CHAPTER 10

USING FINANCIAL STATEMENT ANALYSIS TO

EVALUATE FIRM PERFORMANCE

CHAPTER OVERVIEW

The chapter begins with a closer look at the income statement. Specifically, the discussion

centers on separately reported items on the income statement, including discontinued operations

and extraordinary items. The definition and accounting treatment for each of these items is

briefly covered.

The next part of the chapter presents analysis of financial information. Horizontal analysis and

vertical analysis is explained. Finally, ratio analysis is discussed. All of the ratios presented in

previous chapters are reviewed and segregated into liquidity ratios, solvency ratios, and

profitability ratios. Two new market indicator ratios are introduced (price-earnings ratio and

dividend-yield ratio) and explained. A full ratio analysis is then presented.

LEARNING OBJECTIVES

After completing Chapter 10, your students should be able to answer these questions:

1. Recognize and explain the components of net income.

2. Perform and interpret a horizontal analysis and a vertical analysis of financial

statement information.

3. Perform a basic ratio analysis of a set of financial statements and explain what the

ratios mean.

4. Recognize the risks of investing in stock and explain how to control those risks.

CHAPTER OUTLINE

Closer Look at the Income Statement (LO 1)

I. Earnings (net income) are the focus of financial reporting.

a. Not uncommon for firms to be accused of manipulating their earnings

b. GAAP defines two items that need to be separated from regular earnings of a

business:

i. Discontinued operations

ii. Extraordinary items

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 10-1

II. Discontinued operations are those parts of the firm that a company has eliminated by

selling a division.

a. Financial implications related to that segment are separated from the regular

operations of the firm.

i. Net income is used to evaluate the performance of a company and to predict

future performance.

ii. To make evaluations meaningful, one-time occurrences are separated out.

b. Financial implications of discontinuing a business segment are reported separately.

i. Gain or loss on disposal

ii. Earnings or loss of the segment for the accounting period

Teaching Tip

Use the example on pages 462-3 to illustrate the separate reporting of discontinued operations.

III. Extraordinary items are events that are unusual in nature and infrequent in occurrence.

a. Examples:

i. Eruption of a volcano

ii. Takeover of foreign operations by the foreign government

iii. Effects of new laws or regulations that result in a one-time cost for

compliance

b. Each situation is unique and must be considered in the environment in which the

company operates.

Teaching Tip

Explain how situations must be considered within the context of the company’s environment. For

example, in 2005 Hurricane Katrina caused considerable damage to property in Louisiana and

Mississippi. The loss incurred by companies located along the coast of Louisiana and Mississippi

would not be extraordinary because it was not unusual or infrequent. However, loss incurred by

companies located in Vicksburg, Mississippi (200 miles away from the coast) might be

extraordinary because hurricane damage in Vicksburg is both unusual and infrequent.

Teaching Tip

Use the example on page 463 to illustrate the separate reporting of extraordinary items.

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 10-2

Teaching Tip

The issues surrounding the classification of an item as “extraordinary” came under scrutiny

following the terrorist attacks of September 11, 2001. Although accounting issues are trivial

compared to the human factors involved in these tragic events, an interesting debate arose.

Clearly, those businesses located in the World Trade Center suffered extraordinary losses (to the

extent that they did not have business interruption insurance). What about the businesses that

were not directly affected by the damage to structures? For example, the tourism industry ground

to a halt for a substantial period after the attacks. Should hotels, restaurants, theater companies,

airlines, travel agents, resorts in the Caribbean, etc., have been allowed to estimate the losses

they suffered as a result of September 11 and report them as extraordinary?

Teaching Tip

Have students give you examples of items they believe would be classified as extraordinary

losses. Use examples like earthquakes in California and tornadoes in Kansas to demonstrate

when natural disasters are not classified as extraordinary as it does not meet the infrequent and

unusual test.

Horizontal and Vertical Analysis of Financial Information (LO 2)

I. Horizontal analysis is a technique for evaluating financial statement amounts across

time.

a. Purpose is to express the change in an item in percentages, based on a specific past

year chosen as the base year

Teaching Tip

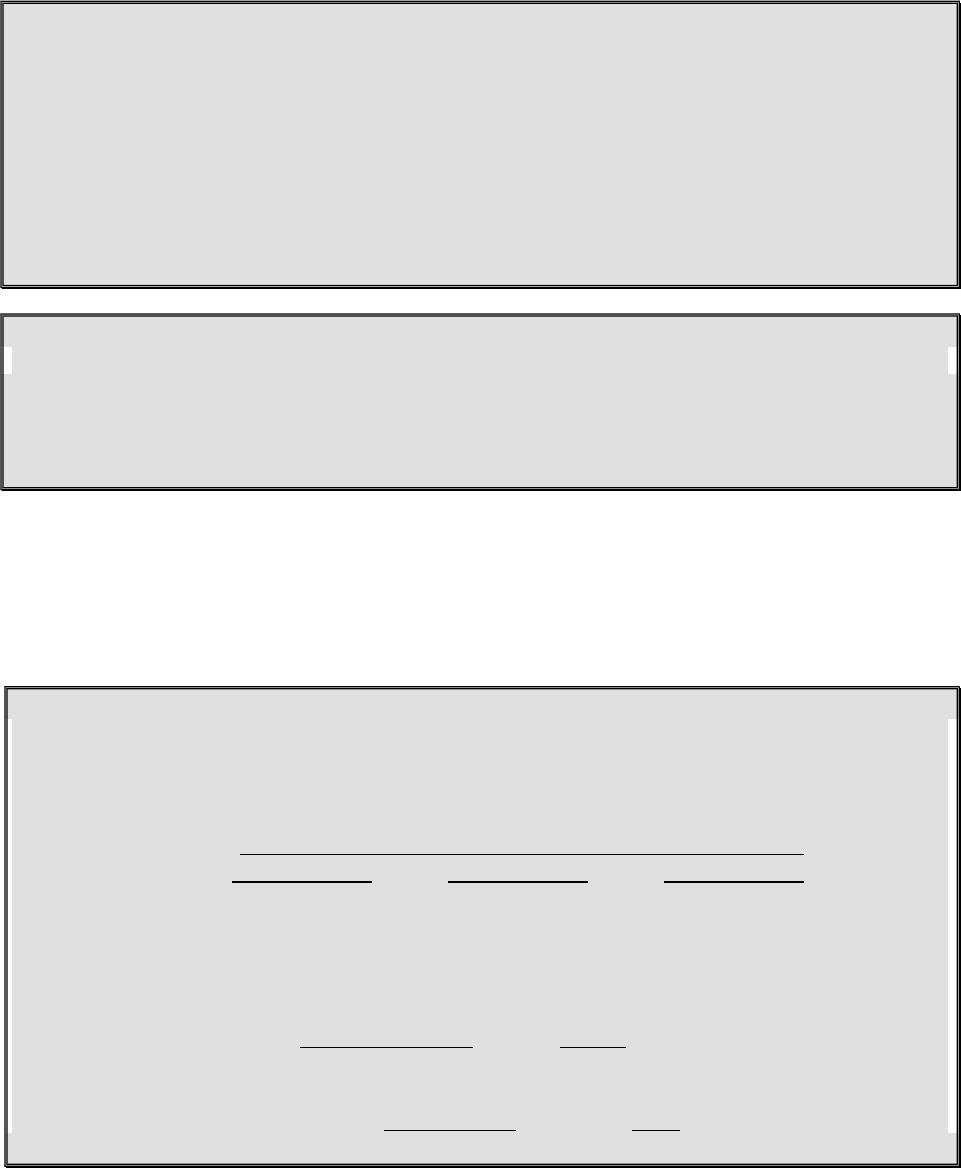

PepsiCo. Inc. reported the following information (in millions) for the years ended December 31,

20X3, 20X2, and 20X1.

For the Years Ending

Dec. 31, 20X3 Dec. 31, 20X2 Dec. 31, 20X1

Sales $26,971 $25,112 $23,512

Net Income 3,568 3,000 2,400

Compute percentage changes for Sales and Net Income for 20X3.

% change in Sales = $26,971 – 25,112 = $1,859 = 7.4% increase

$25,112 $25,112

% change in Net income = $3,568 – 3,000 = $568 = 18.9% increase

$3,000 $3,000

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 10-3

Vertical analysis is a technique for comparing items in a financial statement in which all items

are expressed as a percent of a common amount.

b. Similar to horizontal analysis, but involves items on a financial statement for a single

year

c. Common-sizing involves converting all amounts on a financial statement to a

percentage of a chosen value on that statement, also known as vertical analysis.

d. Each item in the financial statement is expressed as a percentage of a selected item on

the statement.

i. Sales are the common amount or base for income statement items.

ii. Total assets are the common amount or base for balance sheet items.

Teaching Tip

Common size statements are simply vertical analysis statements presented without the

percentage signs and with no dollar amounts provided. Common-size analysis is helpful when

comparing different size companies, because all amounts are stated in percentages.

Teaching Tip

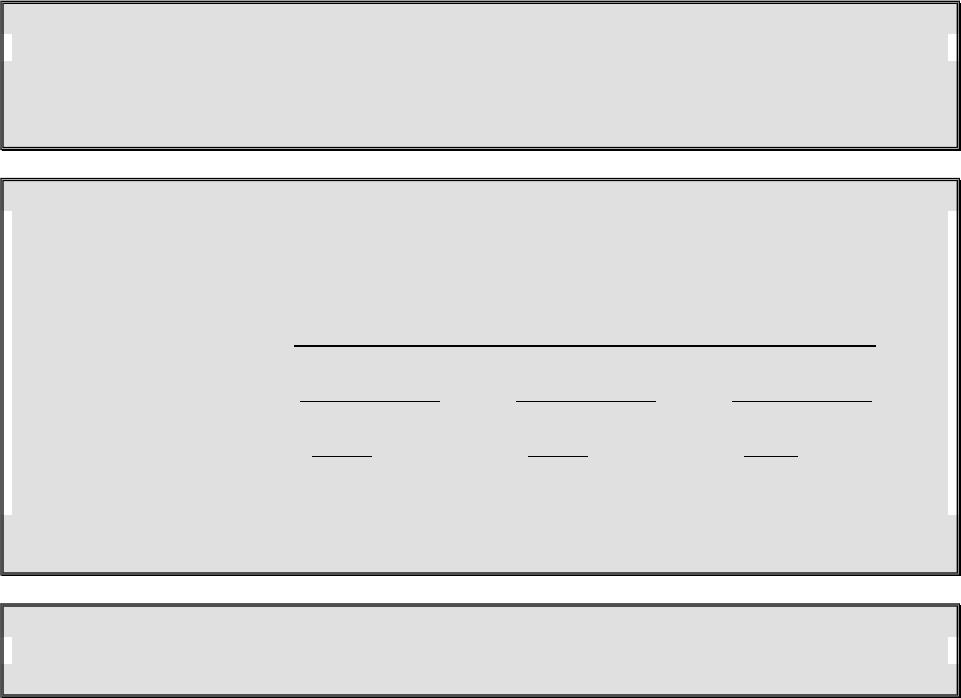

Use the information in the earlier Teaching Tip for PepsiCo. Inc., to compute the vertical analysis

percentage for net income.

For the Years Ending

Dec. 31, 20X3 Dec. 31, 20X2 Dec. 31, 20X1

Vertical analysis % = $ 3,568 = 13.2% $ 3,000 = 11.9% $2,400 = 10.2%

$26,971 $25,112 $23,512

Net income was 10.2% of every sales dollar in 20X1 but rose to 13.2% of every sales dollar in

20X3.

Teaching Tip

Exhibit 10.2 provides a vertical analysis for General Mills, Inc.

Ratio Analysis (LO 3)

I. Liquidity ratios measure the company’s ability to pay its current bills and operating

costs.

a. Current ratio

i. Current assets divided by current liabilities

ii. This ratio was first presented in Chapter 2.

b. Cash from operations to current liabilities

i. Net cash from operating activities divided by current liabilities

ii. This ratio measures a company’s ability to meet its short-term obligation.

c. Inventory turnover ratio

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 10-4

i. Cost of goods sold divided by average inventory

ii. This ratio was first presented in Chapter 5.

d. Accounts receivable turnover ratio

i. Net credit sales divided by average net accounts receivable

ii. This ratio was first presented in Chapter 4.

II. Solvency ratios measure the company’s ability to meet its long-term obligations and to

survive over a long period of time.

a. Debt-to-equity

i. Total liabilities divided by total shareholders’ equity

ii. This ratio was first presented in Chapter 7.

III. Profitability ratios measure the operating or income performance of a company.

a. Profit margin

i. Net income divided by net sales

ii. This ratio was first presented in Chapter 3.

b. Return on assets

i. Net income + interest expense divided by average total assets

ii. This ratio was first presented in Chapter 6.

c. Asset turnover ratio

i. Net sales divided by average total assets

ii. This ratio was first presented in Chapter 6.

d. Return on equity

i. Net income minus preferred dividends divided by average common

stockholders’ equity

ii. This ratio was first presented in Chapter 8.

e. Gross profit ratio

i. Gross profit divided by net sales

ii. This ratio was first presented in Chapter 8.

f. Earnings per share (EPS)

i. Net income minus preferred dividends divided by weighted average number

of shares of common stock outstanding

ii. This ratio was first presented in Chapter 8.

IV. Market indicator ratios are ratios that relate the current market price of the company’s

stock to earnings or dividends.

a. Price-earnings ratio (P/E)

i. Market price of a share of stock divided by the current EPS

ii. Indicates the return an investor might earn by purchasing the stock

iii. Gives an indication of future earnings

iv. An extremely high P/E ratio might indicate an overpriced stock.

v. A very low P/E ratio might indicate an underpriced stock.

b. Dividend-yield ratio

i. Dividend per share divided by the market price per share

ii. Investors are willing to accept a low dividend yield when they anticipate an

increase in the price of the stock.

iii. Stocks with low growth potential may offer a higher dividend yield.

V. Understanding ratios

a. A ratio by itself does not give much information.

b. To be useful, a ratio must be compared with:

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 10-5

i. Ratios from prior years

ii. Ratios of other companies in the same industry

iii. Industry average ratios

iv. No standard formulas for computing ratios (except for EPS)

c. Be consistent in calculating ratios so comparisons will be meaningful.

d. Look for trends, components in the values that are part of the ratios, and other

information about the company that may not even be contained in the financial

statements.

e. Financial statements are only one source of information.

f. Ratio analysis is only one tool for analyzing financial statements.

Teaching Tip

Students should be aware that not all ratios apply to all companies. For example, inventory

turnover would not be applicable to a service company.

Teaching Tip

Have students give examples of pairs of companies that could be benchmarked against each

other. Coke and Pepsi would be a good start. If time permits, obtain the information needed and

complete the analysis.

Teaching Tip

Call a company that issues annual reports and ask them to send you enough copies of their

annual report for your class to use, or copy the annual report of the company from the Internet.

Use a copy of Robert Morris and Associates’ (RMA) Annual Statement Studies, and select an

appropriate industry category for comparison. Use this annual report to help illustrate the

calculations, and then compare your results to the industry averages. In some cases, the ratios

are calculated differently than in the text.

Teaching Tip

Use the example that begins on page 470 to demonstrate how to use ratio analysis.

Financial Statement Analysis – More than Numbers (LO 3)

I. The notes are an integral part of the financial statements.

a. Some analysts believe there is more real information about the health of a company in

the notes to the financial statements than in the statements themselves.

II. A business plan is a detailed analysis of what it would take to start and maintain the

operation of a successful business.

a. It should include a sales forecast, total expenses estimated, and prospective

financial statements.

b. Banks often require these prior to lending money to new firms.

III. Because accounting is such an integral part of business, accounting principles will

continue to change as business changes.

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 10-6

a. Each year the FASB and other standard-setting bodies add and changes rules for

including, excluding, and valuing items in the financial statements.

b. The accounting profession will be increasingly concerned with electronic

transactions, e-business, and real-time access to financial data.

Business Risk, Control, and Ethics (LO 4)

I. There are risks with owning stock.

II. How do you minimize those risks?

a. Be diligent about finding a financial advisor or financial analyst to help you.

i. Become an expert in the analysis of available stock.

ii. Know some financial accounting and financial statement analysis.

b. Diversify.

i. This means to vary or expand.

ii. Don’t put all your eggs in one basket.

iii. This allows you to earn a higher rate of return for a given amount of risk.

III. You cannot eliminate all the risks of stock ownership.

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 10-7

CHAPTER 10 NAME ___________________________________

TEN-MINUTE QUIZ Section _____________ Date____________

_____________________________________________________________________________

_

_____ 1. Items separated from the regular earnings of a company include:

a. Discontinued operations

b. Extraordinary items

c. Loss on sale of equipment

d. Two of the above

_____ 2. To be reported as an extraordinary item, the event must be:

a. Unusual and infrequent

b. Unusual and frequent

c. Normal and infrequent

d. Part of continuing operations

_____ 3. When using horizontal analysis, the base year is normally:

The current year

The earliest year presented

The latest year presented

The year with the highest revenues

_____ 4. Jacksonville Company reported cost of goods sold of $80,000 in 20X5 and

$92,000 in 20X6. The percentage change is:

12%

13%

15%

None of the above

_____ 5. A method of financial statement analysis that must use two or more years of

financial statements is known as:

Horizontal

Diagonal

Ratio

All of the above

_____ 6. What type of ratios measure the company’s ability to pay its current bills and

operating costs?

Liquidity

Solvency

Profitability

Market indicator

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 10-8

_____ 7. Liquidity ratios include all of the following, except:

a. Return on assets

b. Current ratio

c. Working capital

d. Acid test

_____ 8. Which of the following types of ratios measure the ability of a company to

survive over a long period of time?

a. Liquidity ratios

b. Solvency ratios

c. Profitability ratios

d. Market indicators

_____ 9. An extremely high price-earnings ratio may indicate:

a. That the stock is underpriced

b. That the stock is overpriced

c. That the investment is low risk

d. That the company pays high dividends

_____ 10. Dividend-yield ratio is calculated by:

a. Dividing dividend per share by market price per share

b. Dividing market price per share by dividend per share

c. Subtracting the dividend per share from the earnings per share

d. Dividing the dividend per share by the earnings per share

ANSWER KEY – CHAPTER 10 – TEN-MINUTE QUIZ

D

A

B

C

A

A

A

B

B

A

Copyright © 2011 Pearson Education, Inc. publishing as Prentice Hall 10-9