Chapter 19

International Monetary Systems:

An Historical Overview

■ Chapter Organization

Macroeconomic Policy Goals in an Open Economy.

Internal Balance: Full Employment and Price Level Stability.

External Balance: The Optimal Level of the Current Account.

Box: Can a Country Borrow Forever? The Case of New Zealand.

Classifying Monetary Systems: The Open-Economy Monetary Trilemma.

International Macroeconomic Policy under the Gold Standard, 1870–1914.

Origins of the Gold Standard.

External Balance under the Gold Standard.

The Price-Specie-Flow Mechanism.

The Gold Standard “Rules of the Game”: Myth and Reality.

Internal Balance under the Gold Standard.

Case Study: The Political Economy of Exchange Rate Regimes:

Conflict over America’s Monetary Standard during the 1890s.

The Interwar Years, 1918–1939.

The Fleeting Return to Gold.

International Economic Disintegration.

Case Study: The International Gold Standard and the Great Depression.

The Bretton Woods System and the International Monetary Fund.

Goals and Structure of the IMF.

Convertibility and the Expansion of Private Capital Flows.

Speculative Capital Flows and Crises.

Analyzing Policy Options for Reaching Internal and External Balance.

Maintaining Internal Balance.

142 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

Maintaining External Balance.

Expenditure-Changing and Expenditure-Switching Policies.

The External Balance Problem of the United States under Bretton Woods.

Case Study: The End of Bretton Woods, Worldwide Inflation, and the Transition to Floating Rates.

The Mechanics of Imported Inflation.

Assessment.

The Case for Floating Exchange Rates.

Monetary Policy Autonomy.

Symmetry.

Exchange Rates as Automatic Stabilizers.

Exchange Rates and External Balance.

Case Study: The First Years of Floating Rates, 1973–1990.

Macroeconomic Interdependence under a Floating Rate.

Case Study: Transformation and Crisis in the World Economy.

Case Study: The Dangers of Deflation.

What Has Been Learned Since 1973?

Monetary Policy Autonomy.

Symmetry.

The Exchange Rate as an Automatic Stabilizer.

External Balance.

The Problem of Policy Coordination.

Are Fixed Exchange Rates Even an Option for Most Countries?

Summary

APPENDIX TO CHAPTER 19: International Policy Coordination Failures

■ Chapter Overview

This is the first of four international monetary policy chapters. These chapters complement the preceding

theory chapters in several ways. They provide the historical and institutional background students require

to place their theoretical knowledge in a useful context. The chapters also allow students, through study of

historical and current events, to sharpen their grasp of the theoretical models and to develop the intuition

those models can provide. (Application of the theory to events of current interest will hopefully motivate

students to return to earlier chapters and master points that may have been missed on the first pass.)

Chapter 19 International Monetary Systems: An Historical Overview 143

Chapter 19 chronicles the evolution of the international monetary system from the gold standard of 1870–

1914, through the interwar years, the post-World War II Bretton Woods regime that ended in March 1973,

and the system of managed floating exchange rates that have prevailed since. The central focus of the

chapter is the manner in which each system addressed, or failed to address, the requirements of internal

and external balance for its participants. A country is in internal balance when its resources are fully

employed and there is price level stability. External balance implies an optimal time path of the current

account subject to its being balanced over the long run. Other factors have been important in the definition

of external balance at various times, and these are discussed in the text. The basic definition of external

balance as an appropriate current-account level, however, seems to capture a goal that most policy makers

share regardless of the particular circumstances.

Underlying each of these exchange rate systems is the “open economy trilemma,” the observation that you

can have two, but never three, of the following: exchange rate stability, independent monetary policy, and

free capital mobility. Whereas the gold standard traded independent monetary policy for exchange rate

stability and capital mobility, the Bretton Woods system allowed for autonomous monetary policy by

limiting capital flows, and the modern floating era sacrifices exchange rate stability for the other two

goals. The price-specie-flow mechanism described by David Hume shows how the gold standard could

ensure convergence to external balance. You may want to present the following model of the price-specie-

flow mechanism. This model is based upon three equations:

1. The balance sheet of the central bank. At the most simple level, this is just gold holdings equals the

money supply: G = M.

2. The quantity theory. With velocity and output assumed constant and both normalized to 1, this yields

the simple equation M = P.

3. A balance of payments equation where the current account is a function of the real exchange rate

and there are no private capital flows: CA = f(E × P*/P).

These equations can be combined in a figure like the one below. The 45° line represents the quantity

theory, and the vertical line is the price level where the real exchange rate results in a balanced current

account. The economy moves along the 45° line back toward the equilibrium point 0 whenever it is out of

equilibrium. For example, the loss of four–fifths of a country’s gold would put that country at point a with

lower prices and a lower money supply. The resulting real exchange-rate depreciation causes a current

account surplus, which restores money balances as the country proceeds up the 45° line from a to 0.

144 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

Figure 19-1

The automatic adjustment process described by the price-specie-flow mechanism is expedited by

following “rules of the game” under which governments contract the domestic source components of their

monetary bases when gold reserves are falling (corresponding to a current-account deficit) and expand

when gold reserves are rising (the surplus case).

In practice, there was little incentive for countries with expanding gold reserves to follow the “rules of the

game.” This increased the contractionary burden shouldered by countries with persistent current account

deficits. The gold standard also subjugated internal balance to the demands of external balance. Research

suggests price level stability and high employment were attained less consistently under the gold standard

than in the post-1945 period.

The interwar years were marked by severe economic instability. The monetization of war debt and of

International Monetary Fund was set up to oversee the system and facilitate its functioning by lending to

countries with temporary balance of payments problems.

A formal discussion of internal and external balance introduces the concepts of expenditure-switching and

expenditure-changing policies. The Bretton Woods system, with its emphasis on infrequent adjustment of

fixed parities, restricted the use of expenditure-switching policies. Increases in U.S. monetary growth to

Chapter 19 International Monetary Systems: An Historical Overview 145

© 2018 Pearson Education, Inc.

finance fiscal expenditures after the mid-1960s led to a loss of confidence in the dollar and the termination

of the dollar’s convertibility into gold. The analysis presented in the text demonstrates how the Bretton

Woods system forced countries to “import” inflation from the United States and shows that the breakdown

of the system occurred when countries were no longer willing to accept this burden.

Following the breakdown of the Bretton Woods system, many countries moved toward floating exchange

rates. In theory, floating exchange rates have four key advantages: They allow for independent monetary

policy; they are symmetric in terms of the costs of adjustment faced by deficit and surplus countries; they

act as automatic stabilizers that mitigate the effects of economic shocks; and they help maintain external

balance through stabilizing speculation that depreciates the currency of a country with a large current–

account deficit.

These advantages must be matched with the experience of countries running floating exchange rate

regimes. Floating exchange rates should give countries greater autonomy over monetary policy. However,

the evidence suggests that changes in monetary policy in one country do get transmitted across borders,

limiting autonomy. Second, exchange rates have become less stable. For example, in the mid 1970s, the

United States chose to pursue monetary expansion to fight a recession, whereas Germany and Japan

contracted their money supplies to counter inflation. As a result, the dollar sharply depreciated against

these currencies. The symmetry benefit of floating rates is also limited by the fact that the dollar still

serves as the world’s reserve currency, much as it did under Bretton Woods. Although floating rates do

work as automatic stabilizers, the effects may be unevenly distributed within countries. For example, the

U.S. fiscal expansion of the 1980s appreciated the dollar, limiting inflation overall. However, U.S. farmers

were hurt by this action as the stronger dollar weakened exports. With immobile factors of production,

these asymmetric effects can have long-run consequences. Finally, empirical evidence suggests that

external imbalances have actually increased since the adoption of floating exchange rates. The chapter

concludes with a discussion of policy coordination under floating exchange rates. For example, a large

country with a current-account deficit that attempts to reduce its imbalance could cause global deflation.

There is also a market failure at work here in that policies by one country have external effects. For

example, the 2007–2009 financial crisis sparked a number of fiscal expansions in countries. Increased

government spending in the United States, for example, helped lift demand not just in the United States

but in other countries as well. Because the benefits of fiscal expansion are not fully internalized (though

the costs are through accumulated budget deficits), there will be an inefficiently small expansion from a

global perspective. Thus, international policy coordination, even in a world of flexible exchange rates,

may still be warranted. This is especially relevant given the observation that given increased capital

mobility, fixed exchange rates may not even be an option for most countries in a world without

146 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

international coordination of monetary policy.

■ Answers to Textbook Problems

1. a. Because it takes considerable investment to develop uranium mines, you would want a larger

current-account deficit to allow your country to finance some of the investment with foreign

savings.

2. Because the marginal propensity to consume out of income is less than 1, a transfer of income from B

to A increases savings in A and decreases savings in B. Therefore, A has a current account surplus and

3. Changes in parities reflected both initial misalignments and balance of payments crises. Attempts to

return to the parities of the prewar period after the war ignored the changes in underlying economic

4. A monetary contraction, under the gold standard, will lead to an increase in the gold holdings of the

contracting country’s central bank if other countries do not pursue a similar policy. All countries

© 2018 Pearson Education, Inc.

5. The increase in domestic prices makes home exports less attractive and causes a current account

6. An increase in the world interest rate leads to a fall in a central bank’s holdings of foreign reserves as

domestic residents trade in their cash for foreign bonds. This leads to a decline in the home country’s

7. Capital account restrictions insulate the domestic interest rate from the world interest rate. Monetary

8. We are given that the growth rate in GDP may be computed as g = (GDPt + 1 − GDPt)/GDPt. Solving

for GDP in time t + 1 yields: GDPt + 1 = GDPt(1 + g). Using this expression alongside that derived

for IIPt + 1 allows us to compute:

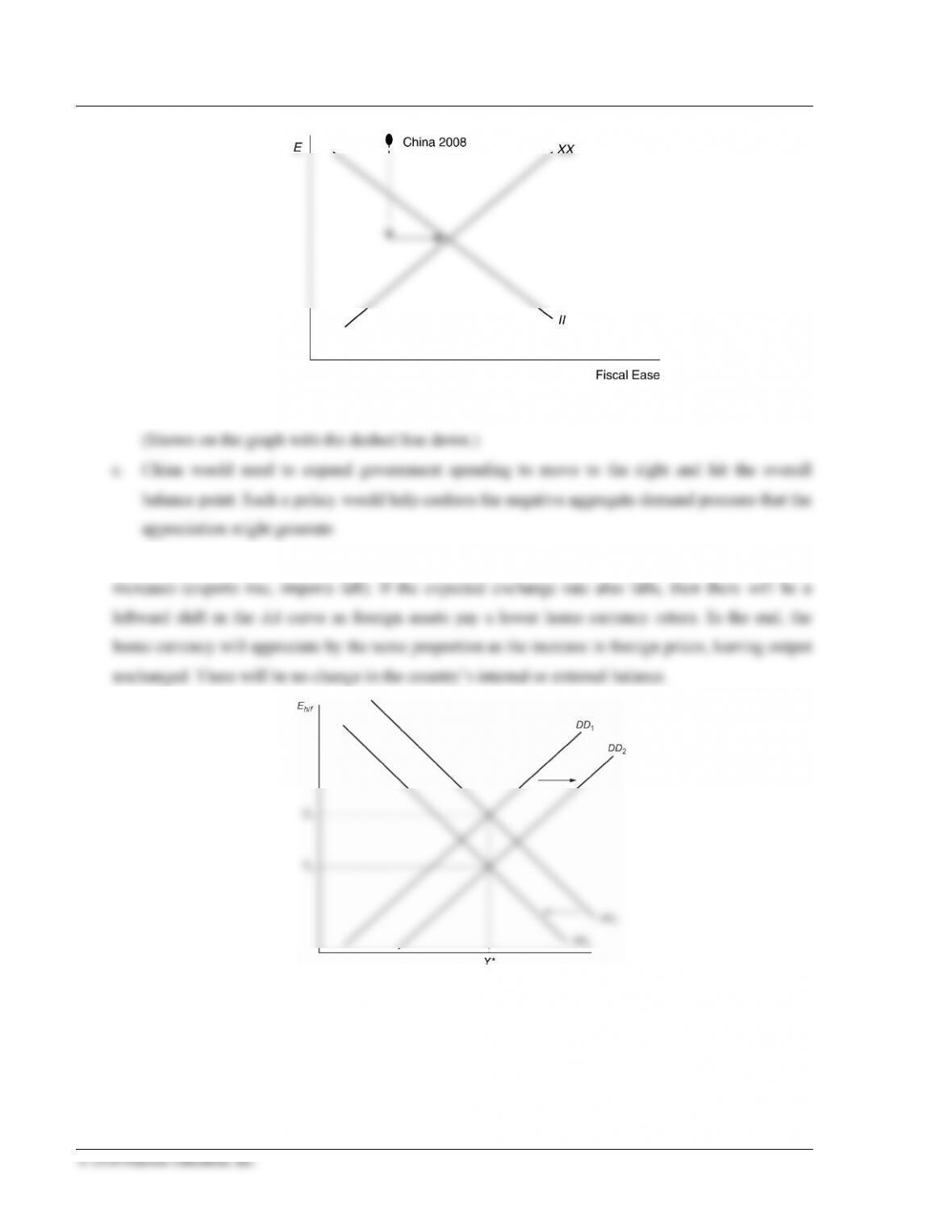

9. a. We know that China has a very large current-account surplus, placing them high above the XX

line. They also have moderate inflationary pressures (described as “gathering” in the question,

implying they are not yet very strong). This suggests that China is above the II line but not too far

148 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

b. China needs to appreciate the exchange rate to move down on the graph toward the balance.

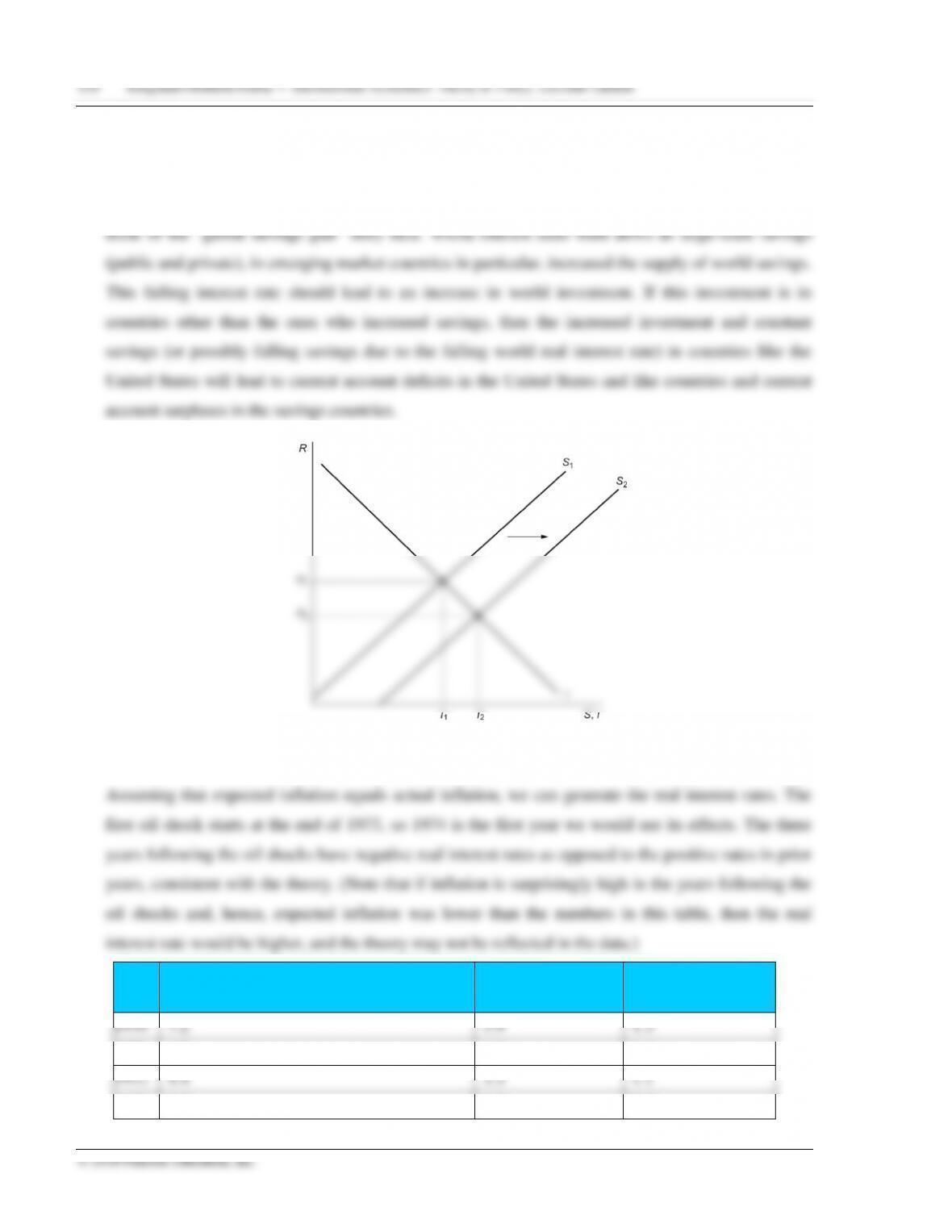

10. The increase in foreign prices will shift the DD curve out to the right as demand for home products

Chapter 19 International Monetary Systems: An Historical Overview 151

1974

10.5

11.0

−0.5

1975

5.8

9.1

−3.1

1976

5.1

5.7

−0.6

15. If other central banks sell dollars for euros, then it is equivalent to a sterilized sale of dollars because

neither the United States nor any other central bank’s asset side of the balance sheet has changed.

16. Students may find navigating the Australian Bureau of Statistics website challenging, given the large

volume of information available on this site. That said, once the data has been collected, the solution

to this problem is fairly straightforward.