P6-29A Accounting for inventory using the perpetual inventory system—FIFO, LIFO, and

weighted-average, and comparing FIFO, LIFO, and weighted-average

Learning Objectives 2, 3

5. FIFO GP $5,235

Steel Mill began August with 50 units of iron inventory that cost $35 each. During August, the company

completed the following inventory transactions:

Units Unit Cost Unit Sales

Price

Aug. 3 Sale 45 $ 85

8 Purchase 90 $ 54

21 Sale 85 88

30 Purchase 15 58

Requirements

1. Prepare a perpetual inventory record for the merchandise inventory using the FIFO inventory costing

method.

2. Prepare a perpetual inventory record for the merchandise inventory using the LIFO inventory costing

method.

3. Prepare a perpetual inventory record for the merchandise inventory using the weighted-average

inventory costing method.

4. Determine the company’s cost of goods sold for August using FIFO, LIFO, and weighted-average

inventory costing methods.

5. Compute gross profit for August using FIFO, LIFO, and weighted-average inventory costing

methods.

6. If the business wanted to maximize gross profit, which method would it select?

SOLUTION

Requirement 1

P6-29A, cont.

Requirement 2

P6-29A, cont.

Requirement 3

P6-29A, cont.

Requirement 4

Requirement 5

Requirement 6

P6-30A Accounting principles for inventory and applying the lower-of-cost- or-market rule

Learning Objectives 1, 4

Some of M and C Electronics’s merchandise is gathering dust. It is now December 31, 2018, and the

current replacement cost of the ending merchandise inventory is $24,000 below the business’s cost of

the goods, which was $97,000. Before any adjustments at the end of the period, the company’s Cost of

Goods Sold account has a balance of $380,000.

Requirements

1. Journalize any required entries.

2. At what amount should the company report merchandise inventory on the balance sheet?

3. At what amount should the company report cost of goods sold on the income statement?

4. Which accounting principle or concept is most relevant to this situation?

SOLUTION

Requirement 1

P6-31A Correcting inventory errors over a three-year period and computing inventory turnover and days’ sales in inventory

Learning Objectives 5, 6

2. 2019, overstated $9,000

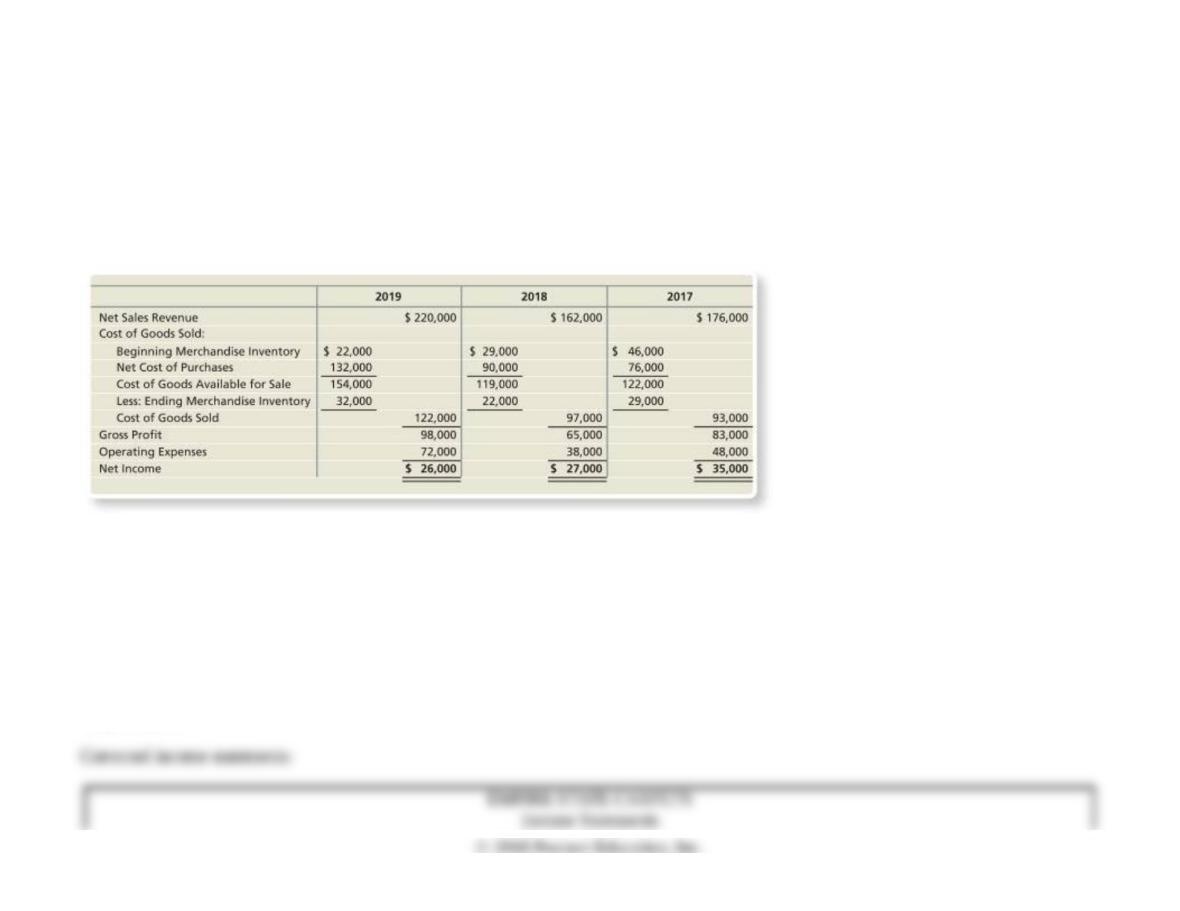

Empire State Carpets’s books show the following data. In early 2020, auditors found that the ending merchandise inventory for 2017 was

understated by $8,000 and that the ending merchandise inventory for 2019 was overstated by $9,000. The ending merchandise inventory at

December 31, 2018, was correct.

Requirements

1. Prepare corrected income statements for the three years.

2. State whether each year’s net income—before your corrections—is understated or overstated, and indicate the amount of the

understatement or overstatement.

3. Compute the inventory turnover and days’ sales in inventory using the corrected income statements for the three years. (Round all

numbers to two decimals.)

SOLUTION

Requirement 1

P6-31A, cont.

Requirement 2

Requirement 3

P6-31A, cont.

Requirement 3, cont.