Chapter 13

Managing Your Own Portfolio

◼ Outline

Learning Goals

I. Constructing a Portfolio Using an Asset Allocation Scheme

A. Investor Characteristics and Objectives

B. Portfolio Objectives and Policies

C. Developing an Asset Allocation Scheme

1. Approaches to Asset Allocation

a. Fixed Weightings

b. Flexible Weightings

c. Tactical Asset Allocation

2. Asset Allocation Alternatives

3. Applying Asset Allocation

Concepts in Review

II. Evaluating the Performance of Individual Investments

A. Obtaining Needed Data

1. Return Data

2. Economic and Market Activity

B. Indexes of Investment Performance

C. Measuring the Performance of Investments

1. Stocks and Bonds

a. Stocks

b. Bonds

2. Mutual Funds

3. Options and Futures

D. Comparing Performance to Investment Goals

1. Balancing Risk and Return

2. Isolating Problem Investments

Concepts in Review

250 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

III. Assessing Portfolio Performance

A. Measuring Portfolio Return

1. Measuring the Amount Invested

2. Measuring Income

3. Measuring Capital Gains

4. Measuring the Portfolio’s Holding Period Return

B. Comparison of Return with Overall Market Measures

1. Sharpe’s Measure

2. Treynor’s Measure

3. Jensen’s Measure (Jensen’s Alpha)

C. Portfolio Revision

Concepts in Review

IV. Timing Transactions

A. Formula Plans

1. Dollar Cost Averaging

2. Constant-Dollar Plan

3. Constant-Ratio Plan

4. Variable-Ratio Plan

B. Using Limit and Stop-Loss Orders

1. Limit Orders

2. Stop-Loss Orders

C. Warehousing Liquidity

D. Timing Investment Sales

1. Tax Consequences

2. Achieving Investment Goals

Concepts in Review

Summary

Key Terms

Discussion Questions

Problems

Case Problems

13.1 Assessing the Stalchecks’ Portfolio Performance

13.2 Evaluating Formula Plans: Charles Spurge’s Approach

Excel with Spreadsheets

Chapter 13 Managing Your Own Portfolio 251

◼ Key Concepts

1. The role of investor characteristics and objectives and portfolio objectives in planning and building

a portfolio

2. Procedure for building a portfolio using an asset allocation scheme that considers investor

characteristics and objectives as inputs to the establishment of portfolio objectives and policies

3. Obtaining needed data, indexes of investment performance, and techniques for measuring the

performance of investments

4. The methods used to compare investment performance to investment goals

5. The techniques used to measure the amount invested, current income, capital gains, and total

portfolio return relative to the amount of money actually invested in the portfolio

6. Statistical measures and uses of portfolio return—Sharpe’s, Treynor’s, and Jensen’s measures—and

the importance of portfolio revision

7. The role of common types of formula plans in timing purchase and sale decisions

8. The use of limit and stop-loss orders in investment timing, the warehousing of liquidity, and the key

factors in timing investment sales in order to achieve maximum benefits

◼ Overview

This chapter describes how investment portfolios are constructed and monitored, including procedures for

evaluating investment performance and timing portfolio transactions.

1. The first section of the chapter provides basic guidelines for building a portfolio using an asset

allocation scheme. In addition to portfolio objectives, an individual’s level and stability of income,

family factors, net worth, experience and age, and disposition toward risk are key factors to consider

during portfolio construction. The instructor should mention that tax and liquidity considerations

should also be taken into account when constructing a portfolio. The logic as well as general

procedures involved in developing an asset allocation scheme consistent with the investor’s needs are

demonstrated. All these discussions focus on the chapter’s key idea: the individual investor should

assemble a portfolio that will yield maximum expected returns commensurate with the level of risk

he or she is willing to assume.

2. The evaluation of an individual investment’s performance is discussed. Such performance may be

measured by comparing an investment’s return against a standard. Two such standards might involve

comparing actual with anticipated returns or comparing an actual return against the return of another

vehicle of a similar type. The text stresses the need for a broad range of data to assess performance

accurately.

3. Investment performance also may be measured by computing and comparing holding period returns

(HPR) before and after tax. The instructor might work out HPRs for different investments such as

stocks, bonds, mutual funds, or real estate. It should be emphasized that the comparison of HPRs

must be accompanied by the consideration of the associated risk. Riskier investments should provide

higher returns than low-risk investments to compensate for the greater risk involved.

256 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

(c) Jensen’s measure, also called alpha, uses portfolio beta and the capital asset pricing model

(CAPM) to calculate the excess return—the difference between the actual return and the required

18. Jensen’s measure is similar to Treynor’s measure; both focus only on nondiversifiable risk by using

19. When an investor decides to change the composition of a portfolio by selling some securities and

replacing them with others, he or she is engaging in portfolio revision. Periodically, the investor must

20. Formula plans are mechanical methods of portfolio management that try to take advantage of price

21. (a) The dollar cost averaging plan involves investing a fixed dollar amount in a security at fixed

(b) A constant-dollar plan uses a two-part portfolio. The speculative portion is invested in securities

having high promise of capital gain. The conservative portion consists of low-risk investments

Chapter 13 Managing Your Own Portfolio 257

(c) The constant-ratio plan establishes a desired fixed ratio of the speculative to the conservative

(d) The variable-ratio plan is a more aggressive strategy. The target ratio between the speculative

portion and the conservative portion of the portfolio is varied by the investor and depends on the

22. A limit order can be used to specify the investor’s minimum sell price or the maximum price the

investor will pay to buy the security. The stop-loss order is a type of suspended order that requests

23. The first reason investors should maintain some funds in a low-risk, highly liquid investment is

simply to protect against the chance of a total loss. Thus, a low-risk investment acts as a buffer

against possible investment adversity.

24. The two considerations in timing investment sales are tax consequences and compatibility with

investment goals. When there is a capital loss, the investor receives the benefit of a tax deduction. In

◼ Suggested Answers to “Ethics in Investing” Questions

Virtues of Ethical Investing: The Remarkable Life of John Templeton

Suggestion:

258 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

◼ Suggested Answers to Discussion Questions

◼ Solutions to Problems

1. Investor A would more likely be the retired couple because they would want to have low risk.

3. Capital gain = $2,500 – $1,762 = $738

Dividend Capital gain

HPR Purchase price

$200 $738 53.24% (for a 15-month holding period)

$1,762

+

=

+

==

4.

A

Cost

B

Proceeds

B–A

Profit

Trading

Cost

Profit

after Costs

$2,000

$9,500

$7,500

$20

$7,480

HPR = $7,480/$2,000

374%

Annualized (12/6)

748%

5. HPR (before tax) =

$2,000 ($26,746 $25,000)

$25,000

+−

= 14.98% (13-month holding period)

Tax Calculations

1.

Interest

$2,000

2.

After tax (1 − .31)

$1,380

3.

Capital gain

$1,746

4.

After tax (1 − .15)

$1,484

5.

After-tax income [(2) + (4)]

$2,864

Therefore, HPR (after-tax) =

$2,864 11.46%*

$25,000 =

For a 13-month holding period

©2011 Pearson Education, Inc. Publishing as Prentice Hall

11. (a) Sharpe’s measure

Total portfolio return Risk-free rate

(SM) Portfolio standard deviation

11.8 6.2 .397

14.1

pF

p

rR

s

−

−

==

−

==

12. Treynor’s measure for the portfolio = (12.0 – 6.0)/1.3 = 4.62

13. (a) Treynor’s measure

Total portfolio return Risk-free rate

(TM) Portfolio beta

8.6 7.3 1.44

90

pF

p

rR

b

−

−

==

−

==

15. (a) Jensen’s measure (JM) = [(Total portfolio return − Risk-free rate) −

Portfolio beta (Market return − Risk-free rate)]

(b) Chee’s portfolio, with a JM of + .94, outperformed Carri’s portfolio, with a JM of −0.24. A

Chapter 13 Managing Your Own Portfolio 263

HPR for options:

($29,000 $26,000)

$26,000

−

(b) After-tax HPRs:

Stock (400 shares), reduced rate on dividends:

Industrial bonds (eight bonds):

Mutual fund (500 shares), reduced rate on dividend and capital gain distributions:

Options:

(c) Total investment = ($17.25 400) + ($970 8) + ($19.45 500) + $26,000

Total current income = ($.90 400) + ($92.50 8) + ($1.10 500) + $0

Total capital gain = ($1.50 400) + (−$6.25 8) + ($.57 500) + $3,000

$50,385

(d) JM = (rp – RF) – [bp (rm – RF)]

Using Jensen’s measure, the actual portfolio return is better than the required return because it is

(e) This question should lead to discussion—it has no pat answer. In general, the portfolio is balanced

between current income and growth. The ratio of current income to capital gain is 43 ($1,650/$3,835);

Chapter 13 Managing Your Own Portfolio 265

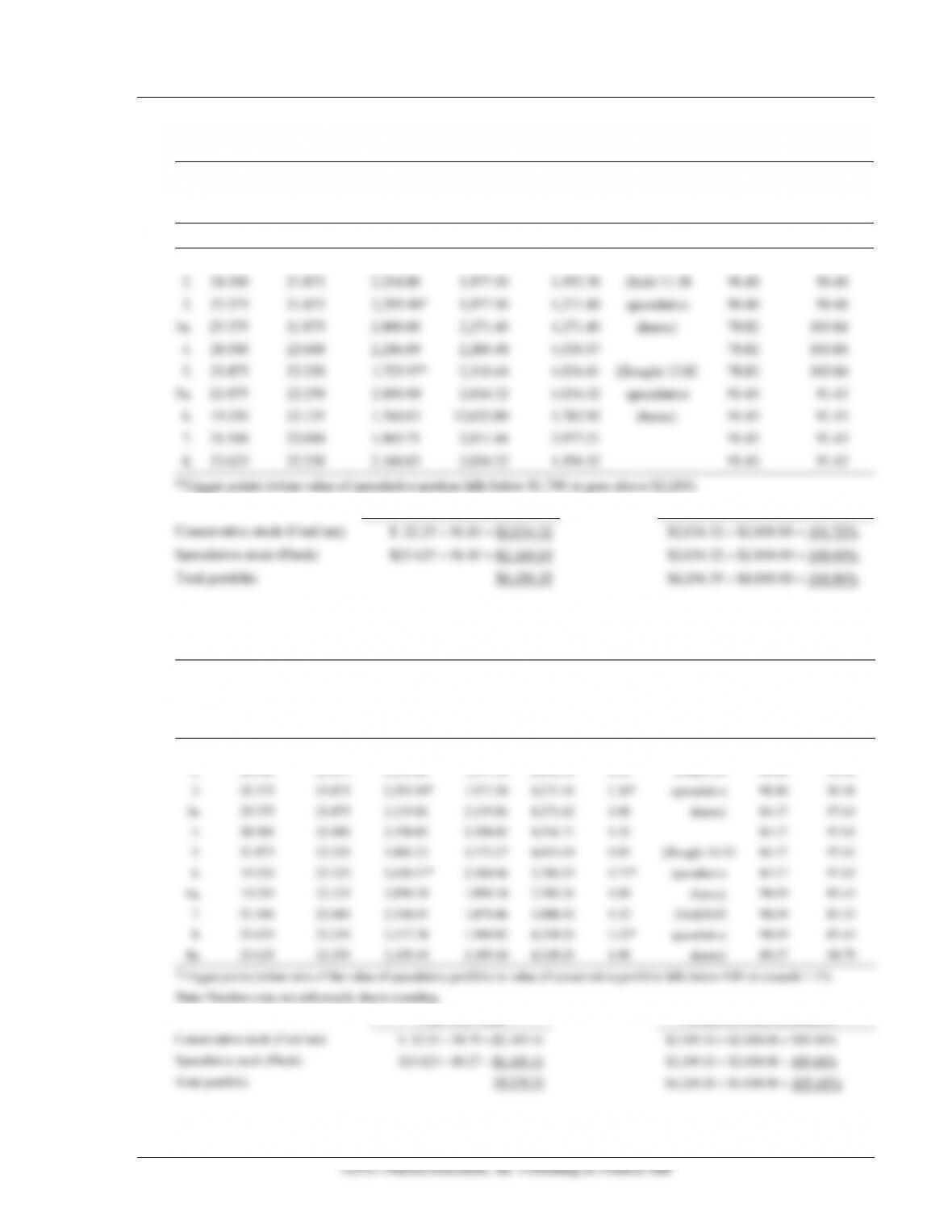

(b) Constant-dollar plan: return speculative value (Fleck) to $2,000 when trigger points are reached.

Price of

Speculative

Stock

Price of

Conservative

Stock

Value of

Speculative

Stock

Value of

Conservative

Stock

Total

Value

Transactions

Shares in

Speculative

Shares in

Conservative

Fleck

ConCam

Fleck

ConCam

1. 22.125

22.125

$2,000.00

$2,000.00

$4,000.00

90.40

90.40

2. 24.500

21.875

2,214.80

1,977.50

4,192.30

{Sold 11.58

90.40

90.40

3. 25.375

21.875

2,293.90*

1,977.50

4,271.40

speculative

90.40

90.40

3a. 25.375

21.875

2,000.00

2,271.40

4,271.40

shares}

78.82

103.84

4. 28.500

22.000

2,246.09

2,284.48

4,530.57

78.82

103.84

5. 21.875

22.250

1,723.97*

2,310.44

4,034.41

{Bought 12.82

78.82

103.84

5a. 21.875

22.250

2,000.00

2,034.32

4,034.32

speculative

91.43

91.43

6. 19.250

22.125

1,760.03

12,022.89

3,782.92

shares}

91.43

91.43

7. 21.500

22.000

1,965.75

2,011.46

3,977.21

91.43

91.43

8. 23.625

22.250

2,160.03

2,034.32

4,194.35

91.43

91.43

*Trigger points (when value of speculative portion falls below $1,740 or goes above $2,260)

Year-End Value

Percent of Initial Investment

Conservative stock (ConCam)

$ 22.25 91.43 = $2,034.32

$2,034.32 $2,000.00 = 101.72%

Speculative stock (Fleck)

$23.625 91.43 = $2,160.03

$2,034.32 $2,000.00 = 108.00%

Total portfolio

$4,194.35

$4,194.35 $4,000.00 = 104.86%

(c) Constant ratio plan: rebalance to value of speculative portion equal to value of conservative portion

when ratio hits trigger point.

Period

Price of

Speculative

Stock

Price of

Conservative

Stock

Value of

Speculative

Stock

Value of

Conservative

Stock

Total

Value

Ratio of

Speculative

Stock to

Conservative

Stock

Transactions

Shares in

Speculative

Shares in

Conservative

1.

22.125

22.125

$2,000.00

$2,000.00

$4,000.00

1.00

90.40

90.40

2.

24.500

21.875

2,214.80

1,977.50

4,192.30

1.12

{Sold 6.23

90.40

90.40

3.

25.375

21.875

2,293.90*

1,977.50

4,271.40

1.16*

speculative

90.40

90.40

3a.

25.375

21.875

2,135.81

2,135.81

4,271.62

1.00

shares}

84.17

97.63

4.

28.500

22.000

2,398.85

2,398.85

4,546.71

1.12

84.17

97.63

5.

21.875

22.250

1,841.22

2,172.27

4,013.49

0.85

{Bought 14.02

84.17

97.63

6.

19.250

22.125

1,620.27*

2,160.06

3,780.33

0.75*

speculative

84.17

97.63

6a.

19.250

22.125

1,890.18

1,890.18

3,780.36

1.00

shares}

98.09

85.43

7.

21.500

22.000

2,108.94

1,879.46

3,988.40

1.12

{Sold 8.82

98.09

85.43

8.

23.625

22.250

2,317.38

1,900.82

4,218.20

1.22*

speculative

98.09

85.43

8a.

23.625

22.250

2,109.10

2,109.10

4,218.20

1.00

shares}

89.27

94.79

*Trigger points (when ratio of the value of speculative portfolio to value of conservative portfolio falls below 0.84 or exceeds 1.15)

Note: Numbers may not add exactly due to rounding.

Year-End Value

Percent of Initial Investment

Conservative stock (ConCam)

$ 22.25 94.79 = $2,109.10

$2,109.10 $2,000.00 = 105.46%

Speculative stock (Fleck)

$23.625 89.27 = $2,109.10

$2,109.10 $2,000.00 = 105.46%

Total portfolio

$4,218.20

$4,218.20 $4,000.00 = 105.46%

266 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

(d) Variable-ratio plan: rebalance speculative portion to 46% of the total portfolio value each time the

upper trigger point is reached; rebalance speculative portion to 50% each time the lower trigger point

is reached.

Period

Price of

Speculative

Stock

Price of

Conservative

Stock

Value of

Speculative

Stock

Value of

Conservative

Stock

Total

Portfolio

Value

Ratio

Transactions

Shares in

Speculative

Shares in

Conservative

1.

22.125

22.125

$2,000.00

$2,000.00

$4,000.00

0.50

90.40

90.40

2.

24.500

21.875

2,214.80

1,977.50

4,192.30

0.53

{Sold 16.72

90.40

90.40

3.

25.375

21.875

2,293.90

1,977.50

4,271.40

0.54

speculative

90.40

90.40

4.

28.500

22.000

2,576.40

1,988.80

4,656.20

0.56*

shares}

90.40

90.40

4a.

28.500

22.000

2,099.99

2,415.21

4,564.20

0.46

73.68

112.06

5.

21.875

22.250

1,611.75

2,493.34

4,105.09

0.39

{Bought 29.43

73.68

112.06

6.

19.250

22.125

1,418.34

2,479.33

3,897.67

0.36*

speculative

73.68

112.06

6a.

19.250

22.125

1,948.84

1,948.83

3,897.67

0.50

shares}

103.11

88.08

7.

21.500

22.000

2,216.87

1,937.76

4,164.63

0.53

{Sold 17.52

103.11

88.08

8.

23.625

22.250

2,435.97

1,959.78

4,395.75

0.55*

speculative

103.11

88.08

8a.

23.625

22.250

2,022.05

2,373.70

4,395.75

0.46

shares}

85.59

106.68

*Trigger points (when ratio of the value of speculative portfolio to the total portfolio value either exceeds 54%, the upper trigger point, or

falls below 38%, the lower trigger point).

Year-End Value

Percent of Initial Investment

Conservative stock (ConCam)

$22.25 106.68 = $2,373.70

$2,373.70 $2,000.00 = 118.69%

Speculative stock (Fleck)

$23.625 85.59 = $2,022.05

$2,022.05 $2,000.00 = 101.10%

Total portfolio

$4,395.75

$4,395.75 $4,000.00 = 109.89%

(e) Formula plan:

Dollar Cost

Averaging

Constant

Dollar

Constant

Ratio

Variable

Ratio

Year-End Portfolio

Value as a Percentage

of $4,000 Invested

101.67%

104.86%

105.46%

109.89%

Number of Transactions

to Rebalance Portfolio

0

2

3

3

In this illustration, the formula plans have performed much the way one would expect. The most

passive and lowest-risk plan—dollar cost averaging—has the lowest year-end value as a percentage

Chapter 13 Managing Your Own Portfolio 267

◼ Answers to CFA Questions (Part V)

1. a

◼ Outside Project

Chapter 13 Assessing Mutual Fund Performance

When risk-adjusted, market-adjusted rate of returns such as Jensen’s measure are not easy to calculate,

other comparisons need to be made. For instance, it is generally difficult to find the beta values of various

mutual funds; therefore, Jensen’s measure is not a useful measure. Instead, performance can be evaluated

by comparing the HPRs of similar funds that are assumed to have similar risk characteristics. This project

asks you to do just that.

Use The Wall Street Journal, Barron’s, or some other source to obtain thorough, readable information on

mutual funds. Obtain this information dated one year earlier, and select five similar funds managed by

different fund management companies. Calculate the holding period return (HPR) for each fund over the

period from a year ago to the present. Barron’s and other sources provide the dividend and capital gains

distributions for the period. If investment performance is considerably different among the funds, you may

want to further investigate their managements through such sources as Weisenberger Investment

Companies, which should be available in your public or university library. Try to assess the risk and return

behaviors of these funds, and use these comparisons to explain any differences you found in their HPRs.