Solutions to Problems

P9-1 Concept of cost of capital (LG 1; Basic)

a. Project North is expected to earn an 8% return. If the analyst expects the cost of debt to be 7%,

she will recommend accepting the project because the expected return exceeds financing cost.

b. Project South is expected to earn 15%, but financing (retained earnings) costs 16%. So, the

analyst will recommend rejecting the project because financing cost exceeds expected return.

c. These decisions may not enhance shareholder wealth because the firm finances investments

e. If the hurdle rate for both projects were 12.4%, the first analyst would recommend rejecting

project North, and the second analyst would recommend accepting Project South.

f. The proper “hurdle rate” will reflect the weights associated with the target capital structure. The

cost of equity is considerably higher than the cost of debt while the weighted average cost of

P9-2 Cost of debt using both methods (LG 3; Intermediate)

a. Net proceeds: Nd Par value – floatation costs = $1,010 $30 = Nd $980.

b

.Cash flows: Years (n) Cash Flows Type of Cash Flow

0 $ 980 Net Proceeds

The interest rate () that makes this equation true is the before-tax cost of debt. In Excel, RATE

is the command for finding the before-tax cost of debt. The proper syntax is:

[Note: Net proceeds enters as a negative number.] After-tax cost = rd (1 – T), where T is the

d. The approximate before-tax cost of debt, rd, (from equation 9.1 on page 404 of the text) is:

where:

After-tax cost is = rd (1 – T), where T is the firm’s tax rate. As noted, some versions of the text

e. Using Excel or a calculator will yield a more precise answer in fewer steps. But the

approximation formula is fairly accurate in the absence of a financial calculator or laptop.

P9-3 Before-tax cost of debt and after-tax cost of debt (LG 3; Easy)

a. Before-tax cost of debt:

The monthly interest rate () that makes this equation true is the before-tax cost of debt. In

Excel, the RATE command computes . The proper syntax is:

P9-4 Cost of debt using the approximation formula (LG 3; Basic)

After-tax cost of debt rd (1T)

where:

Bond A

9.44% (10.21) 7.46%

Bond B

Bond D

After-tax cost of debt:

Bond E

Bond C

After-tax cost of debt:

P9-5 The cost of debt (LG 3; Intermediate)

In Excel, the RATE command will generate the before-tax interest rate (rd) with the following

syntax: =rate(years, coupon in dollars, -net proceeds, par value). For bond sales, net proceeds = Par

value + Premium (Discount) – Flotation costs. For Alternative A, net proceeds = $1,000 + $250 –

P9-6 After-tax cost of debt (LG 3; Intermediate)

a. The after-tax cost of borrowing from the motorcycle dealer is the same as the pretax cost, 5%.

c. The mortgage loan would cost less after taxes compared to the loan from the dealer.

d. If Bella borrows against her home to buy the motorcycle, she risks foreclosure if she cannot

P9-7 Cost of preferred stock (LG 4; Basic)

The cost of preferred stock is given by rp Dp Np, where Dp is annual preferred dividends (in

dollars) and Np is net proceeds from issuing preferred stock.

a. Np = Sales price – Flotation costs = $99.50 – $1.50 = $98. Given an 8% annual dividend ($8),

P9-8 Cost of preferred stock (LG 4; Basic)

dollars) and Np is net proceeds from issuing preferred stock.

P9-9 Cost of common stock equity: CAPM (LG 5; Intermediate)

According to CAPM, the required return on asset j is given by RF [j(rm RF)], where

j is the

beta for asset j, RF is the risk-free rate, and rm is the expected return on the market portfolio.

c. The problem does not mention flotation costs, so the cost of common stock equity is simply the

P9-10 Cost of common stock equity (LG 5; Intermediate)

a. The RATE command in Excel will compute the dividend growth rate using n (years) = 5,

Note: There is no ongoing payment in this problem, so the second entry in the parentheses is

zero. In addition, as always with the rate function, present value enters as a negative number.

The growth rate can also be found by hand:

c. The required return on Ross stock can be found with Gordon model:

= + g

where:

D1 = Next annual dividend payment in dollars

d. The cost of new common stock for Ross (rn) can be found with:

= + g

where:

D1 = Next annual dividend payment in dollars

Nn = Net proceeds from issue of common stock

P9-11 Retained earnings versus new common stock (LG 5; Intermediate)

The cost of retained earnings is simply the required return on common stock (rs):

= + g

where:

D1 = Next annual dividend payment in dollars

where:

D1 = Next annual dividend payment in dollars

P9-12 Effect of tax rate on WACC (LG 3, LG 4, LG 5, and LG 6; Intermediate)

weight of debt in the firm’s capital structure, T is the firm’s tax rate, rd is the before-tax cost of

debt, wp the weight on preferred stock, rp the cost of preferred stock, ws the weight on common

c. And a tax rate of 25%, rwacc = (0.40)(0.06)(1 0.25) (0.10)(0.08) (0.50)(0.10) = 7.60%.

d. The weighted-average cost of capital rises as the tax rate falls. The deductibility of interest

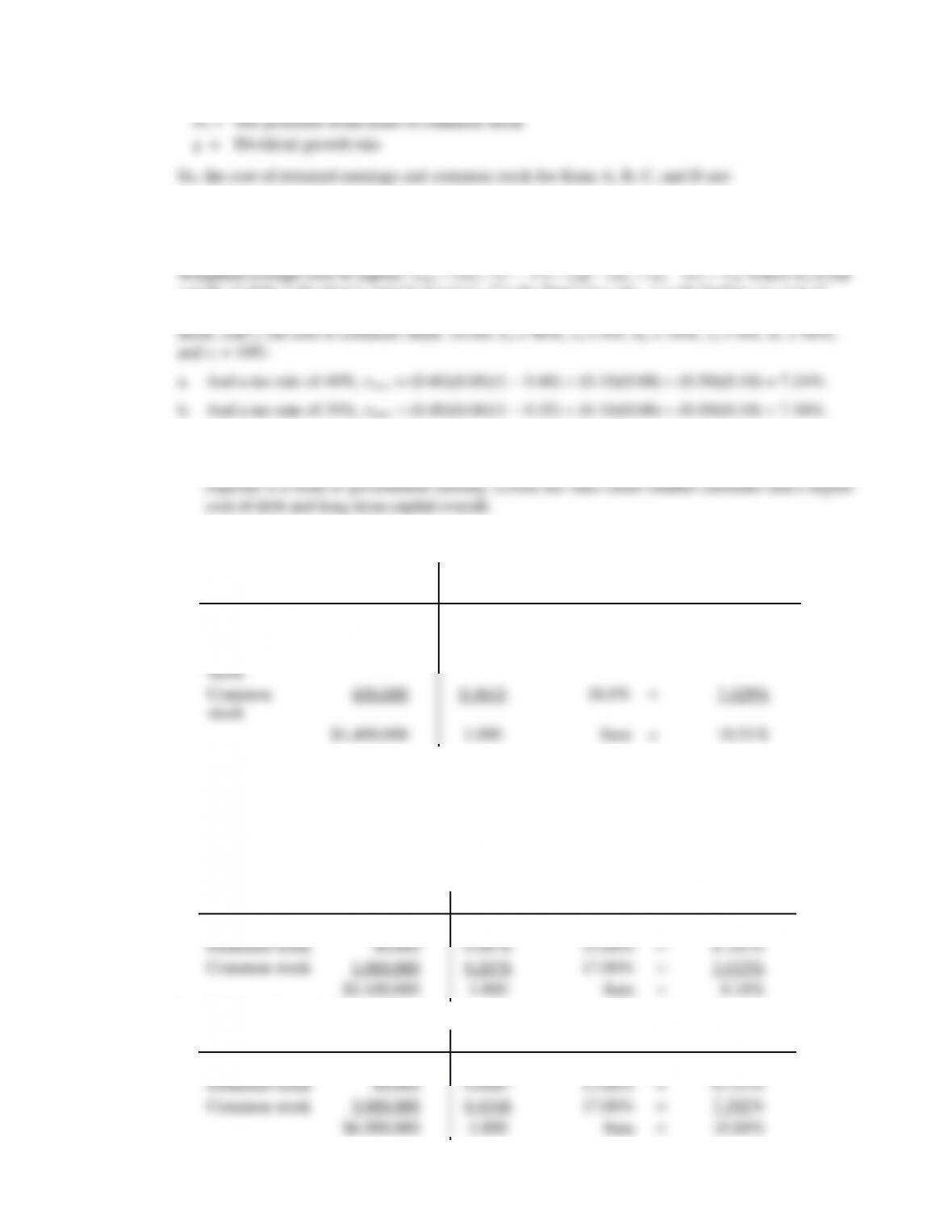

P9-13 WACC: Market value weights (LG 6; Basic)

a. Type of

Capital Market Value Weight Cost = Weighted Cost

Long-term

debt $700,000 0.5000 5.3% = 2.650%

Preferred

b. The WACC is the “hurdle rate” to use in calculating the net present value of investment

projects. Any project with an expected return exceeding the WACC will enhance the value of

the firm.

P9-14 WACC: Book weights and market weights (LG 6; Intermediate)

a. Book value weights:

Type of Capital Book Value Weight Cost = Weighted Cost

Long-term debt $4,000,000 0.7843 6.00% = 4.706%

b. Market value weights:

Type of Capital Market Value Weight Cost = Weighted Cost

Long-term debt $3,840,000 0.5565 6.00% = 3.339%

c. The cost of capital is higher when market values are used to determine the cost of each source

of long-term finance because preferred and common stock—which cost more than debt—

receive higher weights. Specifically, the market value of preferred stock is 50% greater than

P9-15 Weighted average cost of capital and target weights (LG 6; Intermediate)

a. Weighted average cost of capital (rWACC) with historical market weights:

c. Weighted average cost of capital is lower in part (b) because more weight is placed on cheaper

sources of capital (debt and preferred stock) and less on the costliest source (common stock).

P9-16 Cost of capital (LG 3, LG 4, LG 5, and LG 6; Challenge)

a. Cost of retained earnings: The price of Edna stock (P0) is $40. Expected dividend growth (g) is

b. Cost of new common stock: The cost of new common stock (rn) is given by (D1 Nn) + g, where

Nn is net proceeds from the sale of new common stock. Flotation costs are given as $7 per

c. Cost of preferred stock: The cost of new preferred stock (rp) is given by (Dp Np), where Dp is

the expected perpetual annual dividend on preferred stock, and Np is net proceeds from the sale

d. Cost of debt: Net proceeds = Par value ($1,000) + Premium ($200) – Flotation costs ($25) =

text:

r

d

=

I

+

$1,000

–

N

d

n

N

d

+

$1,000

2

where:

rd = Approximate yield to maturity

I = Annual interest in dollars ($100)

Nd = Net proceeds from bond sale ($1,175)

5.98% (1 – 0.40) = 3.59%; with a 21% tax rate, the after-tax cost is 4.72%.

e. If retained earnings supply the needed equity, and the tax rate is 40%, the weighted average

cost of capital (rWACC) is:

With a 21% tax rate, the weighted after-tax cost of debt (column 3) is 1.889% instead of

If the firm sells common stock, and the tax rate is 40% tax rate, rWACC is:

P9-17 Calculation of individual costs and WACC (LG 3, LG 4, LG 5, and LG 6; Challenge)

a. Cost of debt: Net proceeds from the bond sale = Par value + Premium – Flotation costs.

In Excel, rd can be found with the RATE function; proper syntax is =rate(10,70,-990,1000).

[Note: Net proceeds from sale (third term in parentheses) must be entered as a negative

number.]

The after-tax cost of debt is rd (1 – T ), where T is the firm’s marginal tax rate. With a 40% tax

b. Cost of preferred stock: The cost of new preferred stock (rp) is given by (Dp Np), where Dp is

c. Cost of retained earnings: The price of Dillon common stock (P0) is $59.43. Over the past 10

years, dividends have growth from $2.70 to $4,00, a growth rate (g) = – 1 = 4.01%. Assuming

Cost of new common stock: The cost of new common stock (rn) is given by (D1 Nn) – g, where

Nn is the net proceeds from the sale of new stock. Flotation costs are $2 per share. Net proceeds

d. If retained earnings can be tapped for needed common equity, and the tax rate is 40%, rWACC is:

With a 21% tax rate, the weighted after-tax cost of debt (column 3) is 2.257% rather than