Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Supplement

F Financial Analysis

1. Time Value of Money

Underlying concept of time value of money: a dollar in hand today is worth more than a dollar to

be received in the future

1. Future value of an investment

a. Compounding interest is the process by which interest on an investment accumulates, and

then earns interest itself for the remainder of the investment period.

b. Future value of an investment is the value of an investment at the end of the period over

which interest is compounded.

c. Calculating the future value of an investment requires that the interest rate and the

investment time period are expressed in the same units of time as the interval at which

compounding occurs. The formula is:

( )

1n

F P r=+

where

F = future value of the investment at the end of n periods

P = amount invested at the beginning, called the principal

r = periodic interest rate

n = number of time periods for which the interest compounds

d. Example

• The value of a $5,000 investment at 12 percent per year, 1 year from now is:

$5,000(1.12) = $5,600

• If the entire amount remains invested, at the end of 2 years you would have:

$5,600(1.12) = $5,000(1.12)2 = $6,272

e. Future Value of an Investment. Use Application F.1

An investment of $500 will earn interest of 6%, compounded annually for 5 years. The

future value is:

F = P(1+r)n

where

P = $500.00

r = .06

n = 5

F = $669.11

+

r

( )

1201

.

+

2. Present value of an investment

a. Present value of an investment is the amount that must be invested now to accumulate to

a certain amount in future at a specified interest rate.

b. Discounting is the process of finding the present value of an investment, when the future

value and the interest rate are known. The general formula is:

( )

1n

F

Pr

=+

c. The interest rate, r, is also called the discount rate.

3. Present value factors (pf)

a. To find the present value of a future amount, write the foregoing formula as:

( )

1

1n

PF r

=

+

• Multiply F by the pf number found at the intersection of the appropriate interest rate

(columns) and time period (rows).

b. Example

• What is the present value of an investment worth $10,000 at the end of year 1 if the

interest rate is 12 percent?

F = $10,000 = P(1 + 0.12)

c. Example using Present Value Factors

• An investment will generate $15,000 in 10 years. If the interest rate is 12 percent, the

Present Value Factors table shows that pf = 0.3220

The present value is: P = F(pf) = $15,000(0.3220) = $4,830

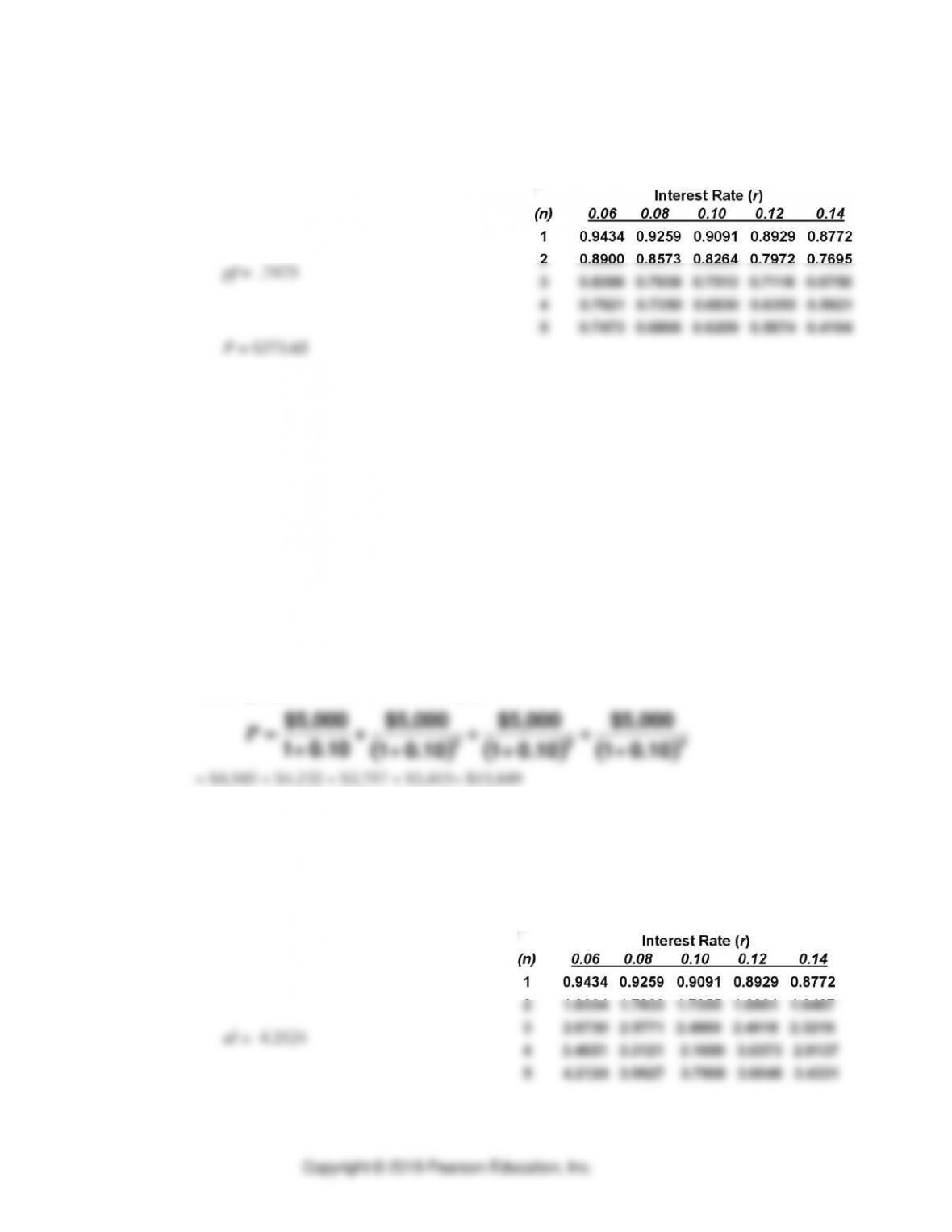

d. Present Value of a Future Amount. Use Application F.2

An investment will be worth $500 in 5 years. The interest rate is 6%. The present value

is:

( )

1n

F

Pr

=+

F = $500.00

r = .06

n = 5

P = $373.63

Solving instead using present value factor (pf) from the table:

P = F (pf)

e. Tutor F.1 in MyLab Operations Management provides an example for calculating the

present value of a future amount.

4. Annuities

a. An annuity is a series of payments of a fixed amount for a specified number of years.

b. The present value of an annuity can be found using the table for the present value factors

(af) of an annuity. Multiply the amount received each year (A) by the present value

factor:

( )

P A af=

c. Example

• At a 10% interest rate, how much needs to be invested so that you may draw out

$5,000 per year for each of the next 4 years?

d. Use Application F.3: Annuities.

You wish to investment and amount that will allow you to withdraw $500 per year for 5

years. The interest rate is 6%. The present value of your investment is:

P = A (af)

A = $500.00

Copyright © 2019 Pearson Education, Inc.

P = $2,106.20

e. Tutor F.2 in MyLab Operations Management provides an example for calculating the

present value of an annuity.

2. Methods of Financial Analysis

• Three basic financial analysis techniques which rely on cash flows are shown below. Only

incremental, after-tax cash flows should be considered.

o Net present value method

o Internal rate of return method

o Payback method

1. Depreciation and taxes

a. Depreciation is an allowance for the consumption of capital. Therefore, it is not a cash

flow, but it does affect net income.

b. Straight-line depreciation: Subtract the estimated salvage value of the asset to be

depreciated. Divide remaining value by the number of years in the assets expected

economic life.

• Tutor F.3 in MyLab Operations Management provides an example for calculating

straight-line depreciation.

c. Accelerated depreciation: The Modified Accelerated Cost Recovery System (MACRS)

allows for shorter “lives” for certain investments. This results in larger tax deductions for

depreciation.

• 10-year class: longer-life equipment

d. Income-tax rate varies with location (state or country). Include all relevant income taxes

in analysis. It may be useful to use an average income-tax rate based on the firm’s tax

rate over the past several years.

2. Analysis of cash flows: Four steps (See Example F.1)

a. Step 1: Subtract the new expenses attributed to the project from new revenues.

Alternatively, use cost savings if revenues are not affected.

b. Step 2: Subtract the depreciation to get pre-tax income.

c. Step 3: Subtract taxes to get net operating income (NOI).

d. Step 4: Compute the total after-tax cash flow by adding back depreciation, i.e., NOI + D.

3. Net present value method (NPV)

a. NPV = the original investment – the present values of all after-tax cash flows.

• If the result is positive for the discount rate used, the project earns a higher rate of

return than the discount rate.

b. The discount rate that represents the lowest desired rate of return on an investment is

called the hurdle rate.

c. Net Present Value from Project. Use Application F.4

A project under study involves the purchase of new equipment and has an initial cash

outflow of $1,550. After-tax cash inflow for the next 3 years is estimated to be:

Present value of investment (Year 0)

= $-1550.00

Present value of Year 1 cash flow

= $ 446.45

Present value of Year 2 cash flow

= $ 518.18

Present value of Year 3 cash flow

= $ 640.62

Project’s NPV

=

$ 55.25

4. Internal rate of return (IRR) method

a. The IRR is the discount rate that makes the NPV of a project zero.

• A project is successful only if the IRR exceeds the hurdle rate.

b. The IRR can be found by trial and error, beginning with a low discount rate and

calculating the NPV. If the result is greater than zero, try again with a higher discount

rate. Repeat until you are near or at zero.

c. IRR for Project. Use Application F.5

Compute the internal rate of return for this project:

Discount

Rate

NPV

10%

$500 (.9091 ) + $650 (.8264 ) + $900 (.7513 ) =

$ 117.88

12%

$500 (.8929 ) + $650 (.7972 ) + $900 (.7118 ) =

$ 55.25

14%

$500 (.8772 ) + $650 (.7695 ) + $900 (.6750 ) =

$ -3.73

Conclusion: IRR is slightly less than 14%

5. Payback method (See Example F.2 on NPV, IRR, and payback period)

a. This is a means of determining how much time will elapse before the total after-tax cash

flows will equal, or pay back, the initial investment.

• Payback is widely used, but often criticized for encouraging a focus on the short run.

b. Payback for Project. Use Application F.6

What is the payback period for this same project?

Payback for year 1

= $ 1550 – $446.45 = $1103.55

Payback for years 1 and 2

= $ 1103.55 - $518.18 = $585.37

Proportion of year 3

= $ 585.37 / $640.62 = .9138

Payback periods for project

= 2.9138 years

c. Tutor F.4 in MyLab Operations Management provides a new example for calculating

NPV, IRR, and the payback period.

6. Computer support

a. Computer support such as spreadsheets and the Financial Analysis Solver (OM Explorer)

allows for efficient financial analysis.

b. The analyst can focus on data collection and evaluation, including “what if” analyses.

3. Using Judgment with Financial Analysis