Capacity Planning ⚫ CHAPTER 4 ⚫

Copyright © 2019 Pearson Education, Inc.

period is longer than 4 years, it does not meet Darren’s threshold.

Consequently, the project should not be undertaken.

25. Dintell Corporation. Assuming a five-year life.

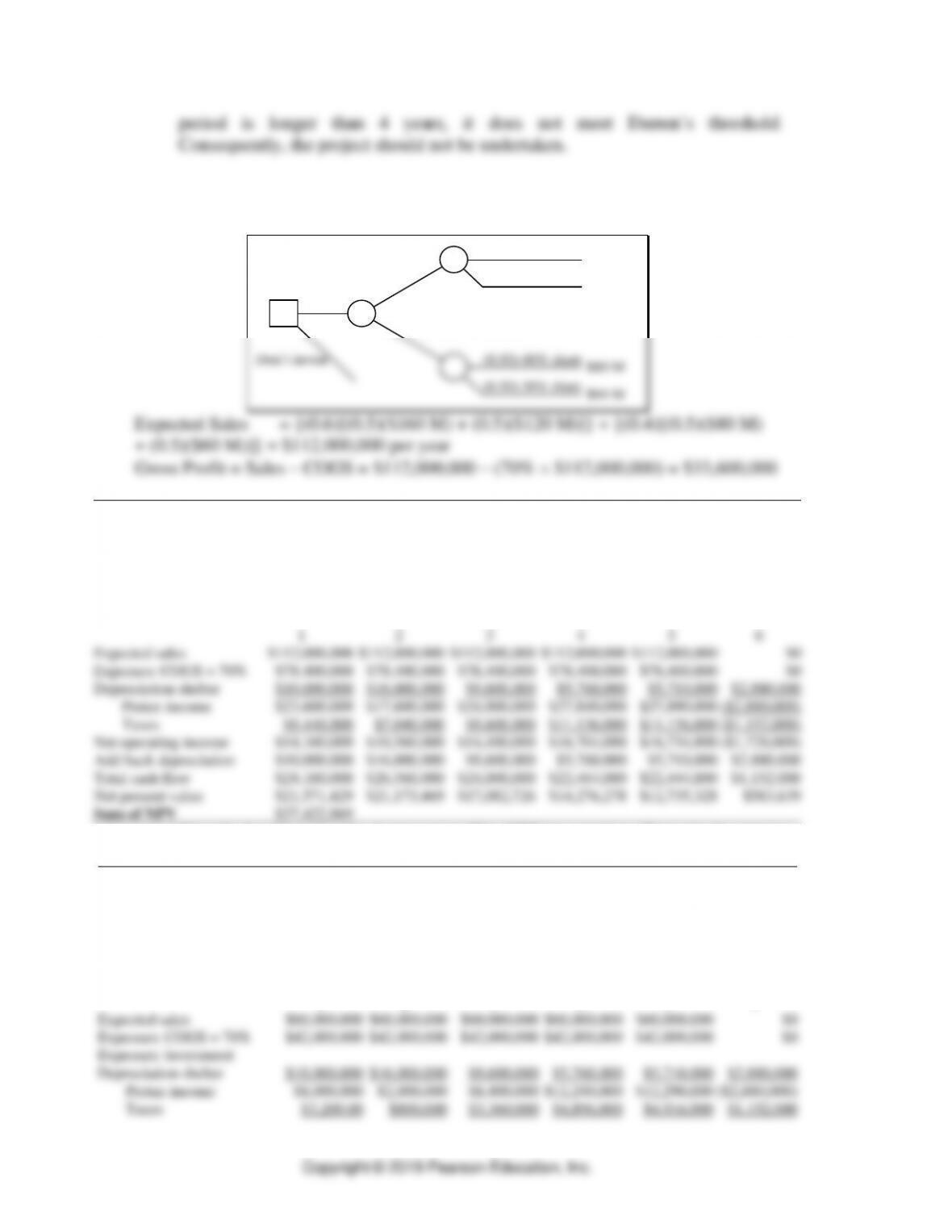

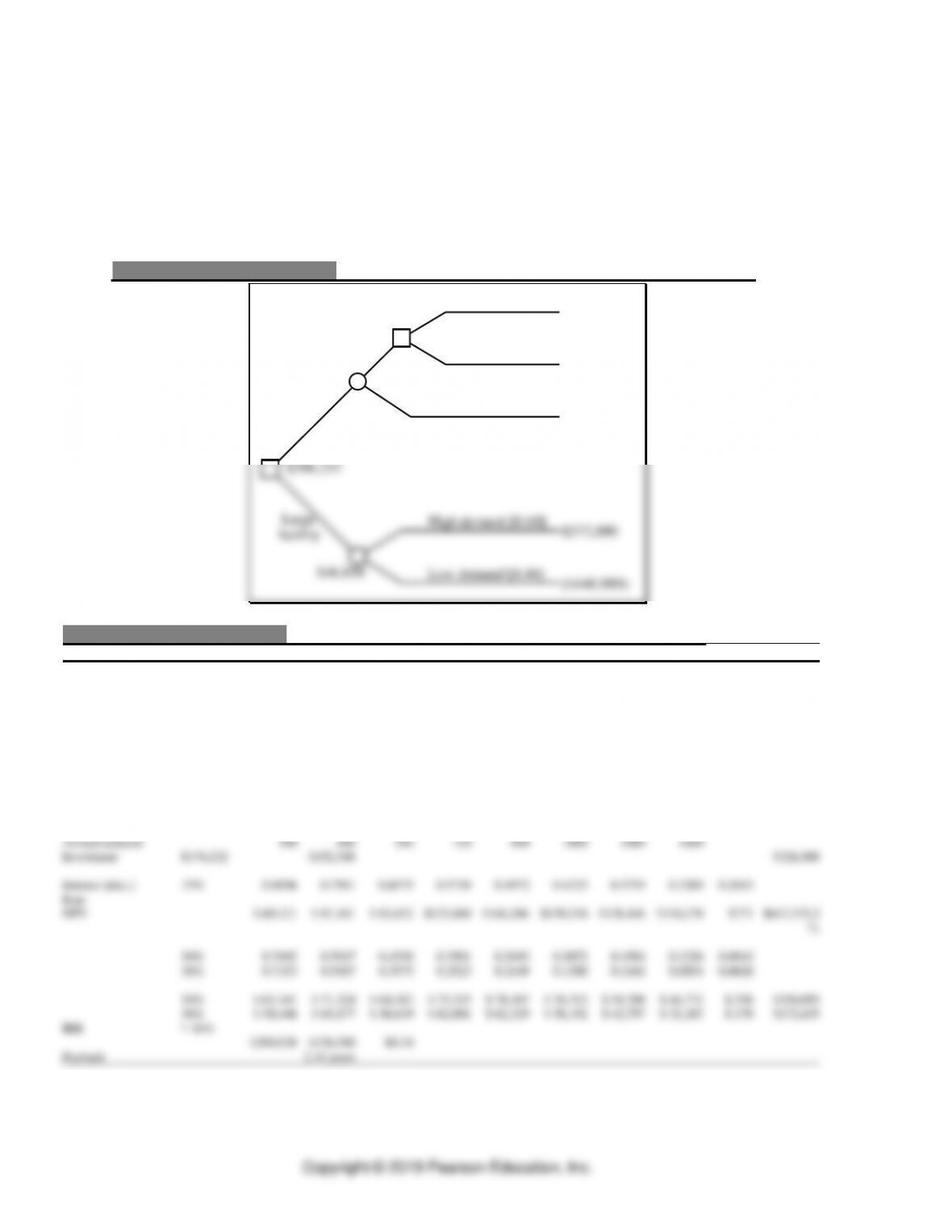

Decision tree:

Invest

(0.50) 40% share

Don’t invest

$160 M

(0.50) 30% share $120 M

(0.50) 40% share $80 M

(0.50) 30% share $60 M

(0.60) $400 M market

(0.40) $200 M market

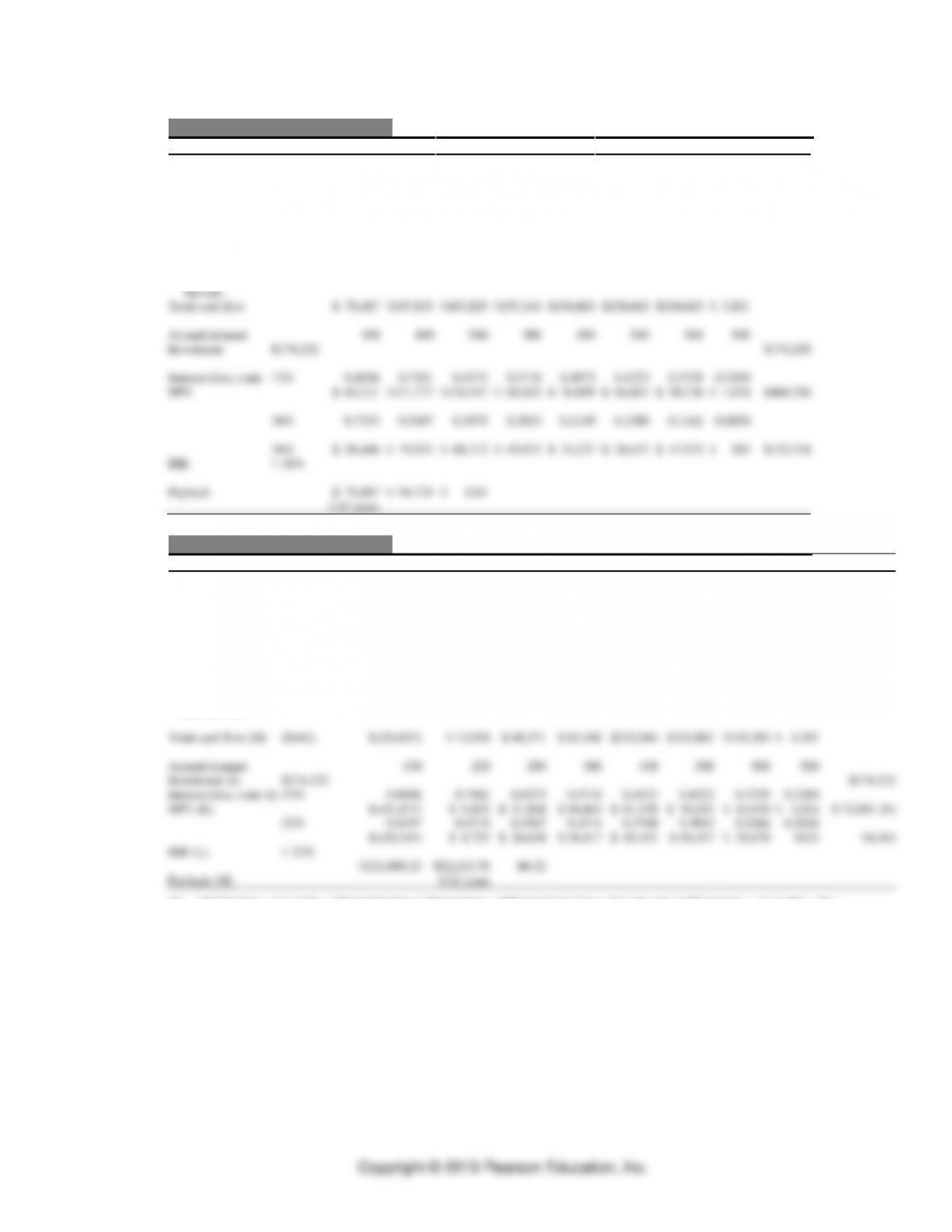

Initial information

Initial investment

$50,000,000

Tax rate

0.40

Discount rate

0.12

MACRS depreciation

0.2000

0.3200

0.1920

0.1152

0.1142

0.0576

Present value factor

0.8929

0.7972

0.7118

0.6355

0.5674

0.5066

Year

1

2

3

4

5

6

Expected sales

$112,000,000

$112,000,000

$112,000,000

$112,000,000

$112,000,000

$0

Expenses: COGS = 70%

$78,400,000

$78,400,000

$78,400,000

$78,400,000

$78,400,000

$0

Depreciation shelter

$10,000,000

$16,000,000

$9,600,000

$5,760,000

$5,710,000

$2,880,000

Pretax income

$23,600,000

$17,600,000

$24,000,000

$27,840,000

$27,890,000

($2,880,000)

Taxes

$9,440,000

$7,040,000

$9,600,000

$11,136,000

$11,156,000

($1,152,000)

Net operating income

$14,160,000

$10,560,000

$14,400,000

$16,704,000

$16,734,000

($1,728,000)

Add back depreciation

$10,000,000

$16,000,000

$9,600,000

$5,760,000

$5,710,000

$2,880,000

Total cash flow

$24,160,000

$26,560,000

$24,000,000

$22,464,000

$22,444,000

$1,152,000

Net present value

$21,571,429

$21,173,469

$17,082,726

$14,276,278

$12,735,328

$583,639

Sum of NPV

$37,422,869

a. Dintell should make the investment. The NPV is positive. Even in the worst

case, as shown below (Sales = $60 M), the NPV remains positive.

Initial information

Initial investment

$50,000,000

Tax rate

0.40

Discount rate

0.12

MACRS depreciation

0.2000

0.3200

0.1920

0.1152

0.1142

0.0576

Present value factor

0.8929

0.7972

0.7118

0.6355

0.5674

0.5066

Year

1

2

3

4

5

6

Expected sales

$60,000,000

$60,000,000

$60,000,000

$60,000,000

$60,000,000

$0

Expenses: COGS = 70%

$42,000,000

$42,000,000

$42,000,000

$42,000,000

$42,000,000

$0

Expenses: investment

Depreciation shelter

$10,000,000

$16,000,000

$9,600,000

$5,760,000

$5,710,000

$2,880,000

Pretax income

$8,000,000

$2,000,000

$8,400,000

$12,240,000

$12,290,000

($2,880,000)

Taxes

$3,200.00

$800,000

$3,360,000

$4,896,000

$4,916,000

$1,152,000

Capacity Planning ⚫ CHAPTER 4 ⚫

4-17

Net operating income

$4,800,000

$1,200,000

$5,040,000

$7,344,000

$7,374,000

($1,728,000)

Add back depreciation

$10,000,000

$16,000,000

$9,600,000

$5,760,000

$5,710,000

$2,880,000

Total cash flow

$14,800,000

$17,200,000

$14,640,000

$13,104,000

$13,084,000

$1,152,000

Net present value

$13,214,286

$13,711,735

$10,420,463

$8,327,829

$7,424,213

$583,639

Sum of NPV

$3,682,164

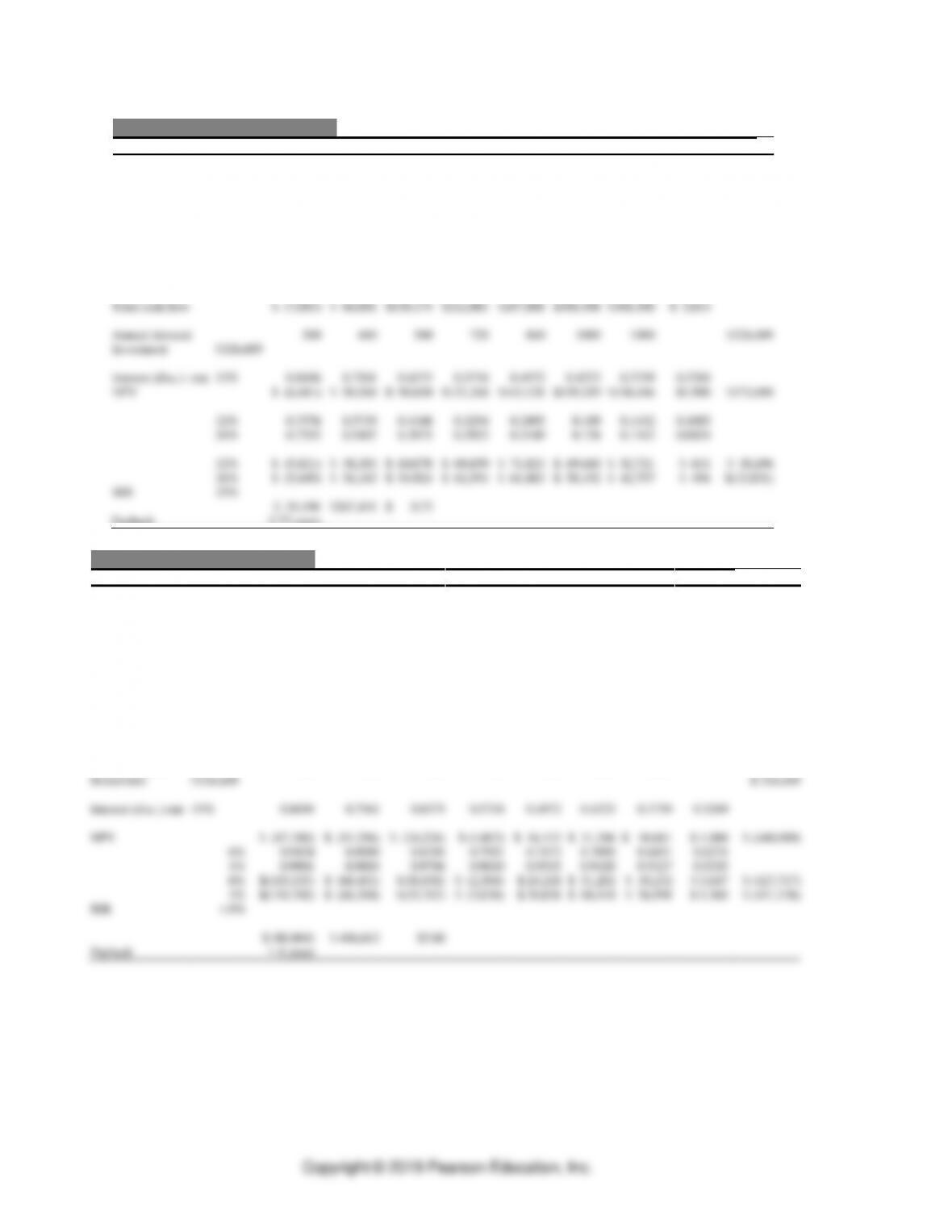

b. The decision remains the same. Greater expected payoffs favor making the

investment.

c. A decrease in the discount rate will have no effect on the decision. The

following spreadsheet shows that even at a discount rate = 12% + 15% = 27%,

the NPV remains positive.

Initial information

Initial investment

$50,000,000

Tax rate

0.40

Discount rate

0.27

MACRS depreciation

0.2000

0.3200

0.1920

0.1152

0.1142

0.0576

Present value factor

0.7874

0.6200

0.4882

0.3844

0.3027

0.2383

Year

1

2

3

4

5

6

Expected sales

$112,000,000

$112,000,000

$112,000,000

$112,000,000

$112,000,000

$0

Expenses: COGS = 70%

$78,400,000

$78,400,000

$78,400,000

$78,400,000

$78,400,000

$0

Depreciation shelter

$10,000,000

16,000,000

$9,600,000

$5,760,000

$5,710,000

$2,880,000

Pretax income

$23,600,000

$17,600,000

$24,000,000

$27,840,000

$27,890,000

($2,880,000)

Taxes

$9,440,000

$7,040,000

$9,600,000

$11,136,000

$11,156,000

($1,152,000)

Net operating income

$14,160,000

$10,560,000

$14,400,000

$16,704,000

$16,734,000

($1,728,000)

Add back depreciation

$10,000,000

$16,000,000

$9,600,000

$5,760,000

$5,710,000

$2,880,000

Total cash flow

$24,160,000

$26,560,000

$24,000,000

$22,464,000

$22,444,000

$1,152,000

Net present value

$19,023,622

$16,467,233

$11,716,559

$8,635,196

$6,793,313

$274,556

Sum of NPV

$12,910,479

d. If we consider an additional investment of $10,000,000 in the third year,

depreciation would greatly complicate the calculations, but would not change

Initial investment

$50,000,000

Third year investment

$10,000,000

Tax rate

0.40

Discount rate

0.12

MACRS depreciation

0.3333

0.4445

0.1481

0.0741

Present value factor

0.8929

0.7972

0.7118

0.6355

0.5674

0.5066

Year

1

2

3

4

5

6

Depreciation shelter

$3,333,000

$4,445,000

$1,481,000

$741,000

Pretax income (loss)

($3,333,000)

($4,445,000)

($1,481,000)

($741,000)

Taxes

$1,333,200

($1,778,000)

($592,400)

($296,400)

Net operating income

($1,999,800)

($2,667,000)

($888,600)

($444,600)

Add back depreciation

$3,333,000

$4,445,000

$1,481,000

$741,000

Adjustment to cash flow

($8,666,800)

$1,778,000

$592,400

$296,400

Previous cash flow

$24,160,000

$26,560,000

$24,000,000

$22,464,000

$22,444,000

$1,152,000

Total cash flow

$24,160,000

$26,560,000

$15,333,200

$24,242,000

$23,036,400

$1 ,448,400

Net present value

$21,571,429

$21,173,469

$10,913,869

$15,406,229

$13,071,472

$733,805

Sum of NPV

$22,870,273

Capacity Planning ⚫ CHAPTER 4 ⚫

CASE: FITNESS PLUS (PART A) *

A. Synopsis

Fitness Plus is a full-service health, fitness, and sports club located in a growing

market. The increase in demand on its facilities brought on by a sizable growth in

membership over the past few years has led to membership’s complaints of

overcrowding of club facilities and the unavailability of equipment. As with most

service organizations, Fitness Plus experiences large shifts in demand both during

the week and within each particular day. The owners are wondering what the

existing capacity of the club is and whether it is time to think about a capacity

expansion move.

B. Purpose

The case presents the students with a set of capacity planning issues within the

context of a service organization. Data in the case provide the opportunity to

address the following issues:

1. How should capacity of the facility be measured? Is there an overall measure of

facility capacity, or is it more appropriate to look at the individual areas (work

centers) and measure their capacity? The different areas may require different

types of capacity measurement. The cardiovascular room can accommodate only

29 people and is more like a job shop where the Nautilus area is similar to an

assembly line where people flow through the equipment.

2. There is the issue of calculating capacity levels and distinguishing between

utilization of capacity at peak versus average demand levels. Toward this end,

students should address the issue of how large a capacity cushion is desired in

this service setting.

3. A major decision facing the students after the measurement issues have been

addressed is the capacity expansion issue. There is information that requires the

students to focus not only on the timing and sizing issue but also on the location

issue.

4. Finally, the students must address the competitive priorities issue as they decide

on a capacity expansion strategy. This is a long-term decision, and new

competition has entered the market. Does Fitness Plus compete by having a full–

service line of equipment, providing flexibility and quality; or is convenience

and location a major competitive factor? Also, what part does cost/price play in

attracting and retaining members?

C. Analysis

Students should begin by analyzing the capacity of the facility; however, the

analysis is not as straightforward as it first may seem. There is an issue of how

capacity should be measured. Students should quickly recognize that an overall

* This case was prepared by Dr. Brooke Saladin, Wake Forest University, as a basis for classroom

discussion.

Capacity Planning ⚫ CHAPTER 4 ⚫

4-19

aerobics. In other areas, such as the Nautilus equipment, the measure may be an

“input measure,” the number of machines available.

A second set of complicating issues deals with the impact that management policies

and assumptions have on capacity measures. In their analysis the students need to

determine how many members can be serviced in each area of the club. The number

served per hour in the cardiovascular area, for example, will depend on whether

management chooses to limit the time on each machine during peak hours of

With these issues in mind, the students can develop capacity estimates similar to the

following:

1. Aerobics

❑ Assumption: Aerobics classes begin on the hour and last for 50 minutes.

❑ Capacity: 1 class per hour for 35 members

2. Cardiovascular

❑ Assumption: During peak demand times, each piece of equipment is limited to

30 minutes per member.

❑ Capacity: With 29 pieces of C-V equipment, 58 members per hour peak

capacity

3. Nautilus

Capacity Planning ⚫ CHAPTER 4 ⚫

Tennis:

12 members/hour for singles

24 members/hour for doubles

Racquetball:

16 members/hour for singles

32 members/hour for doubles

There were no details given in the case to determine the capacity of the free-weight

area. So, if we aggregate the individual capacities into an overall measure, the club

can accommodate a peak capacity of 181 to 209 members per hour, excluding the

free-weight area—far more than the peak demand of 80 per hour. Of course, what is

important is not the aggregate demand level, but rather the demand mix and how

this mix matches the individual area capacities.

The next step in the analysis is to focus the students on estimating the demands that

are placed on the club facilities. Because this is a service being provided, the focus

should be on looking at the club’s ability to satisfy peak demand. Students should

quickly derive the following estimates of peak demand:

Arrival rate at peak

=

80 members/hour

Aerobics @ 30%

=

24 members/hour

Cardiovascular @ 40%

=

32 members/hour

Nautilus @ 25%

=

20 members/hour

Racquetball @ 15%

=

12 members/hour

Tennis @ 10%

=

8 members/hour

Free-Weights @ 20%

=

16 members/hour

These potential demand rates during the peak times indicate a number of things.

First, when compared to the area capacities calculated earlier, there seems to be

plenty of excess capacity in all areas of the club. Second, it is obvious that members

use more than one area of the club during their visits, as the total potential demand

across all areas of the club adds to 112-person hours, impossible with only 80

members arriving per hour.

capacity expansion needs to be addressed. The fact is, members are complaining,

and expected service levels are not being met. The analysis should focus on both

short-term and long-term solution alternatives and looking at the pros/cons of each.

Exhibit TN.1 gives an example of how to present this analysis. Be sure to tie the

alternatives into other operating decisions and discuss how each may impact

different competitive priorities, such as convenience and location, full-service range

Capacity Planning ⚫ CHAPTER 4 ⚫

4-21

of activities with quality facilities, availability of services in a timely manner, or

low costs/price.

D. Recommendations

When this decision case is used as an outside assignment, the instructor should be

prepared to respond to three types of recommendations:

1. No action needed: Students who compare the demand rates at peak times with

the designed capacity may conclude that there is plenty of excess capacity.

These students will not seriously consider the need for a capacity cushion, or

conclude that it is already large enough.

E. Teaching Suggestions

This case is best used as an in-class discussion case to present the issues

surrounding capacity management decisions in service organizations. If a more in–

depth discussion is desired, the case can be assigned overnight. However, the data

are not present in the case to allow a thorough analysis of the capacity expansion

issue. Students will find it difficult to address the “capacity cushion” issues.

However, if the case is used in class to introduce capacity concepts, then the

discussion can be quite good.

The class discussion should begin with determining how capacity in a service

organization should or can be measured. Make sure students understand the

importance of peak-load planning. The second stage of the discussion should flow

to the determination of demands on the service system. Once the variability in

demand across time and service areas is established and it looks as though capacity

is sufficient, the concept of “capacity cushions” should be introduced. Finally, get

the students to address the various capacity alternatives, both short and long term.

Here you can reintroduce the concept of competitive priorities and discuss how

different capacity strategies support different competitive strategies.

To fully discuss each of these four areas—capacity measurements, demand

measurements, capacity cushions, and capacity expansion alternatives—will take a

good 45 minutes, especially when the students begin to argue about different

managerial assumptions and policies that affect capacity.

Capacity Planning ⚫ CHAPTER 4 ⚫

F. Board Plan

Capacity

Demand

Expansion

Alternatives

Measures

Measures

Short

Long

+ –

+ –

G. A Note on Waiting Lines

Some students may try to apply waiting line models. Waiting line theory does not

apply very well to the Fitness Plus (A) case, because of inappropriate assumptions

and missing information. The aerobics class is a good example of inappropriate

assumptions. Most likely an aerobics class is prescheduled, and everybody arrives

at the start of the class. There is no variability on the processing rate. The time it

takes for one customer is the same that it takes to handle 35 customers

simultaneously, assuming a one hour class.

On the other hand, we might apply at least approximately waiting line analysis to an

operation such as the 29 pieces of cardiovascular equipment. We must make some

Herculean assumptions to proceed. However, let’s assume that all 29 machines are

available (no maintenance downtime), and that 32 customers will spend their time

at this operation for about 20 minutes per machine and work out on between 2 and 3

machines (say 2.5 machines on the average) during their visit. Thus the service rate

might be 3 customers per hour (20 minutes per machine). As for the arrival rate, we

could assume that a customer “enters” the system an average of 2.5 times during an

hour. If we assume 32 customers arrive to the whole operation per hour, this pace

gets translated into an arrival rate of 80 customers per hour (32 2.5), taking into

account repeat visits.

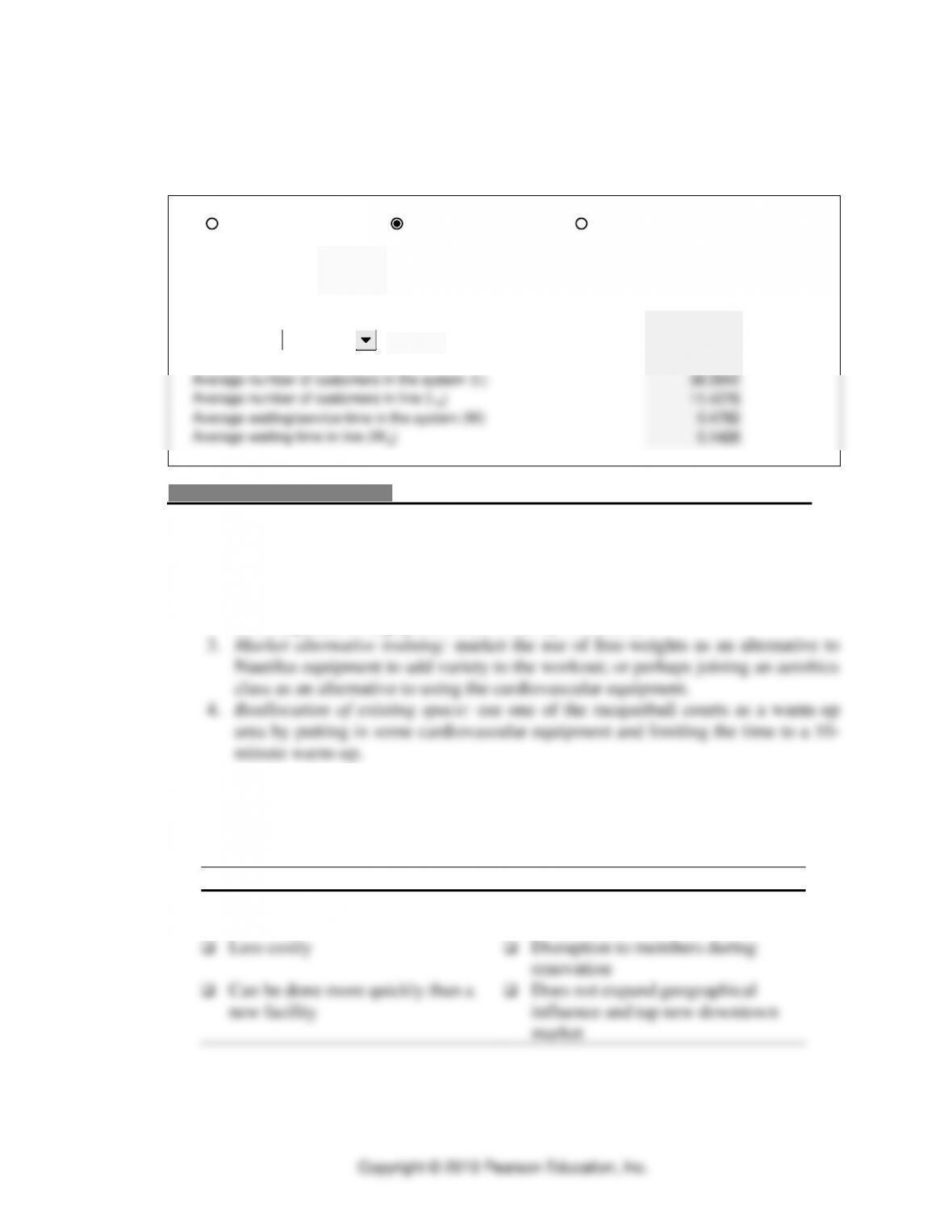

Shown below is some output from OM Explorer’s Waiting Lines Solver that

approximates this set of assumptions. Here the capacity cushion is less than 10

percent and ON EACH MACHINE the customer waits an average of 8.6 minutes to

get a machine (0.1428 x 60).

A second way to analyze the situation is to look at some of the more popular

cardiovascular machines (the real bottlenecks) and apply the single channel

approach used in the Queuing at 1st Bank Villa Italia bank video. It is still an

approximation, but should give some insight. However, customers surely will

“balk” and “renege” as shown in the video. They will move from one place to

another, depending on the lines. To capture more realism such as that, you can turn

to simulation (such as with the SimQuick package).

Of course, there is also a fourth method—actually observing the operation in peak

periods to see how the customers behave, how long the lines are, and so forth.

Interviewing customers who have complaints (the Six Sigma way) would also give

insights.

Capacity Planning ⚫ CHAPTER 4 ⚫

4-23

Inputs

Solver – Waiting Lines

Enter data in yellow shaded areas.

Servers 29

Arrival Rate (l)80

Service Rate (m)3

Probability of zero customers in the system (P0)0.0000

Probability of 4

customers in the system (Pn)0.0000

Average utilization of the server (r)0.9195

Average number of customers in the system (L) 38.0942

Average number of customers in line (Lq)11.4276

Average waiting/service time in the system (W) 0.4762

Average waiting time in line (Wq)0.1428

Single-server model

Multiple-server model

Finite-source model

at most

EXHIBIT TN.1

Capacity Expansion Alternatives

A. Short-term alternatives

1. Use of differential pricing: base on either time of the day or area of the club to

be used.

2. Time limits during peak hours: increase the use of time restrictions being placed

on or adjusted for equipment that is heavily in demand.

B. Long-term alternatives

1. Expand existing facility: this would entail both adding on to the facility where

possible and redesigning the existing space to accommodate high-demand

services.

+

–

❑ Help balance demand and service

area usage

❑ May be temporary solution to long-

term problem of growth

❑ Less costly

❑ Disruption to members during

renovation

❑ Can be done more quickly than a

new facility

❑ Does not expand geographical

influence and tap new downtown

market

Capacity Planning ⚫ CHAPTER 4 ⚫

Copyright © 2019 Pearson Education, Inc.

2. Open a new facility downtown: this is a more aggressive long-term move to

expand the market area.

+

–

❑ Is a strategic answer to a long-term issue

❑ May not help overcrowding at original

facility

❑ Open new markets when competition is

increasing at original facility

❑ More costly; take longer to bring new

capacity on line

❑ Takes longer to bring capacity on line

CASE: FITNESS PLUS (PART B) *

A. Synopsis

This sequel of Fitness Plus (A) opens up even more options for dealing with

capacity issues that are developing at the Greensboro Industrial Park. The economic

growth in the downtown area gives Fitness Plus several new options as they look to

expand. It can restructure the existing layout, expand at the current facility, or add a

new downtown location. If it locates downtown, it can have a one- or two-stage

expansion plan.

B. Purpose

Taken together with Fitness Plus (A), this case lends itself to group projects,

including written report and class presentation. It also can be used on a “cold–call”

basis, if the focus is how the students would proceed in doing the analysis, rather

than actually doing it. It draws from several concepts in the chapter, such as

capacity strategy, decision trees, utilization measures, and cushions. It is more

complex than meets the eye, in terms of capital budgeting analysis and decision

trees. Both qualitative and quantitative analyses are important. The case can be

team taught with a Finance professor to bring home the cross-functional

connections.

C. Analysis

Students should analyze the projected revenue and cost streams for the different

options, taking into account the time value of money and the different demand

scenarios. This analysis can be done with decision trees, with financial analysis

used to determine the present value of different combinations of demand forecasts

and expansion options. The OM Explorer Software offers a spreadsheet approach to

facilitate the financial analysis. Sensitivity analysis is also desirable.

D. Recommendations

A decision tree for the expansion decision is given in Exhibit TN.1, and the

associated NPV, IRR, and payback periods are provided in Exhibit TN.2.

Exhibits TN.3 through TN.8 give the detailed financial analysis for each branch in

the decision tree. These exhibits are from a student analysis and are generally well

* This case was prepared with important inputs from Maureen Campanella of Be Fit.

Capacity Planning ⚫ CHAPTER 4 ⚫

4-25

done. The decision on used versus new equipment is not shown on the decision tree,

based on the argument that used equipment should be ruled out because it might

undermine quality as a competitive priority. Fitness Plus must maintain a

professional appearance, particularly at its downtown facility. The quality of

services offered requires new equipment that has the latest product technologies. If

used equipment is not disqualified, it would look more attractive based on the

financial analysis. The overall downtown market should be closely reviewed. It may

not be economically feasible to proceed with the new club based on future

competition and trends that may influence the necessity of expanding into the

downtown market. For instance, the recent growth in exclusively outdoor activities,

such as cross-country running, Rollerblading and biking, will impact the growth in

future memberships. Other types of equipment and activities should be examined

and new programs introduced as a way to capture this diverging market. Finally, the

effect of the expansion into the downtown area could act to erode the number of

members who currently use the suburban location.

One reasonable, albeit conservative, solution is to expand to the downtown by

starting out with a small facility until forecasted demand is more certain. This

recommendation is supported by the decision tree analysis. It also makes sense

because a drop in the predicted customer membership can dramatically influence

NPV, payback, and IRR calculations. Exhibit TN.7 shows how an adjustment down

in membership numbers, such as 25 percent, can significantly affect the outcome. A

large facility would yield a $72,000 NPV, but a 25 percent drop in memberships

shows NPV at a negative $26,000.

In addition to the quantitative analysis, other factors need to be considered.

Comparisons of these numbers alone will not necessarily determine the best

alternative, and these other factors have to be weighed.

This solution must be coordinated with what is planned for the existing facility, as

discussed for the Fitness Plus (A) case. It may be possible to realign the capacity to

better serve the aerobics, cardiovascular and Nautilus areas. If this is not possible

due to the expansion in the downtown locations, several less-costly solutions are

possible, such as:

❑ Redesign the floor plan to give less room to some of the areas that are operating

well within the range of the desired capacity cushion. Economies of scale in

purchasing new equipment for downtown location. Get some more

cardiovascular equipment for the industrial park location.

❑ Promote time limits on the most popular cardiovascular equipment.

❑ Cross-train members in other fitness areas.

❑ Give price breaks if people only work out during nonpeak hours.

❑ Encourage “lunch–time” workouts for people within the industrial park.

❑ Work on the positioning of the club. With increased competition in the area,

there appears to be a marketable niche for a “family club.”

Capacity Planning ⚫ CHAPTER 4 ⚫

E. Teaching Suggestions

Address the issues in Fitness Plus (A) first, and then move into Fitness Plus (B).

Develop a decision tree on the board with class inputs, and then ask for the NPV

results for the different branches. For at least one of them, investigate the

spreadsheets that were developed. Finally, bring in the insights from sensitivity

analysis and the fit with the firm’s overall strategy.

EXHIBIT TN.1

Decision Tree

$612,375

$396,257

$396,257

Small

facility

$46,858

Large

facility

2

High

demand

[0.6]

$612,375

$409,790

$72,081

$372,090

($440,989)

Expand

Don’t expand

Low demand [0.40]

High demand [0.60]

Low demand [0.40]

EXHIBIT TN.2

Small Facility/High Demand/Expand

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Revenue

$347,280

$449,344

$583,408

$717,472

$851,536

$985,600

$985,600

$985,600

Expenses fixed

$ 64,000

$124,000

$124,000

$124,000

$124,000

$124,000

$124,000

$124,000

Expenses variable

$167,400

$267,200

$267,200

$267,200

$267,200

$267,200

$267,200

Depreciation

(7 yr MACRS)

$ 24,896

$ 64,437

$ 67,781

$ 48,406

$ 34,586

$ 29,163

$ 29,163

$ 21,357

$ 6,779

$326,568

Pretax income

$ 90,984

$ 93,507

$124,427

$277,866

$425,750

$565,237

$565,237

$573,043

$(6,779)

Taxes (40%)

$ 36,393

$ 37,403

$ 49,771

$111,147

$170,300

$226,095

$226,095

$229,217

$(2,712)

Net operating

Income

$ 54,590

$ 56,104

$ 74,656

$166,720

$255,450

$339,142

$339,142

$343,826

$(4,068)

Total cash flow

$ 79,487

$120,541

$142,437

$215,125

$290,036

$368,305

$368,305

$365,183

$2,712

Annual demand

300

440

580

720

860

1000

1000

1000

Investment

$174,222

$152,346

$326,568

Interest (disc.)

15%

0.8696

0.7561

0.6575

0.5718

0.4972

0.4323

0.3759

0.3269

0.2843

Rate

NPV

$ 69,121

$ 91,141

$ 93,652

$123,009

$144,206

$159,218

$138,446

$119,378

$771

$612,375,2

71

30%

0.7692

0.5917

0.4520

0.3501

0.2693

0.2072

0.1594

0.1226

0.0943

36%

0.7353

0.5407

0.3975

0.2923

0.2149

0.1580

0.1162

0.0854

0.0628

30%

$ 61,141

$ 71,324

$ 64,382

$ 75,315

$ 78,107

$ 76,313

$ 58,708

$ 44,771

$ 256

$356,095

36%

$ 58,446

$ 65,177

$ 56,619

$ 62,881

$ 62,329

$ 58,192

$ 42,797

$ 31,187

$ 170

$172,435

IRR

> 36%

$200,028

$126,540

$0.34

Payback

2.34 years

Capacity Planning ⚫ CHAPTER 4 ⚫

4-27

EXHIBIT TN.3

Small Facility/High Demand/Don’t Expand

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Revenue

$347,280

$449,344

$490,800

$478,800

$478,800

$478,800

$478,800

Expenses fixed

$ 64,000

$ 64,000

$ 64,000

$ 64,000

$ 64,000

$ 64,000

$ 64,000

Expenses variable

$167,400

$167,400

$167,400

$167,400

$167,400

$167,400

$167,400

Depreciation

(7 yr MACRS)

$ 24,896

$ 42,667

$ 30,471

$ 21,760

$ 15,558

$ 15,558

$ 15,558

$ 7,753

$174,222

Pretax income

$ 90,984

$175,277

$228,929

$225,640

$231,842

$231,842

$231,842

$(7,753)

Taxes (40%)

$ 36,393

$ 70,111

$ 91,571

$ 90,256

$ 92,737

$ 92,737

$ 92,737

$(3,101)

Net operating

Income

$ 54,590

$105,166

$137,357

$135,384

$139,105

$139,105

$139,105

$(4,652)

Total cash flow

$ 79,487

$147,833

$167,829

$157,144

$154,663

$154,663

$154,663

$ 3,101

Annual demand

300

400

500

500

500

500

500

500

Investment

$174,222

$174,220

Interest (disc.) rate

15%

0.8696

0.7561

0.6575

0.5718

0.4972

0.4323

0.3759

0.3269

NPV

$ 69,121

$111,777

$110,347

$ 89,855

$ 76,899

$ 66,861

$ 58,138

$ 1,014

$409,790

36%

0.7353

0.5407

0.3975

0.2923

0.2149

0.1580

0.1162

0.0854

36%

$ 58,446

$ 79,933

$ 66,712

$ 45,933

$ 33,237

$ 24,437

$ 17,972

$ 265

$152,714

IRR

> 36%

Payback

$ 79,487

$ 94,735

$ 0.61

1.61 years

EXHIBIT TN.4

Small Facility/Low Demand

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Revenue (A)

$173,640

$224,672

$291,704

$358,736

$425,768

$492,800

$420,000

Expenses fixed (B)

$ 64,000

$ 64,000

$ 64,000

$ 64,000

$ 64,000

$ 64,000

$ 64,000

Expenses variable (C)

$167,400

$167,400

$167,400

$167,400

$167,400

$167,400

$167,400

Depreciation

(7 yr MACRS) (D)

$ 24,896

$ 42,667

$ 30,471

$ 21,760

$ 15,558

$ 15,558

$ 15,558

$ 7,753

$174,222

Pretax income (E)

(A-B-C-D)

$ (82,656)

$(49,395)

$ 29,833

$105,576

$178,810

$245,842

$173,042

$ (7,753)

Taxes (40%) (F)

(E x 40%)

$ (33,063)

$(19,758)

$ 11,933

$ 42,230

$ 71,524

$ 98,337

$ 69,217

$ (3,101)

Net operating

Income (G)

(E–F)

$ (49,594)

$(29,637)

$ 17,900

$ 63,345

$107,286

$147,505

$103,825

$ (4,652)

Total cash flow (H)

(D+G)

$ (24,697)

$ 13,030

$ 48,371

$ 85,106

$122,844

$163,063

$119,383

$ 3,101

Annual demand

150

220

290

360

430

500

500

500

Investment (I)

$174,222

$174,222

Interest (disc.) rate (J)

15%

0.8696

0.7561

0.6575

0.5718

0.4972

0.4323

0.3759

0.3269

NPV (K)

$ (21,477)

$ 9,852

$ 31,804

$ 48,663

$ 61,078

$ 70,492

$ 44,876

$ 1,014

$ 72,081 (N)

22%

0.8197

0.6719

0.5507

0.4514

0.3700

0.3033

0.2486

0.2038

$ (20,245)

$ 8,755

$ 26,638

$ 38,417

$ 45,452

$ 49,457

$ 29,679

$632

$4,563

IRR (L)

> 22%

$121,809.22

$52,412.78

$0.32

Payback (M)

4.32 years

(A)

(150 Members 12 months $70 monthly fee) + (150 members $200 membership fee) + Juice bar sales (1150 members 12 months 70)

(14%)

(B)

$8/sq foot 8,000 sq. feet

(C)

Salaries & wages of $120,000 + insurance & liability of $25,000 + maintenance of $2,400 + electricity of $20,000

(D)

Investment of $174,222 1st year’s depreciation percentage of 14.29%

(I)

New equipment $160,000 + carpet $14,222 ($1.77 per sq. foot 8,000 sq. feet)

(J)

Expected ROI & present value table amounts

(K)

(J) (H)

(L)

Used 22% because it was the closest % on the table that brings the investment near its IRR

(M)

Using Row H (-24,697+13,030+48,371+85,106 = 121,809.22, or 4 years) + the investment of 174,222/121,809.22 .32

(N)

Sum of row (K) less the initial investment.

Capacity Planning ⚫ CHAPTER 4 ⚫

EXHIBIT TN.5

Large Facility/High Demand

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Revenue

$347,280

$449,344

$583,408

$717,472

$851,536

$985,600

$985,600

Expenses fixed

$124,000

$124,000

$124,000

$124,000

$124,000

$124,000

$124,000

Expenses variable

$267,200

$267,200

$267,200

$267,200

$267,200

$267,200

$267,200

Depreciation

(7 yr MACRS)

$ 46,672

$ 79,987

$ 57,124

$ 40,793

$ 29,166

$ 29,166

$ 29,166

$ 14,534

$326,609

Pretax income

$(90,592)

$(21,843)

$135,084

$285,479

$431,170

$565,234

$565,234

$(14,534)

Taxes (40%)

$(36,237)

$ (8,737)

$ 54,034

$114,191

$172,468

$226,094

$226,094

$ (5,814)

Net operating

Income

$(54,355)

$(13,106)

$ 81,050

$171,287

$258,702

$339,140

$339,140

$ (8,720)

Total cash flow

$ (7,683)

$ 66,881

$138,174

$212,081

$287,868

$368,306

$368,306

$ 5,814

Annual demand

300

440

580

720

860

1000

1000

$326,609

Investment

$326,609

Interest (disc.) rate

15%

0.8696

0.7561

0.6575

0.5718

0.4972

0.4323

0.3759

0.3269

NPV

$ (6,681)

$ 50,569

$ 90,850

$121,268

$143,128

$159,219

$138,446

$1,900

$372,090

32%

0.7576

0.5739

0.4348

0.3294

0.2495

0.189

0.1432

0.1085

36%

0.7353

0.5407

0.3975

0.2923

0.2149

0.158

0.1162

0.0854

32%

$ (5,821)

$ 38,383

$ 60,078

$ 69,859

$ 71,823

$ 69,610

$ 52,721

$ 631

$ 30,696

36%

$ (5,649)

$ 36,163

$ 54,924

$ 61,991

$ 61,863

$ 58,192

$ 42,797

$ 496

$(15,831)

IRR

35%

$ 59,198

$267,411

$ 0.73

Payback

2.73 years

EXHIBIT TN.6

Large Facility/Low Demand

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Revenue

$173,640

$224,672

$291,704

$358,736

$425,768

$492,800

$420,000

Expenses fixed

$124,000

$124,000

$124,000

$124,000

$124,000

$124,000

$124,000

Expenses variable

$267,200

$267,200

$267,200

$267,200

$267,200

$267,200

$267,200

Depreciation

(7 yr MACRS)

$ 46,672

$ 79,987

$ 57,124

$ 40,793

$ 29,166

$ 29,166

$ 29,166

$ 14,534

$ 326,609

Pretax income

$(264,232)

$(246,515)

$(156,620)

$ (73,527)

$ 5,402

$ 72,434

$(366)

$(14,534)

Taxes (40%)

$(105,693)

$ (98,606)

$ (62,648)

$ (29,303)

$ 2,161

$ 28,974

$(146)

$ (5,814)

Net operating

Income

$(158,539)

$(147,909)

$ (93,972)

$ (43,954)

$ 3,241

$ 43,460

$(220)

$ (8,720)

Total cash flow

$(111,867)

$ (67,922)

$ (36,848)

$ (3,161)

$ 32,407

$ 72,626

$ 28,946

$ 5,814

Annual demand

300

440

580

720

860

1000

1000

Investment

$326,609

$ 326,609

Interest (disc.) rate

15%

0.8696

0.7561

0.6575

0.5718

0.4972

0.4323

0.3759

0.3269

NPV

$ (97,280)

$ (51,356)

$ (24,228)

$ (1,807)

$ 16,113

$ 31,396

$ 10,881

$ 1,900

$ (440,989)

6%

0.9434

0.8900

0.8396

0.7921

0.7473

0.7050

0.6651

0.6274

1%

0.9901

0.9803

0.9706

0.9610

0.9515

0.9420

0.9327

0.9235

6%

$(105,535)

$ (60,451)

$(30,938)

$ (2,504)

$ 24,218

$ 51,202

$ 19,252

$ 3,647

$ (427,717)

1%

$(110,760)

$ (66,584)

$(35,765)

$ (3,038)

$ 30,836

$ 68,414

$ 26,998

$ 5,369

$ (411,138)

IRR

< 0%

$ (80,004)

$ 406,613

$5.60

Payback

> 8 years

Capacity Planning ⚫ CHAPTER 4 ⚫

4-29

EXHIBIT TN.7

Large Facility/25% Demand Decrease

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Revenue

$260,460

$337,008

$ 437,556

$538,104

$638,652

$739,200

$739,200

Expenses fixed

$124,000

$124,000

$124,000

$124,000

$124,000

$124,000

Expenses variable

$267,200

$267,200

$ 267,200

$267,200

$267,200

$267,200

$267,200

Depreciation

(7 yr MACRS)

$ 46,672

$ 79,987

$ 57,124

$ 40,793

$ 29,166

$ 29,166

$ 29,166

$ 14,534

$ 326,609

Pretax income

$(177,412)

$(134,179)

$ (10,768)

$106,111

$218,286

$318,834

$318,834

$(14,534)

Taxes (40%)

$ (70,965)

$ (53,671)

$(4,307)

$ 42,444

$ 87,314

$127,534

$127,534

$ (5,814)

Net operating

Income

$(106,447)

$ (80,507)

$(6,461)

$ 63,666

$130,971

$191,300

$191,300

$ (8,720)

Total cash flow

$ (59,775)

$(521)

$50,663

$104,460

$160,138

$220,466

$220,466

$ 5,814

Annual demand

225

330

435

540

645

750

750

750

Investment

$326,609

$ 326,609

Interest (disc.) rate

15%

0.8696

0.7561

0.6575

0.5718

0.4972

0.4323

0.3759

0.3269

NPV

$ (51,980)

$(394)

$ 33,311

$ 59,730

$ 79,620

$ 95,308

$ 82,873

$ 1,900

$ (28,240)

14%

0.8772

0.7695

0.675

0.5921

0.5194

0.4556

0.3996

0.3506

12%

0.8929

0.7972

0.7118

0.6355

0.5674

0.5066

0.4523

0.4039

14%

$ (52,435)

$ (401)

$ 34,198

$ 61,851

$ 83,176

$100,445

$ 88,098

$ 2,038

$ (9,639)

12%

$ (53,373)

$ (415)

$ 36,062

$ 66,384

$ 90,862

$111,688

$ 99,717

$ 2,348

$ 26,665

IRR

13%

$254,965

$ 71,644

$ 0.32

Payback

5.32 years

Fitness Plus is thoroughly investigating the option of opening a new facility

downtown. Doing so would be an aggressive capacity expansion strategy, opening

up new markets when competition is increasing at the original facility. This strategy

would enable Fitness Plus to expand its market area, but may not help the

overcrowding at the current facility. There are several uncertainties as to future

costs, customer demands, and strategies of competitors. It also will take some time

to bring the new capacity on line. However, the resurgence in activity downtown

makes this option worth more careful analysis.

Fitness Plus can lease a facility at $8 per square feet at a new downtown location. It

Capacity Planning ⚫ CHAPTER 4 ⚫

The facility should attract customers from a 6-mile radius. Membership fees would

be $70 per month, with an additional $200 initiation fee in the first year. A juice bar

and tanning beds can be added to bring in additional revenues. The juice bar can

generate an added 14% of sales, and tanning beds can add another 1% of sales. A

tanning bed costs around $5000 with a payback of just one year.

Demand for the new facility can be low or high. If low, there would be 150

members in the first year of operation, and grow until reaching a 500-member

plateau in the 6th year. This level is the largest the leased facility can currently

handle. If demand for the new facility is high, the membership would be 300 in the

first year and could increase to 1000 in the 6th year (assuming sufficient capacity).

If demand turns out to be this high, Fitness Plus has the option of having the leased

facility expanded to 14,000 square feet. This expansion would accommodate a

1000-person membership. If expansion occurs before the facility is opened, the