Chapter 16

Price Levels and the Exchange Rate

in the Long Run

■ Chapter Organization

The Law of One Price.

Purchasing Power Parity.

The Relationship between PPP and the Law of One Price.

Absolute PPP and Relative PPP.

A Long-Run Exchange Rate Model Based on PPP.

The Fundamental Equation of the Monetary Approach.

Ongoing Inflation, Interest Parity, and PPP.

The Fisher Effect.

Empirical Evidence on PPP and the Law of One Price.

Explaining the Problems with PPP.

Trade Barriers and Nontradables.

Departures from Free Competition.

Differences in Consumption Patterns and Price Level Measurement.

Box: Some Meaty Evidence on the Law of One Price.

PPP in the Short Run and in the Long Run.

Case Study: Why Price Levels Are Lower in Poorer Countries.

Chapter 16 Price Levels and the Exchange Rate in the Long Run 111

The Real Exchange Rate.

Demand, Supply, and the Long-Run Real Exchange Rate.

Box: Sticky Prices and the Law of One Price: Evidence from Scandinavian Duty-Free Shops

Nominal and Real Exchange Rates in Long-Run Equilibrium.

International Interest Rate Differences and the Real Exchange Rate.

Real Interest Parity.

Summary

APPENDIX TO CHAPTER 16: The Fisher Effect, the Interest Rate, and the Exchange Rate under the

Flexible-Price Monetary Approach

112 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

■ Chapter Overview

The time frame of the analysis of exchange rate determination shifts to the long run in this chapter. An

analysis of the determination of the long-run exchange rate is required for the completion of the short-run

exchange rate model because, as demonstrated in the previous two chapters, the long-run expected

exchange rate affects the current spot rate. Issues addressed here include both monetary and real-side

determinants of the long-run real exchange rate. The development of the model of the long-run exchange

rate touches on a number of issues, including the effect of ongoing inflation on the exchange rate, the

Fisher effect, and the role of tradables and nontradables. Empirical issues, such as the breakdown of

purchasing power parity in the 1970s and the correlation between price levels and per capita income, are

addressed within this framework.

The law of one price, which holds that the prices of goods are the same in all countries in the absence of

transport costs or trade restrictions, presents an intuitively appealing introduction to long-run exchange

rate determination. An extension of this law to sets of goods motivates the proposition of absolute

purchasing power parity. Relative purchasing power parity, a less restrictive proposition, relates changes

in exchange rates to changes in relative price levels and may be valid even when absolute PPP is not.

Purchasing power parity provides a cornerstone of the monetary approach to the exchange rate, which

serves as the first model of the long-run exchange rate developed in this chapter. This first model also

demonstrates how ongoing inflation affects the long-run exchange rate.

The monetary approach to the exchange rate uses PPP to model the exchange rate as the price level in the

home country relative to the price level in the foreign country. The money market equilibrium relationship

is used to substitute money supply divided by money demand for the price level. The resulting relationship

models the long-run exchange rate as a function of relative money supplies, real interest rates, and relative

output in the two countries:

Eh/f = Ph/Pf = Mh/Mf × {L(Rf,Yf)/L(Rh,Yh)}

One result from this model that students may find initially confusing concerns the relationship between the

long-run exchange rate and the nominal interest rate. The model in this chapter provides an example of an

increase in the interest rate associated with exchange rate depreciation. In contrast, the short-run analysis

in the previous chapter provides an example of an increase in the domestic interest rate associated with an

appreciation of the currency. These different relationships between the exchange rate and the interest rate

reflect different causes for the rise in the interest rate as well as different assumptions concerning price

rigidity. In the analysis of the previous chapter, the interest rate rises due to a contraction in the level of the

Chapter 16 Price Levels and the Exchange Rate in the Long Run 113

nominal money supply. With fixed prices, this contraction of nominal balances is matched by a contraction

in real balances. Excess money demand is resolved through a rise in interest rates, which is associated with

an appreciation of the currency to satisfy interest parity. In this chapter, the discussion of the Fisher effect

demonstrates that the interest rate will rise in response to an anticipated increase in expected inflation due

to an anticipated increase in the rate of growth of the money supply. There is incipient excess money

supply with this rise in the interest rate. With perfectly flexible prices, the money market clears through an

erosion of real balances due to an increase in the price level. This price level increase implies, through

PPP, a depreciation of the exchange rate. Thus, with perfectly flexible prices (and its corollary PPP), an

increase in the interest rate due to an increase in expected inflation is associated with a depreciation of the

currency.

Empirical evidence presented in the chapter suggests that both absolute and relative PPP perform poorly

for the period since 1971. Even the law of one price fails to hold across disaggregated commodity groups.

The rejection of these theories is related to trade impediments (which help give rise to nontraded goods

and services), to shifts in relative output prices, and to imperfectly competitive markets. Because PPP

serves as a cornerstone for the monetary approach, its rejection suggests that a convincing explanation of

the long-run behavior of exchange rates must go beyond the doctrine of purchasing power parity. The

Fisher effect is discussed in more detail and accompanied by a diagrammatic exposition in an appendix to

this chapter.

A more general model of the long-run behavior of exchange rates in which real side effects are assigned a

role concludes the chapter. The material in this section drops the assumption of a constant real exchange

rate, an assumption that you may want to demonstrate to students is necessarily associated with the

assumption of PPP. Motivating this more general approach is easily done by presenting students with a

time-series graph of the recent behavior of the real exchange rate of the dollar, which will demonstrate

large swings in its value. The real exchange rate, qh/f, is the ratio of the foreign price index, expressed in

domestic currency, to the domestic price index or, equivalently, Eh/f = qh/f × (Ph/Pf). The chapter includes

an informal discussion of the manner in which the long-run real exchange rate, qh/f, is affected by

permanent changes in the supply or demand for a country’s products.

■ Answers to Textbook Problems

1. Relative PPP predicts that inflation differentials are matched by changes in the exchange rate. Under

Chapter 16 Price Levels and the Exchange Rate in the Long Run 115

© 2018 Pearson Education, Inc.

An increase in oil prices increases the incomes received by British oil exporters, raising their demand

for goods. The supply response of labor moving into the oil sector is comparable to an increase in

productivity, which also causes the real exchange rate to appreciate. Of course, a fall in the price of

oil has opposite effects. (Oil is not the only factor behind the behavior of the pound’s real exchange

rate. Instructors may wish to mention the influence of Prime Minister Margaret Thatcher’s stringent

monetary policies.)

6. A permanent shift in the real money demand function will alter the long-run equilibrium nominal

exchange rate but not the long-run equilibrium real exchange rate. Because the real exchange rate

does not change, we can use the monetary approach equation, E = (M/M*) × {L(R*, Y*)/L(R, Y)}. A

permanent increase in money demand at any nominal interest rate leads to a proportional appreciation

7. The mechanism would work through expenditure effects with a permanent transfer from Poland to

the Czech Republic appreciating the koruna (Czech currency) in real terms against the zloty (Polish

8. As discussed in the answer to Question 7, the koruna appreciates against the zloty in real terms with

the transfer from Poland to the Czech Republic if the Czechs spend a higher proportion of their

9. Because the tariff shifts demand away from foreign exports and toward domestic goods, there is a

10. The balanced expansion in domestic spending will increase the amount of imports consumed in the

country that has a tariff in place, but imports cannot rise in the country that has a quota in place.

11. A permanent increase in the expected rate of real depreciation of the dollar against the euro leads to a

permanent increase in the expected rate of depreciation of the nominal dollar/euro exchange rate,

116 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

© 2018 Pearson Education, Inc.

given the differential in expected inflation rates across the United States and Europe. This increase in

the expected depreciation of the dollar causes the spot rate today to depreciate.

12. Suppose there is a temporary fall in the real exchange rate in an economy, that is, the exchange rate

appreciates today and then will depreciate back to its original level in the future. The expected

13. International differences in expected real interest rates reflect expected changes in real exchange

rates. If the expected real interest rate in the United States is 9% and the expected real interest rate in

14. The initial effect of a reduction in the money supply in a model with sticky prices is an increase in the

nominal interest rate and an appreciation of the nominal exchange rate. The real interest rate, which

15. One answer to this question involves the comparison of a sticky-price with a flexible-price model. In

a model with sticky prices, a reduction in the money supply causes the nominal interest rate to rise

and, by the interest parity relationship, the nominal exchange rate to appreciate. The real interest rate,

Chapter 16 Price Levels and the Exchange Rate in the Long Run 117

© 2018 Pearson Education, Inc.

real interest rate remains unchanged) and the currency to depreciate because excess money supply is

resolved through an increase in the price level and thus, by PPP, a depreciation of the currency.

An alternative approach is to consider a model with perfectly flexible prices. As discussed in the

preceding paragraph, an increase in expected inflation causes the nominal interest rate to increase and

the currency to depreciate, leaving the expected real interest rate unchanged. If there is an increase in

the expected real interest rate, however, this implies an expected depreciation of the real exchange

rate. If this expected depreciation is due to a current, temporary appreciation, then the nominal

exchange rate may appreciate if the effect of the current appreciation (which rotates the exchange rate

schedule downward) dominates the effect due to the expected depreciation (which rotates the

exchange rate schedule upward).

16. If long-term rates are higher than short-term rates, it suggests that investors expect interest rates to be

17. If we assume that the real exchange rate is constant, then the expected percentage change in the

exchange rate is simply the inflation differential. As the question notes, this relationship holds better

18. If markets are fairly segmented, then temporary moves in exchange rates may lead to wide deviations

19. Recall the definition of the real exchange rate as q$/€ = (E$/€ × PEU)/PUS. According to the problem,

118 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

Goods that are consumed by Americans more than by Europeans are becoming more expensive, thus

raising the general cost of living in the United States more than in Europe. As a result, the real

exchange rate will fall, representing a real appreciation of the dollar.

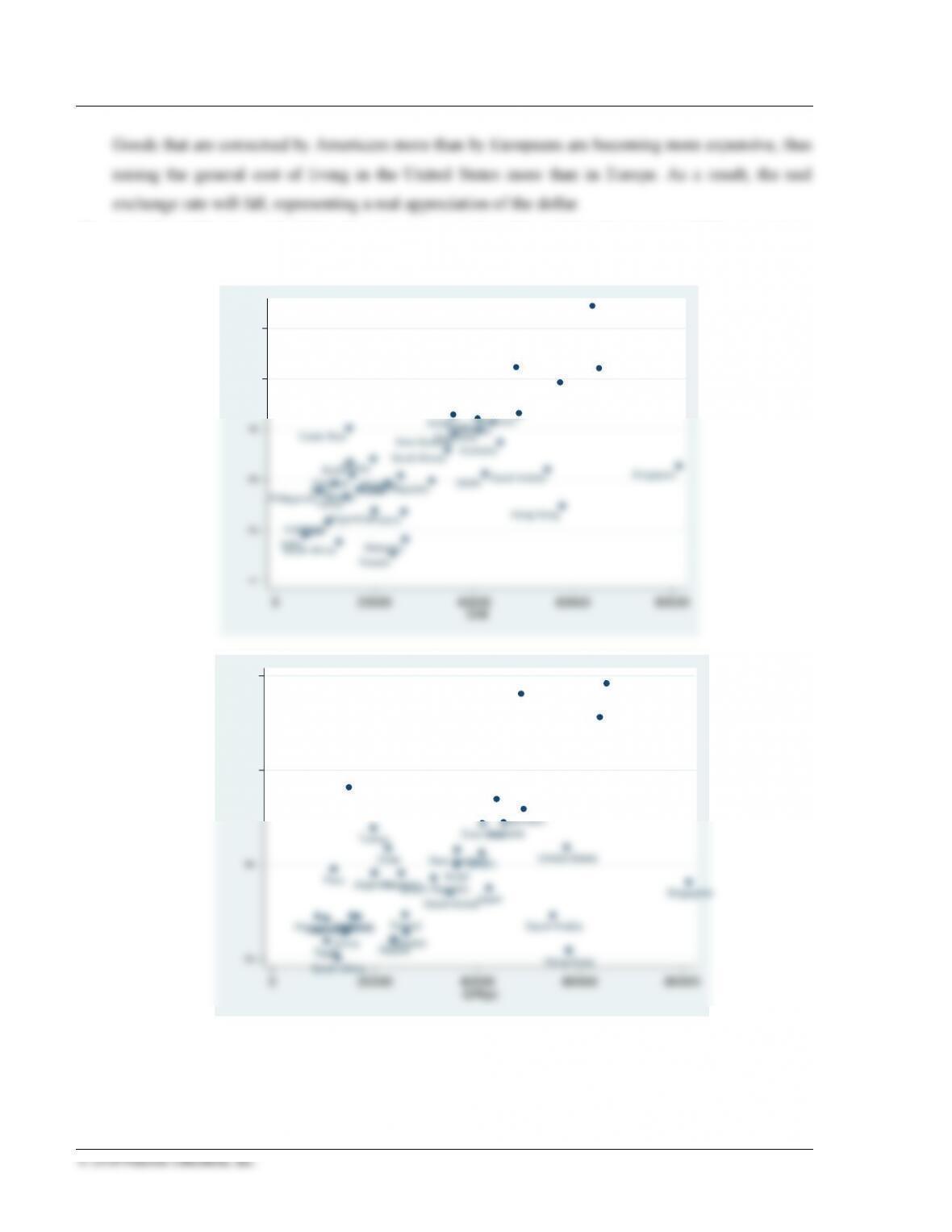

20. As indicated by the graph below, there is a strong and positive relationship between GNI per capita in

a country and the dollar price of a Big Mac:

Argentina

Australia

Brazil

Britain

Canada

Chile

China

Costa Rica

Czech Republic

Denmark

Egypt

Euro area

Hong Kong

Hungary

India

Indonesia

Israel

Japan

Malaysia

Mexico

New Zealand

Norway

Peru

Philippines

Poland

Russia

Saudi Arabia Singapore

South Africa

South Korea

Sweden

Switzerland

Thailand

Turkey

United States

123456

Price

0 20000 40000 60000 80000

GNI

Argentina

Australia

Brazil

Britain

Canada

Chile

China

Czech Republic

Denmark

Egypt

Euro area

Hong Kong

Hungary

Indonesia

Israel

Japan

Malaysia

Mexico

New Zealand

Norway

Peru

Philippines Poland

Russia

Saudi Arabia

Singapore

South Africa

South Korea

Sweden

Switzerland

Thailand

Turkey

United States

2468

Price

0 20000 40000 60000 80000

GNIpc