Chapter 12 Mutual Funds: Professionally Managed Portfolios 239

Advantages of buying CEFs include the enhanced dividend yield arising from investing less than full

6. Answers will vary with each student.

◼ Solutions to Problems

1. (a) Return for the year (all changes on a per share basis):

Change in price ($9.10 − $8.50) $ .60

(b) When all dividends and capital gains distributions are reinvested into additional shares of the

fund ($8.75/share):

Dividends and capital gains per share: $.90 + $.75 = $1.65

Thus, the holding period return would be:

$2,163 $1,700 $463

HPR 27.24%

$1,700 $1,700

−

= = =

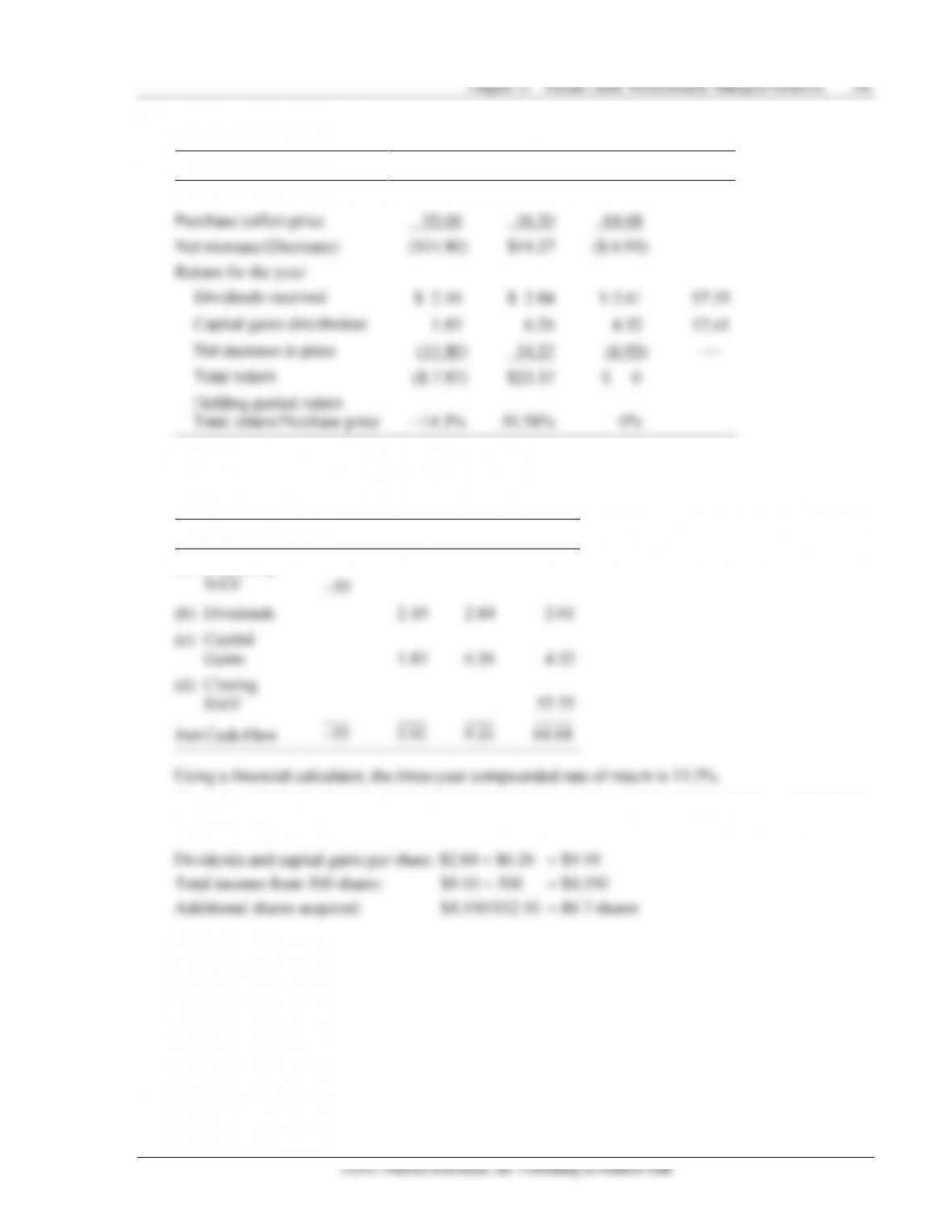

2.

Purchase (offer) price—beginning of year

$23.35

Current price (NAV) end of year

23.04

Decrease

($ .31)

Return for the year:

Dividend and gains distribution

$ 1.05

Loss in value

.31)

Total return

$ .74

Note: The holding period return is 3.12%. This is a good problem to demonstrate the impact of load

242 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

(Number of shares (Number of shares

Ending price) Beginning price)

HPR (Number of shares Initial price)

(586.7 $60.47) (500 $46.20)

500 $46.20

$35,477.75 $23,100.00

$23,100.00

$12,377.75 53.6

$23,100.00

−

=

−

=

−

=

==%

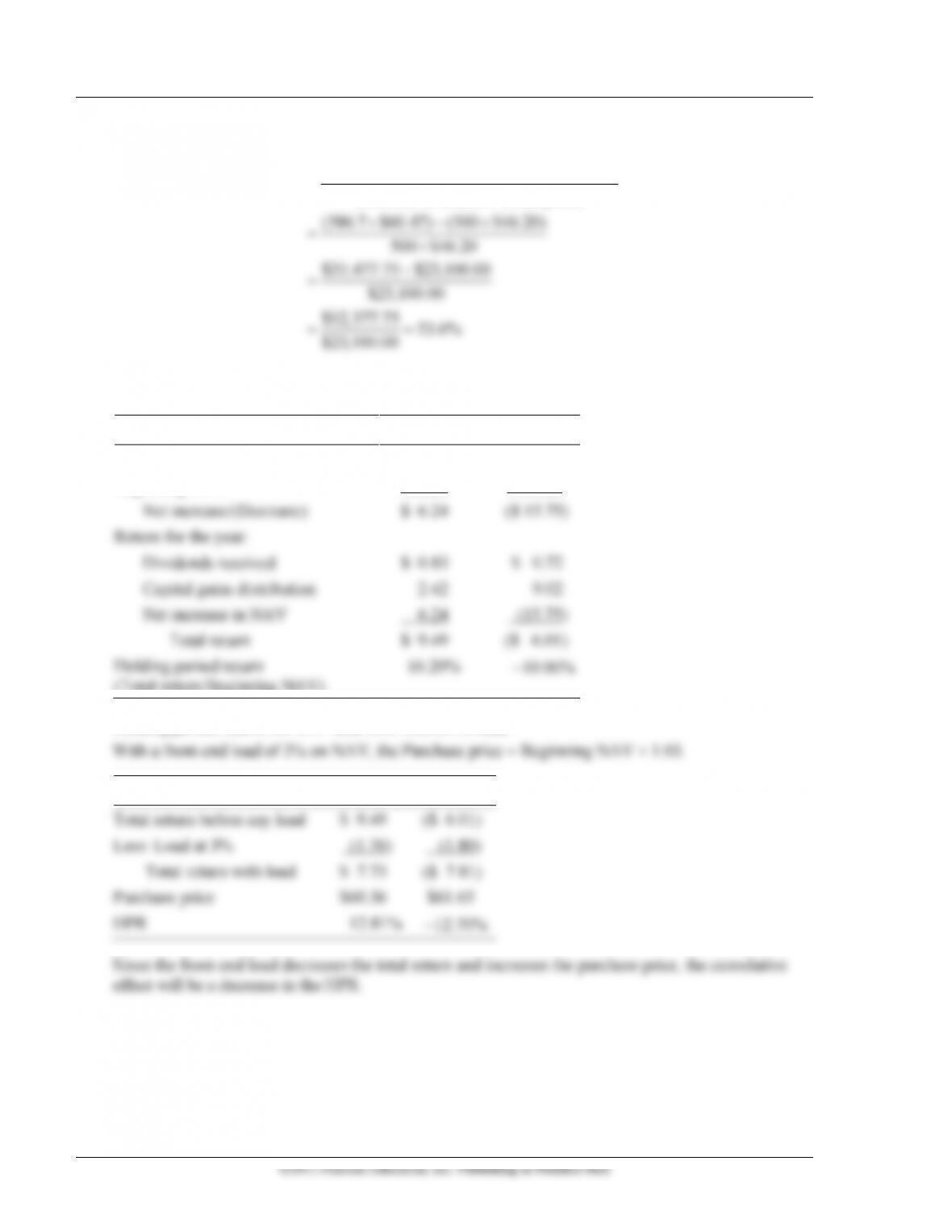

5. Holding period returns for 2011 and 2008:

2011

2008

Ending NAV

$64.84

$ 44.10

Beginning NAV

58.60

59.85

Net increase/(Decrease)

$ 6.24

($ 15.75)

Return for the year:

Dividends received

$ 0.83

$ 0.72

Capital gains distribution

2.42

9.02

Net increase in NAV

6.24

(15.75)

Total return

$ 9.49

($ 6.01)

Holding period return

(Total return/Beginning NAV)

16.20%

−10.00%

Holding period returns for 2011 and 2008 with a 3% load:

2011

2008

Total return before any load

$ 9.49

($ 6.01)

Less: Load at 3%

(1.76)

(1.80)

Total return with load

$ 7.73

($ 7.81)

Purchase price

$60.36

$61.65

HPR

12.81%

−12.70%

Since the front-end load decreases the total return and increases the purchase price, the cumulative

effect will be a decrease in the HPR.

Chapter 12 Mutual Funds: Professionally Managed Portfolios 243

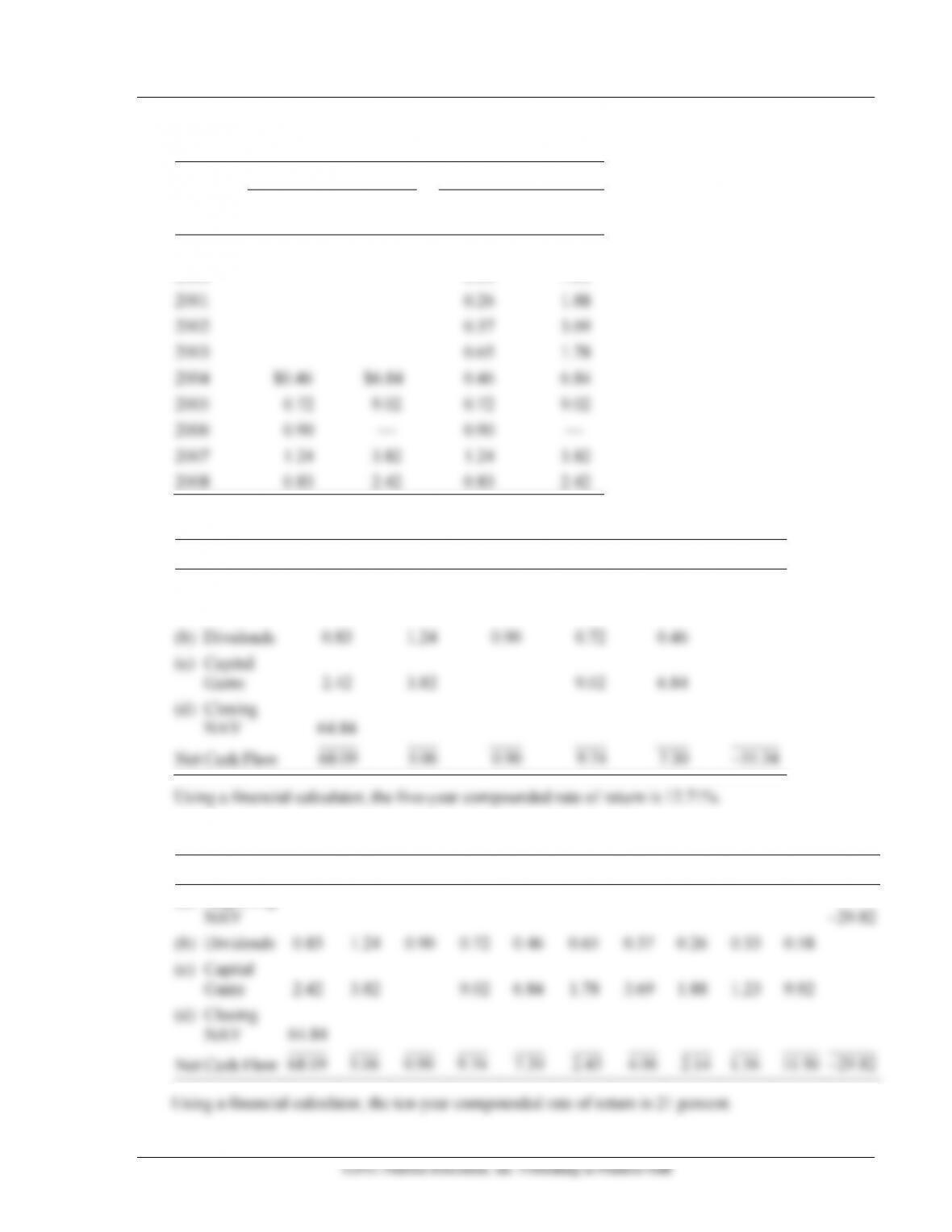

Average annual rate of return over the two periods:

2007–2011

2002–2011

Dividends

Capital

Gains

Dividends

Capital

Gains

1999

$0.58

$9.92

2000

0.33

1.23

2001

0.26

1.88

2002

0.37

3.69

2003

0.65

1.78

2004

$0.46

$6.84

0.46

6.84

2005

0.72

9.02

0.72

9.02

2006

0.90

—

0.90

—

2007

1.24

3.82

1.24

3.82

2008

0.83

2.42

0.83

2.42

Compounded Return for the Five-Year Period with Loading

2011

2010

2009

2008

2007

2006

(a) Beginning

NAV

−55.34

(b) Dividends

0.83

1.24

0.90

0.72

0.46

(c) Capital

Gains

2.42

3.82

9.02

6.84

(d) Closing

NAV

64.84

Net Cash Flow

68.09

5.06

0.90

9.74

7.30

55.34−

Using a financial calculator, the five-year compounded rate of return is 12.71%.

Compounded Return for the Ten-Year Period with Loading

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

(a) Beginning

NAV

−29.82

(b) Dividends

0.83

1.24

0.90

0.72

0.46

0.65

0.37

0.26

0.33

0.58

(c) Capital

Gains

2.42

3.82

9.02

6.84

1.78

3.69

1.88

1.23

9.92

(d) Closing

NAV

64.84

Net Cash Flow

68.09

5.06

0.90

9.74

7.30

2.43

4.06

2.14

1.56

10.50

29.82−

Using a financial calculator, the ten-year compounded rate of return is 21 percent.

244 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

If the fund charges a 3% load on NAV, the beginning price would be different and that would change

the yield:

Compounded Return for the Five-Year Period with Loading

2011

2010

2009

2008

2007

2006

(a) Beginning

NAV

−57

(b) Dividends

0.83

1.24

0.90

0.72

0.46

(c) Capital

Gains

2.42

3.82

9.02

6.84

(d) Closing

NAV

64.84

Net Cash Flow

68.09

5.06

0.90

9.74

7.30

57−

Using a financial calculator, the five-year compounded rate of return is 11.9%.

Compounded Return for the Ten-Year Period with Loading

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

(a) Beginning

NAV

−30.71

(b) Dividends

0.83

1.24

0.90

0.72

0.46

0.65

0.37

0.26

0.33

0.58

(c) Capital

Gains

2.42

3.82

9.02

6.84

1.78

3.69

1.88

1.23

9.92

(d) Closing

NAV

64.84

Net Cash Flow

68.09

5.06

0.90

9.74

7.30

2.43

4.06

2.14

1.56

10.50

30.71−

Using a financial calculator, the ten-year compounded rate of return is 20.4%.

6. There is no set solution to this problem since the answers will vary with the funds selected by the

student. There are many funds that the student can choose from to answer this question. The

248 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

(c) Reverend Mark Thomas’s specific investment needs are retirement and college education for his

child. Both objectives favor a conservative growth fund or a growth-and-income fund. A good

Case 12.2 Calvin Jacobs Seeks the Good Life

In contrast to the previous case, in which the investor was interested in long-term wealth accumulation,

this case illustrates a situation in which current income is the primary objective.

(a) Given Calvin’s existing financial condition, he can take on a certain amount of risk. Also, Calvin

wants to consume immediately. In that sense, an income fund seems attractive. He could obviously

(c) Calvin is clearly not in need of any savings plan. He already has a considerable amount of savings

and is able to manage things well on his own. What Calvin needs is a withdrawal plan because he

Chapter 12 Mutual Funds: Professionally Managed Portfolios 249

(d) Fund earns 12%. Starting balance is $100,000. At the end of the first year, this would be

Year

Initial

Sum

Ending

Sum

Less Annual

Withdrawal

Balance

End of Year

1

$100,000 1.10

=

110,000

−

$15,000

=

$95,000

2

95,000 1.10

=

104,500

−

$15,000

=

89,500

3

91,400 1.10

=

98,450

−

$15,000

=

83,450

4

83,450 1.10

=

91,795

−

$15,000

=

76,795

5

76,795 1.10

=

84,474

−

$15,000

=

69,474

Thus, at a 10% earning rate, the value of his $100,000 investment will steadily decline to $69,474 by

the end of the fifth year. The reason for this is simple: he’s taking out more than he’s earning. This

◼ Answer to Chapter Opening Problem

Answers will vary depending on when students solve it.

◼ Outside Project

Chapter 12 The Other Kind of Investment Company

The most popular form of investment company is the open-end mutual fund. But the closed-end company

also holds a place in the market for professionally managed investment companies. This project will help

you understand the difference between open-end mutual funds and closed-end investment companies.

From the list of closed-end companies given in the text, select a diversified stock fund and a bond fund; in

addition, find two open-end mutual funds that have roughly the same investment objectives. You can find

information on fund objectives, etc. in Weisenberger Investment Companies or any other similar

investment company’s services. Now compare the four funds by looking at the following features:

(a) Management fee charged

(b) How long the fund has existed

(c) Size of the fund or amount of dollars under management

250 Gitman/Joehnk/Smart • Fundamentals of Investing, Eleventh Edition

(d) Financing of the fund—does it issue debt to employ leverage?

(e) Dividend and capital gains distributions for the last three to five years

(f) The approximate yield for the last three years

(g) Load charges

Comment on your findings. Do you think open- and closed-end companies really behave all that

differently? In the final analysis, what’s the most important thing in determining the amount of

investment success (or failure) achieved by open- and closed-end funds?