chapter 18 Real Estate and Other Tangible Investments 343

©2011 Pearson Education, Inc. Publishing as Prentice Hall

Loan balance after three years: $145,631

344 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

Estimated annual property appreciation rate: 9%

(a)

Years

(1) (2) (3)

Gross Rents $35,200 $38,720 $42,592

− Operating Expenses 16,200 17,496 18,896

After-Tax Cash Flows

Years

(1) (2) (3)

NOI $19,000 $21,224 $23,696

After-Tax Net Proceeds from Sale of the Building in Three Years (CFR3)

Forecast Selling Price (Estimated Value) $259,000

Capital Gain

Recaptured Depreciation (7,272 3) $ 21,816

Web Chapter 18 Real Estate and Other Tangible Investments 345

(b)

0

I

= $200,000 − $150,000 = $50,000

3 R3

12

0

1 2 3

1 2 3

CF CF

CF CF

NPV (1 ) (1 ) (1 )

$3,312 $4,754 $6,358 88,057 $50,000

(1 .15) (1 .15) (1 .15)

($2,880 3,595 62,079) $50,000

$18,554

I

r r r

+

= + + −

+ + +

+

= + + −

+ + +

= + + −

=

The net present value is positive, and the investment is therefore acceptable.

(c)

Year 1

Year 2

Year 3

Cash Flow

3,312

4,754

6,358

+ 88,057

= 94,415

The instructor can take the students through an iterative process as described in the book until they

(d) By assuming the existing mortgage, Marilyn would not really increase her return. This financing

would probably work against increasing her rate of return since the 60% greater initial cash outlay

(e) Marilyn has accumulated relevant quantitative data and should be able to establish needed financial

parameters for use in the investment analysis. She also wants to diversify her investment portfolio

and reduce her tax liability. So, to a point, Marilyn has performed a fairly good investment analysis.

346 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

◼ Outside Project

Chapter 18 Analyzing Local Real Estate Demand and Supply

Every day we participate in the economy and acquire information about the world around us. Sometimes

we do not fully appreciate how much valuable knowledge we really possess. The purpose of this project

is to analyze the real estate investment potential of your neighborhood.

The section in this chapter entitled “Determinants of Value” lists demand, supply, the property, and the

property transfer process as important factors in real estate valuation. Since we want to look at the

neighborhood, not a specific piece of property, an analysis of demand and supply is all that you need to

perform. Mortgage information can be obtained from a local mortgage lender such as a savings and loan

or bank. Depending on the size of the city you live in, the Sunday newspaper usually has an extensive

real estate section that includes mortgage information as well as other useful data and comments about

the local real estate market.

As you perform this analysis, follow the questions and comments in the text under “Demand” and “Supply”

and see how well you can do your own analysis based on your knowledge of trends in the area, the people

who live there, and what you observe about the desirability of real estate investment. Comment on the real

estate investment outlook in the area. You may want to augment your analysis with information available

from the local chamber of commerce or economic development agency.