Chapter 21

Optimum Currency Areas

and the Euro

■ Chapter Organization

How the European Single Currency Evolved.

What Has Driven European Monetary Cooperation?

Box: Brexit.

The European Monetary System, 1979–1998.

Germany Monetary Dominance and the Credibility Theory of the EMS.

Market Integration Initiatives.

European Economic and Monetary Union.

The Euro and Economic Policy in the Euro Zone.

The Maastricht Convergence Criteria and the Stability and Growth Pact.

The European Central Bank and the Eurosystem.

The Revised Exchange Rate Mechanism.

The Theory of Optimum Currency Areas.

Economic Integration and the Benefits of a Fixed Exchange Rate Area: The GG Schedule.

Economic Integration and the Costs of a Fixed Exchange Rate Area: The LL Schedule.

The Decision to Join a Currency Area: Putting the GG and LL Schedules Together.

What Is an Optimum Currency Area?

Other Important Considerations.

Case Study: Is Europe an Optimum Currency Area?

The Euro Crisis and the Future of EMU.

Origins of the Crisis.

Self-Fulfilling Government Default and the “Doom Loop.”

A Broader Crisis and Policy Responses.

162 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

ECB Outright Monetary Transactions.

The Future of EMU.

Summary

■ Chapter Overview

The establishment of a common European currency and the debate over its possible benefits and costs was

one of the key economic topics of the 1990s. Students should be familiar with the euro but probably not

with its technical aspects or its history. This chapter provides them with the historical and institutional

background needed to understand this issue. It also introduces the idea of an optimum currency area and

presents an analytical framework for understanding this concept.

The discussion in this chapter points out that European monetary integration has been an ongoing process.

Fixed exchange rates in Europe were a by-product of the Bretton Woods system. When strains began to

appear in the Bretton Woods system, concerns arose about the effects of widely fluctuating exchange rates

between European countries. The 1971 Werner Report called for the eventual goal of fixed exchange rates

in Europe. Reasons for this included enhancing Europe’s role in the world monetary system, declining

confidence that the United States would place its international monetary responsibilities ahead of national

interests, and turning the European Union into a truly unified market. Also, many Europeans hoped

economic unification would encourage political unification and prevent a repeat of Europe’s war-torn

history.

The first attempt at a post-Bretton Woods fixed exchange rate system in Europe was the “Snake.” This

effort was limited in its membership and placed too high a burden of adjustment on countries with weak

currencies. The European Monetary System (EMS), established in 1979, was more successful. The

original member countries of the EMS included Germany, France, Italy, Belgium, Denmark, Luxembourg,

the Netherlands, and Ireland. In later years, the roll of membership grew to include Spain, Great Britain,

and Portugal. The EMS fixed exchange rates around a central parity. Most currencies were allowed to

fluctuate above or below their central rate by 2.5%, although the original band for the Italian lira and the

bands for the Spanish peseta and the Portuguese escudo allowed for fluctuations of 6% in either direction

from the central parity.

After attacks and realignments in its early years, the EMS grew to become sturdier than its predecessors.

The presence of small bands instead of pure fixed rates helped, as did the guarantee of credit from strong

to weak currency countries. The EMS was, in some sense, simply a peg to the DM. Many felt that the

dominant position of the DM had allowed other countries to import Germany’s inflation fighting

credibility and that this was another advantage of fixed rates in Europe.

Chapter 21 Optimum Currency Areas and the Euro 163

A key component of the EMS was the presence of capital controls. However, limits on capital mobility

were counter to a unified European market. Starting in 1987, capital controls were gradually phased out.

The removal of these controls contributed to the EMS crisis of 1992–1993. German reunification had led

to higher interest rates in Germany (to fight inflationary pressures), but other countries were not in a

position to follow the rate hikes. Fierce attacks followed, and some countries (the United Kingdom and

Italy) left the EMS in 1992, and the bands were widened to 15% in August 1993.

In 1986, the European Union launched a more aggressive integration package known as “1992” that was

intended to complete the internal market by 1992. To further that goal, a plan of the European Economic

and Monetary Union, which involved a single currency and was embodied in the Maastricht Treaty, was

begun, and by 1993 had been accepted by all EU countries. Reasons for pursuing a single currency

included furthering market integration, broadening the viewpoint of monetary policy by moving decision

making from the Bundesbank to a European Central Bank, avoiding the difficulties in maintaining fixed

rates with free capital movements, and supporting political unification.

A crucial aspect of EMU has been the goal of economic convergence embodied in the Maastricht

convergence criteria and the Stability and Growth Pact (SGP). These agreements stipulate low deficits and

debt-to-GDP ratios and are an attempt by low-inflation countries to prevent free-spending counterparts

from turning the euro into a weak currency. Eleven nations participated in the launch of the euro in 1999,

with the United Kingdom and Denmark choosing not to join, Sweden failing the exchange rate stability

criteria, and Greece failing all criteria (Greece joined two years later). The nations in the euro area have

ceded monetary control to the Eurosystem, comprised of the European Central Bank (ECB) plus the 18 (at

press!) national central banks of the euro area. The national central banks are now part of an overarching

structure headed by the governing council of the ECB. The ECB is a very independent central bank with

no political control and little accountability. In addition, a new exchange rate mechanism has begun in

which non-euro EU members peg to the euro.

There are both advantages and drawbacks to this decision to form a common currency union. The theory

of optimum currency areas provides a way to frame an analysis of the benefits and costs of a single

currency. The benefits of a common currency are the monetary efficiency gains realized when trade and

payments are not subject to devaluation risk. These benefits rise with an increase in the amount of trade or

factor flows, that is, with the extent of economic integration. A common currency also forces countries to

give up their independence with regards to monetary policy (at least those countries that are not at the

“center” of the system). This may lead to greater macroeconomic instability, although the instability is

reduced the more integrated the country is with the other members of the common currency area. The

analyses of the benefits and costs of membership in a common currency area are presented in the text

164 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

chapter as the GG and LL schedules, respectively. The GG–LL framework is applied to the question of

whether Europe is an optimum currency area.

An illuminating way to frame the question is to compare the United States to Europe. The evidence that

Europe is an optimum currency area is much weaker than the evidence supporting the notion that the

United States is an optimum currency area. Trade among regions in the United States is much higher than

trade among European countries. Labor is much more mobile within the United States than within Europe.

This is significant as capital mobility has increased, suggesting that a country hit with a negative economic

shock may actually experience worse unemployment given that capital will flow to other countries, while

labor does not. Furthermore, federal transfers and changes in federal tax payments provide a much bigger

cushion to region-specific shocks in the United States than do analogous EC revenues and expenditures,

which have no clear mechanism for fiscal federalism. Finally, there are greater differences in factor

endowments in Europe, which may promote greater regional specialization to take advantage of

economies of scale. Such regional specialization increases the possibility of asymmetric shocks that a

common monetary policy has difficulty dealing with.

The chapter then considers the future of the EMU. The facts that the European Union is probably not an

optimum currency area, that economic union is so far in front of political union, that EU labor markets are

very rigid, and that the SGP constrains fiscal policies will all present challenges to Europe’s economy and

to its policy makers in the years ahead. Additional challenges will be faced with the likely eastward

expansion of the EMU, given the larger structural differences between current EMU members and the

Central and Eastern European candidates that joined the European Union in 2004. In addition, the

increased popularity of economic nationalism motivated by anti-immigrant fears that drove the Brexit vote

presents an obstacle to further economic integration. Instructors may wish to call upon current events and

news stories that illuminate how these challenges are being met.

Such a current event to consider is the euro zone debt crisis that originated in Greece in 2010. Budget

deficits and debts in Greece were revealed to be much higher than had been reported, leading to a large

selloff of Greek assets. Borrowing costs rose not only in Greece, but in fellow euro zone members Ireland,

Italy, Portugal, and Spain as investors worried that the debt crisis would rapidly spread. The roots of this

crisis extended back even further, however, to a (later revealed to be false) sense of confidence in the debt

of these euro zone countries on the periphery. The interest rate spreads between these nations and the most

credit worthy countries using the euro (e.g., Germany) narrowed, injecting capital into these countries.

Borrowing and spending rose dramatically, leading to large current account deficits in these periphery

nations. Thus, when the financial crisis began, many of these nations were already deeply in debt.

A swift bailout by the strong currency EMU members could have resolved the crisis, but countries like

Chapter 21 Optimum Currency Areas and the Euro 165

Germany did not want to pay the bill for excessive government spending by other nations. A combined

bailout between the EMU and the IMF was eventually reached, but the plan was met with significant

opposition, highlighting one of the difficulties in managing the currency union. Emerging from this crisis

was recognition of the need to further coordinate fiscal policy across the Eurozone. The Fiscal Stability

Treaty signed in 2013 by 16 countries attempts to achieve this goal.

■ Answers to Textbook Problems

1. The stability of the EMS depended upon the ability of member countries’ central banks to defend

their currencies. The level of foreign currency reserves to which a central bank has access affects its

2. The maximum change in the lira/DM exchange rate was 4.5% (if, for example, the lira starts out at

the top of its band and then moves to the bottom of its band). If there was no risk of realignment, the

3. A 3% difference on the annual rate of a five-year bond implied a difference over five years of

4. The answers to the previous two questions are based upon the relationship between interest rates and

exchange rates implied by interest parity because this condition links the returns on assets

166 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

5. A favorable shift in demand for a country’s goods appreciates that country’s real exchange rate. A

favorable shift in the world demand for non-Norwegian EMU exports appreciates the euro (and hence the

6. Compare two countries that are identical except that one has larger and more frequent unexpected shifts in

its money-demand function. In the DD–AA diagrams for each country, the one with the more unstable

7. a. While in the ERM, British monetary authorities were obliged to maintain nominal interest rates at a level

commensurate with keeping the pound in the currency band. If this obligation were removed, British

c. British policy makers may have gained credibility as being strongly committed to fight inflation and to

d. A high level of British interest rates relative to German interest rates would suggest high future inflation

in Britain relative to that in Germany by the Fisher relationship. Higher British interest rates may also

Chapter 21 Optimum Currency Areas and the Euro 167

e. British interest rates may have been higher than German interest rates if British output were relatively

higher. The smaller gap at the time of the writing of the article cited may reflect relatively poor British

8. Each central bank would have benefited from issuing currency because it would have gained seigniorage

revenues when it printed money; that is, it could have traded money for goods and services. Money

9. A single labor market would facilitate the response of member countries to country-specific shocks.

Suppose there is a fall in the demand for French goods that results in higher unemployment in France. If

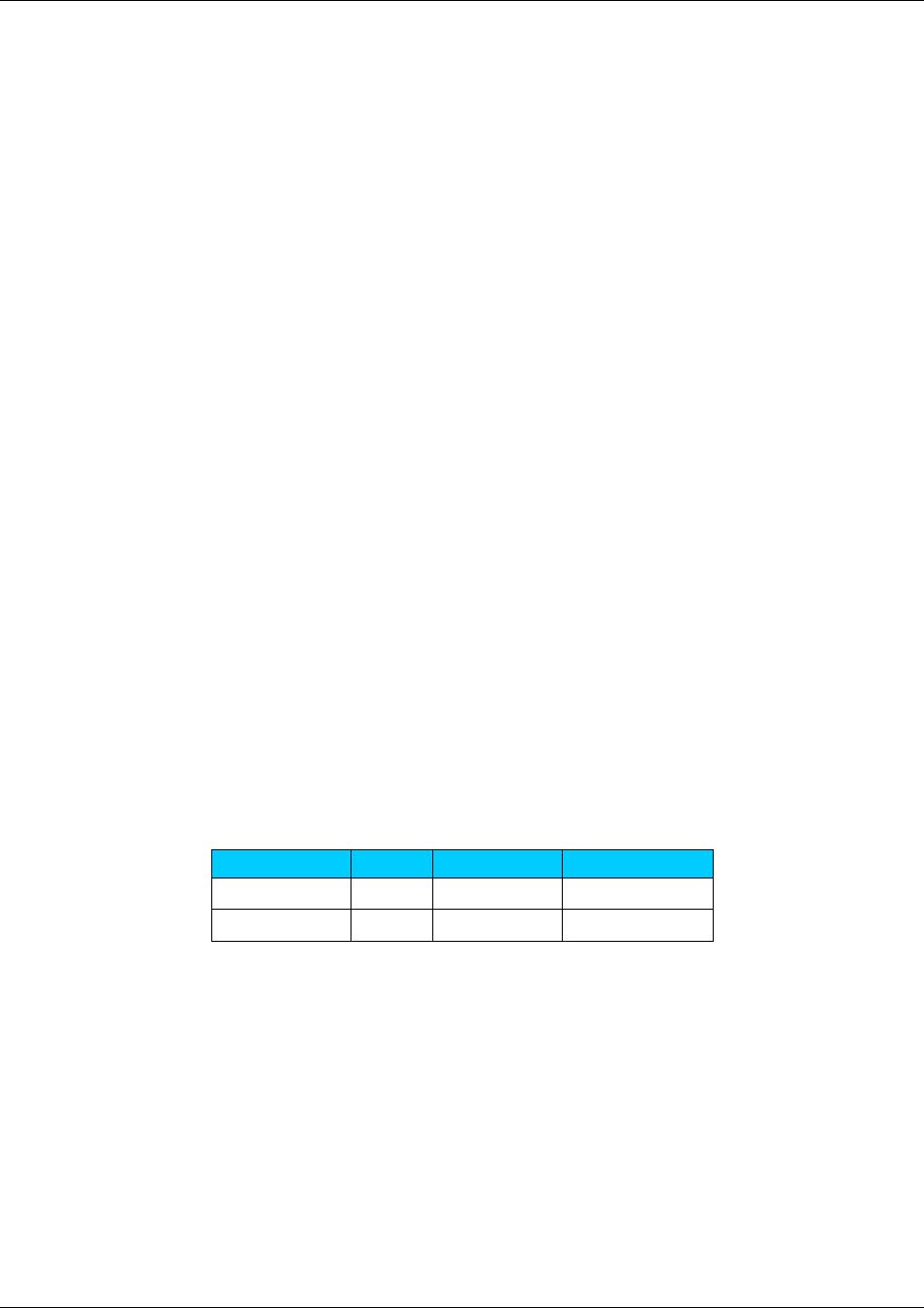

10. a. The table below compares the average rates of inflation, unemployment, and real GDP growth in the

United Kingdom and the euro zone from 1998–2015 using data from the World Bank.

Inflation

Unemployment

Real GDP Growth

The United Kingdom has had a stronger economy for much of the period since 1998 as compared to

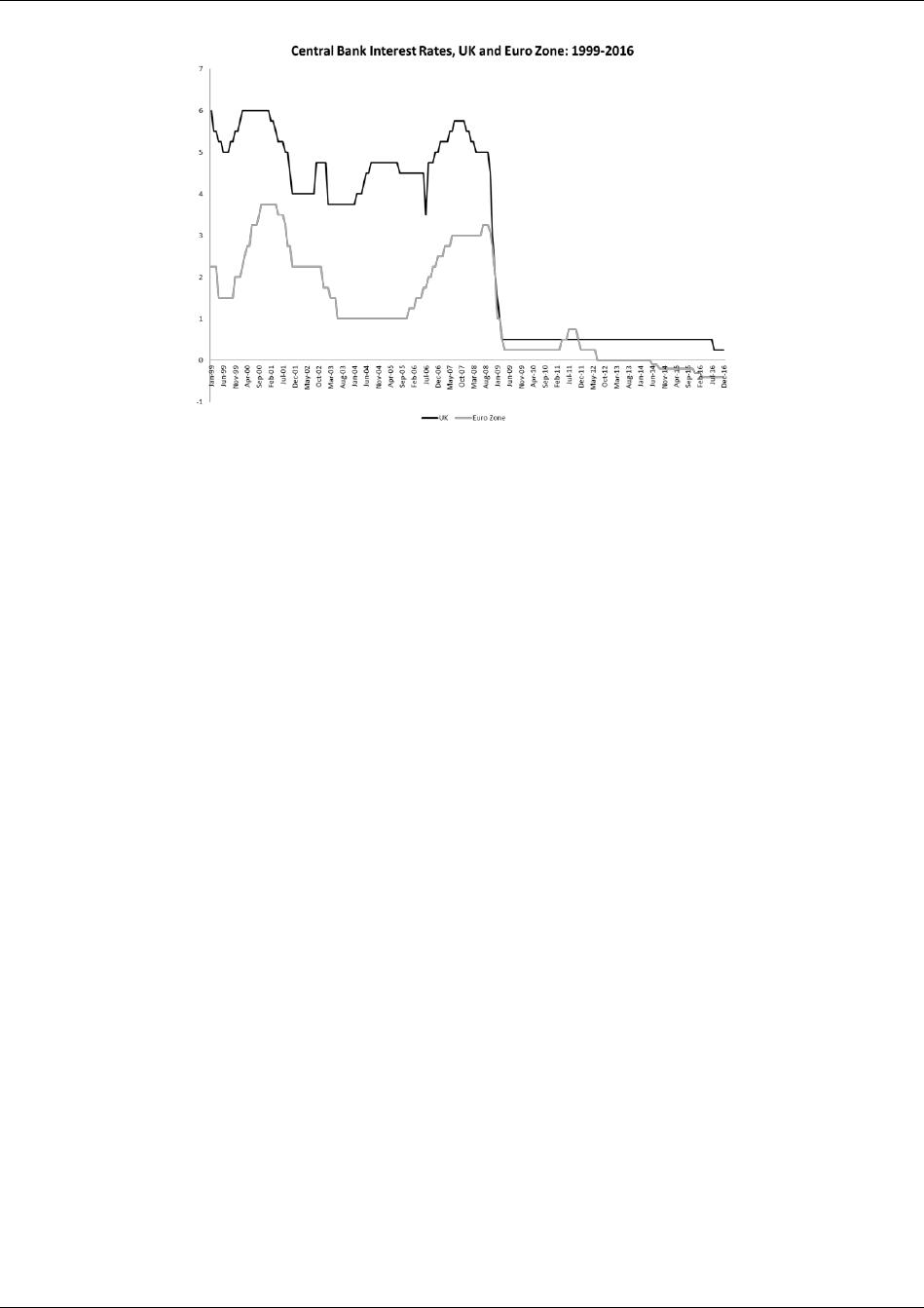

b. The chart below gives the central bank interest rates for both the UK and the euro zone between 1999

168 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

Had the United Kingdom been part of the euro area, it would have shared monetary policy with the

other countries. On the one hand, this would have meant interest rates were perhaps too low for the

11. When the euro appreciated against China’s currency in 2007, EU countries that compete with China

in third country export markets should have seen a larger drop in aggregate demand as various

customers may have switched to the suddenly relatively cheaper Chinese products. Germany should

12. Much like the concern that individual country governments would borrow too much and put pressure

on the ECB to print too much money, an excessive CA deficit of an individual country may signal

Chapter 21 Optimum Currency Areas and the Euro 169

13. All of these countries experienced significant increases in their current account balances (though the

14. If a country had an “escape clause” and could readily leave the Eurozone, the currency stability

offered by a monetary union is weakened. If the ECB signals that it will no longer act as a lender of

15. A condition of the bailout package to Cyprus was that some bank deposits in Cypriot banks would

essentially be taxed to help pay for the financial support. To make this tax binding, the government

16. a. A fiscal expansion in Germany would shift the euro area DD curve to the right. If this is a

permanent fiscal expansion, then the change in the expected exchange rate will also shift the AA

curve down, reflecting the asset market clearing at an appreciated value of the euro. In the end, output

170 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition