Chapter 15

Money, Interest Rates, and Exchange Rates

■ Chapter Organization

Money Defined: A Brief Review.

Money as a Medium of Exchange.

Money as a Unit of Account.

Money as a Store of Value.

What Is Money?

How the Money Supply Is Determined.

The Demand for Money by Individuals.

Expected Return.

Risk.

Liquidity.

Aggregate Money Demand.

The Equilibrium Interest Rate: The Interaction of Money Supply and Demand.

Equilibrium in the Money Market.

Interest Rates and the Money Supply.

Output and the Interest Rate.

The Money Supply and the Exchange Rate in the Short Run.

Linking Money, the Interest Rate, and the Exchange Rate.

U.S. Money Supply and the Dollar/Euro Exchange Rate.

Chapter 15 Money, Interest Rates, and Exchange Rates 101

Europe’s Money Supply and the Dollar/Euro Exchange Rate.

Money, the Price Level, and the Exchange Rate in the Long Run.

Money and Money Prices.

The Long-Run Effects of Money Supply Changes.

Empirical Evidence on Money Supplies and Price Levels.

Money and the Exchange Rate in the Long Run.

Inflation and Exchange Rate Dynamics.

Short-Run Price Rigidity versus Long-Run Price Flexibility.

Box: Money Supply Growth and Hyperinflation in Zimbabwe.

Permanent Money Supply Changes and the Exchange Rate.

Exchange Rate Overshooting.

Case Study: Can Higher Inflation Lead to Currency Appreciation? The Implications of Inflation

Targeting.

Summary

■ Chapter Overview

This chapter combines the foreign-exchange market model of the previous chapter with an analysis of the

demand for and supply of money to provide a more complete analysis of exchange rate determination in

the short run. The chapter also introduces the concept of the long-run neutrality of money, which allows an

examination of exchange rate dynamics. These elements are brought together at the end of the chapter in a

model of exchange rate overshooting.

The chapter begins by reviewing the roles played by money. Money supply is determined by the central

bank; for a given price level, the central bank’s choice of a nominal money supply determines the real

money supply. An aggregate demand function for real money balances is motivated and presented.

Money-market equilibrium—the equality of real money demand and the supply of real money balances—

determines the equilibrium interest rate.

A familiar diagram portraying money-market equilibrium is combined with the interest rate parity diagram

presented in the previous chapter to give a simple model of monetary influences on exchange rate

determination. The domestic interest rate, determined in the domestic money market, affects the exchange

102 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

rate through the interest parity mechanism. Thus, an increase in domestic money supply leads to a fall in

the domestic interest rate. The home currency depreciates until its expected future appreciation is large

enough to equate expected returns on interest-bearing assets denominated in domestic currency and in

foreign currency. A contraction in the money supply leads to an exchange rate appreciation through a

similar argument. Throughout this part of the chapter, the expected future exchange rate is still regarded as

fixed.

The analysis is then extended to incorporate the dynamics of long-run adjustment to monetary changes.

The long run is defined as the equilibrium that would be maintained after all wages and prices fully

adjusted to their market-clearing levels. Thus, the long-run analysis is based on the long-run neutrality of

money: All else being equal, a permanent increase in the money supply affects only the general price

level—and not interest rates, relative prices, or real output—in the long run. Money prices, including,

importantly, the money prices of foreign currencies, move in the long run in proportion to any change in

the money supply’s level. Thus, an increase in the money supply, for example, ultimately results in a

proportional exchange rate depreciation. The link between money supply growth, inflation, and exchange

rates is highlighted with a case study on the recent hyperinflation in Zimbabwe. Rampant money supply

growth led to prices in Zimbabwe doubling nearly every day at the peak of the hyperinflation and only

ended when Zimbabwe legalized the use of foreign currencies for domestic transactions.

The combination of these long-run effects with the short-run static model allows consideration of

exchange rate dynamics. In particular, the long-run results are suggestive of how long-run exchange rate

expectations change after permanent money-supply changes. One dynamic result that emerges from this

model is exchange rate overshooting in response to a change in the money supply. For example, a

permanent money-supply expansion leads to expectations of a proportional long-run currency

depreciation. Foreign-exchange market equilibrium requires an initial depreciation of the currency large

enough to equate expected returns on foreign and domestic bonds. But because the domestic interest rate

falls in the short run, the currency must actually depreciate beyond (and thus overshoot) its new expected

long-run level in the short run to maintain interest parity. As domestic prices rise and M/P falls, the

interest rate returns to its previous level and the exchange rate falls (appreciates) back to its long-run level,

higher than the starting point, but not as high as the initial reaction.

The chapter concludes with a useful case study that helps bridge the gap between the stylized world of the

model and the real world of central bank policy making where the central bank sets the interest rate rather

than money and news about inflation may change expectations about future money supply changes when

the central bank has committed to a particular level of inflation.

Chapter 15 Money, Interest Rates, and Exchange Rates 103

■ Answers to Textbook Problems

1. A reduction in the home money demand causes interest rates in the home country to fall from Rh,1 to

2. A fall in a country’s population would reduce money demand, all else being equal, because a smaller

population would undertake fewer transactions and thus demand less money. This effect would

3. Equation 15-4 is Ms./P = L(R, Y). The velocity of money, V = Y/(M/P). Thus, when there is

equilibrium in the money market such that money demand equals money supply, V = Y/L(R, Y).

104 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

© 2018 Pearson Education, Inc.

amount (because the elasticity of aggregate money demand with respect to real output is less than

one), and the fraction Y/L(R, Y) rises. Thus, velocity rises with either an increase in the interest rate or

an increase in income. Because an increase in interest rates as well as an increase in income causes

the exchange rate to appreciate, an increase in velocity is associated with an appreciation of the

exchange rate.

4. An increase in domestic real GNP will cause domestic real money demand to rise. This will cause

domestic real interest rates to rise from Rh,1 to Rh,2 (see graph below). With no change in

5. Just as money simplifies economic calculations within a country, use of a vehicle currency for

6. Currency reforms are often instituted in conjunction with other policies that attempt to bring down

106 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

© 2018 Pearson Education, Inc.

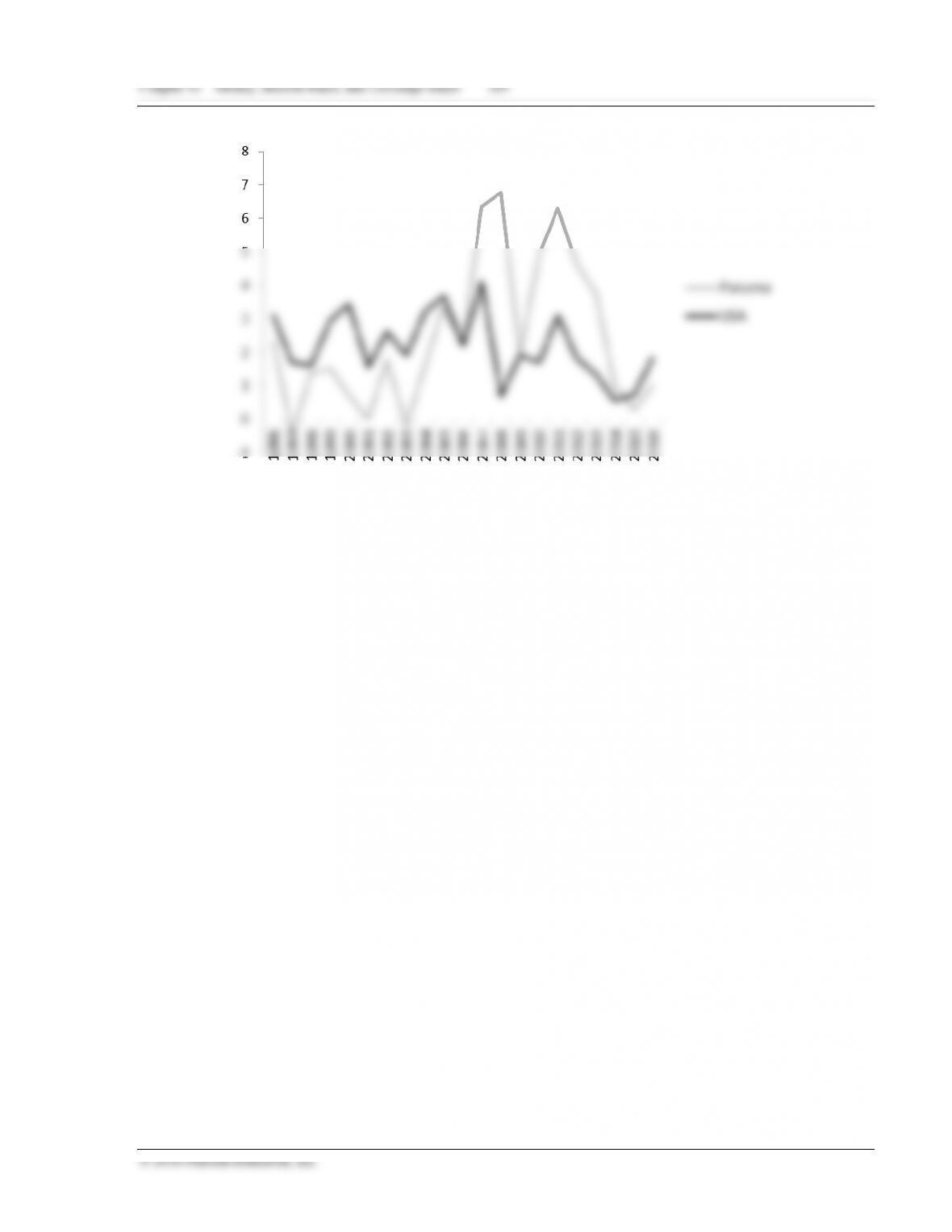

8. The chart below gives inflation rates since 1980 for New Zealand, Chile, Canada, and Israel:

9. If an increase in the money supply induces an increase in real output in the short run, then the

short-run decrease in the real interest rate will not be as pronounced as it was without the increase

in real output. In the diagram below, the money supply rises from Ms.,1 to Ms.,2. This causes real

Chapter 15 Money, Interest Rates, and Exchange Rates 107

© 2018 Pearson Education, Inc.

This shifts the expected return on foreign assets from

,1

e

f

R

to

,2 .

e

f

R

As a result of these shifts, the

home currency depreciates from E1 to E2. However, the drop in the value of the home currency is

not as severe as it would have been had output not increased (thus limiting the decrease in interest

rates).

10. As the interest rate falls, people prefer to hold more cash and fewer financial assets. If interest rates

11. One clear complication that a zero interest rate introduces is that the central bank is “out of

ammunition.” It literally cannot reduce interest rates any further and thus may struggle to respond to

108 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Eleventh Edition

© 2018 Pearson Education, Inc.

not operational. As further discussion in Chapter 17 will show, a zero interest rate may also be a

symptom of a lack of responsiveness in the economy to low interest rates.

12. a. If money adjusts automatically to changes in the price level, then any number of combinations of

b. Yes, a rule such as this one would help anchor the price level and imply there is no longer an

c. A one-time permanent unexpected fall in “u” would imply that R would have to fall until prices

have a chance to rise and balance out the equation. As prices rise, R would return to its initial

13. Because Panama uses the US dollar as its currency, we would expect that, all else being equal,

inflation in Panama and that in the United States should be identical. The chart below gives inflation